Why Suprajit Engineering occupies largest position in my portfolio is because of the runway of growth it has

Automotive Cable is a fragmented industry globally worth 3 billion USD (number is confirmed by management in one of the conf call). Suprajit is No 2 player now after Hi-lex with the acquisition of Konsberg LDC business. Hi-Lex EBIDTA is 6-7% while Suprajit has one of best EBIDTA in the industry 16%+

Extent of fragmentation in the industry can be highlighted by the global share of No. 2 player –

Why Market is Fragmented?

The capital required to set up mechnical cable plant is very less. Fixed asset turns are very high. Suprajit never had orgainic capex more than 50 - 60 cr in a year so far. Therefore except Hi-lex, Konsberg (before), Suprajit and I think Dura, most of the players local or have limited prsenece accross continents

What game Suprajit is playing in the space?

Now with manufacturing units and supply chain foot prints across amricas, europe, asia ; Suprajit wants to be preferred global vendor. Rather than giving contracts to 3 vendors across 3 continents, Suprajit alone can fullfill requiremebt across continents for global platforms with top notch QCDD ( Qaulity, cost, delivery and developement

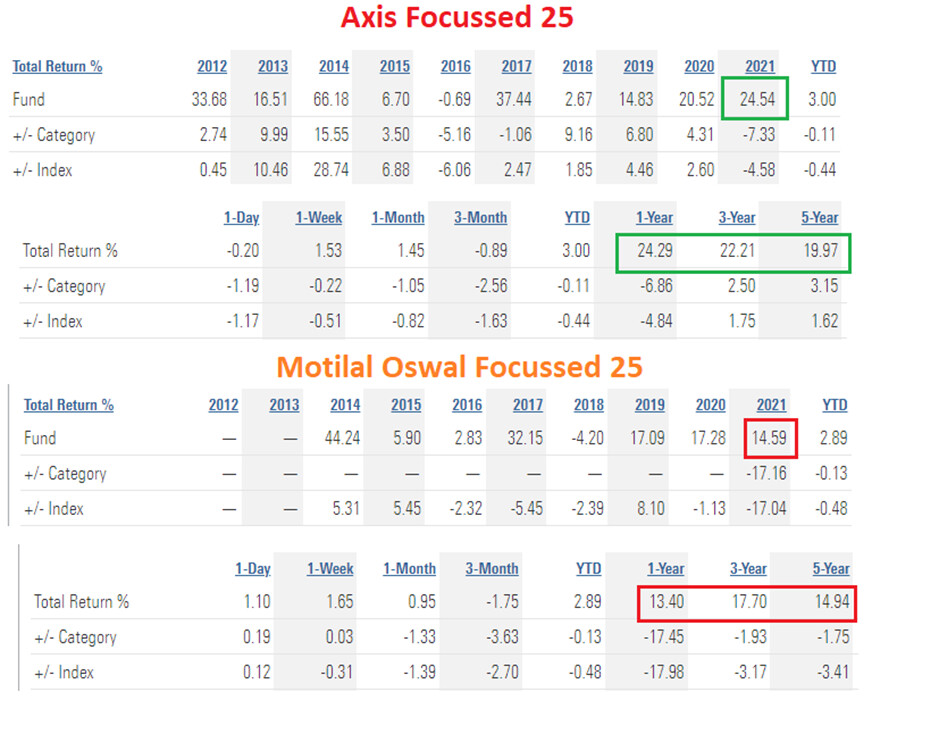

Other good data pointer is comparing with other fund house with similar style. Motilal Oswal amc and Axis amc, both follow ‘Growth’. You can see both the funds have underperformed indices for FY 2021 but Axis has done better than Motilal. That further supports my belief that – ‘’Process is not broken but style has gone out of favour’. If I would have invested in Motilal Oswal schemes, I think I would have pressed sell button because it is not just 1 year phenomena but last 5 years’ trailing returns are lagging index. Having said that equity investing is so asymmetric that one year can change tables for last 7-8-10 years returns and that’s why I tend to be choosy in selection but willing to give long time to managements of portfolio and even company in the portfolio when they are underperforming

Portfolio Update and allocations calculated at the start of the year

Core/Satellite

Company name

Allocation

Recent Action

Core

Suprajit Engineering

33%

No change

Core

Ajanta pharma

12.7%

No change

Satellite

Kotak Bank

9.2%

Adding

Satellite

Abbott

2.9%

No change

Satellite

HCL Tech

2.7%

Adding

Satellite

Axis long term equity

23.9%

SIP + Top ups

Satellite

IDFC tax advantage ELSS

15.2%

SIP

I understand Suprajit’s allocation will raise eye brows which I have been mentioning all throughout the thread. This allocation was 50% + in last cycle and even with recent price rise allocation has come down. I definitely want to create more and more space to let Suprajit and Ajanta to run

Also other intention is to enter each cycle with balance of aggression and defence. Core provides aggression and satellite provides defence

This thread offers descent analysis and behavioural angles for the ‘Core’ part and for the Mutual funds in the portfolio. Satellite portfolio analysis ex MF is tacky and does not offer much insight to reader beyond ‘cute’ presentations (which I enjoy preparing)

Going forward, I am spending some time in understanding IT industry and financials in little more detail. That is the main focus area this year. As and when I will have any insights I will post it over here

Is there a concept called ‘Free Shares’ when a particular company becomes 2X from average cost price?

My opinion is emphatic ‘NO’

In believing ‘Free Shares’, investor is overlooking one of the most important and the most underrated risk – ‘Reinvestment Risk’.

Compounding ‘Net worth’ is the key. If investor books a profit/partial profit (step - 1) and invest that in new idea (step – 2), then he/she can be wrong at two places. If investor decides to hold on then he/she can be wrong at this very decision too.

Therefore in my opinion ‘Free shares’ thought process is wrong

Importance of patience post stock picking is widely discussed topic. Most of the successful investors attribute ‘patience’ to the ‘’key’’ which unlocks doors of long term compounding. This is where cult of Mr Buffet created disciples (and I am one of them)

But what is less discussed, in my opinion, is the patience some of the successful investors exhibit ‘pre’ stock picking. Some of the example in recent readings are – (1) Vijay Kedia interview with Niraj shah few months back where he mentions, sometime he tracks particular company 4/5 years before investing. No wonder he can gauge management by just body language as he mentioned in his recent interview with Vivek Bajaj (2) Someone on Twitter university mentioned that From 1984 - 87 Birkshire Hathaway was sitting on over USD 1 billion cash and did not make a single investment in any public equity until their investment in coca cola in 1987

We are mortals and we also have different goals but I personally believe, I should more carefully pay attention to this treat of successful investors and try to see if I can learn anything from it. This is especially true in the bull phase of the market where you put a finger on any idea and it runs up in no time.

Talking about my portfolio, I can see I have joined IT bandwagon when I invested in HCL tech (May be I could have been more patient or may be not!). Abbott India is something I have been tracking for more than 3 - 4 years and waiting for some Macro/policy action which can pose challenges to its revenue stream. The trade-off of high ROE is geography concentration and that’s where I like Ajanta’s business model more. I have been waiting for all these years for some price control / policy action will make valuations look rich and I can use that opportunity to ramp up my allocation. But hang on! – I just remembered what Mr. Lynch has taught us - ‘’Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves’’. No wonder investing f*$%s your mind!

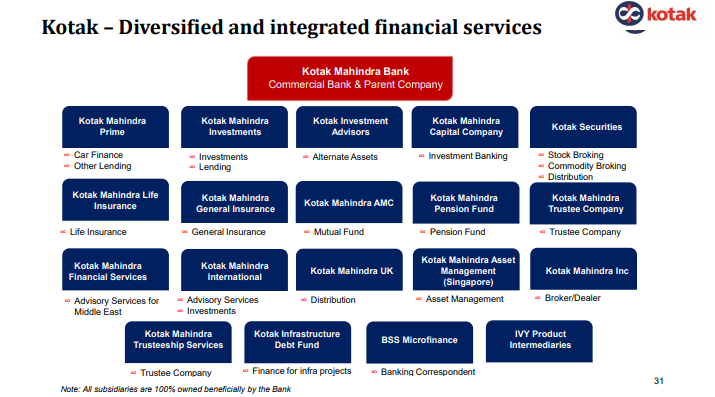

Following slide was the one of the most important reason to buy Kotak. Not much number crunching and business analysis behind decision. Source: Investor ppt

After reading above post, Harsh rightly pointed me to Eris which potentially has similar business blue print as that of abbott. I dont expand my investible universe that easily in bull market. Also despite having mentioned, my poor pharma knowledge, here is why I added Eris in my investible universe. I am trying to understand more about management by going through confcalls and will update my decision as soon as I have further insights

Though I am not a shareholder of IDFC, I am closely tracking the progress of disinvestment of IDFC AMC. If the change of ownership changes fund management team, then I will have to revisit my decision to remain invested with the fund house. Anoop bhaskar who succeeded Kenneth Andrade as a CIO of IDFC AMC in 2015-16 has implemented unique investment philosophy which is different from the street. The change of management and that’s why investment philosophy will have significant impact on my MF portfolio which is designed keeping in mind the strong inverse correlation between investment philosophies of Axis fund house and IDFC fund house.

If change of ownership causes change in fund management team then I will be inclined to redeem all the units in IDFC AMC and invest that money in PPFAS flexi cap. Closely monitoring the situation and will take decision as things unfold. Hoping that current fund management team remains. More about Anoop Bhaskar, I will write in the future post

XIRR as on today since the start of invetsment

Axis long term equity – 18.67%

IDFC Tax advantage elss – 21.88% MF Portfolio return over 6+ years = ~20%

They have stopped taking new capital due to Sebi mandate of cap on maximum foreign investment. They are waiting for rule to change which may take some time.

Yes I am aware. Hopefully PPFAS issue gets resolved soon. Disinvestement process will take some time to complete hopefully. Then only I will come to know what is happening with the fund management team. I also have some time to make the call.

One thing to note is that branded generic players which I track – Ajanta, Abbott and Eris have reported very stable margins for Q2 and Q3 which are high inflationary quarters. I think that highlights the strength of business model provided business has managed other risks well. Also, in the recent Ajanta pharma conf call management highlighted the severity of pricing pressures across generics business which is – From the least to highest – India branded generics, global branded generics without pricing control, global branded generics with price control and finally US generics.

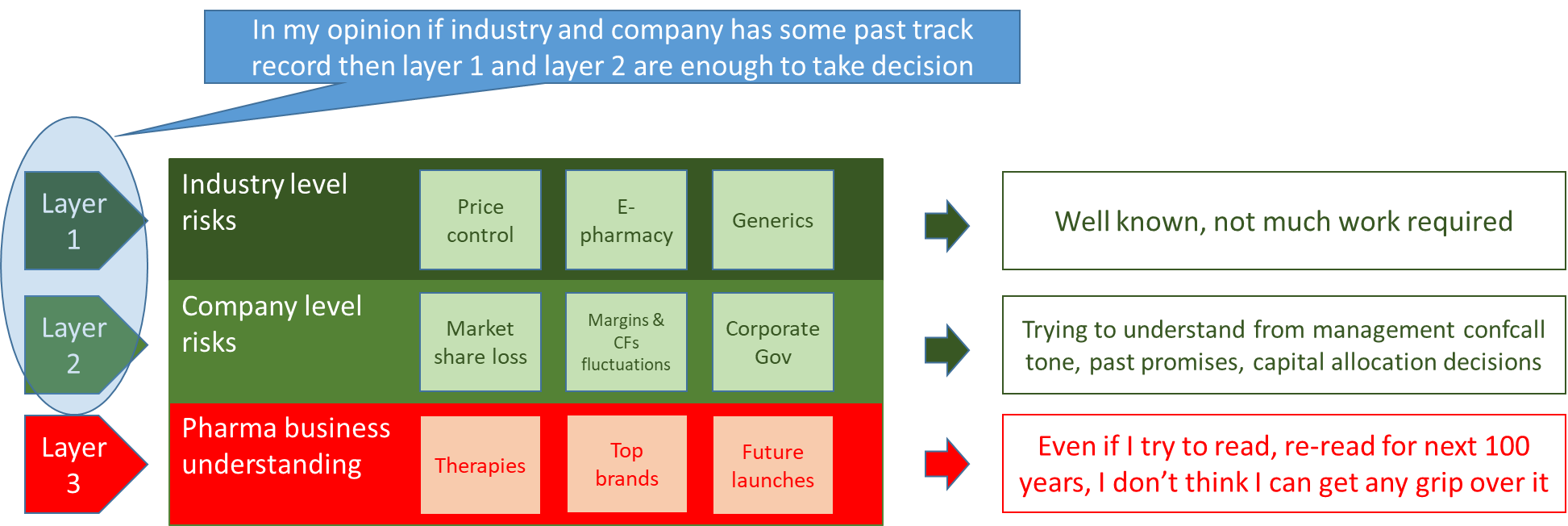

These two reasons along with the simplicity of business model makes branded generics and especially India generics a compelling reason to buy for a pharma toddler like me. Though pharma is difficult to understand, it is also very difficult to ignore as it is the only sector which can show earnings growth in recessionary years

Therefore my approach is to accept the limitation and that’s why accept the compromise of slightly lower growth and higher valuation and stick to the simplest pharma sub segment which has proven winners

The above point in the original investment thesis (The outlier) did not play out in Q3. however medium to long term thesis for investment and concentration intact.

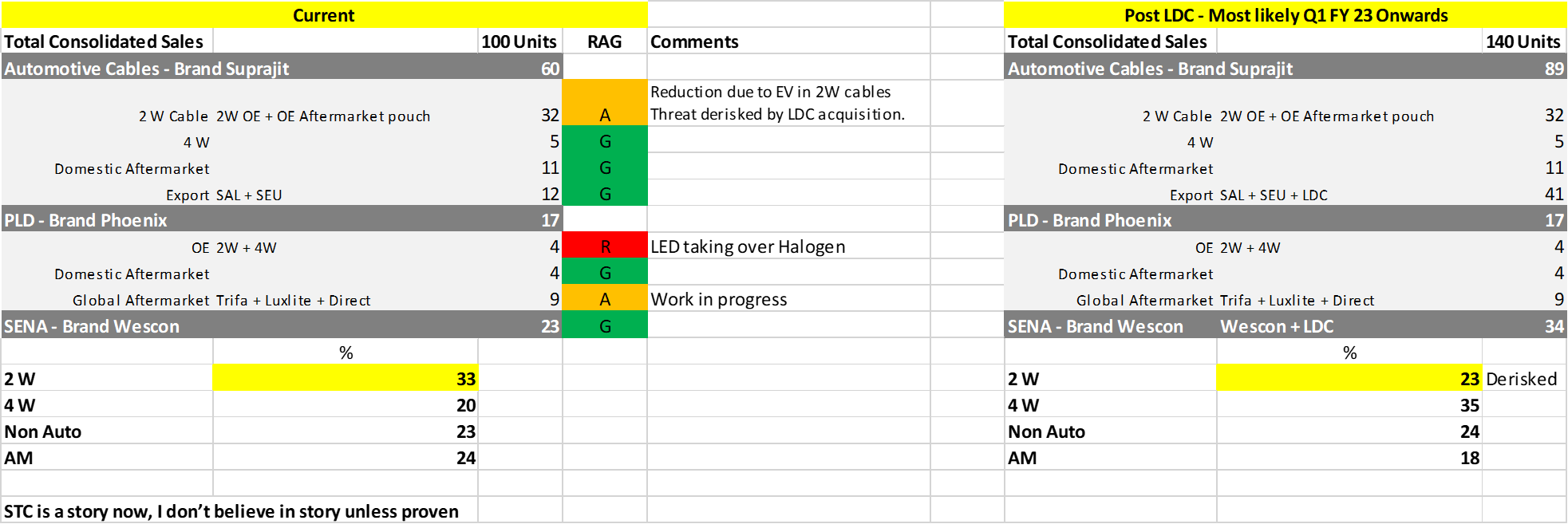

I think Suprajit’s weak result was the first weak result of any portfolio company in the core portfolio since the start of this thread. Therefore trying to give deep dive view of Suprajit’s business print. No dobut my analysis of Suprajit being ‘Outlier’ went for a toss looking just at Q3. Hopefully following table will give ‘zoom out’ view of author for a reader beyond Q3