Pennar Industries Limited is a Hyderabad-based company that is engaged in

providing engineered products and services.

Products manufactured by Pennar Industries Limited include:

Cold-rolled steel strips

Precision tubes

Railway coaches and wagons

Pre-engineered building systems

Sheet metal components

Solar module mounting structures

The company’s products have a presence in several sectors, such as Infrastructure,

Railways, Automobiles, Power, General Engineering, Building and Construction, and Solar.

Source: http://www.pennarindia.com/company.html

Market Capitalization: Rs. 801 Crores

Current Price per share: Rs. 66.55

Price-to-Book Value Ratio: 1.47

Price-to-Earnings Ratio (TTM): 16.17

Debt-to-Equity Ratio: 0.54

Source: Pennar Industries Ltd financial results and price chart - Screener

The company has four business units:

Systems and Projects (railways and solar mounting module structure components)

Industrial Components (general engineering and automotive components)

Precision Tubes (electro resistance welded and cold drawn welded tubes)

Steel Products (cold-rolled steel strips and formed sections)

The company has three subsidiaries:

Pennar Engineered Building Systems Limited (custom designed building systems and

solar module mounting structure systems)

Pennar Enviro Limited (process engineering plants and specialty additives)

Pennar Renewables Private Limited (solar power plant assets [28MW])

Source: FY2016-17 Annual report, http://www.pennarindia.com/annual-report.html

The company has recently entered into an agreement to sell its stake in the third subsidiary listed above, and as a result it plans to reduce debt by Rs. 101 Crores, see https://nseindia.com/corporate/LettertoSE-11082017_11082017152405_399.zip

Investment Rationale: The company appears to be in a transition phase;

it is focusing less on low-margin products such as cold-rolled steel products

and focusing more on high-margin products such as pre-engineered building systems,

railway coaches, and solar module mounting structures. The management expects

significant growth from its railway and solar vertical. The management has projected

double-digit growth for its Precision Tubes business unit over the next few years.

The management also projects significant growth for its subsidiaries over the next

few years. See below for supporting evidence.

Pages 8-11 of the FY2016-17 annual report, http://www.pennarindia.com/annual-report.html

Received orders worth Rs. 252 Crores:

http://www.pennarindia.com/pdf/Earnings%20Releases/sep-pressrelease17082017.pdf

Investor Presentation for Q1 FY2017-18:

https://nseindia.com/corporate/PennarIndustriesQ1FY18InvestorPresentation_17082017093100_057.zip

Negatives:

Low promoter holding (36.36%).

Company has not been paying out dividends for the last three years.

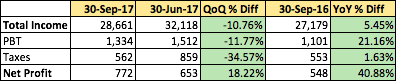

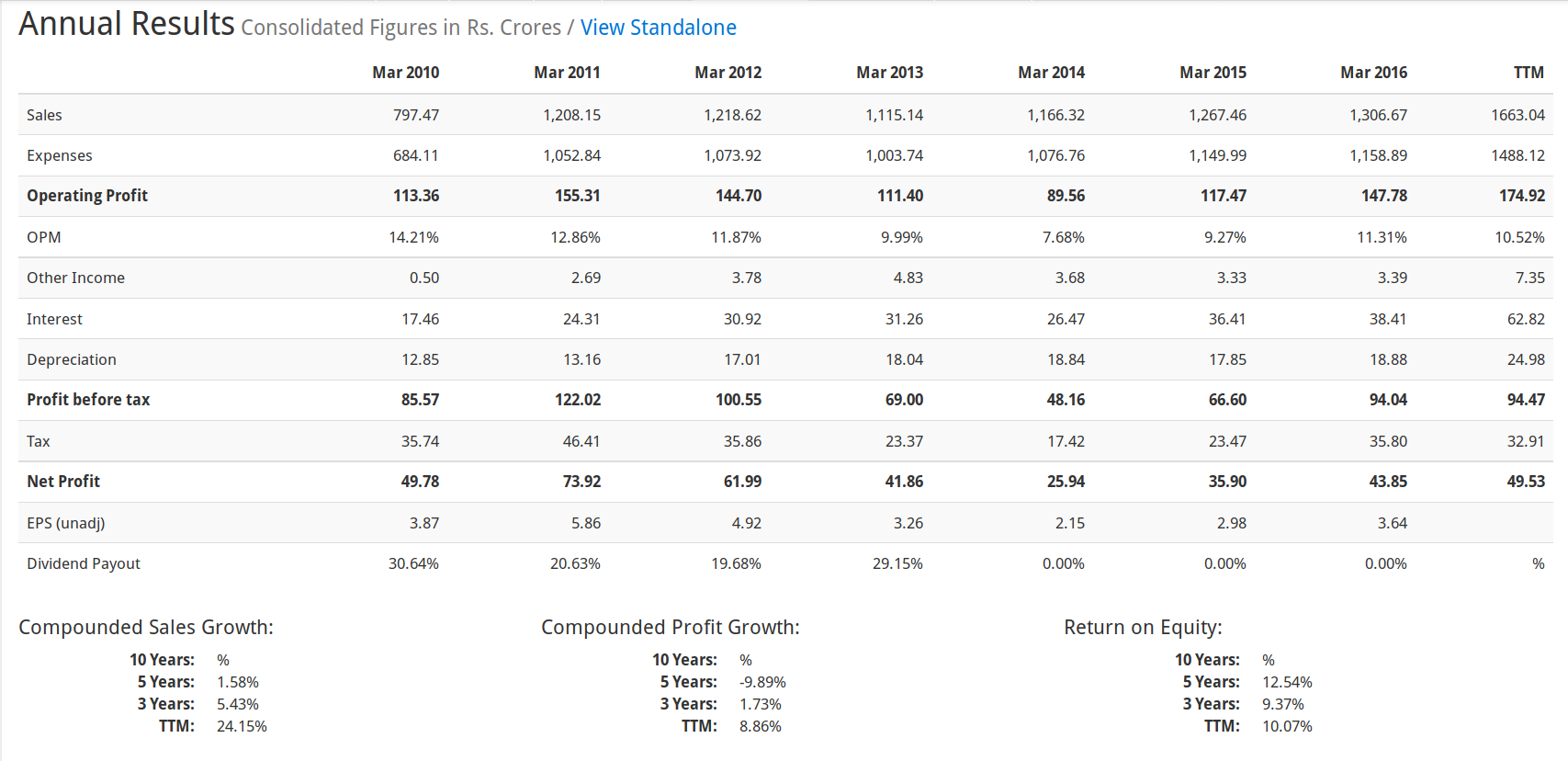

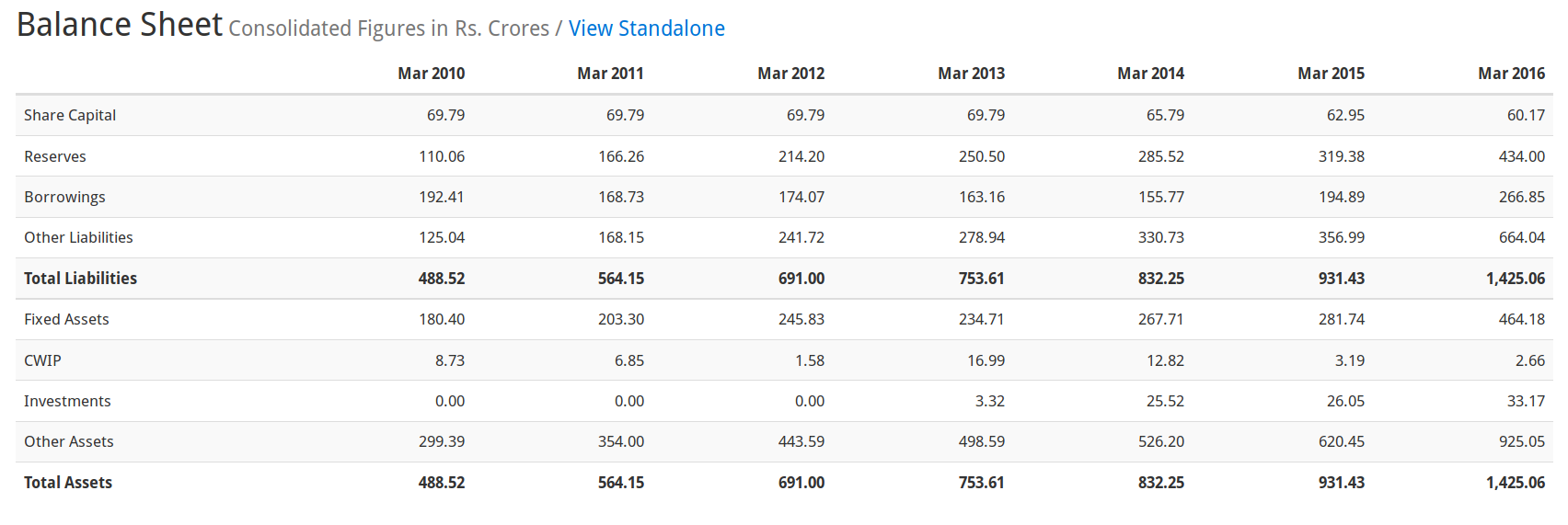

Below are the Profit-and-Loss statement, Balance Sheet, and

the Cash Flow statement. Source: Pennar Industries Ltd financial results and price chart - Screener

Disclosure: Pennar Industries constitutes 19% of my portfolio;

purchased in October 2016, with average purchase price Rs. 52.

I’m a novice, and I am hoping that the experts here will dig deeper

than I have, in order to determine if this is a worthy investment

opportunity.