Fantastic thread by prof. May god give us power to differentiate bad demons and good demons to hold on to potential 100 bagger in our portfolio if any

1 Like

Demons so far in ajanta pharma which I successfully tackled and the ones in progress

- Company has lost focus, its branded generics business in africa and asia is not growing

- Management is not interested in company as they sold 3% stake to SBI mf at 1500

- US generics business of company is a drag on a overall business

- India focussed branded generic companies are better than Ajanta

- Abbott is a cash machine, coffee can stock. Sell ajanta buy abbott

- Alembic pharma’s earnings are way better than ajanta pharma. Alembic is investing 15% in R&D vis a vis 5% of ajanta pharma. Sell ajanta buy alembic pharma

- CDMO has better unit economics than Ajanta. Sell ajanta buy cdmo( demon in progress. Hopefully i dont succumb to it. This does not mean CDMO is not a good business)

- Laurus lab , Dr chhava is a visionary. Sell ajanta buy Laurus (demon in progress. Have huge respect for Dr Chhava)

Will keep adding this list in future

5 Likes

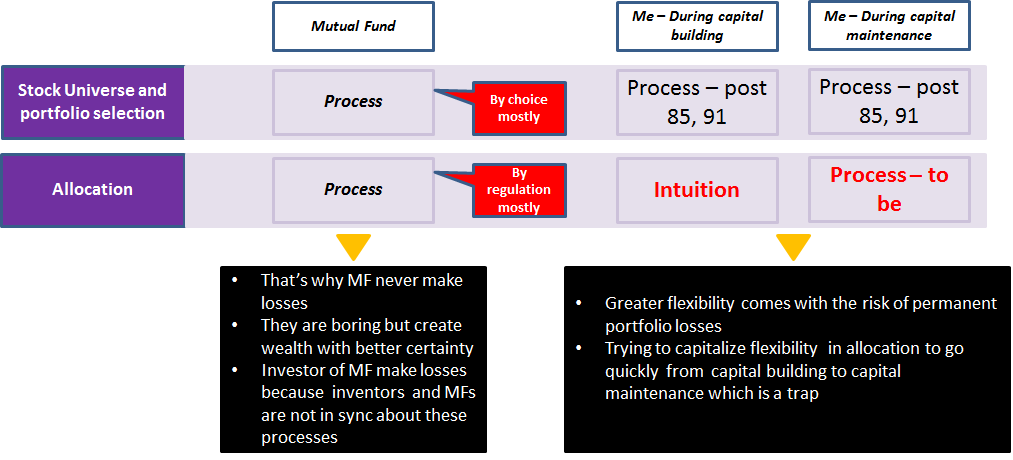

Some more thoughts on process vs intuition. Rather this is just to flush my brain and may not add value to a reader

To be process of allocation will be exactly same as mutual fund

Good to see you staying invested in Ajanta despite so many demons. This is true investing. Sticking with your stocks through testing times.

Sometimes I feel opportunity cost is quite high for such behavior and also impact on future decisions. I know all stocks cannot work all times. But you should consider building a portfolio where underperformance in some stocks doesn’t hurt much.

2 Likes

Agree with you Ishan. Sometimes too much discussion on one company ignores the outcome that matters the most - Return on networth/portfolio

What is wrong with alembic shares.Why is it not moving.

They are on a break  … no clue amrita

… no clue amrita

Please review my portfolio

Portfolio Update June 21

Direct equity - around 55% MF - Around 45%

Suprajit eng - no change

Ajanta pharma - no change

Kotak bank - added

Abbott - Added

MF - continued SIP.

Completed 6 years in one of the funds. Even though idea is suboptimal (Tax fund which is not needed in my case), the returns has been fantastic (20% +) derived purely though good behavior and discipline. If I construct a portfolio, I don’t see myself beating these level of returns.

3 Likes

Portfolio Update - July 21

Direct Equity - Around 56% Mutual Fund - Around 44%

Idea is to keep churn very minimal and try to avoid losers.

| Name | Update | Role in the portfolio |

|---|---|---|

| Suprajit Eng | No change | Lead alpha generation during domestic/global tailwinds |

| Ajanta Pharma | No change | Lead alpha generation during domestic/global headwinds |

| Kotak bank | No change | Support alpha generation along with stability |

| Abbott India | No change | Generate market returns but provide better stability |

| Mutual funds | Will continue SIP | Generate market returns and provide strong foundation |

| Cash | 0 | |

| Fixed Income | 0 |

Suprajit : Thesis Update

There is some progress wrt to point above. Suprajit launched bigger technology center and following are the comments from Ashutosh Rai - Head Suprajit Technology Center. Though, In my investment thesis I dont attach any value to something started / WIP unless executed successfully

Ashutosh Rai, Head(STC), said ‐ “The purpose of STC is to transform Suprajit from a

manufacturing‐centric organisation into a technology‐driven organisation. Suprajit

should be considered as a strong design partner of proprietary parts in technically

challenging environments and industries, with our focus being on mechanical systems,

display and infotainment systems, and control systems. The ultimate goal is for STC to

rapidly conceptualise, design, prototype, test and validate new products that become

the next cornerstone product line of the company. The new Centre will be fully

integrated, with the ability to take an idea from concept all the way through to first

batch production under one roof. Suprajit will be in a unique position as an extremely

lean and frugal manufacturing outfit that is complimented by a highly effective new

product design capability, executing the complete cycle for the customer from concept

to commercialisation.”

Overall except trifa/luxlite (Around 10% of revenue) all divisions are performing decently.As SENA and Gobal aftermarket picks up traction, business model becomes stronger as revenue streams become less and less cyclical

1 Like

Thesis Update - Axis Fund House

I have been an investor in the flagship scheme of the Axis Fund House - Axis long-term equity fund - from Dec 2015. The XIRR has been astonishing 22.22% as of Friday - 3rd Sep 2021. More heartening is the fact that this exceptional performance has come with low volatility. In the last 6 years with the fund, there was no moment where I got anxious or nervous because of the large downside swings. The low volatile (low beta) nature of the fund helped me to stick to my SIPs peacefully without any ‘’thought demons”. The overall experience was rewarding and it confirms my belief of mutual funds being an ‘Alpha generators’ as good as (or even better than) direct equity option in my case. I don’t consider mutual funds as a ‘’secondary’’ equity vehicle anymore.

Original Thesis Summary: Axis Fund House

1. Differentiated Investment Strategy within Fund Houses

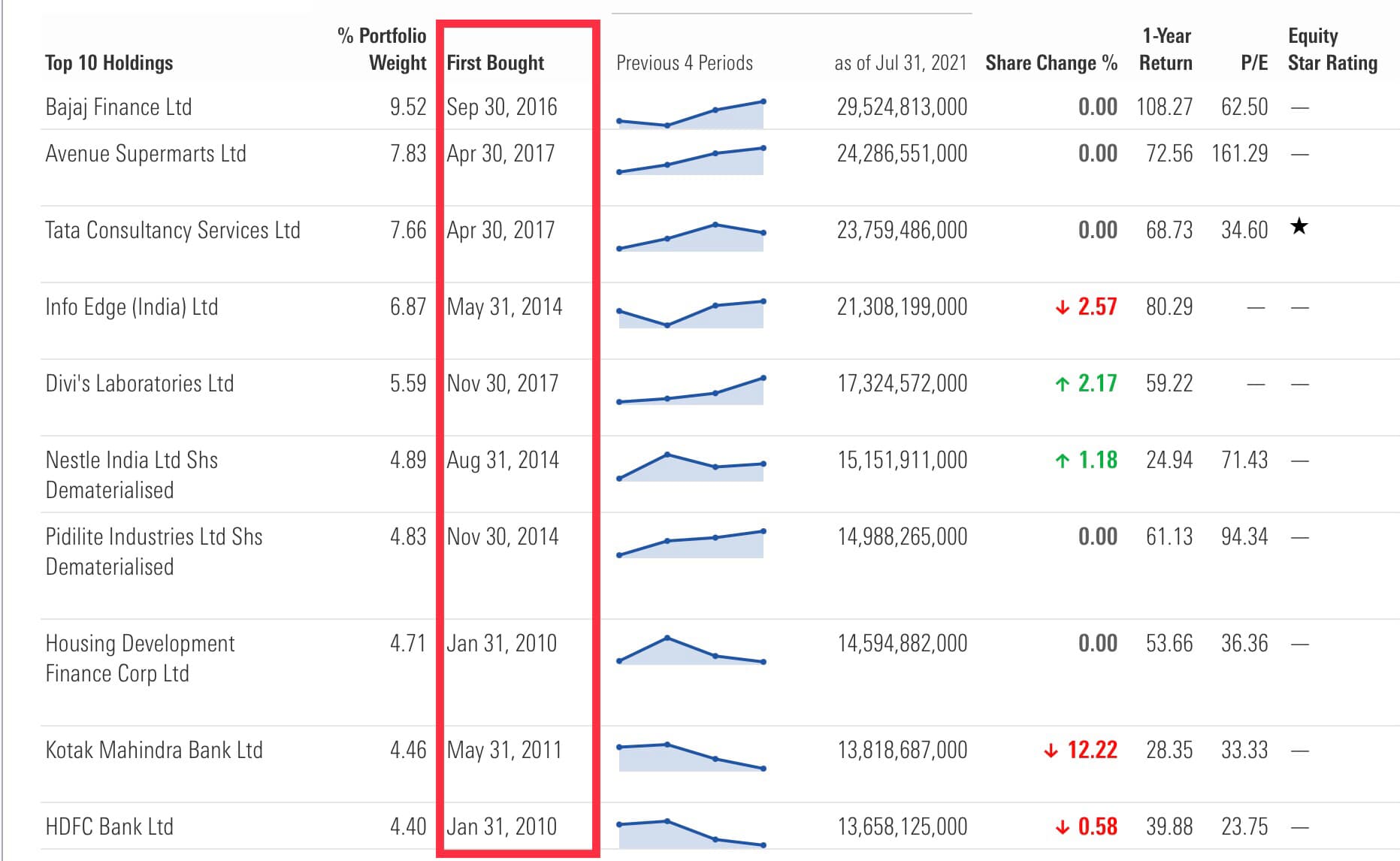

There are only two fund houses that do not mind paying up more than usual market consensus for the stable cash flow generating businesses with good managements - 1) Motilal Oswal Fund House and 2) Axis Fund House. Within these two Axis has executed this strategy more successfully. Axis usually does not mind paying up for the businesses which qualify their investment philosophy of - business with good management, good corporate governance, which have executed well in past cycles, which have stable cash flows & growth, and businesses that are scalable. Once invested they usually do not change their top holdings. The following portfolio screenshot shows that the most of their top 10 holdings which form 60% of the portfolio are part of the portfolio for last many years. Source: Morningstar

2. Size of AUM

Investment limitations due to growing AUM size is one of the most common reasons sighted to highlight why mutual funds are not conducive enough to generate high returns. In my opinion, Indian equity markets are just getting started. The current market cap will look like peanuts in the future when the depth of the market increases. Therefore I do not consider AUM size as a hindrance in the way of generating higher returns.

Also, Axis’ investment strategy is highly scalable. The AUM size of Axis’s long-term equity is 30,000 Cr +. For this ‘large’ AUM size, the portfolio is pretty compact with a total no of stocks = 30 and within that top 20-25 stocks occupying more than 90-95% of the portfolio. Therefore I believe that future returns will not be limited by AUM size. The outperformance or underperformance will be the function of the execution of the strategy

3. Clear Communication

Communication by the fund house, according to me, is a very important aspect of the investment strategy. Fund house should highlight when the strategy will underperform and when it will outperform. Since no strategy outperforms all times, this communication by the fund house forms the basis to judge whether underperformance is due to strategy is gone out of favor or due to the process is broken. Axis’ communication and performance are in sync so far. As communicated, funds underperform during a raging bull market but they tend to outperform during sideways or negative market conditions. This has helped me to stick with the fund during its underperformance in 2016-17 and recently in the post-COVID rally

4. Fund house that used to follow only one style. But not anymore?

One of the most important reasons why I am invested in the Axis MF schemes was their relentless focus on the strategy. Axis MF CEO Chandresh Nigam has mentioned multiple times in the past that as a fund house that follows the ‘Growth’ strategy, they do not want to indulge in the ‘Value’ strategy. Adopting the same strategy across schemes helps them to execute their strategy with greater focus and clarity.

So what’s change now?

Axis is launching the Value fund soon. NFO for which is already open. Jignesh Gopani who’s is the poster boy of ‘Quality’ is going to manage a new fund. Prima facie this looks business as usual and also how they define value is not yet clear. But as a long-term unitholder, it has raised all sorts of doubts for me- (1) Why is Fund House digressing from the previous communication? (2) Can this shift in focus result in not-so-good performance in the future? (3) Does this step changes their core philosophy? Only time will tell whether it is a ‘good demon’ or a ‘bad demon’.

What I am going to do?

At this stage, I am going to wait and watch. It may take 1 or 2 years based on market conditions to decide if Axis is losing its charm because of digression from their core strategy

2 Likes

I was amazed to see, last 5 year SIP performance of different schemes. Just taking Axis fund house as an example, following are the 1,2,3 and 5 year annualised SIP returns.

Source: moneycontrol, SIP returns section

Annualised SIP returns - as on 6th Sep

| 1 year | 2 years | 3 years | 5 years | |

|---|---|---|---|---|

| Axis long term equity | 57.08% | 42.69% | 31.99% | 23.25% |

| Axis mid cap | 67.32% | 52.07% | 39.3% | 28.15% |

| Axis small cap | 80.78% | 60.59% | 45.39% | 30.05% |

2 Likes

Really good way to monitor/assess and review mutual fund performance

2 Likes

Portfolio update - September 21

same old

Holding - Suprajit, Ajanta pharma

Building position - Kotak bank, abbott india

Mutual fund - SIP continues

What i did in this bull market so far

- Not much of a time spent on research but spent time on improving job prospects. Improved ‘P’ in P (1+r)^t.

- Trying to be mindful about bull market mistakes. Risk averse and choosy in stock selection but extremely aggressive equity allocation. 0 cash, 0 debt

- Due to my mediocre stock selection abilities, i still think concentration is the only way to beat mutual fund returns for me

- I am convinced that promoters make highest amount money in stock market compared to institutions and investors therefore i try to maintain 0 churn

6 Likes

Liked your all 4 points. Regarding above full allocation to equity, how much is your bifurcation in direct equity vs MFs in percentage?

Latest -

Mutual fund - 47%

Direct equity - 53%

1 Like

Important points Omkar…

You have decent MF portfolio, can you share the MF scheme names you are holding…

Thanks.

As mentioned in the first post