Also that is not worse time for company , because they were getting good orders from US at that time . Only Indian PEB is not doing good.

1 Like

That doesn’t make management bad. If your statement is taken than every US corporation has bad management. Every company that cut job has bad management. Whatever owner does with his own money should not be questioned but if you are saying he is using company’s money than we can question management.

5 Likes

Q4 FY24

Financials

- The diversified engineering revenue for FY '24 is at Rs. 1,641 crores compared to Rs. 1,511 crores, up by 8%. And similarly, for our custom design building solutions, it is up by 5.24%.

Business

- PEB orderbook at 750 crores and Ascent at 44 million dollars.the current PEB orderbook is meant for the next 6-8 months only and more revenue will come.

- TAM of PEB in india: 7000 to 8000 crores

- Other income includes the earnings that we have from deposits, income from mutual funds, incentives, exchange fluctuation and a large amount is due to the collection of our old receivables.

- Salaries have increased but expected to stay relatively flat or increase slightly

- Finance cost is high because of fuelling growth and being stuck in the wrong businesses which is causing working capital to extend. The impact due to interest rate is 73 basis points and due to higher working capital close to Rs. 142 crores. As a % of net sales the * finance cost is higher but they expect it to come down by the end of the year but moderately increase in the next 2 quarters.

- In terms of working capital, you have to compare the working capital as a percentage of the net sales. Our stated goal is that we will be at around 3.5% as a percentage of net sales which we will be.

- US business has a different taxation and works on state so it can vary a bit but blended we can assume 23-24%

- Peak revenue without the addition of asset base can be 5000 crores.

- To answer your question, the gross margins for our pre-engineered building business in India, margin after variable is about 18%. The market leaders get 28%, 30%. So, we are hard at work trying to get that up. In the U.S., we get a substantially larger number, it’s closer to 30%. And it can move higher than that as well.

- For PEB in the US, it is man driven and you need people called DMs. So if you are increasing capacity and aiming for growth: you hire more of them.Our total manpower in the U.S. right now is over 200 plus. The factory staff is 169 plus DMs, everyone and others combined engineering staff, all combined goes well over 200. But for us to grow, as I said, we are continually adding new DMs

Outlook and expansions

- PEB, both in India and in the U.S. will grow on the back of our new Raebareli plant having been commissioned.

- In the U.S., CAPEX is underway, and our order backlogs have also grown quite well. So, we expect to see substantial double-digit growth in revenue and profitability in this financial year from our U.S. business as well.

- So, for our products in the U.S. and services, we are currently at a 2% to 3% market share. So, there’s a lot of potential for us to grow. Consequently, we are adding a lot of capacity in the U.S. in terms of manpower, sales presence, DMs and also production capacity. This will create over the next few quarters or the next few years, our U.S. business is we probably expect it to be our fastest-growing business. And the margins there are obviously also a lot higher than our India business. So, we intend to focus on U.S. revenue and profitability in addition to our India businesses.

- After the plant, boiler revenue will double this year and it’s good because the PBT margins are around 5-7%. Moreover, the industry standard for margins is even higher at around 10% so they will catch up to that soon in a few years.

- We have a 5-year plan to, shall we say, make most of our businesses, the current size of the entirety of our business. So like 5x their revenue

- we have commissioned and commissioned plants and plant expansions in Hyderabad, in Raebareli, in Trichy, also in France, but that is a small number, it’s a few crores and also in the U.S. So, all of these are growth verticals.

- US PEB capacity which is to be doubled will happen this year

- PAT margins will reach 5% this year or next year and that means PBT of 7% or so.

- Expecting quarter on quarter improvement for the next few years

- US business can do 35 million per quarter but it all comes down to adding DMs and capacity.

my thoughts: Extremely bullish guidance. Will be interesting to see how it does. I had modeled by thesis with low double digit revenue growth but it can surely do mid- high teen growth.

Valuations provide good comfort lets see!

Worried about working capital being overly stretched though

11 Likes

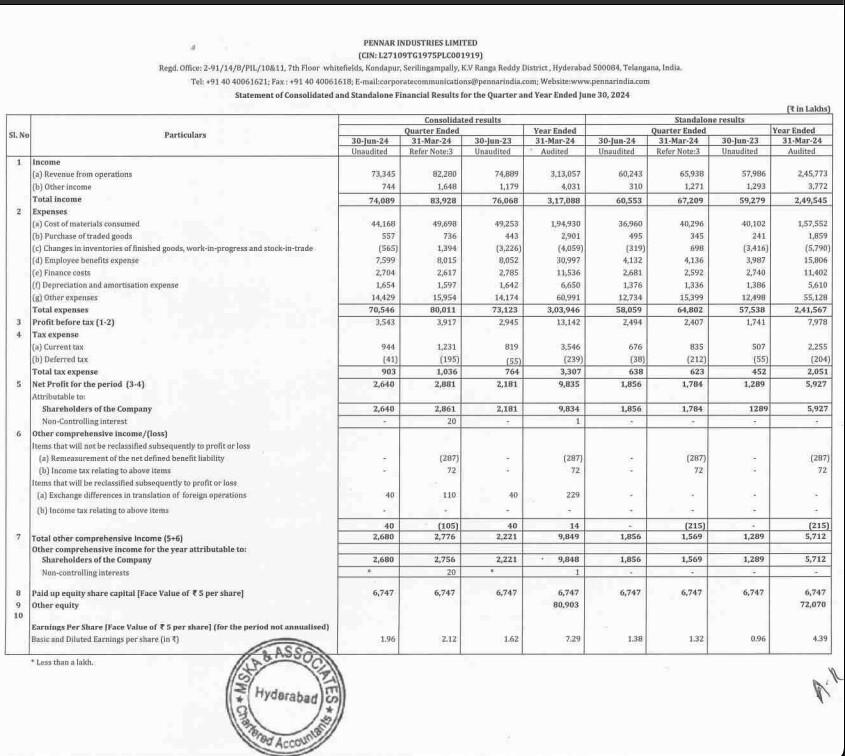

Pennar results

- Hiving of bad businesses.

- Margins seems to have increased

On track

Received new orders from Toyota Boshoku, Oriental Electrical, Jindal Steel, Power Mech Projects, Yamaha, Endurance, Elkart, Haldex, Ashok Leyland, IFB, Nuevosol, Saint Gobain, Thermax, ICF, KCC Buildcon, Oriental Wabtec, Shaurya Ispat, Aditya Balaji Rice Mill, FCA Motors etc

PEB India is Rs. 800+ Cr & PEB US is USD 52+ Mn.

7 Likes

Covers pennar and others PEB. Theme - PEB

4 Likes

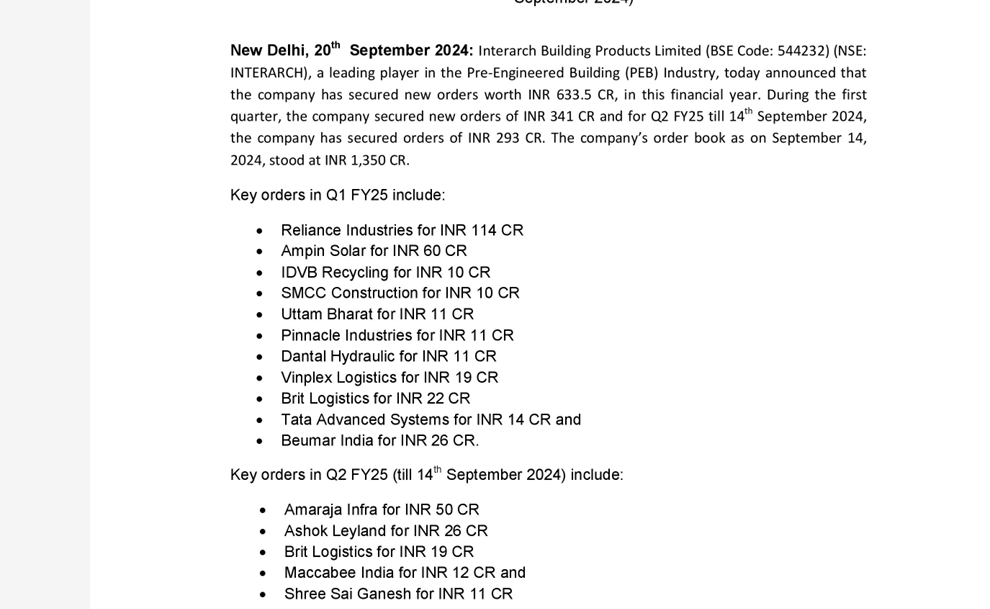

Interarch Building Products Ltd provides detailed report about their order booking, hopefully Pennar also follow the suit. It looks like Interarch IPO will have have positive impact on PEB companies with regard to transparency etc

5 Likes

Looks like one of the Promoter who is at Director Position is Selling. Found Info in Insider Trades on Screener where this Promoter has Sold in both August and September. Any Idea on this?

4 Likes

It’s Potluri Venkateswara Rao, he is been offloading since 2020, still holds more than 2,00,000 shares, which is 0.15% of the company, he offloaded around 27000 shares

6 Likes

Not able to Locate AGM Link or Transcript anywhere. Did any one attend it, can they share notes pls?

1 Like

Made a video some time back analysing Pennar industries…might be useful:)

Link- https://youtu.be/157veHw22J8?si=jUa37Mu6mkDDIFRI

16 Likes

Dhruv bhai…please make videos more interesting…please change the way…like divide the video in 5 parts…1 Brief history 2. What the company do 3. Revenue, ebidta, pat mix, 4. Growth drivers, capacity expantion, peer comparision etc… 5. Final conclusion…In this way video will be more interesting…

5 Likes

Pennar Industries Q2 FY25 Earnings Conference Call Summary

Financial Performance

- Pennar Industries Limited (PIL) reported a total income of Rs. 753.53 crores and a PBT of Rs. 36 crores for Q2 FY25. While revenue declined by around 8%, PBT grew by 20%.

- The decline in revenue was attributed to delays in the commissioning of the Raebareli plant and converting the US order book revenue due to the US election. These are considered temporary concerns.

- The company achieved high capacity utilization in PEB in October and saw a significant ramp-up in US revenue in the current quarter.

- PIL recorded a cash PAT of Rs. 44.31 crores.

- Gross margin improved by 357 basis points, from 38.27% to 41.84%.

- EBITDA reached about 10%, up 16% from 9.35% in Q2.

- PAT reached Rs. 26.87 crores, up 20.17%.

- The total borrowing of the company is Rs. 1,190 crores. This is an increase from the previous period due to term loans and working capital.**

- Working capital days increased by 3 days to 77 due to increased inventory holding in anticipation of higher Q3 sales. PIL expects to return to 74 days within the next two months and reach a goal of 72 days by March 31st.

Margin Guidance

- Management expects margin expansion to continue as higher-margin revenue scales up. This includes margins in the US, Ascent industrial components and hydraulics, and engineering services and metal buildings.

- Over the next 2-3 years, PIL aims to achieve a PBT of 7%. This will be driven by scaling higher-margin revenue streams.

- PIL expects its EBITDA margin to remain above 10% going forward.

- Interest on the exchange percentage is currently at 3.7%, and the company aims to reduce it to 3.75% as they begin capitalizing on the term loan interest.

Business Segment Performance

- The company is exiting low-margin businesses to focus on improving margins.

- These businesses include water treatment and environment, chemicals, aerospace, steel, railways, and solar EPC. Exiting these businesses has reduced overall revenue by approximately Rs. 1,000 crores.

- Growth drivers for PIL include PEB India, Ascent (US PEB business), process equipment, engineering services, tubes, and hydraulics.

- The order book in PEB India has increased to Rs. 800 crores and PEB US to $54 million.

- The Raebareli plant is now operational and will contribute to revenue from Q3 FY25.

- PIL expects strong growth across all chosen revenue streams. They project their highest-ever sales in PEB, the boiler business, process equipment, and engineering.

- Management is confident in sustainable revenue and profit growth over the next 2-3 years.

Management Guidance for the Future

- PIL is pursuing an aggressive growth strategy, targeting double-digit revenue growth. They plan to expand their asset base and increase order backlogs to achieve this.

- The company is undertaking capacity expansion in both India and the US. This includes new greenfield plants in both regions to cater to PEB and structural steel demands.

- PIL aims to achieve a $1 billion revenue target. While no specific timeline was given, management expressed confidence in achieving this goal in the coming years.

- The company is considering strategic options for the divested low-margin businesses. This includes the potential sale of some of these businesses to unlock value.

- PIL is also focused on strengthening its balance sheet. They aim to improve their credit rating from A to A+ and manage debt levels effectively.

Key Risks

While the sources didn’t explicitly list key risks, several potential challenges can be inferred from the discussion:

- Execution risk associated with capacity expansion plans: Successfully commissioning new plants and ramping up production will be crucial for achieving growth targets.

- Competition in the PEB market: Maintaining market share in a competitive environment will require continued focus on quality, service, and competitive pricing.

- Economic slowdown: The construction industry, a key driver for PEB demand, is sensitive to economic cycles. An economic slowdown could impact order flows and growth prospects.

- Raw material price volatility: Fluctuations in steel prices can impact profitability, necessitating effective hedging strategies.

Industry Outlook

- The sources offer limited insights into the overall industry performance. However, the management’s comments suggest a positive outlook for the PEB market in both India and the US.

- Strong order books and the need for capacity expansion indicate healthy demand for PEB structures.

- PIL’s management believes the company is well-positioned to capture market share and benefit from the industry’s growth.

- However, it is essential to acknowledge that the competitive landscape and macroeconomic factors can influence industry dynamics.

Disc:Invested

7 Likes

Aditya Rao was previously betting on Body in White plant in TN as a growth driver. Any clue how it is doing currently?

2 Likes

Source: From Q1FY25

It takes a long time for us to acquire business in BIW segment. So, company is not so bullish on expanding it.

5 Likes

Mostly due to India regulations is my guess currently

Also, based on my reading if OPM is 12-14% for Solar Modules atleast this year as per Crisil report below, then it makes sense as its another important Business Line which has Longer term visibility for them

We need to find more details in concall and JV agreement,

Few links taken from Websol posts

5 Likes

Yeah . It’s quite surprising . He mentioned that solar is not a growth sector they are looking at but the tables have suddenly turned . Solar cells / panels etc is a high investment business with the likes of reliance etc.

5 Likes