My thoughts on investing in the Insurance industry

Before jumping on topic, some thoughts on Circle of Competence

I slightly disagree with Mr. Buffet on ‘Circle of Competence’ at least for my temperament. To give example - I have been working as a Business Analyst / Business Consultant with an IT firm for 7 years now and all these 7 years my experience is in the Insurance domain. (My LinkedIn profile). I have worked with various global / Indian insurers both in life and general insurance. I have worked across functions of sales & distribution, business development, claims, strategy, etc. My knowledge about the insurance industry is easily 100x better than the auto ancillary and pharmaceutical industry. Ironically, I am not capable of making investment decisions in the insurance industry but I am taking bets on the other two.

My current belief is that investing is counterintuitive in this aspect. The usual belief of - more we read or gain knowledge the stronger is the circle of competence does not apply to me. I would like to believe Mr. Market more than my circle of competence to take decisions. In some cases, Mr. Market has made life easier for me to take decisions. For example - investing in HDFC bank/ Kotak Bank is one such gift from Mr. Market. These are high-growth companies with a huge runway for growth where Mr. Market has leaked the entire information one wants to decide without any circle of competence.

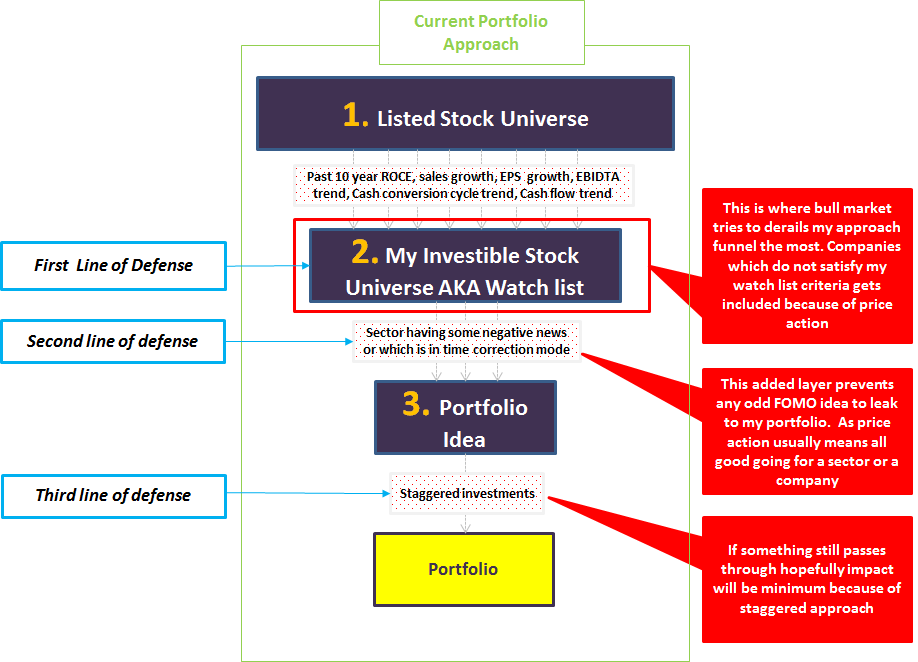

This thought process is one of the building blocks of my WIP investment approach

What has Mr. Market told me about the insurance industry?

There was a great thread on the Insurance industry by JST Investments today on Twitter

Tweet number 24 is the reason why I have not invested in the Insurance business so far. Quoting same below

“However, underwriting remains a function of management. If one can see them go through a few storms unscathed, then one can bet. Indian private insurance companies are no more than 20 years old, relatively young compared to western peers, so be cautious”

In our journey as an Investor, I believe Mr. Market sometimes screams at you to tell you to invest so that retail investors can make decisions even without the circle of competence. For the insurance industry, I have not received such a signal so far or maybe I am failing to grasp it

Simple hack to invest in the Insurance industry

With all these limitations in decision making, I am still convinced of the growth prospects and that is why I would like to participate in the growth phase of the insurance industry. The simple hack I am using to cover myself is investing in Kotak Bank and in the future Bajaj Finserv, which has an insurance business along with the lending business.

Watchlist – HDFC life and ICICI Lombard