My thoughts first before giving an opinion. This is just general gyan which I am sure you also must be knowing. Never the less just setting up the context –

In my opinion, successful investing is more about avoiding blunders than chasing returns. If we have the right infrastructure created for compounding, that itself enables us to earn base case returns which I would say low teens without any efforts. (Example of blunder – locking down in low yielding policies) But if we are looking to create alpha over base case then the portfolio structure should be ‘’Optimal’’ rather than just designed to avoid blunders

Now let’s understand the arrangement –

Monthly SIP in blue-chip and multi-cap fund for 15 years. Let us assume you invest 10k per month, with 12% CAGR that amount becomes 47.59 L. At the end of 15 years, that amount will be transferred to BAF and you will get monthly 30K from SWP. That’s around – 7.5% (3.6/47.59). If we assume inflation of 6%, from 16 years onwards to maintain your corpus level till 2099, BAF should earn returns > = 13.5%. But if you want to exhaust funds by 2099 then I am not sure what should be the returns

Therefore to conclude –

Is this investment a blunder? – Definitely No.

Is this investment Optimal? - My answer is No because

After 15 years you are transferring monies to BAF, I am not sure about your age but if you still have your primary income then you do not require SWP. That’s why you might be better off continuing in equity funds

You do not have the flexibility to choose funds outside the ICICI fund house. You can do a similar setup yourself by choosing your funds.

So at 12% CAGR for SIP of 6000/- We can expect above 30 Lacs and at 10% CAGR about 25 Lacs in 2035! Also my wife informed that at the end of 15 year we can opt to Withdraw the entire amount at the NAV rate at that time. My wife will be 45 Years old then. Very fact that we will have 25 - 30 Lacs of rupees at that time feels so good!! Also my wife is regularly putting some amounts in Sukanya Samriddhi Yojana since 2016.

At least it is not a blunder - that is a relief. I will be closely following your thread - lot of insights here. Thank you bro.

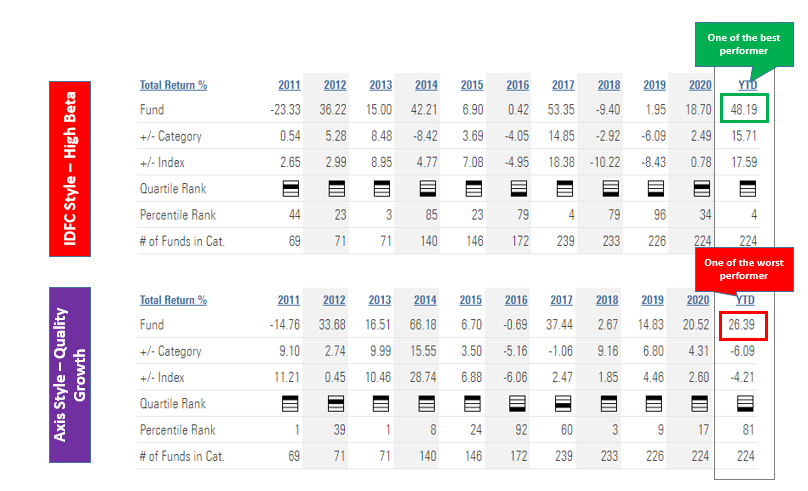

Axis long term equity - 20.73%

IDFC tax advantage elss - 21.48%

This complementary style of both funds, makes life easy to ‘‘hold on’’ during umderpeformance of individual funds ( like Axis this year ). Apart from the complementary styles, other factor helping me hold on through underperfoamnce is excellent returns over investment tenure ( 20.73% )

Demons so far in ajanta pharma which I successfully tackled and the ones in progress

Company has lost focus, its branded generics business in africa and asia is not growing

Management is not interested in company as they sold 3% stake to SBI mf at 1500

US generics business of company is a drag on a overall business

India focussed branded generic companies are better than Ajanta

Abbott is a cash machine, coffee can stock. Sell ajanta buy abbott

Alembic pharma’s earnings are way better than ajanta pharma. Alembic is investing 15% in R&D vis a vis 5% of ajanta pharma. Sell ajanta buy alembic pharma

CDMO has better unit economics than Ajanta. Sell ajanta buy cdmo( demon in progress. Hopefully i dont succumb to it. This does not mean CDMO is not a good business) - Demon Closed Mentally

Laurus lab , Dr chhava is a visionary. Sell ajanta buy Laurus (demon in progress. Have huge respect for Dr Chhava) - Demon Closed Mentally New demon -

Some boredom creeping in because of no or sideways price movement. Last 5 years price CAGR (point to point) - 2.4%

In your retirement plans, I see a high emergency fund as medical cover insufficient. Is this insufficient medical cover intentional?

Also, since we are discussing this important aspect, wanted to get your views on medical cover. For salaried individuals, the cover provided by company health insurance is also inadequate even after choosing maximum option available (by self pay). Under such case, is it good decision to go for top up plan and are you aware how does the top up work and how to go about it?

For retired/self employed - what should be ideal health insurance cover and how to go about it? Should one buy complete desired cover in one floater policy or go for a smaller cover and rest do a top up on it?

Lastly, I see many sales pitch and advertisements of Health insurance mentioning to lock in early for lesser premium for same amount…but guess the premium is valid for only 2 years and every year/2 year the premium is revised as per age…and it is similar to someone of that age buying it for first time…so the entire point of getting locked in to have a low premium at higher age does not seem to be true at all…Pls correct me if I am wrong here…

Only thing which may help in locking early is having less preexisting illnesses at time of initiating the first cover…however, say if a person is diagnosed with a major illness 10 years into the policy, what will the insurance company do to his premium in his 11th year?

I hope my points are communicated clearly and would be great to know your & other’s thoughts. Thanks

@Investor_No_1

I have very limited understanding on the topic. -

The retirement plan above is for my parents and not me. Insufficient medical cover is not intentional unfortunately.

I don’t have much knowledge about how top up works. But I have read somewhere that room rent limit in some policies is derived from the Base Coverage. That means your base coverage is 5L, top up is 3L and if room rent limit is 1% of the base policy. That means you will be covered for only for INR 5000/day for room rent. This has implications on your overall claim pay out. If your room is 8000/day, you will be only paid (5000/8000) 62.5% of your total bill. Please verify this rule as I am not sure about it

I usually prefer to have health cover worth 10L, with no room rent limit, no copay

, having restore clause and have good hospital network. The advantage of locking early is, you get larger coverage as part of no claim bonus

Again I have very limited knowledge on topic as I am not residing in India. Therefore my views may not be correct

How does this no claim bonus work? do they keep adding the sum insured every Year on year? In case of insurance via corporate policy in which one works, one loses out on this as if an employee changes job in 10 years with no significant claim, his policy is gone and when he joins a new company with new policy (and quite possibly new insurance firm as well) - the entire 10 years no claim bonus is lost…any ways of mitigating this?

I am aware very few would have clear answers to these, me myself do not have…hence jotting down this in case you or anyone with more knowledge can let us know. Thanks again

Corporate policies generally do not have no claim bonus

No claim bonus is limited to 50-100% of the base cover depending on policy

Earlier i used to have Apollo Munich Optima Restore. Now max bupa reassure has similar features. You cam call policy bazar or coverfox for details and your requirements.

As an investor, I always have that one side which nudges me to become aggressive investor at the same side conservative side tries to keep me away from the jaws of aggression. I have learnt that, my past experience is a key factor which influences whether I lean towards side of aggression or towards side of caution ( which itself is debatable ). There are several dilemmas which I am battling with currently. Some of then are as below

Dilemma - Ajanta pharma concentrate or keep measured

My current allocation of Ajanta pharma is around 10% and I am constantly battling with thought - whether to step up allocation or not. With an announcement of board meeting today for buyback, it has intensified the mental battle

Here is what both sides are telling me. The points on the both sides are in random order

Aggressive mind

Cautious mind

Capacity for next 4-5 years in place

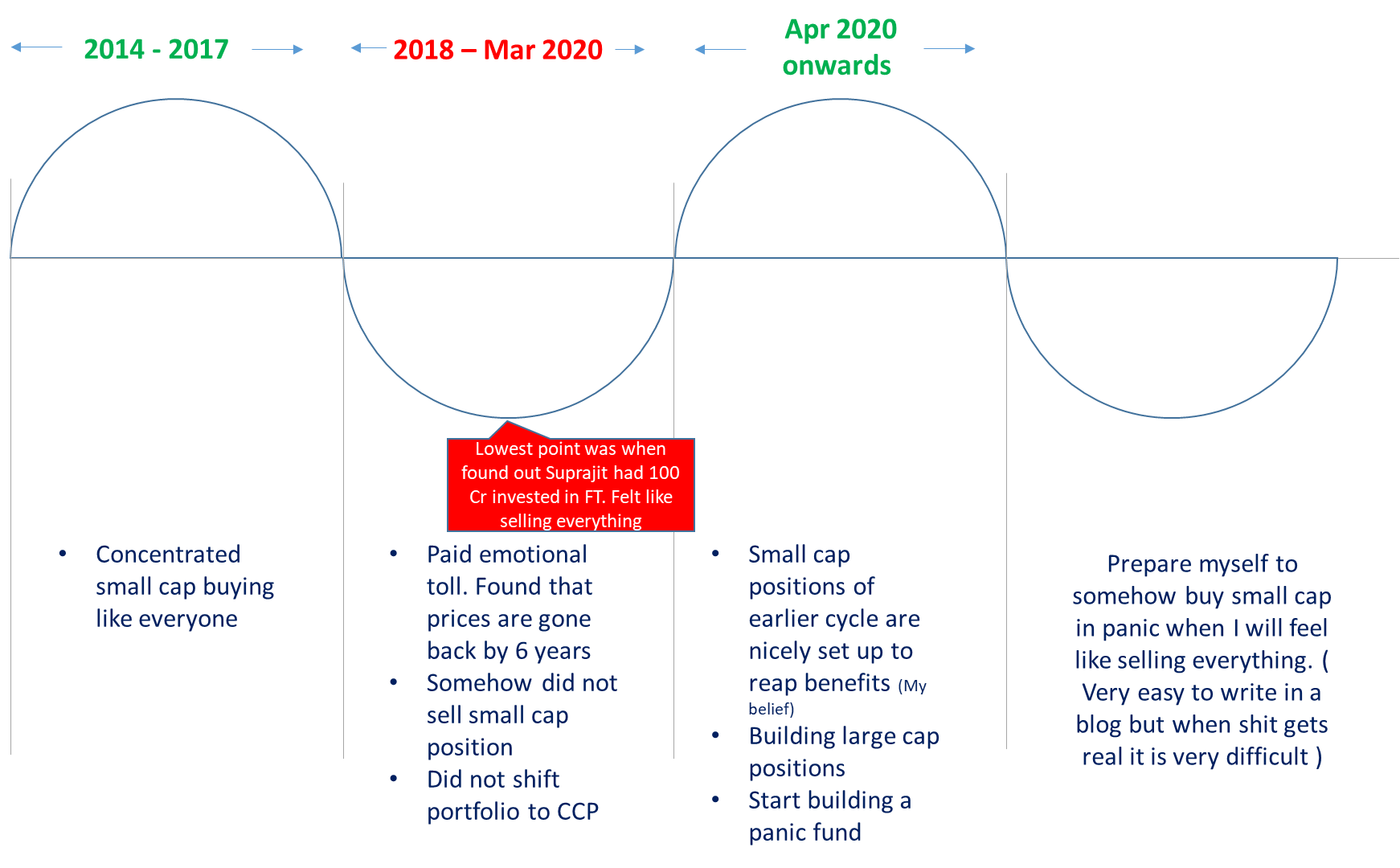

Dont repeat Suprajit

All 3 strategies - india generics, branded generics and generics have picked up traction

Focus on making robust portfolio and process which is scalable

Margins of branded generics are protected and one of the few pharma companies who executed US generics well in the past quarter

Dont let error of judgement in one company impact entire portfolio

Consistently beating IMS growth and africa/asia market growth

US FDA - be mindful

Next 5 years will be deepening existing strategies rather than venturing new startgies which reduces chances of capital allocation error

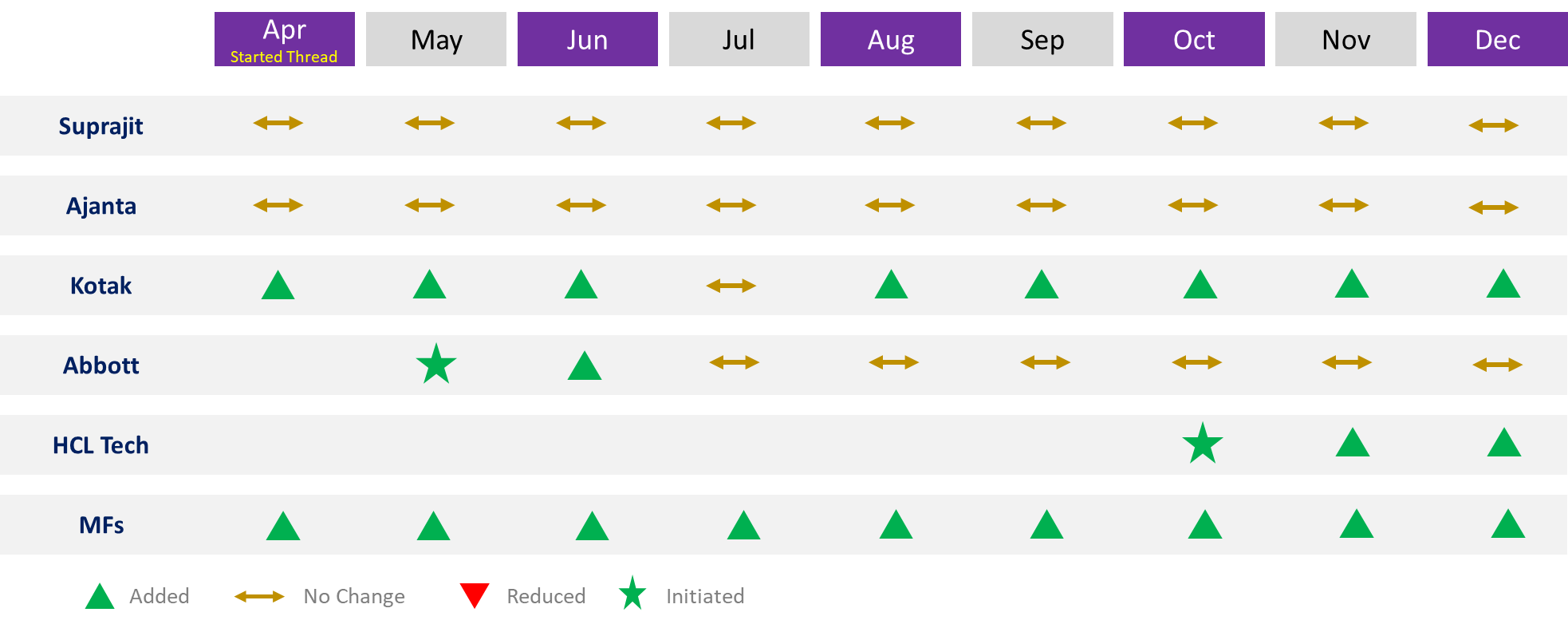

Focus on Kotak, hcl tech which gives good diversification to portfolio

I have done this before with Suprajit therefore I know how to handle this

Remember Suprajit from 2018-2020

Know your limits… in crude language “aukad me rehna”

Winner - Cautious side so far

DileMma 2 - Trim Suprajit or not (current allocation 25-30%)

Winner - Aggressive side

Dilemma 3 - mutual fund (cautious side) or direct equity (aggressive aside)

Winner - Tie

Dilemma 4 - To give importance to past data (cautious side) or focus on industry tailwind (aggressive side)

Winner - Cautious side but willing to change in next bear cycle

Pharma sector whole is down. So if possible bear. Compare performance of your holding with its competitors to see how you perform. Only when tied is low, you can see how others are.

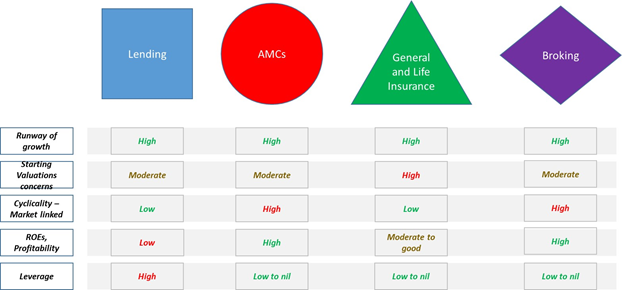

Investing in Financials (Warning – Analysis is retrofitted. Buy first think later)

If an investor is looking for mid to high teens returns then I believe blue-chip financials are the best bet because – They are amongst very few large caps which can deliver mid to high teens earnings growth for foreseeable future in my opinion and all this comes with low to no efforts. That’s a great value deal – large cap, mid to high teen stable returns and no efforts. That is why Financials are perfect fit for my satellite portfolio where I am looking for lower but stable returns (Current holdings – Kotak, HCL tech and Abbott)

We all know what this long runaway of growth comes with industry specific risks. Following table tries to highlight some of them

With all these risks in mind, I have decided to go for basket approach. That is selecting an investment which has exposure to all these sub segments.

What are the options available? – Kotak Bank, HDFC, Bajaj FInserv and ICICI Bank

Joker in the pack: Technology and fintech/insuretech disruption – My inclination is to include HDFC in portfolio but ICICI and Bajaj has superior technology stacks. Also, ICICI has to prove itself in the down cycle

Portfolio allocation – I would like to create 20% allocation for financials. 10% of kotak will be completed in next 1 or 2 months. Yet to decide about other 10%

First key decision of 2022. I have decided to boost Axis long term equity SIP by 100%. In the last cycle, these boosters during fund’s underperformance helped me to achieve behaviour premium over fund returns which helped me to achieve 20% + CAGR over long term from MF portfolio. Only time will tell if it boosts my XIRR in this cycle also. Even if it don’t, it will give more and more space (much required) for my key winners in the portfolio to run without sucking into any demons.

Duration of booster SIP will be till fund’s underperformance compared to the category

Second key decision of 2022 is to start building some sort of ‘panic’ fund. When I say ‘panic’, I am not talking about corrections, I don’t want to associate any number to it. It is a state of mind, I felt like selling everything and run away. One cannot believe what they are seeing on screens. Stock prices go back to last cycle levels. With some funny and naive hope, attempt is to buy descent small cap position in next panic. Very easy to write in a blog but to pull execution is extremely difficult. If my thread is live by then, you will find out

Going forward, I am going to add #company name ( 1yr, 3 yr, 5 yr) CAGR returns of the company stock price at the beginning of every post. It may add good value in future when I am evaluating my decisions taken in the past. Example is below