Hello fellow investors,

After procrastinating for almost a year, I am attempting to write this post on my investment journey so far, my current status of the portfolio and my thought process. The idea is to keep this forum as a running diary and try to learn from you all with your comments and inputs.

About myself

I am a typical engineer + MBA guy from Mumbai who finds himself in the bell curve’s average range in the IT industry. With some luck and persistence, I managed to harvest currency arbitrage opportunities. Currently, I am in the UK with my wife and do not have any complaints about my work life. I started investing in the year 2014 post my MBA. After seven years, I can say with some confidence that ‘Equity Investing’ is something that interests me. Hopefully, I will persist with this “side hustle” over the coming years (and hopefully decades!)

A brief overview of my Journey from 2014 till now

You guessed it right; I was drawn to the stock market in the raging small-cap bull market of 2014 with the belief that the best way to invest is to concentrate on the next small-cap multi-bagger idea. Having convinced with my abilities to identify a so-called multi-bagger, I started building a concentrated position in one idea from 2014. I was euphoric about the company’s prospect and expecting many X returns in the next 2 to 3 years. The plot was set where Mr Market was ready to ambush a newbie, and it did not disappoint. The bear cycle in the broader market from 2018 – 2020, followed by the deadly Mar 2020 crash, challenged my temperament and thought process. The bear cycle’s emotional impact was magnified because of my concentrated position, which made me question my approach. It made me introspect about how I should think about my risk appetite and how should I attune my risk/return knobs.

You all must be wondering (or rather judged already!) - Did I lose my capital in the concentrated bet? Did I make a horrendous mistake by believing Warren Buffet’s famous quote – “All you need is three investments in your entire life”?

Hold on to your thoughts, you will know that by the end of this post, but before that, I would like to share some of my important learnings about myself, my skills and my temperament.

Lessons learnt

Some of the important aspects which I learnt about myself and investing are -

-

Concentrated bet makes me overdo business analysis. Over-analysis increases anxiety and does not give breathing space to hold a company for a very long term.

-

To make the right judgment on any business is very difficult as there are a lot of “unknown unknowns” and moving parts. These unknown unknowns become evident in the bear cycle. Example – liability issues in NBFCs, US market down cycle for pharma etc. With this inability to make a sound judgment, I also allude to the way I did my school, engineering studies, and even the MBA program. As a student in the Indian education system, I could score well in an exam by simply remembering the concepts without developing any ability of critical thinking. Therefore, the tendency to believe that “I understand the concept completely” is very high only by reading about that concept (and not reading between the lines). It worked well for me to get degrees, but it exposed my decision-making abilities in investing. I understood the world is more dynamic, and the concept of “circle of competence” is non-existent for me.

-

My ability to construct a portfolio is not better than (even as good as) a fund manager. If I am going to construct a portfolio, it is very difficult to earn higher returns on a net worth by myself compared to a fund manager.

-

What makes sticking to the process in equity investing difficult is the market cycle and its changing texture. The market cycle at a time usually favours only one particular style of investing, followed by a different style at the start of the next cycle. This is stark different from FD or RD, where FD in one bank gives me the same return as FD in another bank. The same equity market cycle can give varying returns for two portfolios depending on the investment style. It is important to recognize that a portfolio’s underperformance due to style going out of favour is more than a norm.

To summarize, lessons learnt were contradictory in nature. First, a Concentrated portfolio makes me anxious or over analyse the business. Still, at the same time, my ability to construct a portfolio is limited (or I must say inferior to the options available in the market). Second, how should I improve my ability to hold the investment for a long time by objectively weighing the under-performance? (In business or MF performance)

Implementing my learning in portfolio construction

-

Diversify a portfolio to allow each position to run for the longest time possible and avoid over thinking about a particular business. Use mutual fund to construct a “portfolio”. Even if I happen to outperform average mutual fund returns, the low to mid-teens kind of a return by mutual fund without using much of your intellectual bandwidth, just by focusing on behavioural aspect was alluring because of two reasons. (1) If selected right, mutual funds can create desired compounding effect with a good process in place which can absorb larger capital as well (2) It leaves your intellectual bandwidth and time free to focus on ‘something else’ and that ‘something else’ in my case is - ‘Investing in two or three wonderful businesses in my circle of competence.’

-

Hold your position across market cycles and do not get bog down by the 2-3 (or even 5 in some cases) years of under-performance. This can be further nuanced depending on whether you are investing in a mutual fund or direct stocks

a. Direct stock investing –

In direct stock investing, I started thinking like an owner of a business than as an investor. This simple change in thought process enabled me to take a very long term view of a business. Whenever I want to judge a business, looking from the owner’s lens helps to stick with the company for a very long time.

I agree with your point that, for a retail investor, thinking as an “owner” is only possible in a utopian world. The idea is to invest in a company where promoters try to make money for themselves as well as for their fellow shareholders. Again, this is a qualitative judgment, but historical data indicates the promoter’s integrity. I will try to elaborate in an individual stock thesis, which data points I used to decide the promoter’s integrity.

b. Mutual Fund

Each mutual fund house has a style of investing, and under-performance of a style is a norm. Therefore understanding whether the underperformance is because of style is out of favour or because the process is broken is important. It is common for a style to be out of favour for 3-4 years. An investor needs to stick to the same mutual fund in a period when it is under-performing to gather more and more units.

My current portfolio

That brings me to the last point of the post - my current portfolio construction and the answer to the question – What did I do with my concentrated bet? Well, I still hold that concentrated bet with the same enthusiasm and bullishness that I used have 5 years back. When I speak about a company’s investment thesis, I will discuss how did I think through the bear cycle.

My current portfolio has two sections –

- Mutual Fund (around 50%)

a. Axis long term equity – Started SIP in Dec 15. Ongoing (XIRR – 17.9%)

b. IDFC tax advantage elss – Started SIP in Jul 15. Ongoing (XIRR – 17.39%)

I know you will have a question on why both funds are Tax schemes. It’s more of a coincidental, and I will try to explain about Mutual Fund selection process in the follow-up posts

- Concentrated Bets (Around 50%)

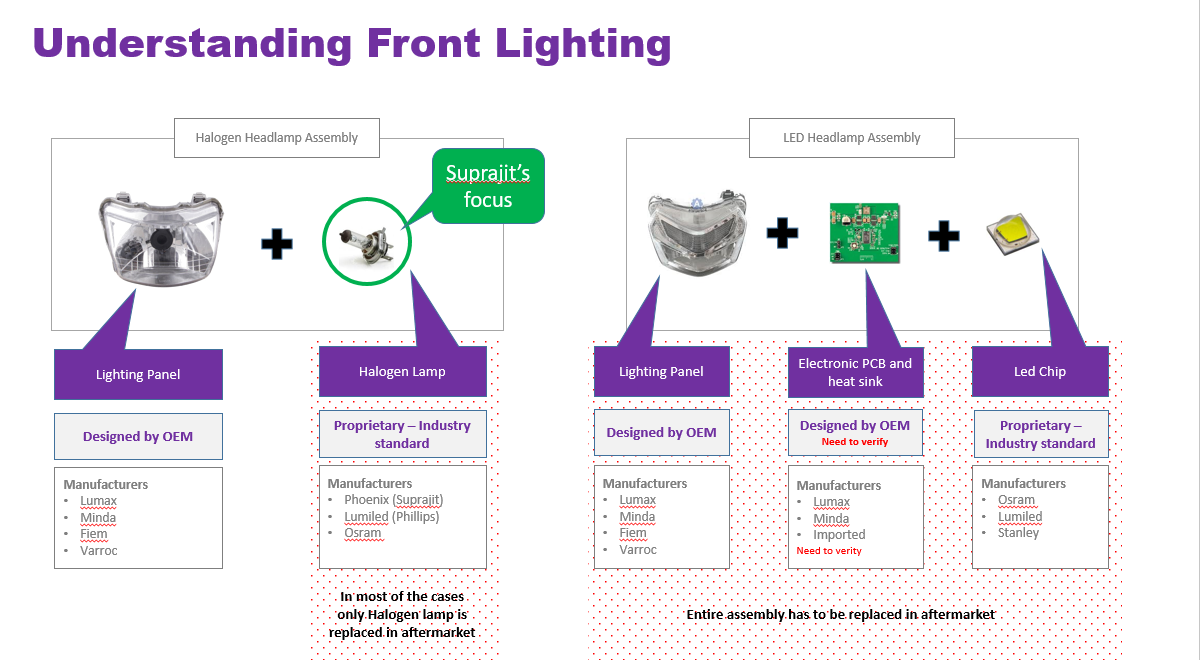

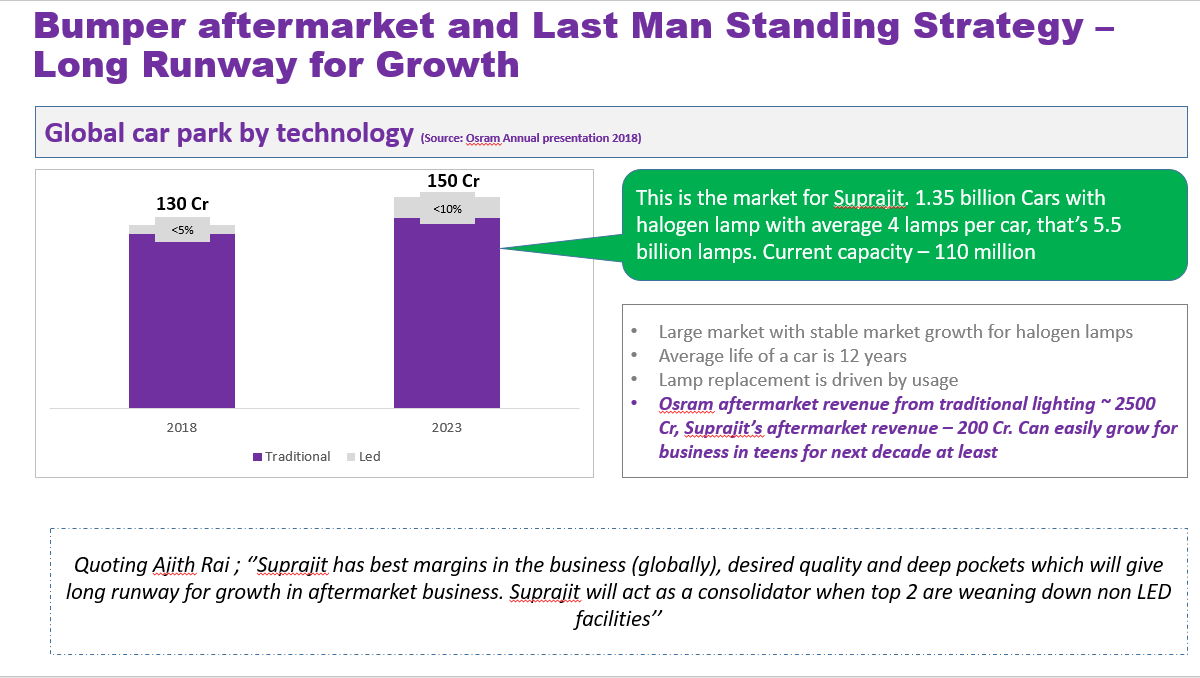

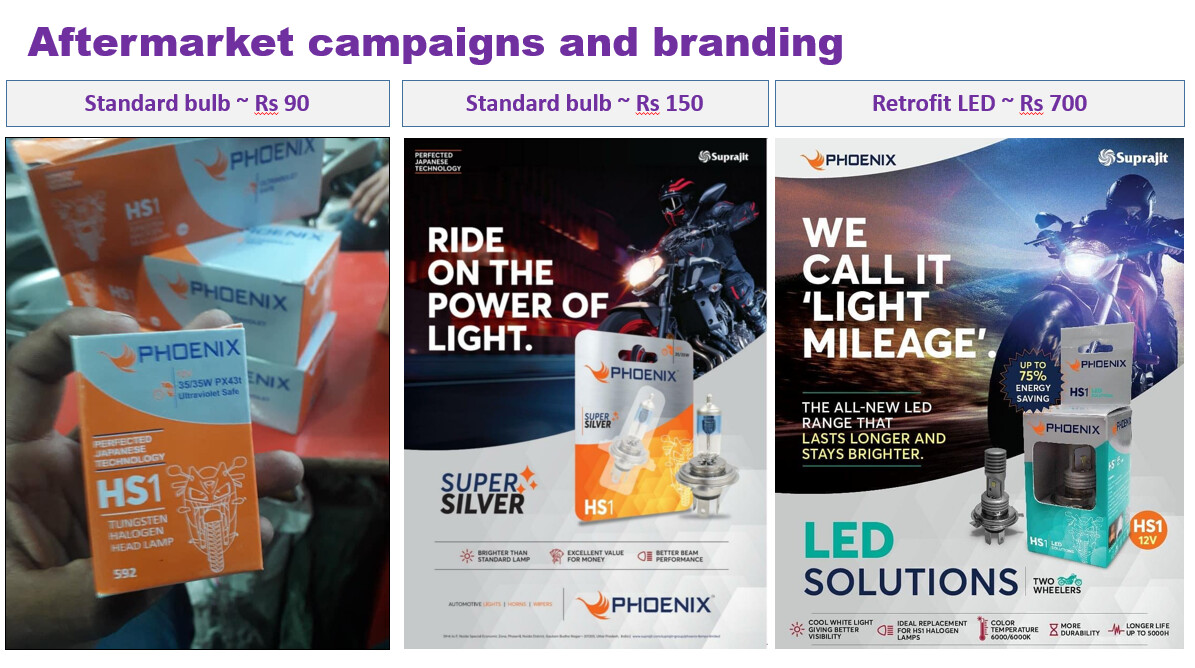

a. Suprajit engineering – holding since 2014. Averaged up and down from 2014 till Feb 2020. Average cost price/share ~ 250

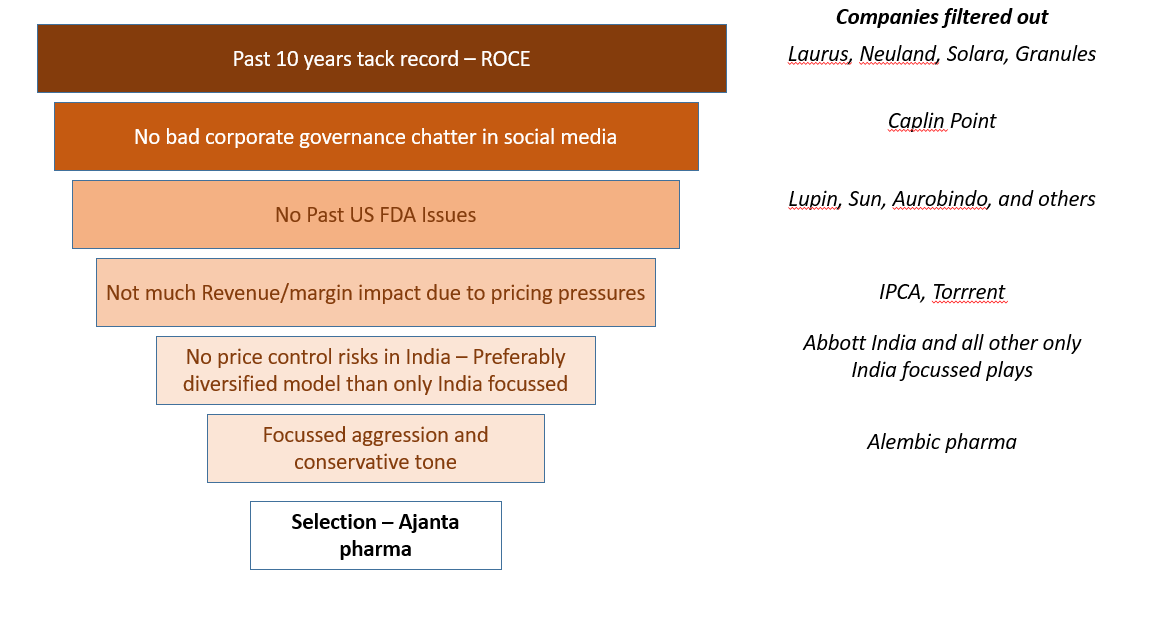

b. Ajanta Pharma – Holding since 2017. Averaging up and down from 2017 till to date. Average cost price/share ~ 1400

c. Kotak Mahindra Bank – Started building position in the second half last year. I will use this whole year to build a position

I will explain in detail the investment thesis of each idea in upcoming posts. Also, please note that I don’t try to time market. I invest a predefined amount of monthly savings on the 1st of each month

Note – I am trying to see if I can use Saurabh Mukherjee’s ‘Consistent Compounder template to create a diversified portfolio with minimum time and effort, which will take care of the diversification aspect. I haven’t made much progress on this; it is still a work in progress.

what say motherson shareholders?)

what say motherson shareholders?) . Have a nice week ahead!

. Have a nice week ahead!