When you sell the shares and company is the buyer, you will receive a mail from BSE/NSE about number of shares bought by company. That is your count.

2 Likes

2 Likes

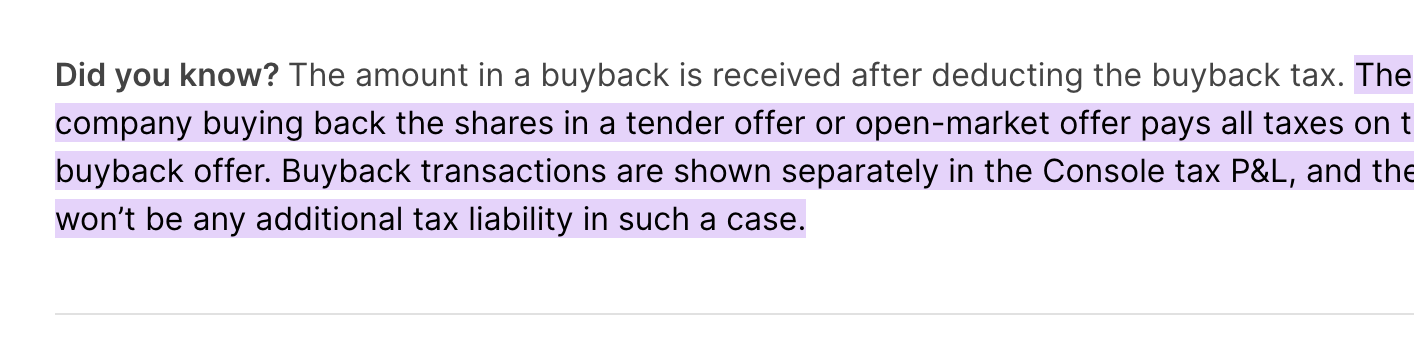

Thanks for the information. That still leaves out one question - is there a way for the seller to know before he sells, who the buyer is? The seller may want to sell only to the company and not to other buyers so as to avoid paying tax.

In open market buyback this is not possible at all. Any buyer can put a buy order above the company’s price. Even if the company is the sole buyer at that price, the transaction report never says who it is sold to.

In fact when you execute a sell order you’re obligated to deliver the stocks T+1 (or 2) days later. It is just settled and no one knows who is the buyer or seller

1 Like

Can anyone help me understand how Paytm and Paytm Payments Bank are interlinked? What sorts of transactions happen between them and stuff?

1 Like

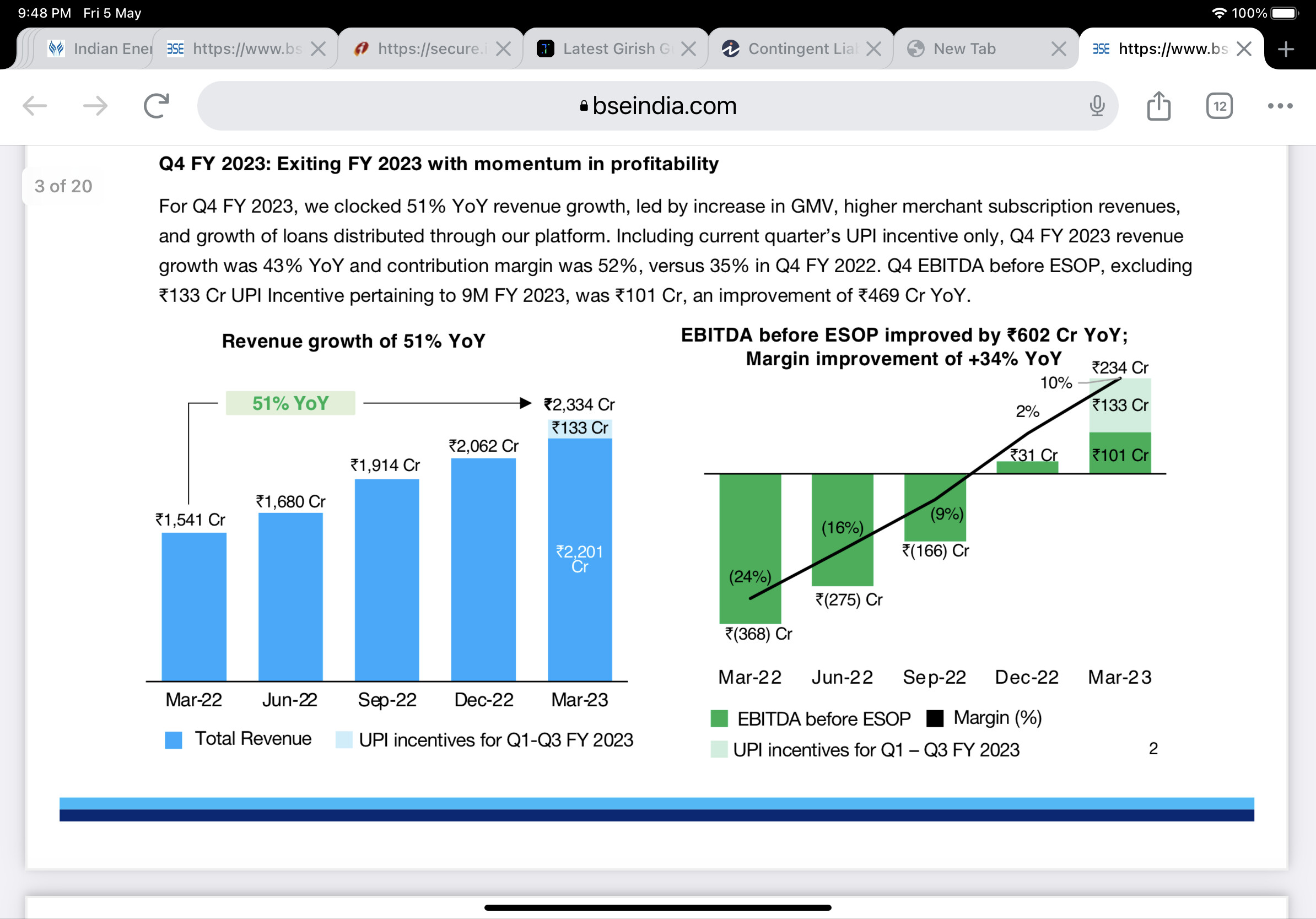

How do you rate Paytm’s results today?

Here is my take on the results:

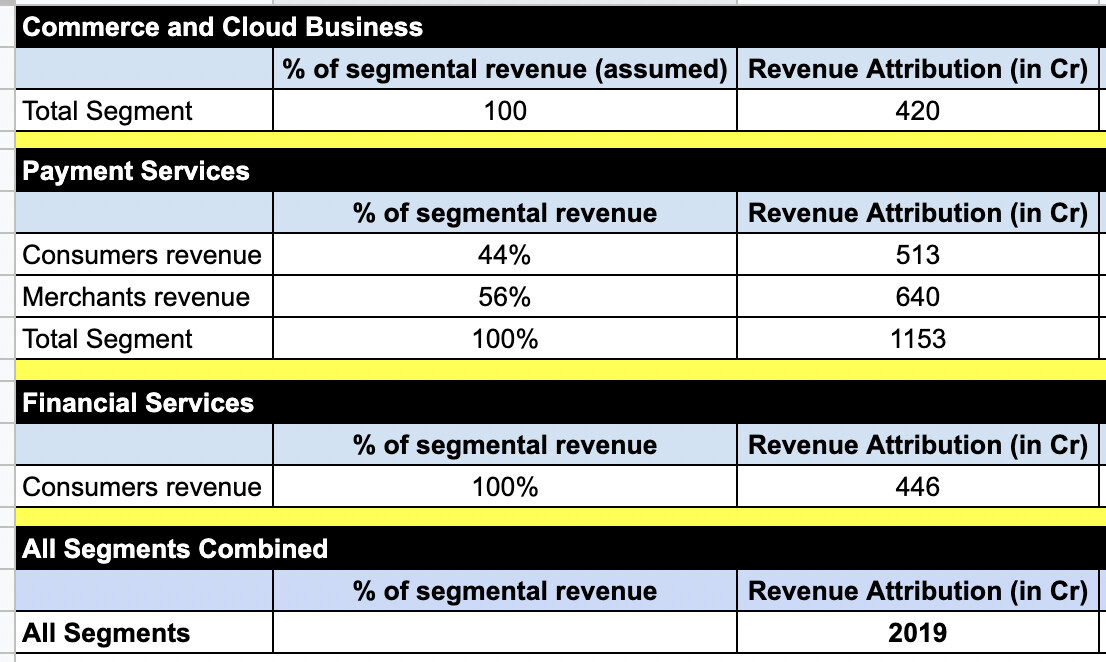

Payment Services Revenue

- Revenue Growth

This segment has been flat. About 1% growth QoQ and 21% YoY (34% adjusting for UPI incentive) - Expenses

Reduction of 1% QoQ and 6% YoY driven by festive season sales (though the report incorrectly says Q2 FY2023) - My take

Disappointed with this segment. Flattish revenue (QoQ or even compared to last few quarters). Expenses have gone down, marginally, which is a positive, but I am not sure if this is an aberration or the new normal. Further, the guidance is that the payment processing margin will reduce from 7-9 bps to 5-7 bps

Financial Services & Others

- Revenue Growth

Steep revenue increase. 250% YoY and 27% QoQ - Expenses

Check overall expenses - My take

Impressive performance in this segment. The company gets 2.5-3.5% of loan value at disbursement and 0.5-1.5% post-portfolio closure (which should come in in about a year or so).

Commerce and Cloud

- Revenue Growth

Flattish revenue. 24% YoY - Expenses

Check overall expenses - My take

Indifferent

Overall Expenses

- Indirect expenses have decreased from 58% of revenue (Dec-21) to 51% of revenue (Dec-22). Very impressive.

- ESOPs have gone up by 150%. This is very disappointing, especially when the company’s stock price is struggling. I understand that not 100% of ESOPs will vest, but the company should provide visibility on ESOP cost in the future, and the method of allocation.

Final Note

1. I think Paytm is becoming more of a lending company as opposed to a Payment Company

2. Strong performance in lending. Not so much in payments and commerce/cloud business

3. Operational profitability is good. But the management has to provide visibility on ESOP allocation, and not abuse this instrument.

Disc:

For educational purposes.

Ex-Paytm employee (left org in 2019).

Invested

8 Likes

PayTM ad spend as a % of sales has come down, and might be one of the driving factors behind EBITDA positive

Ad spend as a % of sales

Jun 21 ~15.4%

Sep 21 ~17%

Dec 21 ~19.4%

Mar 22 ~16.2%

Jun 22 ~18.9%

Sep 22 ~17.1%

Dec 22 ~11%

What matters here is the consistency of the same .

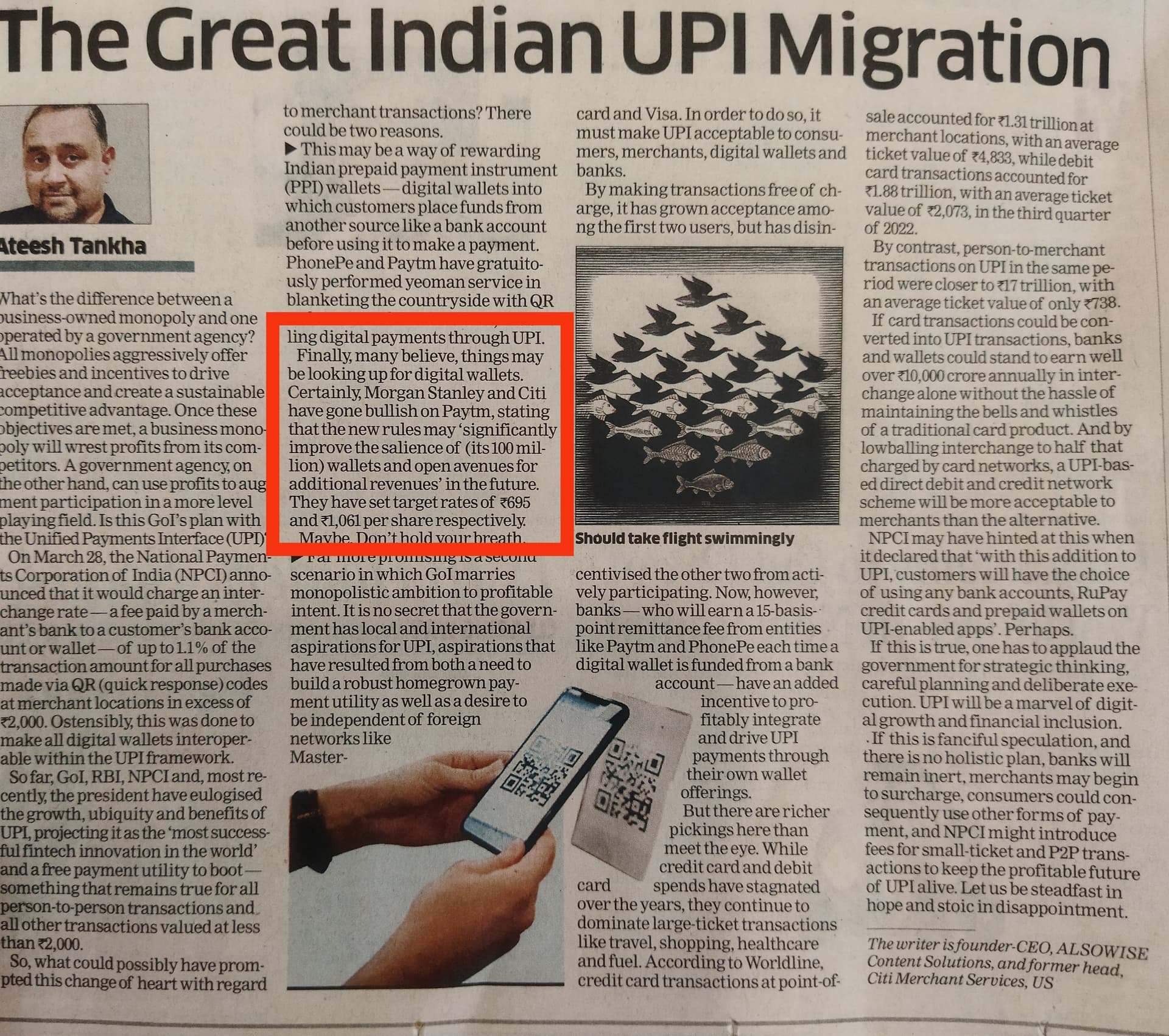

Phone pay and google pay also gained market share in UPI payments.

Found this article value-adding.

1 Like

Interesting article on Ant finance (which to me is a lot like China-equivalent of Paytm).

Key excerpts from the article:

-

Ant neither took deposits, nor piled risky loans onto its balance sheet. Nearly all of the short-term credit offered on Alipay, the consumer-facing app that boasts over 700 million domestic users, was securitised or underwritten by third-party banks and partners >> Exactly like Paytm (minus Postpaid)

-

If there’s one thing that makes regulators nervous – for good reason – it’s rapid growth in new areas of finance that they don’t directly oversee. From now on, the Ant must fund 30% of the loans it makes with partners, and those banks can’t originate more than half of their total loans through online companies >> Led to reduction of loan balance by 75%

-

On a multiple of 11 times forecast 2023 earnings – between where mid-sized Chinese banks and technology hotshots trade – and Ant today is worth perhaps just over $55 billion >> Its IPO was planned at US$ 300B

Takeaways for me:

- In the short run, Paytm is likely to see massive momentum due to lending (we are already seeing this)

- In the long term, the regulator will have the final say.

5 Likes

Does Paytm lends from it own book for Paytm Postpaid(BNPL product). If yes, Which entity under One97 have this loan in balance sheet?

A good thread to understand the business model of Paytm.

Seems select consumer fintech cos like Paytm & PB Fintech can give good returns over next 2-3-4 years as they become profitable.

5 Likes

I also feel PayTM has advantage when it comes to UPI P2M transactions as it generates some revenue and Payment bank has it advantage, I hope PayTM is paying less for P2M transactions to Payment bank as it will act as acquiring bank. PhonePe case, they need to take help from yes bank (from it’s handle @ybl).

Disc. Invested so might be biased.

(694) How Paytm is secretly KILLING Phonepe and Bharatpe? : Detailed Business CaseStudy - YouTube

One more good video to understand how Paytm is outpacing Phonepe & understands its moat of Soundbox and use of Algos to extend loans after doing homework on creditworthiness n intt rates being charged for loan products.

discl- invested recently

4 Likes

Vijay Sekhar sharma says SVN no longer an investor in Paytm

SVB crisis: Vijay Shekhar Sharma says Silicon Valley Bank not a stakeholder in Paytm (msn.com)

1 Like

what is stopping Phonepe and Bharatpe to develop similar solutions (soundbox and Algos for loans)?? All fintech payment startup firms eventually want to get into lending as Govt continues to push for zero fees on payments made by end customers!

PhonePe and BharatPe(remember seeing it with merchants) are already deploying sound box solutions.

https://www.phonepe.com/business-solutions/offline-merchant/smartspeaker/

They give loan from NBFC and Banks and Not from there own book.

The Ken’s story today is on Paytm. As always, the story is for paid-subscribers only.

But here are the four key summary points for everyone’s reference:

-

Payments business makes up 60% of Paytm’s revenue, but the sharp jump in its loan distributions in FY23 has garnered far more interest

-

A well-oiled distribution service and an upselling mechanism reveal only half the story behind this spike

-

A nifty FLDG workaround and an efficient loan-collection service underpin Paytm’s fledgling loan distributions

-

Maintaining this pace amid growing competition without compromising on the quality of borrowers will be the key to its future profitability

Here’s the link to the full story: Paytm’s results hint at a turnaround. But loan-collection hacks drive it

4 Likes