try Jokey international…the best of the lot

true, but i feel consolidation period will start in some months and left and right hand chart would start looking same before it turns for long term. Only going by purely chart way.

I don’t think anyone can dispute the greatness of Page Industries.

Cash is oozing out of its nose & ears. Lots & lots of cash. With profits multiplying, working capital under tight control & hardly any capex requirement, it doesn’t know what to do with the excess cash.

As a ratio, capex constituted 96% of net profit in 2008. In 2019, it fell to just 10% (partly due to outsourcing of manufacturing; now stands at around 27%)

| Rs cr | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Net profit | 394 | 347 | 266 | 232 | 196 | 154 | 113 | 90 | 59 | 40 | 32 | 24 |

| Capex | 38 | 57 | 62 | 26 | 55 | 53 | 45 | 27 | 29 | 25 | 31 | 23 |

| Capex/NP | 10% | 16% | 23% | 11% | 28% | 34% | 40% | 30% | 48% | 62% | 96% | 96% |

And what is Page doing with the excess cash? Giving out huge dividends. Up 34x in 12 years

| Rs/share | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dividend | 344 | 131 | 97 | 85 | 72 | 60 | 50 | 37 | 26 | 21 | 17 | 10 |

( no of equity shares have remained constant; so easy to compare over years)

And how is the business doing? Low days receivables vis a vis its competitors provide an idea of Page’s market position & the strength of its brand.

| FY2019 | Page | Lux | Dollar | Rupa | Aditya Birla Fashion |

|---|---|---|---|---|---|

| Days receivables | 16 | 111 | 123 | 125 | 35* |

*For entire company; breakup for innerwear business not available

Above shows that competitors cannot survive without giving a high credit period. The only real competitor emerging is supposedly Aditya Birla Fashion through its Van Heusen brand.

Based on limited disclosed information, Van Heusen innerwear division together with the Global Brands division which includes Ted Baker, Hackett, Ralph Lauren reported Q1 FY2020 sales of Rs 125 cr (up 76%) but an ebitda loss of Rs 22 cr during the Q. As per a Motilal Oswal report, full year 2019 innerwear sales for Van Heusen were around Rs 200 cr & it hopes to breakeven in FY2021. Call this competition???

Any competitor must be salivating looking at Page’s return ratios. Many have tried to attack Page’s market position in the premium innerwear segment but have either given up (Fruit of the Loom could not face the heat & exited India in 2012; has now re-entered with Rupa) or simply reconciled to running a mediocre business. Page’s combination of a strong brand & distribution network seems impregnable.

| FY2019 | Page | Lux | Dollar | Rupa | Aditya Birla Fashion* |

|---|---|---|---|---|---|

| RoCE | 72% | 27% | 23% | 19% | 10% |

*For entire company

On valuation.

| Page | Lux | Dollar | Rupa | Aditya Birla Fashion | |

|---|---|---|---|---|---|

| MCap Rs cr | 27,778 | 3,062 | 1,010 | 1,456 | 16,311 |

| P/E | 72 | 30 | 13 | 16 | 49 |

Frankly, for Page to command such valuations, it can’t have 12% sales growth, 14% net profit growth & 6% volume growth (FY2019). Page MUST grow faster.

But is this the new normal for Page? Is the India consumption story over? Or is the PE ratio optically high due to a slowing economy & thus a temporarily low pat number. Does the market know something we don’t?

The past clearly looks great for Page. Unfortunately, markets look at where you are going rather than where you’re coming from.

| Rs cr | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 2852 | 2552 | 2130 | 1796 | 1543 | 1188 | 863 | 683 | 492 | 339 | 255 | 192 |

| % growth | 12% | 20% | 19% | 16% | 30% | 38% | 26% | 39% | 45% | 33% | 33% | 41% |

| Net profit | 394 | 347 | 266 | 232 | 196 | 154 | 113 | 90 | 59 | 40 | 32 | 24 |

| % growth | 14% | 30% | 15% | 18% | 27% | 36% | 26% | 53% | 48% | 25% | 33% | 41% |

Page has now entered the children wear segment with its Jockey Junior brand (target audience of 15.5 mln; largely catered by unorganized sector). Speedo’s growth has disappointed. Where else will growth come from?

The jury is still out whether the Page story is over or is it just taking a breather!

Your guess?

Sources:

-

Press Release by company (August 6, 2019). Separate numbers for just Van Heusen innerwear division not provided

-

Motilal Oswal Report on Aditya Birla Fashion (May 15, 2019)

24 Likes

In the last quarterly call, management talked about overall slowdown that affected the sales, but at the same time talked on 2 points

- They are working really hard on Jockey Junior brand, right from creating completely separate sales organization which brings accountability at the brand level.

- They said that it is a deja vu feeling for them when worked on original Jockey brand and excitement of making something really big.

From the call, I felt management has the hunger to grow much faster.

@Multiplier777, you have done very elaborate analysis, thanks for that, with this kind of cash I believe they will go all out to create a very successful story around Junior brand.

Disclosure - Invested since last 8 years.

6 Likes

Page Industries Q2FY20 Concall Summary

Business Updates

- Revenue growth rate of 12% and volume growth rate of 9% yoy

- The target market is of 150 million consumers and penetration level stands at around 20%

- The premium market is growing in double digits

- The management is continuing on plans of doubling capacity from 260 million pieces annually over next 4-5 years

- The management is pushing hard on the athleisure side of business and kids wear area is also a key focus area

- The marketing initiatives will be focused towards “Jockey Junior” segment

Participants

IIFL

Concept Invest

Systematix

Anived PMS

Goldman Sachs

Credit Suisse

Naredi Investments

Kotak Mutual Fund

ASK Investments

Kotak Securities

Alphaccurate

Birla Mutual Fund

Shubkam Ventures

QnA

- Growth in all segments have been encouraging and all verticals of business are under penetrated

- Inventory levels have been maintained at similar levels with 1 month of raw materials

- The EBITDA margins will remain at similar past levels of around 21% over FY20. The management is not concerned about maintaining EBITDA margins

- The business is very labor intensive and since managing a very big taskforce is a challenge have started hedging a little by getting 20-30% of production outsourced with a quality manager appointed by the company

- The export sales are very negligible currently and in the long run the sales wont contribute more than 3-4% of the total revenues

- The price hike of 3-5% will happen as per last years

- The salaries and bonuses were slightly higher because the company is building up team on marketing side

- The premium products have been growing at a very healthy rate

- The “Jockey Junior” is a key focus area and the company has setup a 100 member strong team for this segment

- The liquidity issue still persists and footfalls are still far below normal across its EBO’s

- There has been no change in distributor level margin/incentive in the last quarter

- The company has installed automatic replenishment system across 22% of its distributors at present which replenishes inventory automatically at distributor level

- This has led to distributors only ordering the necessary products where inventory is low at their end

- The company has 3000 distributors and plans to install this system across 100% of distributors in a year’s time

- The “Speedo” business is poised for decent growth going forward

- The management and company is geared towards growing at 20% plus but the market has not been supportive and demand has been tepid

- The growth rate in ecommerce is around 5-6 times the growth rate in the other course of business

- The company was present in kids segment since inception but this is the first time that the company is single mindedly focusing on kids wear segment with more designs and focused departments managing marketing and operations

- There are over 150 distributors who have signed up for the kids business

- The kids wear is present across 7000 plus stores

- There are no plans of reducing incentives for distributors going forward and the management would want them to grow equally with the company and be happy with the brand

6 Likes

Few points to add

- Speedo has degrown by 15% , no concrete explanation on revival

- ECom channel growing multifold to other channels

2.ARS will take 2 qtrs to stabilize and an year to rollout to majority of distributors ( using 80:20 principles to rollout) - No intention to reduce distributors margins( currently 3.75%)once ARS driven RoI kicks in and expand distributors margins - kudos to mgmt

Overall positive tone with dependence on demand scenario revival rider

1 Like

was there any discussion on the % of online sales in the overall pie?

what is the view of the management in increasing this? given that the first bunch of customers are always online buyers- variety, comfort of ordering from house, some discounts as well( from jockey website, amazon,flipkart etc).

Good to know that they are putting more energy into kids wear now.

Competition wise, there is no major player with all India supply chain in this section.

1 Like

There wasn’t any discussion on where online sales stands as a percentage of sales as on today or whee the management wants to take it from here onwards. They only answered that their sales in online segment are growing at 5-6x their usual sales.

1 Like

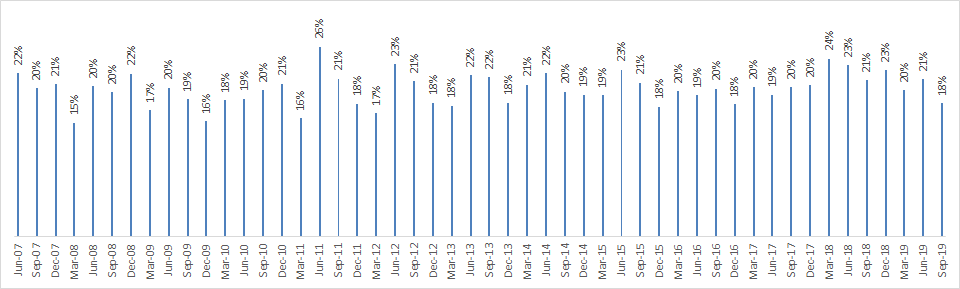

EBIT margins for every quarter since its listing. If you want long term margin stability, then page is a good example. No wonder it trades at an elevated PE

9 Likes

Great info. Can I understand how you extracted this info. Is it from screener? Thanks

Regards,

Matt

1 Like

Partly Screener and mostly exchange filings

1 Like

I have analysed this stock a lot…but seems it has lost it mojo…a scuttlebutt of the stores provide a not so encouraging story(not much refresh of the merchandise,I have been seeing the same t-shirts/boxers for the last one year), the revenue growth has been below average for the last 4-5 quarters. Not to mention, there is another player(Van Heusen) which started from scratch and is eating away incremental growth anticipated by Page. Its a clear case now of a stock whose market cap is getting close to the market size of the entire industry.When the market cap of the leader gets close to the entire market size(revenue) of the sector, it sends a definite sign pf overvaluation.So, no matter how PMS managers convince(because it is their top holding), I would consider this as a past glory.

I specifically wanted to see how their kids section’s variety is in the stores, but compared to others kids players, they have minimal range, and that too starts from age 5 yrs onwards…could not figure out the commentary that the promoters are giving about the aspirations in the junior segment

10 Likes

Your point of elevated valuation is valid.

The management has been talking about Jockey Junior from last 2 quarters.

I think we should give another 3-4 quarters to see if this story has enough potential for the stock to sustain at this valuation or to go further…

PAGE INDUSTRIES LIMITED CHANNEL CHECK report by Mangal Keshav Securities Limited

The sales traction for Jockey is healthy and it has maintained its market leadership. Jockey’s products are utilitarian and not exposed to the vagaries of fashion as is the case with other apparel categories.

Jockey has a more than 50% market share in innerwear and athleisure.

Given Page’s market leadership and healthy financial performance, they see its net worth growing by 15% CAGR over the coming two years

The Report is attached. Page Industries Limited Channel Check.pdf (1.1 MB)

7 Likes

Q3FY20 Results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/22380a27-4238-45b0-a7fc-6ab197a78e8f.pdf

Cost of material to sales item #2.(a+b+c) is increasing

Dec-2019 46.83% (16636+16726+3817)/79380

Sep-2019 44% (17740+18769-2407)/77540

Dec-2018 42.9%(17927+16823-3064)/73832

1 Like

The issue is very high expectations since a long time. Investors are giving lofty valuations to the stock and putting unjustified pressure on the management to continue to deliver unsustainable rates of growth!

Even after this result and the pressure clearly evident, the market will continue to maintain the share price because lot of institutions are stuck at high prices. next few days there could be several broker reports initiating coverage and a strong buy using narratives like strong market share, base effect etc.

Retail investors should be very careful

11 Likes

Intent is not to trigger the “which is the better investment” debate but to just observe and document how the market appears to be calibrating to the business performance

Over the past few quarters we have seen growth slowing down across the industry. For Q3 Page Industries, Rupa & Co and Lux Industries each did 7-8% revenue growth but the market reaction to the stories has been very different. By no means is this a long enough period to come to conclusions but the market is always telling us something…

Page Industries which has a long term growth rate of 18-20% is struggling to do half of that right now. Valued at 23,000 Cr at a TTM PE of 60+

Lux Industries with a long term growth rate of 15% is managing to grow volumes in low double digits, valued at 4100 Cr and a TTM PE of 31 (after the merger of subsidiaries this will drop to 26-27)

Rupa & Co with a long term growth rate of 10% is valued at 1750 Cr at a TTM PE of just below 19

In terms of the quality of business the leader is very clear, but the best investment performance will be delivered by the company which manages to match/beat embedded expectations. Figuring out what those expectations are is the key exercise that determines investing success in the medium term if not the long term.

This is a real time case study that I am keenly watching over the next few years.

9 Likes

Page caters to totally different market segment when compared to Dollar or lux or Rupa. Hence the same cannot be compared.

Stocks like page, eicher, marico, bandhan bank are now in a spot becoz forecasting their future growth is rather tricky.

The last several months, “quality” is moving up since quality rather than valuation is taken as the benchmark for value.

For the retail investor, page is a clear avoid for the time being. Better to pay high valuations for the hdfcs and the kotaks of the world.

It appears like market is now completely favouristic towards quality companies who are showing earnings growth. A story like a Marico or a Page would never end so roughly within just a year or two (assuming no major disruption/competition in any of their businesses)

Earnings based investing is a big momentum trend, Page is a child of the same play (remember the jubilation in Aug 2018 when stock price almost hit 35000). This would obviously backfire when the engine stops growing according to the market estimate. Although I’m not defending the poor growth and the abysmal margins shown by Page in the recent quarter (s), innerwear is a very under-penetrated market and has a decent long term growth visibility. If I can remember correctly,Page has close to ~1.3 crore unique customers in the men’s innerwear segment. Considering the fact that more than 3/4th of our country is still below the average GDP per capita, many people can migrate from “poor” to “middle class”. That would be a fantastic opportunity for someone like Page. If you’re hopeful of India growing and our population drifting to middle class, one-two year underperformance of Page can be pardoned

2 Likes