About

Interarch Building Products Limited, established in 1983, specializes in the design, engineering, manufacturing, installation, and erection of pre-engineered buildings (PEBs). They are a leading turnkey pre-engineered steel construction provider in India, with a 6.5% market share as of March 2024, making them the 2nd largest player in the organized market. They act as a proxy to private capex, so if the private investment improves, these indirectly benefit. These can be called as a capital good industry.

They have a market share of about 15% in the organized sector which has a TAM of 8000 crores amongst 7-8 companies.

They currently have five manufacturing facilities (September 2024) - two in Sriperumbudur, Tamil Nadul; one in Pantnagar, Uttarakhand; one in Kichha, Uttarakhand; one in Athivaram, Andhra Pradesh.

Apart from the facilities, they have eight sales and marketing offices in eight cities and additional personnel in five more cities.

They follow a business-to-business model, typically based on standalone purchase orders which means that they do not have long-term agreements with their clients and rely on projects issued by them from time to time.

There primary revenue streams include -

- Sales of PEB contracts

- Sales of building materials

- Others which include scrap sales and design & engineering services provided towards PEB Contracts.

They have a diverse customer base, including:

- Industrial and manufacturing constructions which contributed 73% revenue in Q2 FY25

- Infrastructure which contributed 25% revenue in Q2 FY25

- Others which contributed 2%.

They utilize both fixed and variable price contracts, deciding on the contract type based on the length of the project, steel price fluctuations, and other factors. The split between variable and fixed contracts is not static and as of Q2 FY25 it was 33-66% (variable-fixed).

Unit Economics

- The steel and other direct cost constitute 65% of the final sale price.

- The conversion cost of steel into a building or building parts, including engineering, designing, manufacturing, paint and other costs constitute 15%.

- A built in Overhead cost constitute 10% which doesn’t increase as sales increase and 10% is the profit.

- Erection cost is considered pass through and is not part of the above calculation.

- The larger projects are more profitable than smaller ones

- There could be a possible mismatch between the revenue and tonnage of steel sold due to fluctuating steel prices.

- They consider tonnage as the primary metric for gauging growth, rather than solely relying on revenue figures as it reflects the volume growth in the business. Their margins are decided by quantity, not by value.

Products

-

PEB Contracts

- Provide complete PEBs on a turnkey basis and also provide on-site project management

capabilities for the installation and erection of PEBs - They do not have long-term agreements with their clients and rely on projects issued by them from time to time.

- This segment contributed 87.74% of the company’s total revenue in the fiscal year ending March 31, 2023.

- Provide complete PEBs on a turnkey basis and also provide on-site project management

-

Metal ceilings and corrugated roofing

a) Metal ceilings

- Metal suspended ceiling systems are designed taking into account design, construction

practices and weather conditions. They are available in a variety of designs including lineal ceiling, clip-in or layin tile and C-grid (brand raster) ceiling and are manufactured from fully recyclable materials under the brand, “TRAC”. - They are suitable for various interior and exterior spaces, including airports, offices, hospitals, schools, restaurants, shops, hotels and power plants

b) Metal roofing and cladding systems

- Under the brand “TRACDEK”, they are used as a single skin roof or wall cladding or as sandwich panels formed by installing the cladding system in two layers with the insulation inserted in between the two layers combined with multi-layer insulation.

c) Permanent/metal decking (lost shuttering) over steel framing

- Under the brand "TRACDEK BoldRib”, they consist of cold formed zinc-coated steel decking panels, designed for construction of composite floor slabs which also act as permanent shuttering.

- Metal suspended ceiling systems are designed taking into account design, construction

-

PEB steel structures

a) Primary framing systems

- Provides the load-bearing structure, transferring loads to the foundation. They include primary load-bearing frames (main frames), end-wall frames, wind bracings, crane brackets, and mezzanine beams, all made from high-strength steel structures designed for stability and support.

b) Secondary framing systems

- Consists of structural components that support metal ceilings and corrugated roofing while transferring their loads to the primary framing system. These include roof purlins, wall girts, eave struts, and clips, typically made from Z-shaped and C-shaped pre-galvanized steel.

c) Non-industrial buildings

- Supply for non-industrial PEB buildings such as farmhouses and residential buildings (under the brand, “Interarch Life”) for erection and installation by third party builders/erectors

-

Light Gauge Framing Systems (LGFS)

- These are composite PEB structures comprising our primary framing systems, secondary framing systems and metal ceiling and/or corrugated roofing designed to support light-weight non-industrial buildings.

-

This contributed 10.72% of the company’s total revenue in the fiscal year ending March 31, 2023.

Raw Material

-

Basic raw material is steel in various forms: hot rolled steel plates, galvanized steel coil, galvalume steel, standard hot rolled sections and it is procured from third parties based on purchase orders and do not have continuing arrangements with their suppliers.

-

They source their steel (specialized steel) from all major suppliers: Tata Steel, Jindal, JSPL, JSW, SAIL, AMNS.

-

Tata Bluescope is the primary supplier of special coated steel which is used for Roofing and cladding.

-

HR steel 345 MPa is used for the columns and beams. Galvanized steel is 275 GSM steel and color-coated roof and wall coils.

-

To mitigate risks from steel price fluctuations, they use a mix of fixed-price and variable-price contracts. Stable steel prices - customers prefer fixed prices, but if prices decline, it benefits Interarch. Steel price increases are passed on to customers in variable-price contracts.

-

They maintain an inventory of steel and aim to have at least two months of stock at hand, plus two months of orders in the pipeline with steel companies at fixed prices.

Geography

| Facilities | Installed Capacity (MTPA) | Utilizable capacity (MTPA) | Nature of manufacturing |

|---|---|---|---|

| Pantnagar Manufacturing Facility | 31,000 | ~26,000 | PEB steel structures, comprising complete PEBs, primary framing systems (consisting of built-up sections such as H-shaped structures and I-shaped structures), and secondary framing systems (consisting of built-up sections and accessories such as angles and bracings) |

| Kiccha Manufacturing Facility | 59,500 | ~50,000 | (i) PEB steel structures comprising complete PEBs, primary framing systems (consisting of built-up sections such as H-shaped structures and I-shaped structures), and secondary framing systems (consisting of built-up sections and accessories such as angles, bracings and galvanized cold formed C&Z sections made from galvanized coils), (ii) metal ceilings and corrugated roofing, comprising metal suspended ceiling systems, metal roofing and cladding systems and permanent/metal decking (lost shuttering) over steel framing, and (iii) LGFS |

| Tamil Nadu Manufacturing Facility I | 10,000 | ~8,500 | Metal ceilings and corrugated roofing, comprising metal suspended ceilings systems and metal roofing and cladding systems |

| Tamil Nadu Manufacturing Facility II | 40,500 | ~34,000 | PEB steel structures, comprising complete PEBs, primary framing systems (consisting of built-up sections such as H-shaped structures and I-shaped structures), and secondary framing systems (consisting of built-up sections and accessories such as angles and bracings) |

| Andhra Pradesh Phase I | 20,000 | ~17,000 | Complete PEBs, primary framing systems (consisting of built-up sections such as H-shaped structures and I-shaped structures), and secondary framing systems (consisting of built-up sections and accessories such as angles, bracings and galvanized cold formed C&Z sections made from galvanized coils) |

| Andhra Pradesh Phase II (planned) | 40,000 | ~32,000 | (i) PEB steel structures products, comprising complete PEBs, primary framing systems (consisting of built-up sections such as H-shaped structures and I-shaped structures), and secondary framing systems (consisting of built-up sections and accessories such as angles, bracings and galvanized cold formed C&Z sections made from galvanized coils), and (ii) metal ceilings and corrugated roofing products comprising, corrugated roofing, metal roofing and cladding systems |

| Gujarat (planned) | - | - | - |

- They are primarily focused in India and don’t have any direct exposure to government entities.

- They are expanding into new states like Andhra Pradesh, Gujarat.

- Data Center demand could unlock export market for them and they are considering expanding their network to Central and West Asia, Southeast Asia, and Africa.

Clients

- Top 10-12 clients contribute roughly 40-43% of the turnover in any given year but from different clients.

- Repeat orders make up 80-85% of the topline. The regular clients for them are mostly warehousing firms like IndoSpace, Welspun who frequently order buildings for their warehousing needs.

- Three of five customer groups have worked with the company for over five years.

- There are two kind of customers:

- Traditional customers like Warehousing companies, FMCGs like HUL, Marico, paints and consumables like Grasim, Berger Paints, automobile companies.

- Customers from emerging themes; companies in renewables like Avaada, Exide, Reliance Solar; companies in data center, lithium battery plants.

- They do not engage in government contracts directly, however, collaborate with private sector partners like Delhi Airport through GMR, ONGC project through L&T, Railway coach factory in Jhansi through URC.

Industry

- The PEB market in India is valued at approximately Rs 195 billion in FY24 and is projected to grow to Rs 340 billion by FY29 at a CAGR of about 10.5-11.5%.

- The organized sector accounts for 40-45% of the market, with the top six organized players controlling 80-85% of the organized sector. In FY24

- The industry does not require significant upfront capital investments in terms of manufacturing facilities and suitable technology which tells us that there is threat of new entrants.

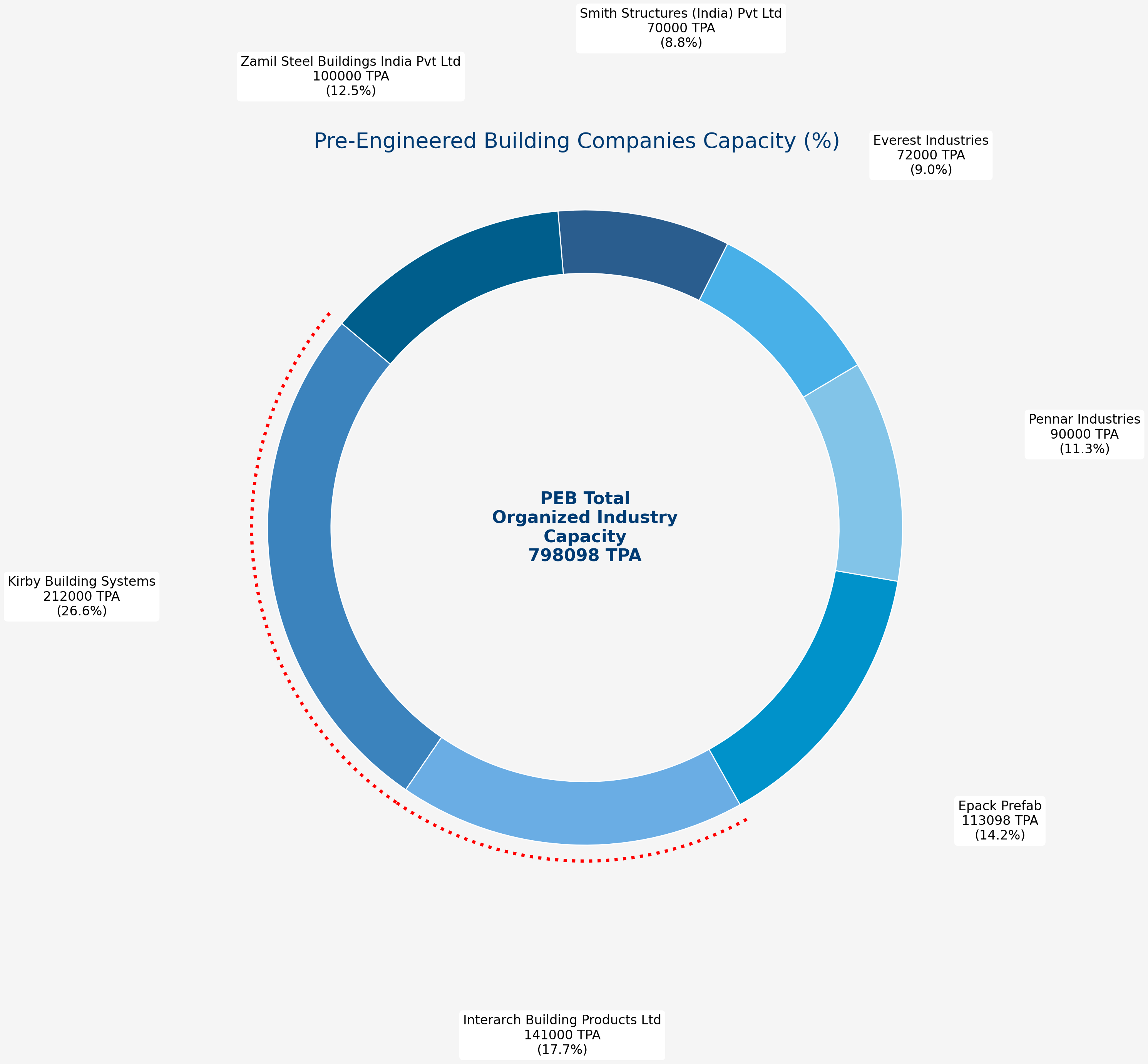

- Kirby Building Systems & Structures India Pvt Ltd, Pennar Industries Ltd, Interarch Building Products Ltd, Zamil Steel Buildings India Pvt Ltd, Phenix Building Solutions/M&B Engineering, Everest Industry are some of the local players while global players include names like ATAD Steel Structure Corp, BlueScope Steel Limited, Butler Manufacturing, etc.

- Dedicated players are Kirby, Interarch, Zamil; Diversified players are Pennar, Everest, Epack.

| Company | Installed Capacity (MTPA) |

|---|---|

| Kirby Building Systems & Structures India Pvt Ltd | 300,000 |

| Interarch Building Products Ltd | 161,000 |

| Zamil Steel Buildings India Pvt Ltd | 100,000 |

| Pennar Industries Ltd | 90,000 + 36,000 |

| Everest Industries Limited | 72,000 |

Advantages & Disadvantages of PEB

| Advantages | Disadvantages |

|---|---|

| Faster Construction Times and lower maintenance requirements | Vulnerability to fluctuation in raw material (steel) prices |

| The cost is estimated to be at times 15-35% lower than conventional structures for sheds, warehouses, and depots | Logistics and Transportation challenges since the components are made off site |

| More sustainable due to less wastage than RCC buildings | Requirement for skilled labor and managing shortage issues |

| Higher salvage value as they can be dismantled and sold as scraps | Fire and Heat resistance is lower compared to RCC |

| High flexibility as they can be dismantled and relocated as per needs | Design Limitation in achieving complex architectural forms |

| Quality control since it’s made in a controlled environment | Higher upfront cost |

| More durable - resistant to termites, earthquakes |

Key Growth Drivers

- Rapid Urbanization and Industrialization: Increase in demand for warehouses, cold storage and manufacturing, initiatives like Smart cities, Make in India will boost demand.

- Government Initiatives and Investments: PLI schemes to different industries will indirectly benefit demand for construction and hence the PEB industry. There is a push for increasing steel consumption by the govt. which also helps the industry to grow. National Infrastructure Pipeline (NIP) also creates huge opportunity for the industry

- There is a PLI on special steel (2023-2028) which will benefit the PEB players since it’s their main raw material.

- Growing demand in emerging sectors like E-commerce, Renewables, Data center.

- Shift towards organized players and increasing market share due to brand awareness

- Cost and Time efficiency: Offers cheaper and more efficient alternative to RCC buildings. With technological advancements, they can be modularized and are industry agnostic which makes them faster to deploy.

Challenges / Risks

- Heavy dependence on steel as a raw material, making it vulnerable to steel price fluctuations. Any geopolitical issue, government policies can influence steel prices and hence indirectly affects the industry.

- Dependance on 3rd party suppliers for their raw material.

- Economic slowdown could lead to a demand slowdown

- Shortage of skilled labor for design, engineering, fabrication, and erection of structures which can lead to implementation delays and increase labor cost.

- The components are made off site, hence transportation and logistics are very crucial in the industry.

- Currently a fragmented industry and has high competition which can lead to price wars.

- Design Limitations will make them uncompetitive in case of complex requirements.

- Compliance with regulations and standards. For eg. Different regions will have different requirement for earthquake resistant structures, etc.

Expansion Plans

So, the expansion of Attivaram is classified into 2 phases.

-

Phase 1

- To expand into Southern states to meet the growing demand, secured 40,470 sq meters of land in Attivaram, Andhra Pradesh with a lease period of 33 years.

- Phase 1 will increase the capacity by 20,000 MTPA, was done with internal accrual and was finished in August 2024 and commenced operation in September 2024.

-

Phase 2

- The Attivaram facility will be expanded next to Phase 1 facility with a capacity of 40,000 MTPA and is expected to finish by first quarter of FY26. It is being funded by the IPO proceedings with a cost of 57 crores.

-

Kheda Facility

- Secured land in Kheda, Gujarat, to produce 50,000 to 60,000 MTPA, with the expansion to be done through internal accruals.

- The investment of Rs 100 crores will be made post-completion of the Athivaram project, which can generate revenue of Rs 550 crores at current steel prices.

-

There is an expansion in their North facilities, upgrades at Kichha and Andhra Pradesh.

Guidance

- The H2 is better than H1 with a ratio of 60:40 based on historical trends.

- The company aims to double its revenue over the next 3-4 years.

- They expect revenue growth of 10% in FY25 and 10-15% in FY26 with a sustainable margin of 9-10%. They are expecting a PAT north of 100 crores.

- Double-digit volume growth with an expectation of 15-20% growth in FY25.

- There might be a slight margin improvement in Q3 FY25 due to softening steel prices.

Notes

- They are providing building solutions to upcoming sectors like EV infrastructure,

renewable energy projects, data center facilities, with a move into multi-story commercial

residential and institutional buildings. - They have a pipeline of potential projects worth around INR 4,000 crores and a hit rate of their pipeline is 20-27%. These pipelines are all fully engineered and customized, so they are considered “qualified” opportunities instead of bids.

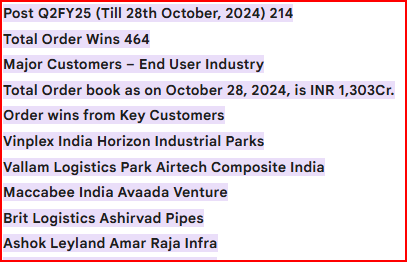

- Order book of Rs 1,350 crores as of September 14, 2024, expected to be executed in the next 9-10 months.

- They operate in the light steel building segment and plan to expand into the heavy steel building segment, used for industries like sports, steel plants, and fertilizers, in the next 1-1.5 years.

- They are expanding focus to business-to-government engagement, opportunity in the railways like railway stations, freight terminals, factories, depots due to huge investments in modernization, capex and supporting infra.

- Despite 6% revenue growth, they had 17% volume growth in Q2 FY25, this is due to fluctuation in the steel prices which comprises the bulk of the cost.

- Management talks about the shortage of skilled labor and strategies to handle it.

- They partner with third-party logistics to transport their products.

- They are transitioning the Business-Critical ERP Application system to cloud-based platforms, enabling improved availability, scalability, and flexibility.

- Have formed a strategic partnership with Jindal Steel & Power Ltd (JSPL).

- JSPL could probably provide them with discounted steel and which could help them improve their margins

Note: Most of the information is from Concalls, AR, DRHP, PPTs

Disclosure: Not invested, tracking it along with Pennar Industries. Actively researching the whole PEB industry as it feels like a proxy to any infra development