Indeed very curious to see the future growth pattern for Page.

my hypothesis (qualitative)

Mid to long term volume growth will likely be more influenced by newer categories(Kids & atheletic - Page is vocal about it and pushing it) compared to mature categories(Mens, women), Innovation & quality is being expected which Page can handle well.

Advt & mktg cost will inch higher - new launches, broader portfolio etc, to be compensated by efficient supply chain and investments in digital(again page is vocal about it and using current scenario as opportunity) as well as working capital efficiency(again Page is in different league here)

Page is superior to competition in return ratios and likely to be so with innovation across value chain and not afraid of being first movers/mkt creator

It is anyone’s guess as to when economy will grow faster but at the end of day - Page makes something which is essential for end users, inventory optimization at channel is new norm and Page is conscious and adopting to it (tech and SCM).

while it is apparent that last decade(2005-2015) growth performance is unlikely to be delivered in coming decade - Can page do a Volume+price performance delivered in range of 15-20% growth - very likely (case has been in 2016-2019).

On valuation - around 40 PE would be ideal with decent MoS - but hey we are talking about Page and mkt may not easily give that opportunity.

@zygo23554 - shouldn’t PE/Growth should be seen along with Return ratios -

Even assuming same growth(although page has grown above industry) for all players Page return ratios would justify this valuation gaps?

I have been a user of page industries products for a decade now.Last month when I visited a big market in Noida, I found quite a few stockist not having page products , but has macho brand which in wholesale post discount was costing around 70% of page.I could make out they hv stopped stocking page and if I keep the prices in mind, even the other brands offered had a good value proposition.Foes it mean that shop keepers are getting better earnings from other brands than page and customers too switching over? In it’s true then page will not have past growth rates in sales &profit. In future.views invited

In this market where quality rather than valuation is being considered as a benchmark for value, is it the same whether it is a PE of 40 or say 400? If page is perceived to be a quality company and a safe stock, does it really matter what the PE the return ratios are so long as the value is perceived to be higher?

If at all the assumption is right that the company delivers very good growth over the next 5 years or 10 years, then can the buy be price agnostic similar to Avenue?

Yes, PE by itself is meaningless unless it is seen in context of growth, capital efficiency and longevity. Page obviously deserves a premium over all others but to what extent? This is where things get interesting and opinions can differ

My objective is to optimize the return I make from the investment rather than go with the best managed business in a segment. So the effort I need to put in is to find a bet that may not be as great a business as the best one but is under priced compared to what the business can potentially achieve.

I am over time drifting towards an approach where I look for expectation mismatches between the stock price and what the business can deliver. For this I either need to have an edge at understanding how the business pans out over the next few years, or the stock needs to be undervalued enough for me to be able to take a probabilistic bet and not bother about having an edge. By definition one cannot have this edge in many businesses, there are bound to be very few. I had this edge in HDFC AMC but not in Abbott India, though I did buy both (just to drive home this point) and the return I’ve made from both is similar as of date. For this very reason I was very happy buying an Abbott India at 35 PE but am not happy adding right now at CMP. Whereas an HDFC AMC I was happy buying at both 32 PE and 45 PE.

One can always pick and choose his battles based on his world view and his edge. It is as much about the individual as it is about the business.

Jockey now have a brand store on Paytm. I have ordered two times in last 3 months. You get 20-25% discount if you manage your purchase with-in 600-800. At least for Bangalore deliveries order get shipped from Jockey Bangalore address . Also packing material has Jockey embossed on it.

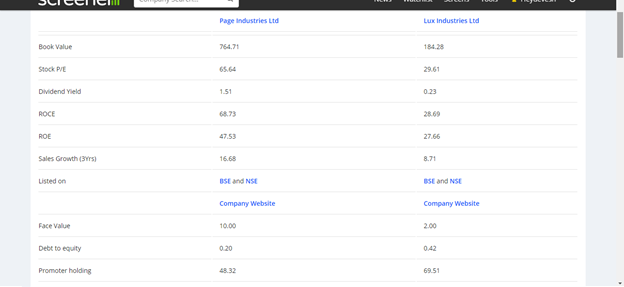

That is where hoping that Page premium quantitatively has to be double(or there about) of next guy given ratios are double or higher (ROCE/ROE) etc - unless going forward there is expectations of next guy to improve returns ratio meaningfully and catch up with Page.

Do you mind sharing your thought process here - given that HDFC AMC and industry AUM in general likely to be growing at 10% CAGR and HDFC may grow bottom-line at 15-20% CAGR - does that justifies 50PE for this growth? Would be helpful to hear your thoughts!!

A fund manager’s recent interview on ET is relevant.

He mentioned that passive flows + liquidity are chasing quality stocks which have limited float. The bubble is clearly evident and so far as this trend continues the stocks will continue making new highs. The markets can remain irrational longer than one can remain solvent.

At this point it is important to balance between quality and valuations-based-investment to avoid getting caught in any kind of bubble, whenever it might burst.

Interestingly one can better see the impact of compounding on a business that can use better cash flows to reduce debt, clean up balance sheet and hence improve PAT and ROE, rather than a business that is already at minimal debt and can at best pay out higher dividends. The next guy appears to be doing exactly that at a valuation than is less than 2X of Page Industries - which is what makes this a finely nuanced choice.

There is no concept of inventory or receivables management in the AMC business. That by itself takes away some much of operating complexity away as compared to any brick and mortar business. If Page wants to scale the women’s business to 1500 Cr and beyond, at some point of time we will see higher inventory since the no of SKU’s in women’s innerwear is at least 4X more than that in the men’s segment.

Also an AMC business is much more scalable than Page business model since it does not need capital or even people investments. In HDFC AMC I cannot see a singe P/L item that can scale faster than revenue growth, in 5 years time the operating margins will most likely be higher than they are today.

Point taken @zygo23554, with improving ratios Lux do stand a better chance of some re-rating as opposed to Page going anywhere much on upside.

However with single digit growth - whole industry is at risk with higher pressure on Page.

Also Page will need some heavylifting resulting in some pressure on return ratios in near future(Kids/women etc) and for short term Lux etc numbers will start to look better/closer (case in point last quarter where OPM were even higher for Lux)

Thanks for trigger - helped to look with a different lens.

i was a user of page industries jockey and speedo products but have stopped using them since a long time as the quality has deteriorated imho as compared to earlier . many brands give a guarantee in their swim goggles for a year or two while page industries dont give a warranty more than 15 days .

Results and investor call on 23-June. Looks like company has broken tradition of not speaking to investors for several years and coming up with concall. It’s anyones guess why they are doing so!

I’ve been following Page Industries for sometime now. I actually observed that most of the discussion surrounding the Page over here is whether the company would be able to maintain its growth in the upcoming years and whether the business is overvalued or not…

Sharing a link to an article which does not directly link to Page but gives a different approach towards analysing expensive looking businesses. I hope this helps -

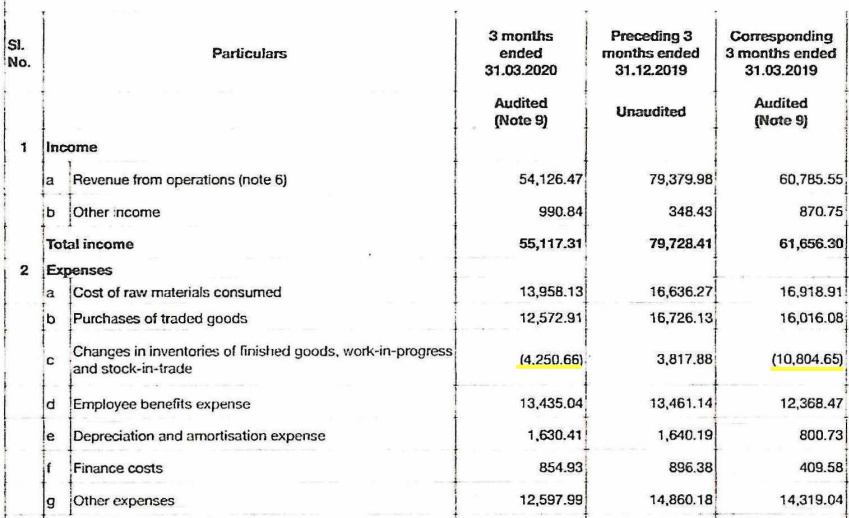

Financial Highlights for Q4 FY20

• Revenue down by 11.0% to Rs. 5,413 million as compared to Rs. 6,079 million in the

corresponding period of the previous year. Sharp volume impact in March was the result of

retail outlets being temporarily shut on account of the nation-wide lockdown.

• Gross margin remains strong and steady at 38.3%.

• Lower absorption of costs invested in sales and marketing, people and technology contributed to the lower PAT.

• Profit after Tax stood at Rs. 310 million compared to Rs. 750 million in the corresponding period of the previous year.

PAT is down only because of corona issue, as they could not dispatch booked orders or it was in transit and could not be delivered. And it will be in Q1 results.

Hi Hrishi - sorry if am reading this wrong but shouldn’t this have reflected in 2c (the inventory seems to have increased by a lesser number than Q4 2019)

I have attended the concall. Could not hear completely due to bad connection. But got a feeling that management was bit evasive while responding. For eg. when someone asked what amount is included in last quarter as “one time costs” (management confirmed there are one time costs during the quarter like IT spend etc), they said we will respond it offline. Also someone raised exactly same question as raised by @grovmo above, management did not respond convincingly. For some others, they said they would not disclose. (and these were fairly simple questions) . They did say they are seeing better traction in this quarter.

So either they did not want to share due to competitive reasons or are not used to open communication with the investor community. But when company is having deteriorating performance, they need to do more than just to have concall, to assuage fears of the analysts/investors. These were my first impressions. I could be completely wrong…