Underperformance is guaranteed (at least some of the time)

Our investments in companies ignores whether they form part of the index or not and if it is a part of the index, the weightage of the company in the index. Our portfolio looks very diff erent from the index and as a consequence, for better or worse, the performance will be different from the index.No strategy (even if it has a long successful track record) beats the benchmark index all of the time.There are times and sometimes long stretches of time where the performance of an actively managed portfolio lags that of the benchmark. In our case this is usually, but not always, seen in bull markets where the market keeps scoring via sixes and we take singles

same is true for individual portfolios - underperformance is guaranteed (at least some of the time).

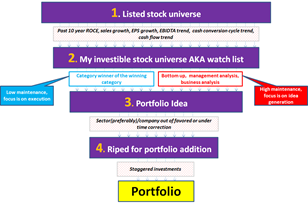

Possible New Portfolio addition alert – HCL Technologies

Key Reasons -

In Rajiv Thakkar’s language, looking to score singles and twos when the market is hitting sixes.

Good sector addition to shape up large-cap part of the portfolio

The company matches overall quality in the portfolio in terms of past track record and management quality

Analysis done before selection

Low to no analysis done. Actively tracking sector for past few years. I was working in the IT industry for the last many years but that does not give me any circle of competence in terms of investment decisions

Why HCL Tech from IT pack –

Since I have not done much homework, mid-caps and small caps are out of the question. I don’t deserve them. What I have in mind is just the overall big picture – over the medium term demand looks robust and all big IT companies should grow earnings at a descent pace. HCL tech is relatively cheap with slightly better past performance compared to TCS, Infosys, and Wipro. Valuations are still sensible (even at a premium to historic averages)

Comparing it with my investment framework

Yes

Yes

Yes

No ( As sector is not facing any headwinds/time corrections)

Return expectations (Looking to score 1s and 2s)

Since 4 = No, I will lower my return expectation - low to mid-teens (From mid to high teens)

Going in cash Vs HCL Tech

Demand look robust over medium term. Staggered allocation will give cushion if demand falls and sector start facing challenges

Why I am waiting

Waiting for Q2 margins before pulling the trigger. Though I believe focussing too much on attrition and margin is a short term thinking. Let’s see!

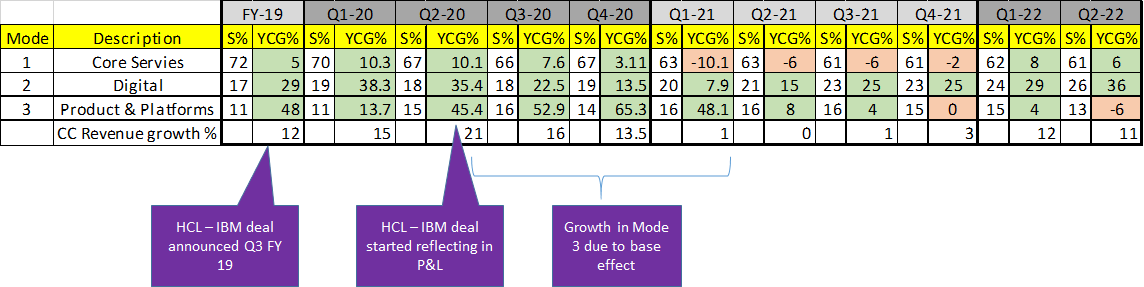

I have decided to go ahead with HCL tech investment. From Q2, there are some concerns regarding growth compared to peers and future of the product business.

Regarding growth - I believe chasing or focussing too much on growth may blur the big long term picture. Following is the yoy sales growth comparison for big 4, you can see winner keeps changing (Souce - Moneyworksforme). Thats why I beleive its better to chase farnchise value than growth. A good framchise with good management has tendancy to swing back to growth time after time. All big 4 IT are good franchises

Regarding drag in product business - Though investments are forward looking, I always like to keep one eye on the past executions. HCL management has delivered in past and thats why I would like to beleive they will deliver in future. Even if they dont deliver overall franchise value will be intact ( ROEs will be maintained )

I don’t follow hcl closely but agree see a degrowth in product business. In current enviornment of digital tailwind, I can expect slow growth but it would need some effort to achieve a degrowth…

In other words, was it a conscious effort from management to degrow their product business? If not conscious, then how did they achieve this? Also, What are their major products and they cater to which areas? If I am not wrong they acquired some IBM products also…

They seem to have multiple products, which ones are significant and why did they almost failed in them to achieve scale would be good to know…

S% - %share in revenue, YCG% - YoY Constant Currency Growth in each startegy in %

The reason for degrowth given by mangement was delay in closing few deals in Mode 3. I think scratching below this layer of analysis and to make investment decision is impossible for me. Even if I know in detail which applications are part of Mode 3, I dot have any expertise to make investment case based on that.

All I have is - one or two quarter growth here and there in one of the BU should not make much difference. Management has executed in past and therefore I am willing to give more time. Deal is still young, done 3 years back. It may succeed or fail. Even if it does not click it will not break franchise

HCL acquired legacy sunset products from IBM. The plan is to make them cloud. Native and resell them in their new version to customers

Among the acquired products is Lotus notes which is a really old mail server. They have lost some big customers on this in the recent past. I will not be surprised if this is causing the drag. My evidence on this is anecdotal.

That said they have a few other products like big fix and some security and deployment products which seem to be doing better.

Original investment thesis (The outlier) - strengthened

Summary of original thesis – The outlier (Post No. 7)

Weaknesses of Auto ancs

Suprajit Business Model

1. Margin Squeeze

Propriety product portfolio

2. Shorter product life cycle, continuous need for capex

Product portfolio with multiple segments - Indian OEMs, Global OEMS, Indian aftermarket, global aftermarket, various non-auto segments - expands product life

3. Cyclicality

Non-auto and aftermarket business act as an antidote

Original thesis to concentrate - strengthened

Proven past track record of more than 2 decades for company under a billion USD

Incredible M&A track record in terms of execution

Incredible M&A track record in terms of deal value

Transparent and conservative management

Very easy to understand corporate structure and that’s why strategy

Thesis Update

Suprajit acquired Light Duty Mechanical Cables of Konsberg for the EV = USD 42 million. The acquired entity is projected to have sales of USD 100 million next year with 10% EBIDTA margin. We are talking about EV/EBIDTA ~ 4 for a company which is around 50% of the current sales of Suprajit and which is cash generating

Why Suprajit is able to acquire companies with attractive prices deals after deals?

The reason for this according to me goes back to the original thesis of selecting product

Mechanical cable is a non glamourous product but finds its use in multiple functions and not dependent on any platform whether EV, ICE or hybrid. Example of some of the applications – door latch opening, seat movement, mirror adjustment, hood and bonnet opening etc. When most of the auto ancs player are busy investing for new technologies or to increase kit value, Suprajit’s focus is to become global major in existing product portfolio. Mechanical cables, being non glamourous, tend to be ‘’Legacy’’ products in the age of e-mobility. Since Suprajit is able to ache out margins which are more than new age products for most of the companies (Export 20%+, Domestic – 16%+), they can maintain their focus on core portfolio and at the same time buy assets at incredibly low prices.

Why this acquisition strengthens the thesis

Most of this is covered in conf-call and deck and therefore I am not going to repeat. For me it becomes truly global player in the mechanical cable space with manufacturing spanning across US, Europe and China.

Key Risks

Execution of the acquired business. As you know Trifa and luxlite (part of earlier acquired phoenix) are still crying babies

One of the easiest time period to hold on to Ajanta in the recent past. They are executing well, more importantly, compared to ‘‘Others’’. That does not mean this ‘‘realtive better performance’’ wil last. Busiensses are asymetric and each follows its own cycle. Key is to not jump from one company to another looking at recent performance ( Note to myselft and not preaching )

One of the advantages, according to me, of focussed aggression is it helps in keeping the organisation structure lean. The lean structure enables fighting cost pressures more efficiently. As per my observation, it is very evident in Q2 results that the companies trying do too many things at same time are struggling to cope up with cost pressures.

My current style of investment is buy and hold few companies for exceptionally long amount of time (ideally 10 + years) to beat mutual fund returns. I have tendency to over concentrate (which I am working on to reduce) and that’s why ‘’holding’’ can be very challenging especially in tough Macro conditions like the inflationary pressures we are in today

If company’s margins are swinging 400 – 500 bps due to inflation alone then I lose my interest because holding on to such company is not easy for my temperament. Past 10 or 15 years data gives me idea about how margins and cash flows fared in earlier period of high inflation. I believe management with proven track record of maintaining margins and cash flows in inflationary period has better odds of executing in future inflationary periods irrespective of industry outlook

When I first noticed companies/MFs in my portfolio

Suprajit

I would like to thank my MBA batchmate @ishan who introduced me to this company in 2013. He along with our other batch mates participated in the competition in the first year of our course where they presented the attached report. Suprajit.pdf (4.4 MB)

Ajanta Pharma

Scorching growth and industry-leading return ratios of 2013 – 15 brought the company to my notice. On one fine lazy Sunday in 2016, while doing head massage at my usual barber it suddenly dawned me that this company perfectly fits my philosophy and should be included in the portfolio

Abbott India

EPS, cashflow and price performance of 2018 – 20 and off course CCP tag made me interested in a company. Became part of portfolio only this year

Kotak Bank and HCL Tech

Needed no introduction. The awareness of limitation of constructing all small cap portfolio (intellectually and behaviourally) in 2019-20 and realization of these being ‘’No Brainer’’ ideas for my portfolio return expectation

IDFC tax advantage of ELSS

ET wealth – looking at past returns

Axis long term equity

Legends of axis philosophy and Jinesh Gopani in last decade

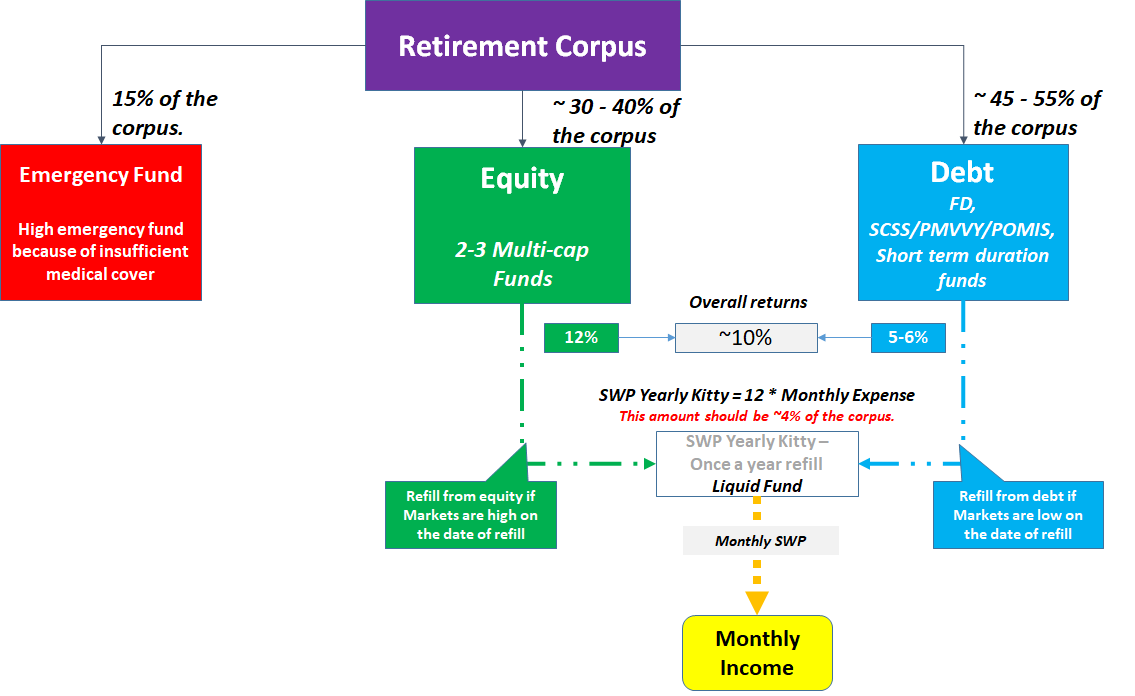

Hi, in planning above - where is the emergency fund parked? Also, the 30-40% of equity part - why you have chosen only multi-cap funds (2-3) and why not divided into Large, mid and multi caps in a desired ratio?

Also, if you yearly SWP from Equity to Liquid fund (from which final monthly SWP happens)…it further increases your debt ratio to more than 45-55% as mentioned above…as entire yearly expenses is also in debt…so if say yearly expenses is say 5% of corpus, then debt part becomes upto 60%

If emergency fund is also into debt, then it becomes upto 75% debt…

I have just given range. One can adjust based on own requirement. Return from the portpofilio shoud be > = ( Withdrawal rate + inflation ). If your withdrwal rate is 2%, you can have even higher debt portion. If you ask me excact nos in my case -

Emergency corpus - 15%

Equity - 40%

Debt - 45%

Emergency corpus will be any instrument which can give you immediate access to your money. May be 50 - 60% savings account and some liquid fund or FD

Equity or Debt to Liquid fund is not a SWP, its a manual process once year. When I am starting this process, I will keep first lot of yearly expense aside and count the corpus. Counting 4% of Annual expense in the debt or not may be not that important discussion if you have got right framework

Multi Cap ( I meant FLexi Cap) Vs 3 funds - Large mid small … I think again if I am looking for 12% returns, this discussion is not that important. I personally perfer Pareag Parekh Flexi cap and Axis flexi Cap. You can definitely have 1 large cap 1 mid cap and 1 small cap instaead of 1 Flexi cap

The reason of setting up SWP on liquid fund and not on Equity or Other debt insurement is because, we can maintain asset allocation. When markets are overheated then one can withfraw from EQuity to Liquid Fund. If Markets are down one can withfraw from Debt pool to Liiquid fund

you can juggle between Equity, emergency corpus, debt funds and liquid funds anyway you want as along as you are maintaining your asset allocation which in my parent’s case is 40% equity

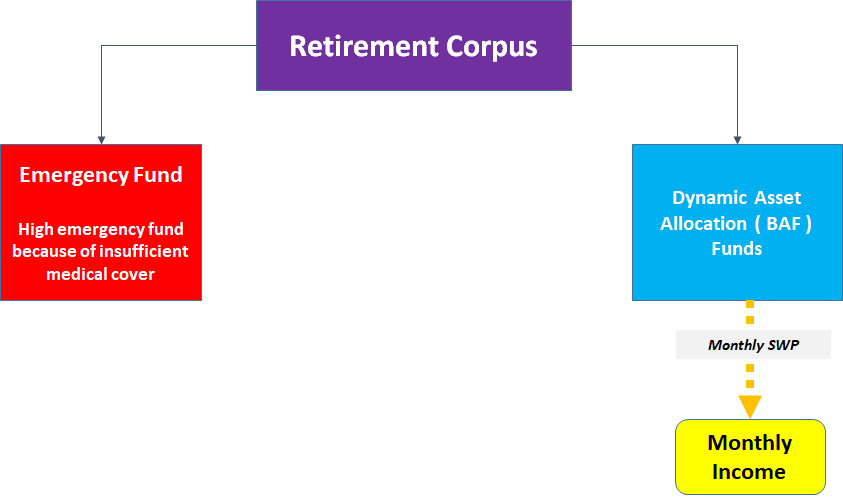

Another option according to me, is very simple set up using Dynamic Allocation Fund which are also called as Balance Advantage Funds. In this case you are leaving your asset allocation in the hands of Mutual Fund Company. Each mutual fund company has its own model to decide asset allocation. I personally really like this category because of the algorithm which decides asset allocation does not have any emotions and that is why it’s highly effective. The only problem with this kind of monthly income set up using BAF is, very few previous gen people (like my parents) are ready to put major chunk of their corpus in Mutual Funds. They are comfortable with instruments like SCSS/PMVVY/POMIS or FDs and that is where they find peace of mind to deploy their hard earned money. Mutual funds are preferred only for the part of corpus ( usually minor )

Current BAF model allocation for some of the top fund houses

Fund House

Equity

Debt

DSP

29.8%

70.2%

Motilal Oswal

42.1%

57.9%

ICICI

36.5%

63.5%

Axis

45.1%

54.9%

Also, one more added advantage with this category that it’s highly tax efficient. Even in its debt overweight avatar (like today), it is still taxed as Equity – 10% LTCG for the profits exceeding 1 L

@OmkarT bro I need your help…

My wife started SIP investment from July 2020 in a retirement scheme called ICICI Pru Freedom SIP without informing me

SIP amount every month is Rs. 6000/- for 15 years ie. till June 2035. The bank guy advised her to select 2 schemes - ICICI Blue Chip Fund and ICICI MultiCap fund. Upon completion of 15 years whatever accumulated units will be switched to ICICI Pru Balanced Advantage Fund and from July 2035 my wife will start getting Rs. 18000 (3 x the SIP amount) Every month until year 2099 or until she survives. She nominated our 6 year old kid and in unfortunate event, our kid will get the remaining amount.

I checked ICICI Pru website and checked offer document but could not understand this properly. I am really anctious to know if this scheme is good.

I have attached the document. I am graceful to you if you could check this out. FreedomSIP_DOC.pdf (1.7 MB)