This is very interesting. A year-back things were not so rosy when looking at near-term performance but have changed drastically now.

But as you rightly pointed out there is not much difference in long-term performance. It is time to stay clam and we should never extrapolate short-term performance.

When we invest in a company, we are typically looking to stay invested for a minimum of 5 years. Investors in our fund should have a similar approach to investing. We also do not force ourselves to be fully invested at all points in time and may have cash equivalents and / or arbitrage positions in our fund.

We do not expect our stocks to outperform the indices on a weekly, monthly or yearly basis and the comparison comes into picture only over a longer time horizon. There have been numerous occasions in the past where our fund has lagged the indices and there will surely be such occasions in the future.

To the extent that we are not in the hottest sectors of the moment and that we may see some build up of cash in the portfolio, the fund could see some underperformance in the near term.

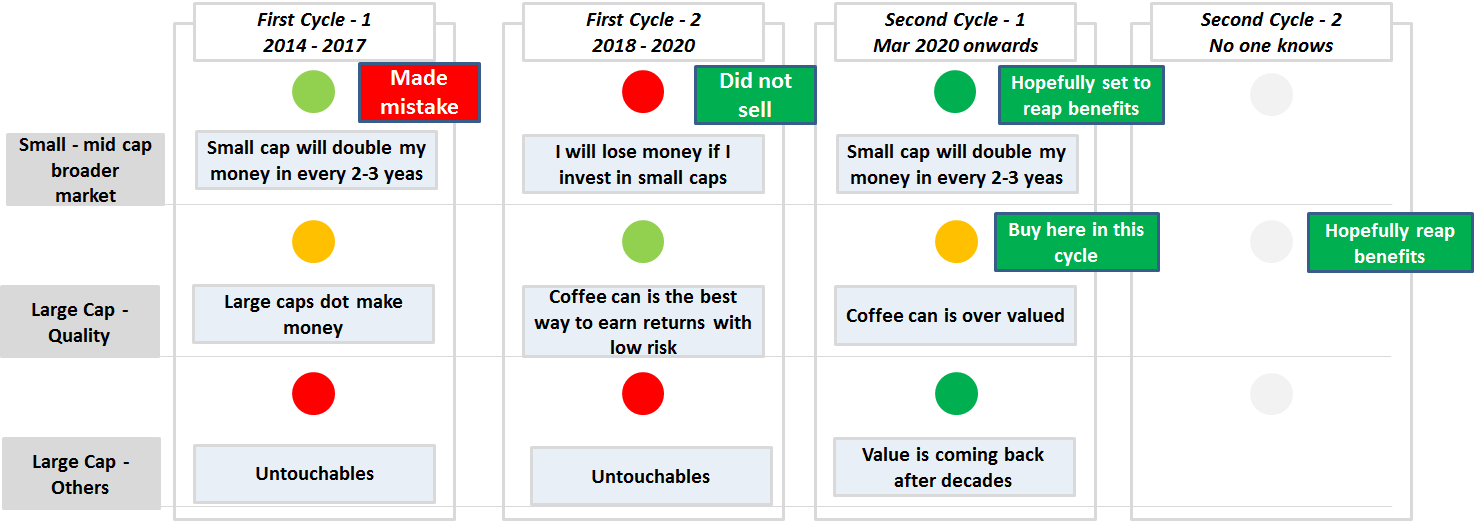

Approach is to try to be ready for next cycle with incremental capital than enjoying returns of this cycle

Quality underperformance can be really long this time same as what prashan jain’s elongated underperformance in last cycle

Long quality underperformance window can be exploited to be ready for the next turn of quality outperformance

Most likely, my small cap allocation with incremental capital will start in next cycle than this cycle. Hoping current small cap allocation which was built over last entire cycle will give some rewards now.

I like this definition of risk–“Risk is what is left after you have thought through everything that can go wrong.”

The usual risks such as raw material fluctuations, customer or supplier concentration are not as big a risk. If a risk is understood by the management, you can evaluate whether they are aware of it and actively working on reducing it. For example, FDA audit risk is now a known risk and investors can evaluate how the management is addressing it. This was not the case in 2015, when the challenge first appeared.

Assuming one has not paid evidently high prices for portfolio companies, long term portfolio returns will gravitate towards the collective earnings growth of portfolio companies

The return for the investor of the portfolio depends on the collective earnings of the portfolio companies and investor’s behavior. Depending on how investor “behaves” behavior can provide premium over earnings growth or it can drag returns below earnings growth

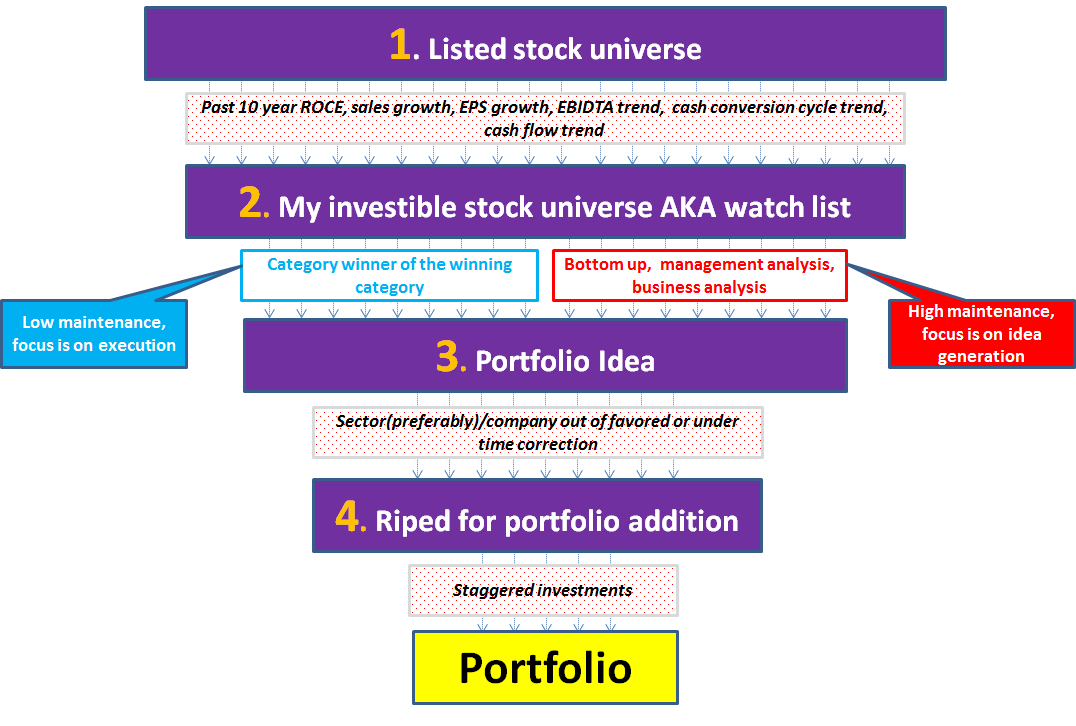

Earning growth profile and behavior equation for my portfolio companies

Category

Earnings Profile

Behavior Premium Possibility

Category winner of winning category

Mid to high teens

Can be high because of lower volatility and established business

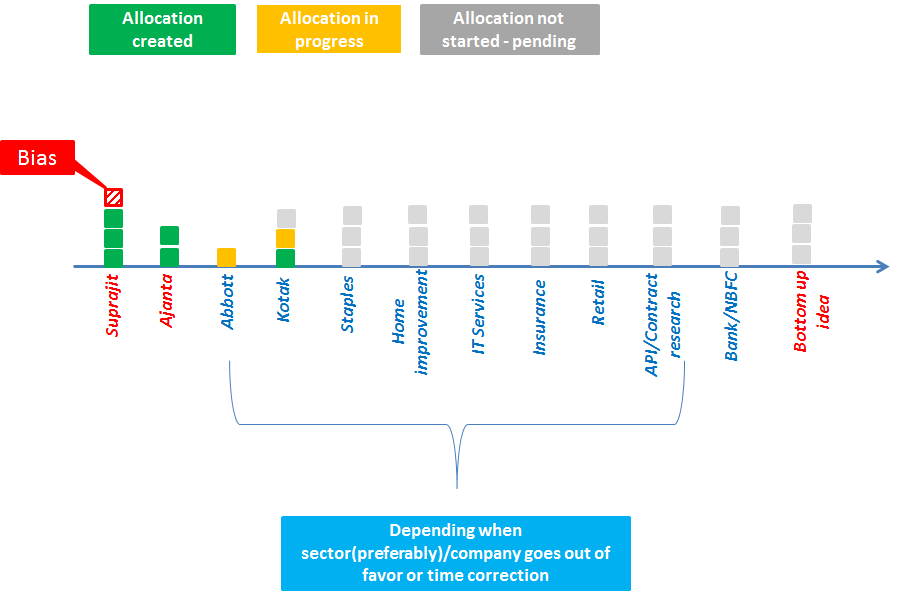

Buying kotak bank at 1100

Bottom up

20+

Low to nil because of high volatility and not so established business

Not able to buy Suprajit at 100

Combining both, my aspiring return expectations are – portfolio returns of mid to high teens + behavior premium. But let’s be conservative and assume my behavior will have no impact on the returns or even with good behavior portfolio earnings growth is low teens. Therefore mid to high teens return expectations are fair to assume

Opportunity cost

The reason I am a big fan of Mutual Funds because they have best possible framework to boost behavior premium. All one has to do is know the fund’s strategy, understand when it underperforms, buy more units with few clicks when strategy is underperforming and stay discipline with SIPs for rest of the time. Last week before market corrected on Thursday and Friday, my mutual fund portfolio XIRR since Jul 2015 touched 20% and settled at 19.5% by end week. My behavior premium is around 300 – 350 bps in the mutual fund XIRR achieved.

My effort is to build a framework/approach which will enable behavior premium as good as if not better than mutual fund framework

Very inspired by your story sir . I am also investing in MFs my current mf portfolio is Parag parikh flexi cap, Nasdaq 100+ Edelweiss china off shore fund , SBI index 50 ETF, Axis small cap for next 15 years.

Can you please review my portfolio and any suggestions for me ?

I usually refrain from giving portfolio advice because first of all i am also amateur and second there are many ways to make money in the market.

Therefore i wont comment on your portfolio. You must have thought something different than me which is more suitable to you. I will just tell you my thought process

I like to make fewer decisions and that reflects in my MF portfolio as well as direct portfolio

For MF portfolio, as per my thinking, 2 multicap funds with complementary strategies are good enough.

For mutual fund selection- you can refer to the post i have shared earlier

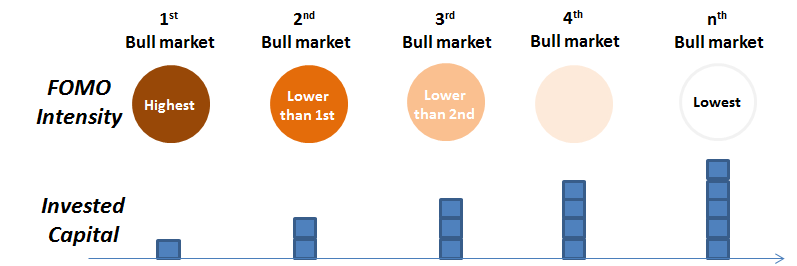

As a 90’s kid, this was the famous RIN ad I grew up with. The advertisement exploited the behavioral flaw of human nature – ‘The tendency to compare’. The bull market is manipulating me on the exact same lines, making me think ‘’Bhala uski earnings mere earnings se jyada kaise’’

What I earlier thought about second bull market FOMO

Earlier I thought the second bull market FOMO will impact me lesser than the first bull market FOMO because - now my portfolio size is bigger than first bull market and that’s why, I can settle with lower but steady returns

Reminds me one quote of famous Peter Lynch book I am reading nth time…“you don’t lose anything by not owning a successful stock, even if it’s a ten bagger”

In adverse situations like melt down or up, I tend to read such books which make me cut the noise even after being right in middle of noise by listening to one of most sensible person…it’s kind of he reinforces things I already know in the most positive manner…it’s strange that we keep needing such reinforcements…only says I am just a beginner!!