People were afraid to touch the stock when it crashed to 300, not much really has changed in the fundamentals but it’s always instructive to see how sentiments from “will not touch the stock” to “it will be 6-8x”. Only difference is that so called technical charts painted a very bad picture (which is the case during price falls) and now charts look damn good (after 3x move) which they did before the 60% crash earlier this year.

The stock is moving up because most of the new age tech stocks (Zomato, Swiggy etc.) have made very nice up-moves.

The fundamental issue I have for this stock is its ability to compete with Phonepay on any of the businesses. People don’t change banks generally because there is a bit of stickiness due to familiarity of branch staff, and the entire lock-in ecosystem of products such as FDs, Income Tax website integration, Salary account, any existing loan account and e-Nachs and so on…

However, its very easy to change an UPI application without much lock-ins and I believe that phonepay/google pay with unlimited capital and no hurry to make profits will eat paytm in the long run. A lot of business/revenue that Paytm does is because of the existence of the legacy Paytm app on a lot of people’s mobile phones (remember Paytm was the first and most popular wallets for a long time). However, everytime people will change phone, the Paytm will lose a fraction of customers. History also attests this fact. Paytm has consistently lost marketshare in almost all of the products it competes in. It has closed many divisions as well.

I believe its going to be very difficult for them to have any edge to maintain a leadership position in any of the product line in the long term and hence I doubt it’s ability to create long term stakeholder value.

PS: This is my personal view and I am very often wrong in my predictions.

Agree. I was just making a point that it’s easy to get carried away when stocks are going up in one direction. If technical charts 1 year ago didn’t predict 70% price fall, then how can they be reliable indicator for future prices if nothing has changed in the business model?

I always thought it was way too overvalued and didn’t understand the comparison with Zomato.

So I bought it at 300 purely on the basis of risk and reward which looked good. But at 1000 the issues of stretched valuations and lack of any clear moat take center stage and should make people cautious of jumping into the stock.

I partially agree with you but tax rate could also be significant consideration while deciding this kind of sale.

In IPO case (assuming it would happen in USA), so USA public would be buyer then proceed move to Japan and then WOS of Paytm and then Paytm holding company.

In this case, both seller (WOS of paytm) and buyer(Z holding) are from Japan and then proceed moves to direct to Indian holding company. I can’t be sure as i tried to find tax rate but this DTAA treaty are very complex between countries.

On top of it, Paytm has started giving DLG so it would need some money as backup (given VSS experience with market it is like “Dudh ka jala chhas bhi phu phuke pita hey”) and I do believe in long-term, they should think about co-lending (20-80) with lender.

PayPay is in news for IPO since 1.5 years at least and if you look at USA market environment, it might be time before that would happen but we can’t be sure as it all depends on Softbank’s intention and valuation (see MobiKwik IPO for valuation and subscription).

SoftBank has previously set a PayPay listing as a goal, with one executive saying in November it was worth just under 1 trillion yen ($7.17 billion). That the conglomerate is considering a U.S. listing has not been previously reported.

Given the valuation (not considering time value), looks fair.

Thanks!

Disc. In core portfolio and one of top holding.

Is $7.17 billion valuation true? If so, why is Paytm’s calculated stake only at ~3.x% instead of 5.4% as previously disclosed?

Why did Paytm disclose the valuation of PayPay and not the stake? My hypothesis is that SoftBank wanted Paytm’s stake for cheaper than the $7 bn valuation, but at the same time it didn’t want to benchmark PayPay’s valuation on a lower valuation right before the IPO. So there seem to me that there are some financial shenanigans here which allowed both, for SoftBank to get Paytm’s stake for cheaper + to publicly still have the valuation at $7 bn.

The obvious question: even if there are no financial shenanigans at play here and I assume best intentions. Paytm has more than a billion dollars in cash in the bank. What’s $270 million more going to do?

Summary of Current Challenges and Future Outlook from Investor Presentation:

Current Challenges:

Revenue Decline in Key Segments:

Payment services revenue saw a year-over-year (YoY) decline of 40%.

Marketing services revenue dropped by 48% YoY.

Financial services revenue decreased by 17% YoY due to tightening risk policies by lenders.

Operating Losses:

Despite improvement, the company recorded an EBITDA before ESOP cost of ₹(41) Cr and a PAT of ₹(208) Cr.

Higher Costs for New Initiatives:

Default Loss Guarantee (DLG) program saw a doubling of disbursements, increasing associated costs and reducing margins.

Customer and Merchant Acquisition Costs:

Indirect expenses remain substantial, although reduced YoY. Marketing costs and employee expenses are expected to rise as expansion continues in tier-2 and tier-3 cities.

Regulatory Constraints:

Awaiting Reserve Bank of India (RBI) approval for onboarding new online merchants under the payment aggregator license.

Slower Growth in Consumer Credit Products:

Adoption of RuPay Credit Card on UPI is slower than expected, impacting revenue opportunities.

Future Outlook:

Focus on Growth in MSME Segment:

Targeting India’s 10 Cr merchants with tailored digital payment solutions and financial services.

Expanding distribution networks in tier-2 and tier-3 cities.

Revenue Diversification:

Emphasis on subscription-based revenue through devices and value-added services.

Monetization of marketing services like advertising, ticketing, and gift vouchers.

Technological Advancements:

Leveraging AI for operational efficiency and cost reduction.

Innovating with new hardware and software products to enhance merchant services.

International Expansion:

Exploring global opportunities through partnerships, strategic investments, and local licensing in similar markets.

Loan Distribution Growth:

Scaling up merchant loans with higher repeat customer rates and increasing disbursements under the DLG model.

Profitability Goals:

Continued reduction in indirect costs and increased contribution margins to move toward profitability.

Lower expected ESOP costs and capex due to refurbished device redeployment.

The company is strategically focusing on reducing costs, diversifying revenue streams, and leveraging technology to strengthen its position in the competitive fintech space.

I have been buying items from kirana stores and last year he used paytm app and told that it was free to use. This year he is replacing the paytm QR code with direct bank QR code.

Today he received around 1700 in paytm app and he needs to pay Rs 0.11 to get the amount into his bank account. Also whatever received from the paytm app, will be availble in bank only from tomorrow. That is what he told.

[Loading Google Sheets]

Can someone have a look if something is off here as poer the available info. or the stock is really a doubler from here in 3 years

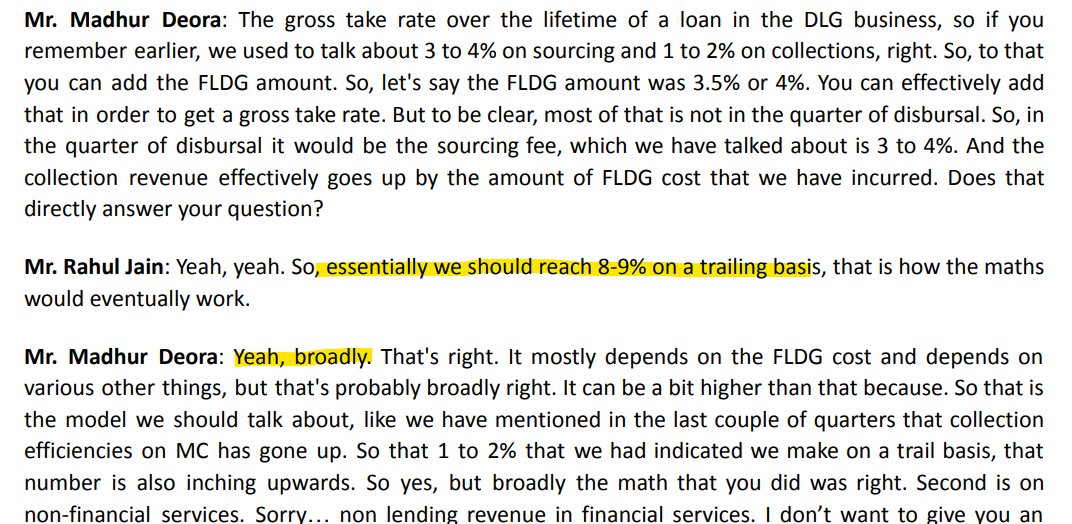

Very reasonable estimate and quite achievable in base case scenario however such high take rate for loan portfolio is not quite sustainable once lending portfolio mature

The only thing I haven’t been able to get around this Gross take rate. Why do they record 8-9% gross take rate when they only get 3-4% on sourcing and 1-2% on collection that to which comes in next 3-4 quarters ??

You can see more details in Q3FY25 concall. It should go up to 8-9% under FLDG agreement. I have one doubt for DLG setup, does first first 5% loss is taken under this guarantee or it is revoked when ECL is above expected range. Thanks!

I do understand that. But the reason is why would you add FLDG cost as your income first and then deduct it as a cost when most of it is going to be incurred anyway and call it Gross Take Rate. Why Can’t they just recognize sourcing income which is the actual inflow and then subsequently record the collection revenue and reduce the FLDG cost if any previous provisions are written back ??

More than that how is the Net margin similar in FLDG vs non FLDG model ?? effectively you are adding the FLDG cost to the revenue in the name of Gross take rate and then reducing the same amount in the cost line item. which most of it is not going to come back if ECL is 4-5% and saying that my Net Margins are 4-5% similar to a case where there is no FLDG but effectively it is way lesser because FLDG is a real cost

Lets’ assume a case - they are getting 4% Sourcing margin and providing 4.5% FLDG cost (which is an actual cash (Outflow as they have to provide it in a lien marked FD format). If lets say even 3.5% of that is revoked by the lender, Paytm’s effective net Inflow will be Sourcing Margin - FLDG cost + whatever the the collection revenue they get (lets assume 1.5%) which is equal to Net margin of 2% vs a case where they just getting Sourcing margin of 4% + collection of 1-2% withput providing any FLDG. Net margin comes out to be 5-6% in the second case. even in the distribution only model their Net margin would be 4% (Sourcing Margin) and they won’t have to pay any FLDG effectively having higher Net margin than FLDG model (2%)

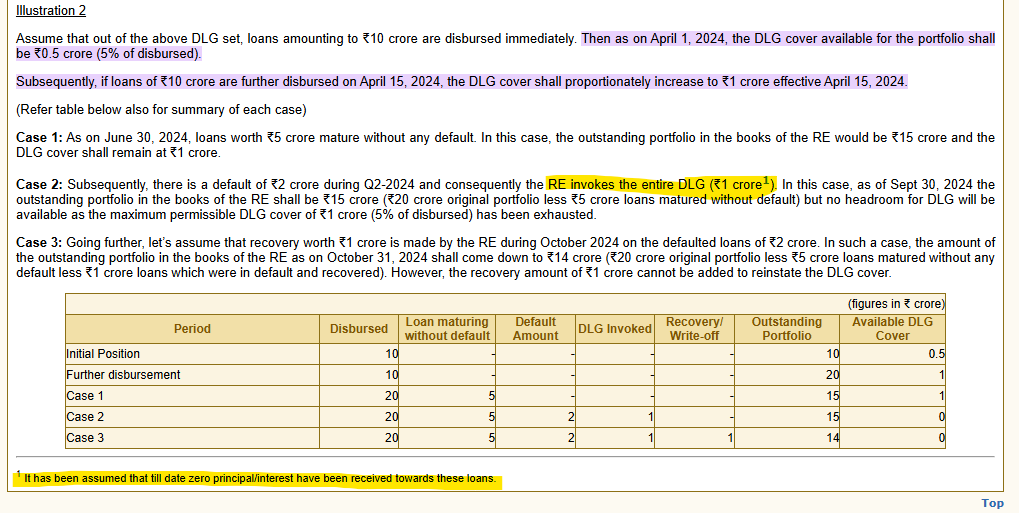

to answer your question I will attach a simple Excerpt from RBI

[Reserve Bank of India]

Though I feel that I am missing something, I think if you are right and RE invokes DLG at first loss they face any portfolio then there would be no benefit of becoming DSA as you might be aware these are high interest loan (than bank) and somewhat questionable credit - all that backed in interest loan so RE is expecting some loans to go NPA and my believe that DLG will be invoked once that limit is breached as RE will hold digital DSA for giving bad clients. please feel free to correct me.