what does this mean for the company? is it good or bad ?

source: https://x.com/CNBCTV18Live/status/1912503301829951505/photo/1

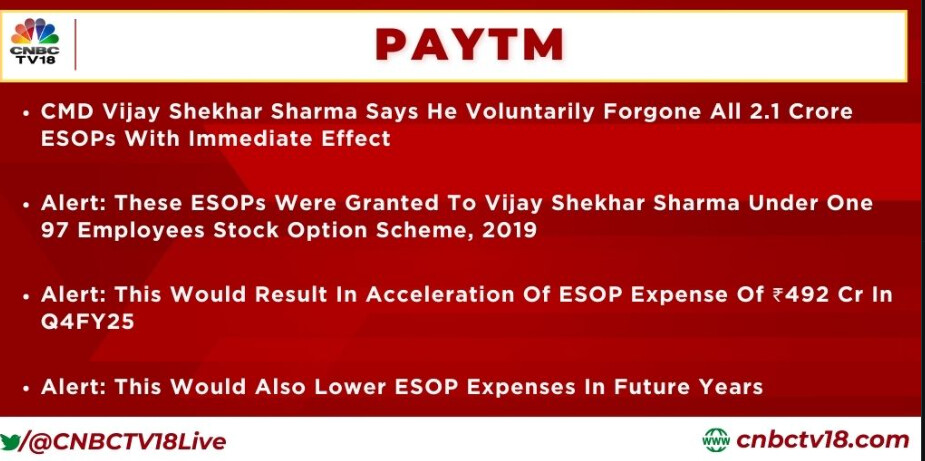

what does this mean for the company? is it good or bad ?

It’s good. However note that it’s not absolute voluntarily, it was recommanded by SEBI.

Anyway it’s positive. It saves esop future cost and will be eps accertive in long term (if VSS taken 2.1 cr shares, share count will have increased, hence eps down). Their cancellation simply means future dilution is avoided.

However in Q4 FY2025 the ₹492 crore one-time expense will lower net profit temporarily. As per accounting rules: if unvested ESOPs are cancelled voluntarily by the employee, then the entire remaining unamortized cost must be booked immediately.

This should also reverse the expense booked in earlier period. right?

No. As per my understanding esop expenses once booked, will remain in book.

It should be, if they are unvested options (in perfect world!) but they are not for reasons below (from Gemini AI).

The reversal of past expenses for cancelled unvested ESOPs is related to the accounting treatment of the remaining unrecognized compensation, while the expenses already recognized are not reversed because they reflect the service provided by the employee before the cancellation.

As company did not mention that whether these were vested or unvested option (as IPO price as performance criteria was added later).

So this Q4FY25 also PAT -ve. whenever they are near to PAT - something just happens!!!

Thanks!

Absolutely. Perplexity explains:

Paytm founder and CEO Vijay Shekhar Sharma’s decision to forego 21 million ESOPs is primarily a result of regulatory pressure from the Securities and Exchange Board of India (SEBI), rather than an act of charity.

Context and Regulatory Background:

Financial and Corporate Impact:

In summary, Vijay Shekhar Sharma’s foregone ESOPs are a direct consequence of SEBI’s regulatory nudge and settlement process, aimed at rectifying non-compliance in ESOP issuance rules, rather than an act of charity.

Answer from Perplexity: https://www.perplexity.ai/search/paytm-s-vss-foregone-esops-is-Sk6LVlTqSYyRvBjViYqweA

How should one view the founder and CEO of Paytm?

Does the CEO work in the interest of the shareholders?

Disclaimer: Invested

Right. In addition to the fact that SEBI nudged the decision and nothing about it was “voluntary”, there are also consequence of this cancellation on the balance sheet.

Will the ESOP cancellation be written back? Logically it should, but accounting rules do NOT usually allow a writeback of previously expensed ESOP charges.

This was a negative which became a positive by virtue of correction of the past negative. Lol.

It’s be interesting to see how this impacts the P&L going forward.

Disclosure: Not invested.

Hello @rpattabi,

I have an opinion on why ESOPs are lucrative for founders of VC backed companies post the IPO.

When you run a company where you do not have any deep technological moat then you have to build brand and distribution. And this is very common. A vast majority of companies are not doing something which only they can do. Some exceptions are ASML which builds EUV machines that are then needed by TSMC to manufacture chips. ASML is a monopoly because they are the only ones who know how to build such a machine. They are not a monopoly because they are the best at branding or distribution.

Also, when you run a company which can’t enjoy a location advantage, then again you need to spend a lot of money in advertising and marketing so that you get distribution before your competitors. For example if you are a five star hotel like Taj Mansingh in the center of New Delhi. You don’t have to bother a lot about distribution. You are centrally located. No one can come and build a hotel on top of your hotel. Your moat is your location. Of course there are other moats like depreciation because your competitor would have to pay more to build a hotel now since the cost of construction has gone up a lot since the Taj was built 50 years back.

So, this brings us to VC backed companies and especially those VC backed companies that are selling a digital product. For example Paytm sells mobile recharges. Or Bookmyshow which sells movie tickets digitally. Put yourselves in the shoes of this founder. If he did not spend money in advertising and marketing, then any of his competitor would come and take away the customer. This is what Google Pay did when they launched. Do you remember getting hundreds of rupees of cashback when Google Pay came in? What can the entrepreneur do to compete with that?

One option is you just sit back and hope that the customer would stick to you for a mobile recharge even though he is going to get a cashback from Google Pay. That is never going to happen. It is irrational for the customer to behave like this. Therefore the only sensible option for any such entrepreneur would be to raise VC money and try to become the biggest. Please remember he can’t raise debt. Unlike a hotel or steel manufacturer there is no appreciating collateral to be offered to a lender here. What will you tell the bank? Please give me debt because I want to spend it on marketing and if you want collateral take my intellectual property as collateral? Would any bank give you big debt on this? A steel manufacturer can always offer his land or/and plant and machinery. This is not an option for an entrepreneur building a digital product.

Also, people like Vijay Shekhar Sharma do not come from a rich family background. They can’t raise money from their parents or uncles because there is no money in the first place for them to offer. So no money from family, no money from banks. And you are in a business which has a big target market but they dont even know about you. Think about how you did your mobile recharge in 2008. Was it efficient? Or how you paid your electricity bill? Do you remember the queues?

Or try booking tatkal on IRCTC even today. How is the experience? For a massive population like India digital businesses have so much societal value. But you need an entrepreneur who is willing to play this risky game. And he needs to convince others to fund him and share the risk with him. And those others are VCs. And what do VCs want? They want equity. Lots and lots of it. Because obviously they are putting their money at risk. Lots and lots of it. For what? For the hope that you will build something which would be useful to a huge population in the future and therefore they agree to spend a lot of money on what? Advertising and marketing.

By the time you get to the IPO the founder is drastically diluted. Vijay is unique in India. He managed to have some equity at the time of IPO. Deepinder from Zomato had 5% and Yashish from Policy Bazaar also had 5%.

This is not unique to India. All VC backed businesses leave the founder with limited equity by the time of the IPO. And even western entrepreneurs try for getting big ESOP rewards that are linked to performance post IPO. Elon Musk is the biggest example. His company was going through hell and he said I will get my ESOPs if we cross 650 billion in market cap. Reed Hastings of Netflix also got a lot of ESOPs post Netflix IPO in 2002. Multiple times of his annual salary. Vijay had also announced in 2022 that he would not get his ESOPs till the time the Paytm stock comes back to its IPO price.

In my opinion ESOPs are a much better way to reward the management as compared to big fat salaries and perks. And if the management is putting that ESOP behind a big goal then all the better. These are not founders with rich forefathers who can keep buying shares from the open market. Nor are they in a sector with a license monopoly. On the other hand they are in sectors where the regulator will actively enact regulation to avoid any kind of market concentration.

++ In one of interview, VSS mentioned that he had to put 4% of personal holding in ESOP pool when paytm started in 2011 so he was getting back this exact 4%. the major mistake they have made in IPO pricing but he accepted this mistake many times in public forum. Thanks!

In the last 10-15 years, the most innovative (in the finserv sector) has been Paytm", says sameer nigam, CEO, PhonePe.

Watch here: youtu.be/RcGyn1j2ZGo

Nice to know this…

Disc: Invested

Paytm Options Volume Spikes as Stock Slides on Policy Setback

Paytm’s options activity surged to its highest level since January after its shares dropped sharply. The decline followed comments from India’s finance ministry indicating there is no current plan to allow merchant fees on digital transactions—a potential revenue lever for the payments firm.

Approximately 120.4k call and 85.5k put contracts traded, driving total options volume to 6.6x the 20-day average.

June ₹900 calls were the most actively traded, followed by June ₹880 puts and ₹940 calls.

The stock fell as much as 10%, hitting a low of ₹864.20.