Let’s speak about Paytm as an opportunity or better to avoid it as a falling knife. Much has been said here in this VP thread…

- Date: 17th Feb 2024

- Valuation: Rs 21,677 cr

- Price/Book value: 1.75x

- 3y revenue growth: 24.6%

- 3y EPS growth: 24.5%

Paytm has quickly become a special situation opportunity - is it a blessing in disguise or an absolute avoid is the question?

In such cases, I always find exploring the narrative vs evidence useful to create multiple scenarios. let’s explore…

Scenario 1: PPB is not rescued, but a third party steps in to settle the UPI transactions. In this case, the wallet business for Paytm is entirely lost. Here, the impact on EBITDA could be Rs 300-500 crore as per the management. Some analysts feel this will hurt its ability to draw on an otherwise large customer base to up-sell its financial products. Others feel Paytm should be able to build the lost base back over time, even though it will have to live with the immediate financial jolt. This is because its rivals like BharatPe and PhonePe too have a similar structure – they do not own a bank like Paytm does.

- Impact: Paytm might lose its edge of having a bank underneath and become very much like PhonePe; then the bet is on management execution

- Action - tracking position; say 1% of portfolio

Scenario 2: PPB is rescued by other banks, both wallets business and UPI transactions are saved. In this case, the impact on EBITDA could be lower than Rs 300-500 crore. The loss of time and opportunity cost till a bank steps in to rescue both parts will impact the company.

- Impact: If other banks buy-out PPBL, then over-time CAN Paytm will retain much of the edge than it’s peers? Not sure, but worth exploring

- Action - staggered position sizing

Scenario 3: No other banks step in to salvage the situation, not even the UPI part. Paytm’s core proposition will be impacted. As users switch platforms, this can potentially threaten Paytm’s existence.

- Impact: Terminal value can be at risk

- Action - absolute avoid for me

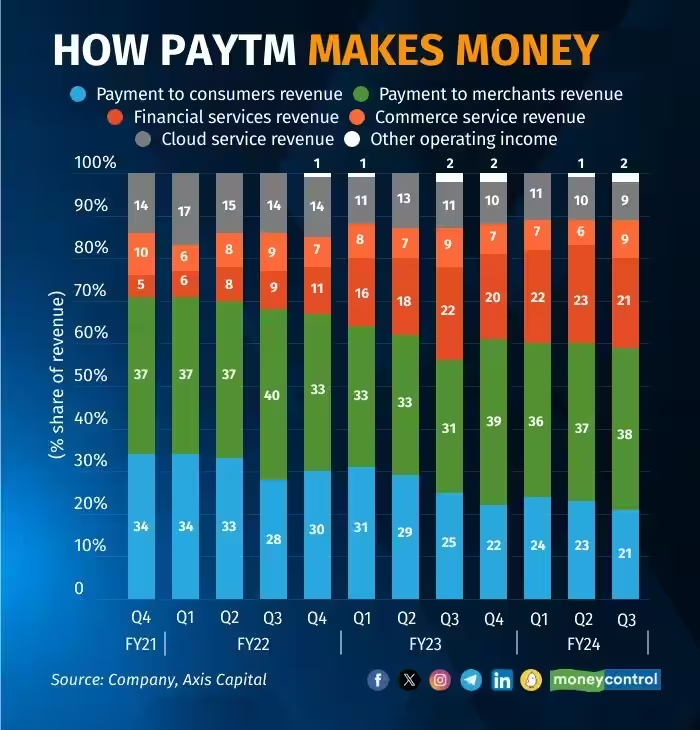

Here’s how Paytm makes money and its subsequent split across segments:

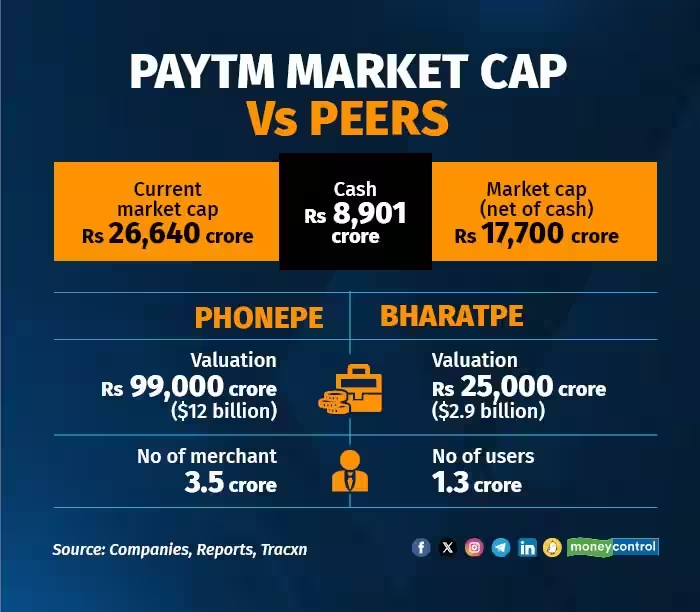

Here’s how Paytm’s m-cap vs other pvt players:

Possibilities:

-

Finds a new sponsor bank (wallet business can be saved) - the impact is minimized (Axis seems to have responded)

-

PPBL is sold to some big banks (ICICI, Axis, HDFC), then the competitive advantage of Patym could be retained (wait and watch)

What to keep an eye on:

-

Case 1: Any bank coming to rescue as a “sponsor bank” for scenario 1 to play out?

-

Case 2: Any bank showing interest in buying out PPBL?

-

Case 3: RBI giving an extension to the 29th Feb deadline could be an indicator (happened as extended till March 15th from Feb 29th)

@rpattabi @ValueV any thoughts?

PS - wrote this note early this week. realized some of the above are getting executed. hence sharing my pvt notes publicly to draw more eyes/criticism (hopefully constructive from the community). also not on Paytm’s main thread, so this discussion which has many speculative points remains here.

Disclaimer: No position. Also, I am not a financial advisor nor a SEBI registered advisor. The content shared here is only for learning purposes. So please use your discretion to make any buy/sell decision and not use the above as a recommendation.