Starting a thread for Discussion on PayTM.

PayTM started as a mobile value-added service company and later started mobile and utility payment along with e-commerce. However, in the last few years Paytm has transformed itself into a complete financial service company.

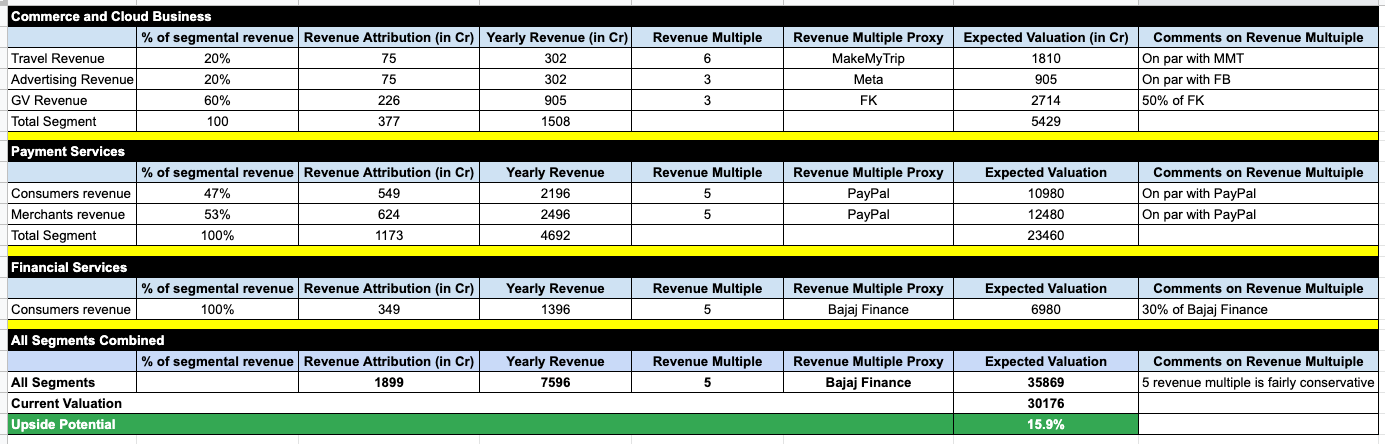

PayTM’s business is bifurcated into 3 segments:

-

Payment Services: According to research firm Paytm is the largest payment platform in India with a gross merchandise value of 4 lakh crore in FY 21, which is 40% of total payment transaction volume.

-

Commerce and Cloud Services: Such as your ticket booking, travel, entertainment, gaming, food delivery, ride-hailing, and so on. It also provides merchants with software and cloud services for various aspects of their business, such as your billing, ledger, vendor management, customer promotion, catalog and inventory management, and so on.

-

Financial Services: mobile banking, lending, insurance, and wealth management services for consumers and merchants. For example, within mobile banking Paytm has launched Paytm payment bank, where Paytm has around 49% equity that provides an option to open saving account, current account, salary account, FD and debit card. As of March 21, Paytm payment bank had 64 million savings accounts.

Company Financials:

Revenue: 3597 in FY19 and 3186 in FY21.

Profit: It has been in losses for the last 3 years. In FY 19 The loss was 4230 crore, in FY 20 It was 2942 crores, and in FY 21 It was 1701 crore.

The company IPO’d at a price of 2150 which has now come down to 600 (-73%).

My Opinion:

There seems to be multiple glaring problems in its current business.

- Lack Of Focus: PayTM has been on a spree to start new verticals without any plan of monetization or profitability.

a. PayTM: PayTM itself has 2 core segments, mediating transactions and providing Value Added Services. They use Payment Options/UPI to attract users to come to their platform and then prompt them to do other tasks such as Bus, Train Bookings etc through the app where they earn money. The problem in this space is that it’s very crowded (PhonePe,GPay,ixigo,MakeMyTrip) and hence margins are paper thin.

b. PayTM Mall: An e-commerce store which was a 1:1 copy of flipkart/myntra. The overall execution of this product is horrible. No checks for scams, poor logistics handling etc seem ripe in this space. This was made as a spinoff of the Original Company which recently lost its Unicorn status and seems to on the verge of shutting down.

c. PayTM Bank: Sometime ago PayTM got approval to provide some financial services but seems to already botched this too as RBI is investigating it for Leaking data to chinese firms.

In Conclusion, none of the segments seems to provide confidence to me that this will become a fundamentally strong business.

-

Company Structure: PPBL which in my opinion is the best of all segments is not completely owned by PayTM. Vijay Shekhar Sharma holds 51 per cent in the entity with One97 Communications Limited holding 39 per cent and the remaining 10 per cent of share is held by a joint venture between Vijay Shekhar Sharma and One97 Communications. Since VSS runs both the companies, this makes us retailers vulnerable to management shenanigans.

-

Management: VSS doesn’t inspire a lot of confidence to me. You can view his interviews here and form your own opinion. Vijay Shekhar Sharma & Madhur Deora React To Macquarie Report On Paytm | CNBC TV18 - YouTube. Another major red flag is that management is conflating talking about PPBL and PayTM. In Interviews, the management says that “PayTM is doing well on lending, it has done 2.8 million loans in september”. Except, the loans are done by PPBL and not PayTM. PayTM may have facilitated the loans but in future PPBL has no obligation to keep using/supporting PayTM.

-

Shareholders: I feel a lot of foreign shareholders compare PayTM to VISA/Mastercard which is a skewed view as India has UPI which kills all these players. I could be wrong on this one.

The only Positive thing I have about this company is that they can adopt BharatPe’s Loan Financing Model really fast which seems to have a lot of room of growth.

Sources: Fundamental Analysis of Paytm | Paytm IPO Review

The Indian Smartphone Revolution: Paytm's "Coming of Age" IPO - YouTube

Disc: Not Invested