I was thinking following options to build financials part of the portfolio. I am going to start with option 2 and may shift to option 3 in future

Option 1 – 20% Kotak Bank

Option 2 – 10% Kotak Bank + 10% HDFC or HDFC bank

Option 3 – 10% Kotak Bank + 5% HDFC or HDFC Bank + 5% Bajaj Finserv or ICICI Bank

As in case of IT and pharma, because of my inability to analyse banks or a lender, I would like to stick with obvious names. I believe private banks will grow mid to high teens over long term and I don’t wish to create any alpha over industry by venturing into the something which I don’t understand even by putting efforts going through conf calls etc.

The only uncertainty in case of HDFC bank is the restructured book and I am willing to believe what management said Q3 conf call without second guessing (as I cannot do that)

I may switch to option 3 in future if I feel comfortable. In case of Bajaj Fiserv I will be taking valuation risk (I can sense Peter Lynch laughing) and In case of ICICI bank I will be taking underwriting risk

This is where, I hit my limit of analysing financials J

There may be more value to be realised in some of the smaller private sector banks. Have been analyzing Federal Bank which could be a candidate for re-rating post listing of its NBFC Subsidiary Fedfina Financial Services. Would recommend to go with one large and one midcap bank for diversification.

Of the 3 options, option 3 is a good one (as long as you don’t land up selling Kotak to invest in Bajaj/ICICI. J

Hi vernon

Appreciate your point on midcap banks. To be honest i am very reluctant to go beyond large cap names in lenders as these are leveraged businesses. But i will take back your suggestion and think over it.Thanks for dropping by

Valuepickr is a powerful platform to find a multi-bagger but in my opinion, it is a more powerful platform to create and document literature around holding a multi-bagger

When I started this thread around a year back I never thought I could write so much as I never had enough “ideas” to write but as I went on writing I realized the importance of this platform in creating logs that can serve as a good source of documentation for “holding” the idea. That was a newfound purpose with which I started creating posts. If at all any one of my core holdings does well in the future from hereon then an attempt is to have some sort of literature - over a longer time period - around holding that position

In this regard, if Valuepickr team can provide a feature to tag a post with a company name (like how one can tag some attributes at a thread level) that will helpful. If authors are successful in creating descent logs over years for their successful investment then all reader has to do is just filter a company name and read how the author held on to his/her idea despite unfavorable conditions to ‘hold’.

With this, I come to the point - why I started writing this post. ‘Dar sabko lagta hai’. If I say I can hold my largest concentrated position without worrying when it is down 30% + from the top then I am lying to myself and this community. Following are the few worry neutralizers in that order

Stable job

Very stable satellite portfolio

Proven past track record of management

Conviction around business and prospects

Experience to hold

The reader has all the right to ask why not spread risk over multiple small-cap positions rather than a concentrated bet - Honest answer is the inability to analyse risks of multiple sectors/ companies and time constraints.

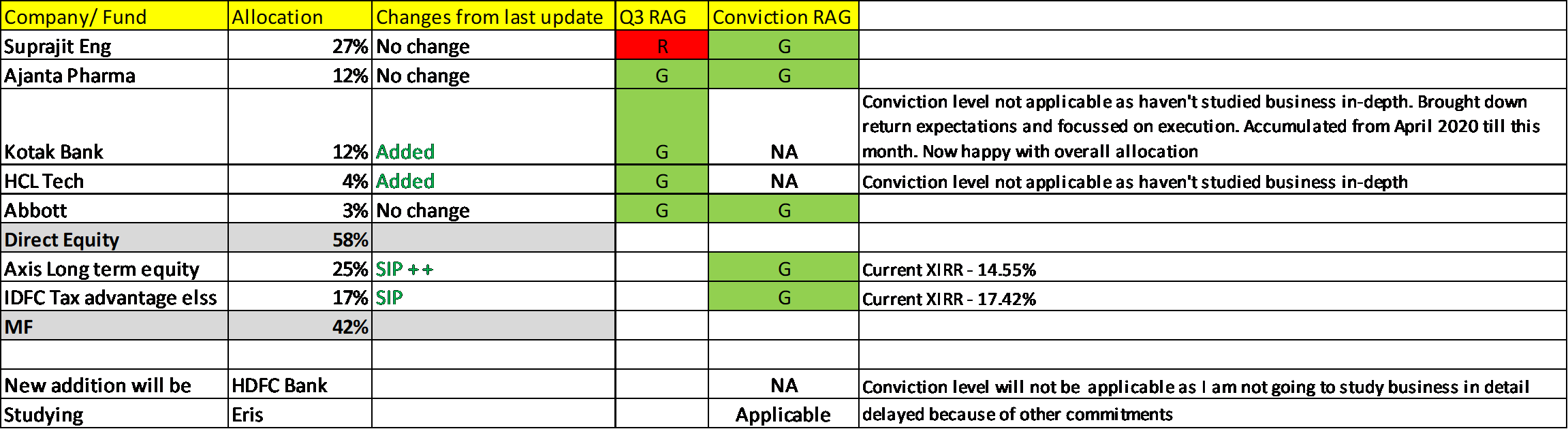

Overall staying the course. Game plan is not changed

Holding - Suprajit, Ajanta, Abbott

Looking to add in existing postions - Kotak, HCL Tech

Will be taking new position in HDFC Bank after a month or so

Studying Eris

Cotinuing SIPs as planned in MFs

I still maintain the point of view which I posted in Ajanta’s orginal thesis. Every now and then I keep getting these cravings to add more in Ajanta pharma. It feels like when odds are in your favour then why follow process. This is your chance but on other side it feels like ‘Control Uday Control’

Same thing as above, I was trying to do for IT but after going through few confcalls I found everyone is doing same thing and I could not objectively differentiate between two companies. Thats why I did not select any small mid cap companies to invest. But I wanted to have some allocation to IT in the portfolio and thats is why selected large cap with relative valuation comfort

It could be that very well all of them pass your process as well. Just because all do the same thing may not mean that they would not pass your process…a thought to think upon?

A day to remember on the timeline of this thread. If someone is reading this thread after 10 years, may act as a good data reference on the timeline. How did we all navigate through these times. Just absorbing the pain today, no buying no selling

Agree to your point. Its precisely same reason I stayed away from Pharma in 2010 bull run of pharma…If you ask me today for IT, no one can differentiate them that well…each has its own strengths…except maybe differentiating them broadly to - Products, Services, Engineering R&D & Digital (slightly high digital revenues)…each under these basket more or less are similar…

So, if we wait to differentiate further and go micro, we may not able to do that except in maybe very small IT companies

It also depends on what role IT is playing in your portfolio. If you are looking for alpha generation then one might have to dig deeper but if you are ok with lower returns then average decision making abilities are good enough in my opinion as sector as a whole has one of the best CG, they are cash generating and has proven track record. My expectation from IT in the portfolio is - 1) provide good diversification 2) provide hedge against currency dep and some stability to portfolio. I also dont want reinvestment risk, if I go for small/mid cap due to lack of understanding there can be higher propensity to reinvestment risk

Considering all these factors, sticking with large cap

Not long ago (March 2020) we had trading halt due to lower circuit break in Nifty and sensex. And prior to that I remember the same happening in 2008. (Not sure if that happened in between years)

Even prior to Russian aggression, the market started correcting due to 40 year record high inflation in USA and hence expected inevitable sharp interest rate hikes this year.

This year is eerily similar to 2008 than 2020. In 2008, the bear market lasted for 18 months, if I remember right, and turned with the election results of 2009.

LED is a mega trend but unfortunately intense competition can bring down ROEs with the lack of strong competitive advantages. That’s why in the small/mid cap space, I usually like to put bets on the companies which are already having a moat and trying to deepen their moats. I lack the ability and interest to catch company early which is in process of building its competitive advantage even though highest amount of returns are possible in this case

Though I am travelling and on&off market, i managed to listen some parts of Ajith Rai (Chairman - Suprajit) interview with Marcellus

In the Q3 confcall and Marcellus interview, first time I heard management talking about the increasing the ‘Content per Vehicle’ for 2 wheeler and automobile. By leveraging Suprajit Tech Center, management is looking to improve the content per vehicle, especially in two wheelers, where number of cables are reducing.

Throttle cable (not required in EV) —> Electronic throttle control

Speedo cable (not required in digital speedo meter) —> digital speedometer

Break cable (not required in disc breaks) —> break actuation

STC is yet to prove itself and that is why I am not updating my thesis to add new dimension of growth through STC rather I am watching carefully how management is de risking 2 wheeler business of cables

Core thesis still remains - expanding geographic footprint and adding new markets for core products - cable and lamps

rather than focusing on content per vehicle.

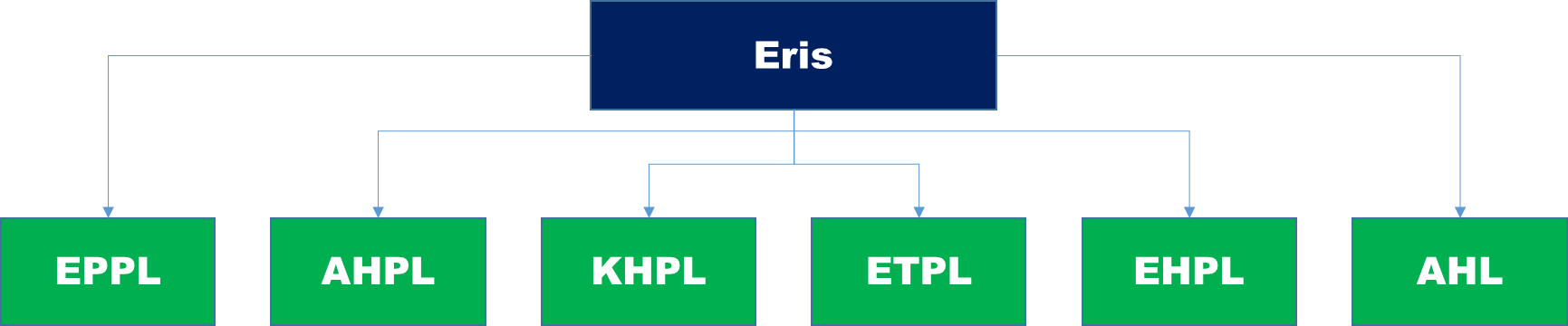

While analysing Eris Lifesciences I am trying to focus on following points

What is the role of each of the subsidiary in the corporate structure. I understand these are the by-product of multiple acquisitions and JV but trying to understand in more detail. I believe that will help me to understand business blue print

How well management has executed compared to promises. Certain X-Factor if any?

Compare outlook with Abbott

Abbott

Eris

Last 5 years sales growth

10.5%

15.5%

Last 5 years profit growth

22%

~13%

EBIDTA Margin

21.4% (Scope for margin improvement?)

35.6% (No scope for margin improvement)

Interestingly, From whatever conf-call I heard so far, being exact same business, the reason for Eris having significant higher margins is because of its in-house production (Views welcome). 5 years back when Eris was outsourcing most of their production, their margins were in 20s. If this observation is right and it is low hanging fruit then why can’t Abbott improve their margins to 30s?? Views welcome

The big difference is in terms of gross margins, domestic specialty focused (not OTC) pharma companies specializing in chronic therapies make 75%+ gross margins. You can look at the gross margin profile of competitors who have similar business mix (Ajanta, Sun and Torrent). These companies make 75%+ gross margins in India, this is due to their higher specialty focused portfolio. On the other hand, companies with large OTC brands are akin to FMCG companies, most of these make gross margins in the 55-60% kind of range. Abbott’s business mix is more towards OTC than specialty. Additionally, Eris has a smaller portfolio under NLEM (around 12-15%) compared to 25% for Abbott. NLEM products will have lower realizations (due to price capping), hence lower gross margins. Also, I don’t know how much of Abbott’s products are in-licensed from other companies (or from the parent entity). In-licensing also has a large adverse impact on margins as royalty payments would be linked with sales. However, in-licensing is ROCE accretive. Eris has very low amount of in-licensed portfolio so far, although this will change in the future.

I don’t think margins has a lot to do with outsourcing vs in-house manufacturing. When Ajanta was outsourcing a majority of its products in 2012-13 timeframe, gross margins were still 70%+. Gross margin is more of a function of product mix (specialty vs OTC vs pure generics). EBITDA margin is more a function of business strategy (marketing vs research based vs B2B). A B2B pharma co can make 35-40% EBITDA margins despite having only 55-60% gross margins (likes of Divis/Gland) as they don’t have to invest a lot in frontend. However, its not possible for a marketing company to make 35%+ EBITDA margin unless their gross margins are 70%+. The only exception I have found so far is Caplin Point (55-60% gross margin but 30%+ EBITDA margin). So, I don’t think its possible for an Abbott to make 35%+ EBITDA margin as their gross margin itself is 45%. There are not many pharma marketing companies whose employee cost to sales ratio can be below 10%.

A better comparison for Abbott is Sanofi India. Sanofi makes 55-60% gross margin and 20-25% EBITDA margins. Hope this clarifies my thought process.