Paytm will immensely benefit if this happens

Thanks for sharing. My reading of this is actually the opposite. The Account Aggregator (AA) system that Mr. Nilekani talks about seems to aim at removing information asymmetry and create a level playing field.

Paytm has been the beneficiary of this information asymmetry, having near exclusive access to transaction data of millions of users and merchants. This is why the company has been making good progress on lending.

When such data is available to everyone, why would financial institutions lend through Paytm? At that time, analytical abilities may be the edge remaining with Paytm, not data. It wouldn’t be difficult to attain this edge for the competition.

As with ONDC, this AA is also aimed at removing monopolies. As ONDC is for Amazon/Flipkart/Swiggy/Zomato, maybe AA is for Paytm/Phonepe. We have to wait and watch.

Disclosure: Invested

3 Likes

Strength of PayTM in my view (in this context) is about loan collection process control. They have direct visibility on every transaction in the account and available balance on a real time basis and also do the monthly collection digitally. So while I am in alignment to some extent with your views on AA removing monopolies, in my view it will impact the lending side of business. However the scale and existing penetration of PayTM should help big time in loan collection business which some other fintech’s may not have.

Just my 2 cents! No investments, on watch list!

2 Likes

Since the article is behind paywall, will it possible for you share the summary of “FLDG workaround” managed by PayTM as mentioned in the article?

1 Like

Financial institutions would still lend through PayTM because PayTM is the channel, it allows for control over the lending and collection process by making it synchronous with the customer’s transaction itself. This removes friction from lending and collection, and by itself will ensure lower defaults compared to lending through other modes. Compare this to hundreds of foot soldiers employed by NBFCs and micro finance institutions to do the same work.

5 Likes

I doubt whether they have direct visibility of account balance.

Typical shopkeeper collect payment through cash / credit card / online payment.

Paytm, processing online payment will have visibility of that channel only. They won’t understand total sales not % of payment coming through online channel.

Disclaimer - I use paytm for online payment collection in my shop. Online payment is approximate 30% of total payment.

2 Likes

They might be giving out guarantees for their customers as well. As per Finshots, this is what Zest Money was doing.

1 Like

Lending services are done via parent company not via payment bank

In 2019, Paytm started offering a one-month buy-now-pay-later (BNPL) loan product, called Paytm Postpaid. Since then, it has built a cohort of users with up to four-year credit history. Now, it is using this customer base to sell personal loans to users and merchant loans to 7.1 million merchants who accept payments through Paytm’s payment devices.

At the moment, there is no dearth of demand for credit. But after the Reserve Bank of India—India’s banking regulator— imposed strict rules on default guarantees, lending practices in the country have changed.

The regulator banned lenders from sharing credit risk with loan-service providers, who distributed loans. This clarified the roles of regulated and non-regulated entities, giving more clarity to regulated entities such as non-banking financial companies (NBFCs) when entering into partnerships. However, it also ended the First Loss Default Guarantee (FLDG) model that lenders used while partnering with loan distributors.

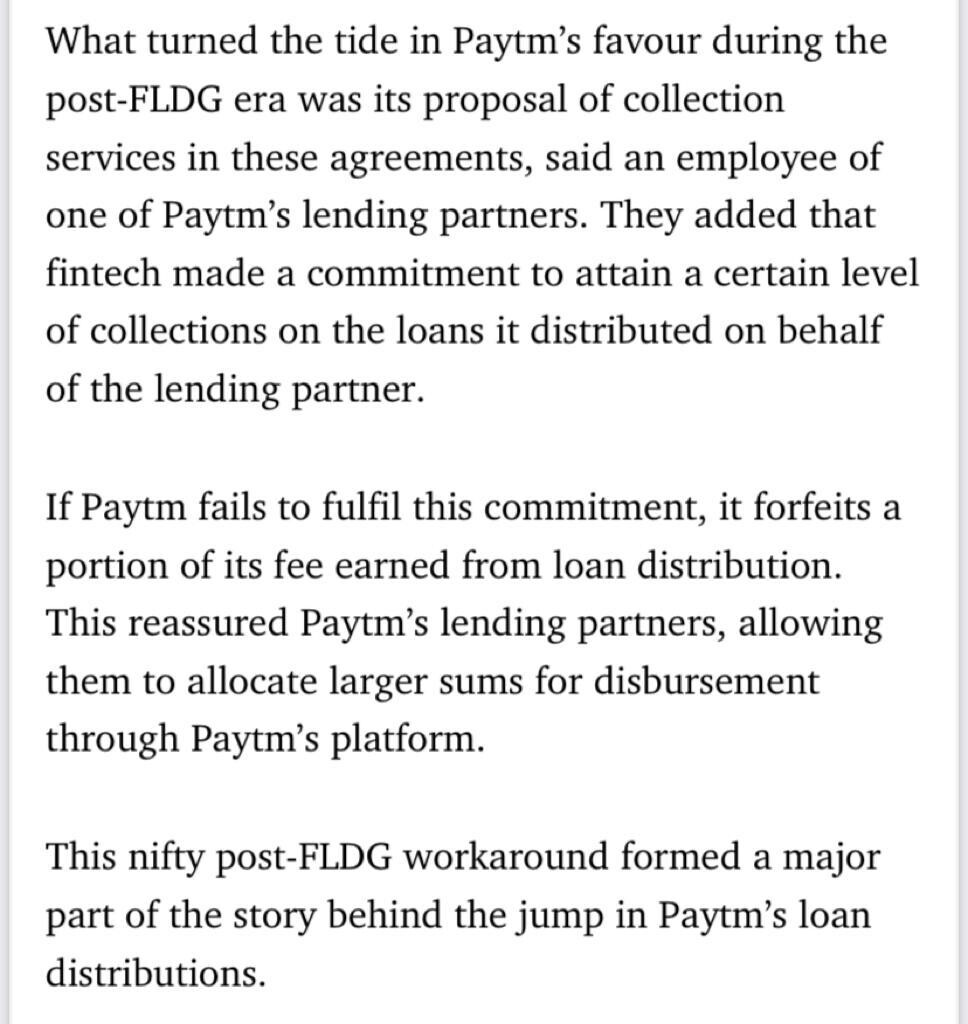

*What turned the tide in Paytm’s favour during the post-FLDG era was its proposal of collection services in these agreements, said an employee of one of Paytm’s lending partners. They added that fintech made a commitment to attain a certain level of collections on the loans it distributed on behalf of the lending partner. *

If Paytm fails to fulfil this commitment, it forfeits a portion of its fee earned from loan distribution. This reassured Paytm’s lending partners, allowing them to allocate larger sums for disbursement through Paytm’s platform.

*This nifty post-FLDG workaround formed a major part of the story behind the jump in Paytm’s loan distributions. *

Prior to the RBI’s FLDG ban, lending-service providers (LSPs) were able to guarantee that they would compensate the lending partners for any credit loss on the portfolio originated by the LSP. But the regulator wanted the regulated lender to shoulder the risk entirely.

*This came as a blow to the intermediaries. Even though default outcomes don’t really affect distributors, lenders’ disbursals are linked to portfolio performance. *

Without FLDGs, lenders have reduced the fees they pay their LSPs to price in the risk, bringing down intermediaries’ margins, said the co-founder of a mid-sized NBFC.

Now Paytm has found a way to not dilute its margins by adding collection services to the mix.

All of its lending partners now rely on Paytm to both onboard borrowers and also collect from them, said a person close to the fintech. And this has increased its average revenue from each lender by a third, they said.

5 Likes

Indeed, Collection Services provided by Paytm is its strength. It is not hard to imagine competition in this area too.

Once data is democratized by UPI, ONDC, and AA systems, it is not hard to imagine competition in the lending and collection areas based on data analytics.

Indeed, Paytm will still have first mover advantage which provides headway, market penetration, and momentum. Let’s see how this goes.

3 Likes

@rpattabi It is not access to data, it is the ease of disbursal & collection which is PayTM’s moat. The biggest headache in small ticket retail loans is operational, and that is the problem PayTM is solving.

@ankit_talreja – As clarified by @Mathew10 above, PayTM is not giving guarantees. They are working solely on commission. If delinquencies are higher, they earn less fees, that’s all. But no Balance Sheet exposure.

8 Likes

two points to clarify my statement:

- While Paytm will have multiple number of data points (including Paytm transactions) to gauge creditworthiness, the loan amount they will sanction would be largely be derived from value of PayTM transactions happening in the account.

- By real time visibility, I meant only the PayTM account visibility

If you combine pt.1 and 2, you reduce a lot of risk on both the lending decision and also on collection efficiency. Hope that clarifies

2 Likes

I have been studying Paytm of late and am mightily impressed. Much has been debated about it in the thread, nevertheless let me add my thoughts.

What does Paytm do? They onboard consumers and merchants through UPI payments and payment solutions, and then distribute loan to them.

Paytm business flywheel:

Consumers come for UPI/merchant payments > Merchants come for these consumers, add more and more use cases > more users > more merchants > Disburse loans to both these types of users.

They did a lot of iterations and figured out/crystalized their strategy to monetize and scale, a well thought out one. And have built a beautiful funnel/upsell workflow:

Consumers:

Come for UPI Payments > Paytm postpaid/credit card > Personal Loan > Repeat loan

Merchants:

Start with free Paper QR code payment > Soundbox > POS/EDC payment solution > Merchant loans > repeat loan

Soundbox, POS/payment solutions bring subscription revenue.

- 50% of personal loans come from postpaid customers

- 20% of personal loan customers repeat buy in 12-18 months

- Device merchants form 80% of merchant loan disbursal

- More than 50% of merchants loan by value come from repeat loans.

- Soundbox/EDC merchants retention rate 85%

Number of monthly transacting consumers - 9 Cr

Number of subscribed merchants - 68 L

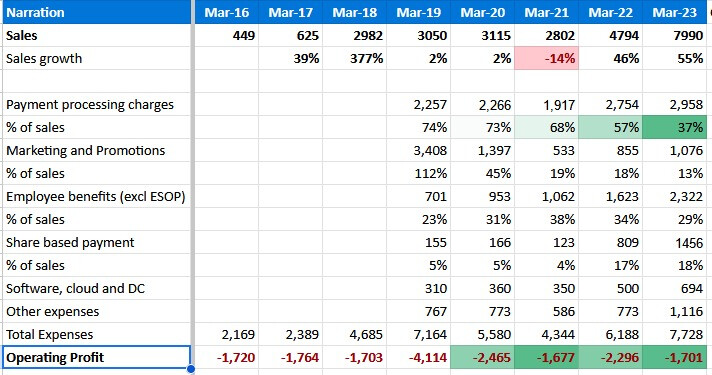

This shows up in their results:

-

Payments revenue is scaling up. Most importantly its margin is steadily improving - better bank rates, adoption/scale, account level rationalization. Margin means the profit after the expenditure on payments revenue.

-

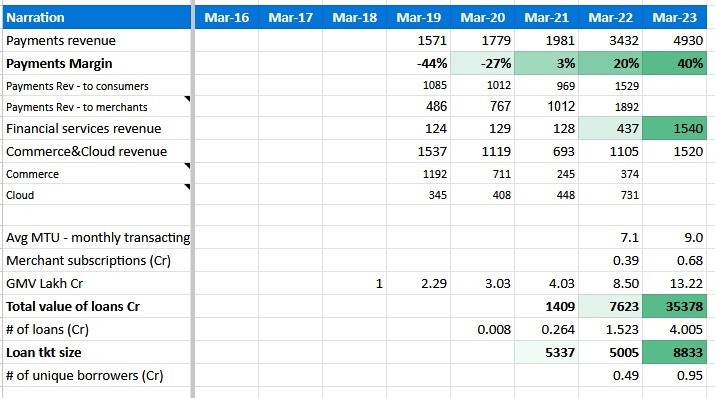

Financial services is growing fast and scaling high. Total value, loan tkt size and no. of borrowers are growing.

But an important point to note here is that they just scratched the surface in lending business. Lending penetration in their captive user base:

- Postpaid - ~5% of MTU

- Personal Loans - 1% of MTU

- Merchant loans - ~6% of device merchants

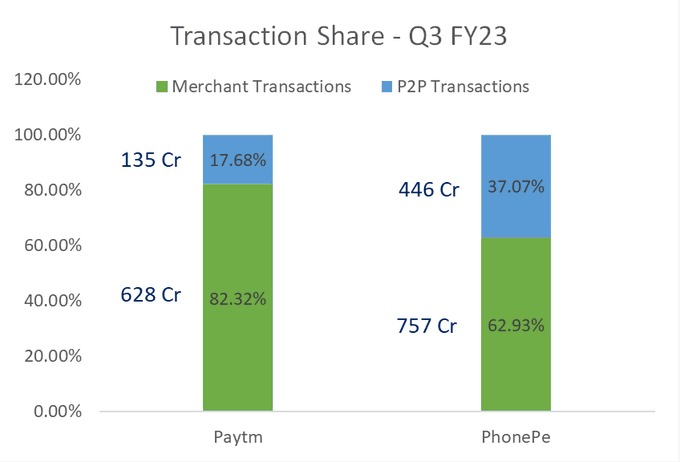

Now where do they stand vs Phonepe?

Digital payments market share:

Phonepe - 46%

Google Pay - 34%

Paytm - 15%

Phonepe has 10x customer base. with a lion’s share in UPI payments. Yet…

Phonepe revenue is only 1/4th of Paytm’s. This is because Paytm focuses on P2M transactions. Phonepe has more consumer UPI txns which doesnt have revenue.

Look at soundboxes deployed by these companies - that is, the merchant side:

Paytm - 30L as of Aug 2022

Bharatpe - 3L

Phonepe - 1L

This is a well planned strategy Paytm played to focus on merchants and give a whole ecosystem of solutions to them.

VSS comment about this in a recent conf call:

But what about the credit/collections risk? - They do not have credit risk as they dont carry the loans on their BL. However they have collection risk. Which they are executing the collection side also amazingly well. With very minimal loan loss. They even have lenders as customers only for collection side. They acquired CreditMate for this in 2017 and invested here really well. All collections are digital, no call center or manual effort.

Paytm’s near term target - 10Cr merchants and 50Cr payments customers

Vision - To bring Half-a-Billion Indians to the Mainstream Economy through Technology-led Financial Services

My conclusion:

Paytm’s distribution and tech are their strength, and of course the strong brand recall. They built an ecosystem around merchants. POS and payment solutions, cloud solutions for accounting, books, loyalty and so on. which other players dont have. This is Paytm’s moat. There could be many players who try to disrupt the UPI market further, but in my opinion this can only make acquisition costlier for Paytm, their distribution and the long headway for their lending and other services will still be their edge.

Digital lending is just 1% of TAM now. MSMEs are 30% of India’s GDP. 63mn in numbers. 20% of their credit needs satisfied by formal sector, 40% by informal, remaining 40% is a gap. Out of this 63mn, Paytm just reached 10%. In my thinking, Paytm is going to be a huge and significant player in the next growth leg of Indian economy. They are also going to build an inhouse general insurance arm, planning to spend 1000Cr in next 10 years. Other financial services like equity broking, mutual funds are being piloted.

Quite capable of pulling a 100x from here.

About the concerns discussed here:

- Buyback - They are sitting on a pile of 8000Cr cash. They are spending/investing aggressively in growing their business, and well on track to be cash flow positive next quarter. ESOPs expenditure will be done by 2026. Why keep excess cash then? Distribute it. I believe they did the right thing.

- Corporate governance - complex subsidiary structure - Berkshire Hathaway is an investor in Paytm, their only investment in India so far. This is my guarantee.

Their disclosures are top notch and as good as it gets. Monthly data published. Quarterly earnings release and PPT is so detailed and consistent, with all relevant KPIs explained.

I did not read up much about VSS before studying Paytm, for I might become a fanboy which could cloud my thought process. However reading through his intro remarks in the conf call scripts itself made me his fan. Clear, concise views about the business. I will add a few of his quotes in another post.

Disclosure: Invested, ~15% of India portfolio

10 Likes

A few quotes from VSS and the management, from recent few quarters, which shows their thought process and execution. Pardon me for the long post, but this gives a sneak peak into how they run the business:

-

Our bet is payments. Our bet is distributing credit, leveraging payments, data and access that we have.

-

I believe that payment is giving way to those customers and small businesses and merchants who did not have access, but deserved credit meaning people who could have had higher CIBIL score or could have got better credit pricing from a formal financial institution, these are the kinds of people who are getting access to large financial institutions (who are our lenders), and our marquee lenders are getting access to this new customer base. I believe that credit, which is in its infancy, has started showing that it is a long-term sustainable space, and is going to become a pretty large business for us. Our bet is payment. Our bet is distributing credit, leveraging payments, data and access that we have.

-

You will see that merchant side device-led strategy where merchants are paying for cloud, and for device subscriptions and rental is growing and it shows in this quarter’s number also.

-

Our number of loans is something that we index ourselves on because the entire focus of the management team, of the credit business is to see that we’re getting more and more merchants and consumers is the mainstream ecosystem of getting credit.

-

Our model is very simple: we are distributors and marketers of loans, we do servicing of loans and we also have collections outsourcing agreement with a lending partner for most of our businesses, through which we have an upside that we get if the portfolio was to perform better than what the lender would expect to.

-

The expected credit loss, the number that we’re quoting here, is a number, that cumulatively we understand from our partners is what they’re providing for. I can only say this here in utmost confidence, so far what we’ve seen over the last year on a static pool basis that the net credit loss is much lower than expected credit loss being called out here by our partners

-

marketing costs to drive MTU 40% yoy, employee costs to drive 8L-1mn devices per qtr and tech

-

we have our own collections infrastructure, which is a company called CreditMate, which is a 100% subsidiary of Paytm. three parts of collections. We do pre EMI delinquency management, which is using the entire Paytm app infrastructure to reach out to consumers and merchants far more effectively, and smartly to make them and to nudge them to make a payment in time. second part, which is a digital engagement model, which has zero cost to us because all of it is led by technology, both in terms of digital engagement of the app, and bot engagement, which is done through either the app or through our progressive and predictive dialing infrastructure that we have. A very, very small percentage of our consumers and merchants have a physical leg of collection for which we have more than 100 people on rolls of Paytm, which number hasn’t been growing.

-

at the time we hit breakeven, I do expect that both in areas like lending commerce and cloud and so on, we would have still barely scratched the surface and these are large profit pools, large opportunities, and very profitable for us.

-

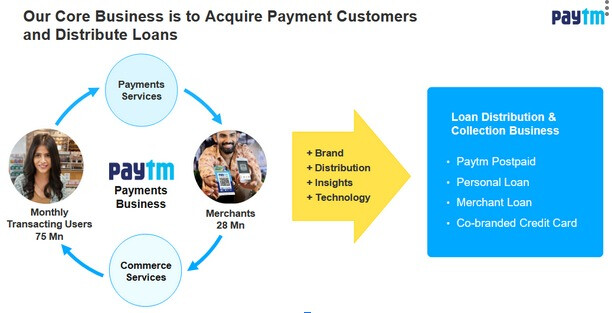

If you see here, we have stated that our core business is to acquire payment customers and distribute loans. Everything else has to amplify either the ability to acquire payment customers, or amplify the ability and capabilities of disbursing loans. In our payments business, as you see, we acquire consumers who in turn, work with merchants and in other words, make payments to the merchants. And merchants in turn, give commerce services to the consumers. This business model, where we have more than 75 million monthly transacting users as of June 2022 and 28 million merchants, allows us to create a brand, distribution, insight and technology that allows us to create an incredible loan distribution and collections business.

-

we acquire customers, and we had 80 million transacting customers, and these customers in turn bring us merchants and we have 30 million merchants who in turn work and give commerce services to consumers. This makes our core business model to acquire customers on payments. And in turn, because this gives us insight, ability to distribute and a great brand name, we work with our lenders to distribute credit. over the last four quarters, we have trimmed, since the IPO, a tremendous amount of businesses and focused on key business areas and pruned many business line items and made it very clean and clear that we acquire customers for payments and distribute loans from our credit partners"

-

the business model is very much aligned with how the regulator sees it. We continue to believe that this loan disbursement and collection business for India will play an important role in democratizing credit. If you remember, at one point in time, RBI leveraged public sector banks, then created private sector banks, then created NBFCs. Through this, different buckets of credit requirements were satisfied. Today, digital lenders, lending service providers or LSPs as RBI calls them, is what Paytm is here for and it will generate and create new opportunities for disbursing digital credit.

-

the best part is that our focus on merchant payments instead of focusing on consumer led UPI payment has created a scalable UPI revenue model in subscription

-

we probably would have purged literally hundreds of various different kinds of merchants if they were not profitable or if they were not useful for us or generating some pain in the system.

-

Lending upsell which is now in my opinion a scalable opportunity and it doesn’t have any regulatory arbitrage and I am especially calling out this line because many credit businesses in the country or Fintechs have been built around some or other regulatory arbitrage. While what we have built is a mature business where the partners have a comfort of credit quality, the regulator has the comfort of the guideline and we have grown organically not acquiring or by making a desperate push of any kind of product in the market.

-

In fact our belief is that with the increase in the digital payment ecosystem in the country there will be market risk or different kind of frauds that would come in the system but I’m very confident with the quality of work Paytm is doing the right operation risk and compliance is a USP of our company and the attention that we are driving on the risk and fraud in the market will become a continued benchmark in the country

-

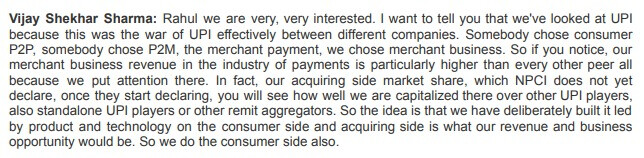

we are a merchants side business. We always call it payments when you are paying a merchant. So, yes, our P2P business numbers are not that great as a market share, we are very aware of it but at the same time we are proud to say when it comes to the merchant, whether consumer making payment to the merchant or merchant choosing a payment solution, Paytm is the market leader here.

6 Likes

Thank you so much for your post.

I have some questions regarding merchant data that PAYTM has and which it can use to properly judge a merchant and provide loans.

-

Whenever we pay a merchant using the QR code, Paytm get the details but when that money is transferred into the merchants Bank Account then even the bank gets the same details. Here the bank can use this data and then sell not only personal loans but all other types of products that the bank has to offer. How does PAYTM have an upper hand ?

-

The loans dispersed are not on PAYTM Balance Sheet, in case a default happens how does it impact Paytm and will it impact the bank and Paytm relation.

-

Personal Loans are risky and PAYTM does not have a track record in the lending business when we compare it with Banks and NBFC. How can we be sure that PAYTMs risk management is strong and when the credit cycles turn their default rate will remain low.

Thank you

2 Likes

- Whenever we pay a merchant using the QR code, Paytm get the details but when that money is transferred into the merchants Bank Account then even the bank gets the same details. Here the bank can use this data and then sell not only personal loans but all other types of products that the bank has to offer. How does PAYTM have an upper hand ?

I do not think it is about upper hand, banks have always had the edge (in finance/tech) e.g UPI as well but see who UPI leader are. It is about how you process data and what is your focus. Even though I think when paytm app is used by merchant they have bank account in paytm payment bank as they provide some benefits to merchant having bank account with them. Bank have their hands full with usual business and this type of innovation need focus and high amount effort when you can earn high ROE without much effort why you take path where you might need to lose money in short term and do more hard work - The loans dispersed are not on PAYTM Balance Sheet, in case a default happens how does it impact Paytm and will it impact the bank and Paytm relation.

It does not impact them directly, but they had to let go off their commission and it impacts their future disbursement with that specific lender/partner. - Personal Loans are risky and PAYTM does not have a track record in the lending business when we compare it with Banks and NBFC. How can we be sure that PAYTMs risk management is strong and when the credit cycles turn their default rate will remain low.

Here, you need to check avg. tenure of personal loan and merchant loan. In Merchant loan, they deduct some amount daily so it is safer than personal loan. As per their presentation or concall – personal loan avg. tenure is around 1-1.5 years so paytm collects loan it disburses in last May’22 (fully!) so it quickly reflects in book of lending partner. You should watch Suresh Ganapathy’s interview (same analyst who had given target of 400 since IPO – multiple downgrades in between). He was vey skeptical about loan growth as it is always easy to disburse but hard to get it back. Postpaid is only for 90 days, if i remember correctly.

Thanks!

4 Likes

-

Bank may get data, but at which contact point they push a loan? The merchant has to go to the bank or its app for some transaction, which could be once in a while. Whereas Paytm can do it easily from their digital interface touch points they have already made. Merchants have paytm business app and they use it very often, as far as I understand, they will get offers on it, for example. This is the benefit of a captive customer distribution and an ecosystem. For consumers, imagine once you make a transaction in Paytm, you get a simple prompt to use BNPL (paytm postpaid) for 30 days, who can refuse it?

-

If loans are defaulted and collections do not come there are two things - 1. Paytm loses the collection incentive - lending partners usually have a standard credit loss rate, say 5%, Whatever Paytm collects above that is their incentive (or a portion of it). 2. The partner will stop giving credit to Paytm, which reflects on its revenue straight away. Paytm has done a lot of work on the collection side, right from acquiring Creditmate in 2017 to develop the platform to building various touchpoints/nudges to take collections from the users.

-

Paytm does not give PL to every consumer straight away. They first extend paytm postpaid to a consumer who make payments on the paytm app, which is a BNPL for 30 days. This is how they credit qualify a user. Once the user pay back the postpaid, they will be extended with a PL offer. This will form 50% of PL users. The remaining who come to Paytm and request PLs straight, as far as i understand Paytm does some kind of credit qualification for them also.

But yes as you said, Paytm is vulnerable to credit cycles as it doesnt own the supply side. For eg, when interest rate goes high and credit tightens, lending partners might reduce or stop lending, which will affect Paytm’s revenues. But remember it is a cycle, when credit cycle loosens, these lenders and customers both will (have to) come back to Paytm.

Long term, I believe they will find ways to overcome these cycles by having long term supply agreements for example, which can mitigate this cyclicality. But this will be after reaching a sizeable book.

Hope this helps.

6 Likes

The Ken podcast on Paytm. Unlike it’s articles which are mostly behind paywall, this is free

2 Likes

was digging more details yesterday on PayTM. Few things I learnt:

-

Money making from payments business is extremely challenging - per transaction it makes approx 7 to 9 bps, and since UPI share keeps going up, it further will get reduced to 3 to 5 bps. One saving grace here is incentive from Govt. I have crossed checked payment margins for Infobeam Avenue (who owns CCAvenue) - they also have margins in 7 to 9 bps range right now.

-

Another saving grace is core payment processing charges are more or less flat over last 2-3 qtrs while transaction volume keeps shooting up. however since most of it is UPI, there is not much hope of operating leverage kicking in unless Govt makes UPI chargeable (at least not for next 12 months with elections around)

-

Merchant loans are more profitable for PayTM and have lower risk since it involves daily debit from total paytm transaction balance for the day (Unlike Paytm Postpaid or Personal loan which follow a monthly EMI cycle). This way PayTM gets early warning signal much faster and can deploy various strategies to nudge the Merchants to continue to pay in case of likelihood of default. However value of Merchant loans is still smaller compared to Personal Loan and PayTM Postpaid

-

Transaction charges from loan collection services are received only after loan portfolio is closed. So this will be back ended for now

-

Its employee costs are still going up at significant rate, they need to find a way to get control on the same.

-

Unless they get more lending partners, they will get constrained with the amount of money available for lending and that can become a dampener on loan growth targets. They recently onboarded Shriram Finance and have said they are in touch with 2-3 more lenders. If any big banks become lending partner for merchant loans, that will be game changing!

Just my 2 cents to aid understanding on the fundamental side of business!

13 Likes

Key points from Paytm’s conference call:

- Business Growth: Paytm’s business is heading in the right direction as per their vision. They see a significant technology potential and business opportunities in the coming years.

- Revenue Growth: Paytm has achieved a year-on-year revenue growth of 39%. The growth is primarily driven by the payment and financial services business, which is expanding significantly.

- Profit Margin Improvement: The company’s profit contribution margin has increased from 51% to 56%, mainly due to higher-margin payment and financial services.

- Free Cash Flow Positive: Paytm is on track to become free cash flow positive by the year-end, which means they can start generating free cash. Positive market conditions and revenue growth are supporting this outlook.

- Payments Business: The payments business is scaling up with improved profitability. Monthly transacting users have increased by 23% year-on-year, and merchant subscription business has more than doubled.

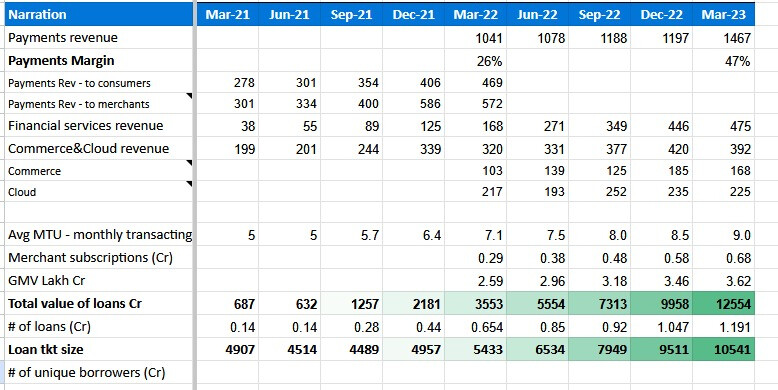

- Loan Distribution Business: Paytm’s loan distribution business has seen substantial growth, with loans distributed amounting to nearly INR 15,000 crores. They are focused on improving credit quality and have experienced positive trends.

- Commerce and Cloud Business: The commerce and cloud business has grown by 22% year-on-year, with co-branded credit cards and advertising driving growth. However, the commerce business growth has been slightly subdued due to factors like a decline in the movie industry.

- Growth Drivers: Paytm’s growth drivers include low penetration of mobile payments on the merchant side, technological innovations, UPI Lite, multi-bank and brands EMI aggregation, and new lending partnerships. They are also venturing into the retail bond investing business.

Overall, Paytm is optimistic about its growth prospects and believes it is well-positioned to take advantage of the opportunities in the market.

5 Likes