I am aggressive in equity allocation (100%) but little conservative in portfolio selection. Mid to high teens return over long term looks reasonable to aim for with my style

For a mid teen to high teen result, why would I prefer active investing to - blue chip or large cap mutual funds (quite a few of them are showing results in that range), and if I was aggressive, both motilal oswal nasdaq ETF and ICICI Pru tech sector funds have returns significantly beyond that range.

Shouldn’t I be targeting returns, if I’m actively managing, in the range of at least 30 percent and upwards? Otherwise, why spend so much time and effort?

1 Like

Please read post no 27 sorry not 28

Went back and read that. unfortunately, it did not answer my question. It talks about how your philosophy changed. But it does not illustrate why your philosophy is profitable.

I will delete this post if it is inappropriate.

I am echoing your thoughts. I also think same

Thank you.

Seriously, thank you.

My thinking is the same. Have a full time job which basically takes up most of my working week time. MF investments, if you basket it properly, and rebalance annually, with some sectoral exposure risk, seems good enough to return 20+pc in average years.

So if I am going to spend time and effort in portfolio management, I would want to target return in x bagger bracket.

Yes. This is likely to be higher risk and higher return profile, but otherwise there is no reason to do it, IMV.

Thanks for entertaining my questions. Much appreciated.

Post 3 - of Learning Portfolio Construction from mutual funds – Allocation and position sizing

Numbers of stocks in the portfolio is the highly debatable topic on any portfolio related discussion. Let us have look at some data from industry

| Mutual fund name | Category | Number of stocks | Last 7 year CAGR returns |

|---|---|---|---|

| JM Core 11 | Large Cap | 11 (yes you are reading it right) | 13.52% |

| Axis long term equity | Large cap focussed multicap | 29 | 18.48% |

| IDFC tax advantage equity | Small cap focussed multicap | 52 | 18.04% |

| Mirae emerging bluechip | Mid cap focussed multicap | 63 | 24.98% |

| DSP small cap | Small cap | 65 | 22.35% |

For a professional fund manager there is no correlation of number of stocks and return. What matter more is the philosophy.

Upper limit of 10%

I consider this thumb rule as the best risk management technique and this cap of 10% results in better risk adjusted returns and has been responsible for making mutual fund experience pleasant

Learning and takeaway

There is lot of things going in my mind regarding this aspect and that is reflected in my confused portfolio strategy. I am just listing down those thoughts and they are conflicting

- Do I have a resources to cover higher number of stocks

- Considering companies like kotak bank, nestle (common sense companies) requires low maintenance, why should I worry about resources required for higher number of stocks

- If I construct a portfolio with ‘common sense companies’ I am not going to do anything better than a mutual fund

- That’s why is a super concentrated portfolio, only way to beat fund manager. As I do not have capacity to construct a portfolio with mid small caps

- What about emotional toll of the super concentrated portfolio. For 5 years nothing happens and on 6th or 7th year portfolio recovers all the past underperformance

- What about downside risk of super concentrated portfolio

- Should I just go back and construct a normal diversified portfolio

- Do I have resources to cover higher number of stocks (Infinite loop continues)

3 Likes

Post 4 – Learning portfolio construction from Mutual Funds – Market cap equation

As usual, to start with let us look at the industry data

| Category | Best CAGR returns in last 7 years | Category average CAGR for last 7 years | Volatility-(Category level – Thumb rule) |

|---|---|---|---|

| Large cap | 16.66 | 12.83 | low |

| Flexi cap | 18.48 | 14.88 | Moderate |

| Mid cap | 22.53 | 18.68 | Moderate to high |

| Small cap | 27.98 | 20.18 | High |

Point of view from the data

-

If investor was able to withstand high volatility of small cap, then he/she has been rewarded with higher returns

-

Large difference in the small best performer Vs category shows the importance of stock picking in that category

-

Most of the Flexi cap schemes are leaning towards large cap and that is why returns of large cap and flexi cap look in the same range ( Recently SEBI has introduced Multi cap category with clear mandate of having at least 25% in each of small, mid and large cap

-

One missing point here is comparing – MF returns Vs Investor returns. Even though small cap category is showing higher returns, it does not mean investor in the small cap category has earned the same returns. High volatility results in investors returns lower than mutual fund returns

Learnings and takeaways

- I don’t want to believe I have capacity to construct all small cap companies portfolio

- I don’t want to believe I can handle the volatility which comes with all small cap portfolio

- I would like to choose best of 3 worlds – Large, Mid and small and limit mid, small cap exposure to 50% max

- Market cap discussion should also tie in with overall philosophy of the portfolio

2 Likes

Flaw in above argument as suggested by Harsh - As I should compare return wrt to bull / bear cycles - (Peak to peak or trough to trough) … ignore the first part of above post. It is not reflecting right picture

Some of the current thought process bites. Not necessary they will remain same in future

Where did I spend my time in last 3 – 4 years

| Item | Amount of time spent (approx.) | Details of time spent on | Portfolio reflection |

|---|---|---|---|

| Suprajit engineering | Very High – Both reading and thinking | I track almost all the Indian auto ancillary companies quarterly updates, track global auto giants and their quarterly updates | Efforts and (bias) are reflected in the portfolio allocation. You can gauge from write up - post 6 and 7 |

| Mutual fund and fund manager analysis | High - Reading and thinking | Following fund house’s strategy, portfolio manager’s thinking, Monthly factsheets of top fund houses | Reflected in the portfolio allocation. |

| Risk management and avoiding big blunders | Moderate to high – Reading and thinking | Trying to learn from other’s errors as much as possible from Twitter and VP threads | So far no big blunder |

| Ajanta Pharma & pharma industry | Low to moderate – More thinking, less reading | Company specific updates and tracking other peers only in formulations space | Descent allocation |

| Other company / industry analysis | Low | Tracking handful companies and haven’t done deep dive in any | Very low to nil allocation |

Core and satellite portfolio thinking

I consider my allocation in Suprajit and Ajanta as a core portfolio ( By end of 2021, this will be around 30-35% unless they move up sharply) and rest of the satellite portfolio is a facilitator to allow me to hold these 2 companies as long as possible. Therefore satellite portfolio will be lazy, common sense portfolio (Kotak Bank is part of satellite portfolio)

Satellite portfolio is kind of contingency fund for a core portfolio. I also maintain high contingency fund. Making sure I am setting up right infrastructure for long term compounding

Success so far?

So far, there no big success from my core portfolio. I was in the position building phase and my average cost for Suprajit is around 250 and Ajanta around 1400. The next big bet in core portfolio will come only when I have some success in these core positions. If they fail, there will be introspection needed on overall approach and thinking

Plan for next 1 – 2 years

Irrespective of success / failure of core portfolio, I plan to deep dive atleast 1 company at the level of Suprajit. And take allocation within core portfolio limits if time permits (depending on the success)

3 Likes

Abbott India

I am really impressed with the ability of Abbott India to generate cash. FY 21: CFO – 726 Cr. Capex – 23 Cr. Dividends paid – 531 Cr

Company does not have to do much R&D as products are borrowed from the parent and even manufacturing is outsourced. Which results in lot of cash generation

Error in the thinking in the past

Till last year, I thought only risk Abbott faces is the pricing risk and I based my judgement on how company performed when its product came under pricing control last time. When Thyronorm came under pricing control (I think 2014 or 15), there was a minor setback for a quarter or two but because of low price, sales ballooned and that resulted in greater operational efficiency

This was ok until last year when one of their power brand Duphaston (for woman infertility) suffered a challenge. Until 2019 Abbott (parent) had a monopoly over a drug. That changed in 2019 when Mankind pharma came up with the generic version and pushed its sales in India which resulted in market share loss in Duphaston. Abbott India relies heavily on its power brands (Duphaston being one of the largest) suffered a drop in revenue because of the impact on only one brand

Though overall impact was limited, I was disappointed with myself because I was completely blind to this risk. It also damaged my overall confidence of risk understanding of the company

Going forward

I still think overall franchise of the company is intact and this company is a good fit for my satellite portfolio. I would like to consider and think if I can allocate 50% of my 1st June equity instalment to Abbott india and 50% to kotak Mahindra bank

Valuations

Valuations are definitely a concern but I am not looking for high returns from my satellite portfolio part ( MFs and kotak mahindra as of today). I am looking for longitivity and stability

3 Likes

This is perfectly true and counterintuitive. The general perception is that the more effort and time you put in something the better reward/returns you expect from it. However, when it comes to portfolio construction & management spending more time and effort doesn’t necessarily result in higher returns. Sometimes over-analysis in few stocks can hurt your portfolio. As per facts are concerned, majority of fund managers in the western world with all the skills fail to outperform the benchmark returns.

I feel investing is more of a game of patience and temperament and less of IQ. Over a long period of time if you can generate mid to high teens returns even by investing in mutual funds or passive funds then you will end up a huge amount.

I strongly recommend reading (if not already), ‘The little book on common sense investing’ by John Bogle

1 Like

Please consider Wonderla Holidays, stock is still down, need conviction to hold, pre-covid it had excellent margins, smart management and entry barrier is there as good investment needed to install or build same level of park.

Your views are very good.

Disclosure: Not invested in wonderla and these are all my personal views.

2 Likes

Thanks @OmkarT for bringing this stock into discussion.

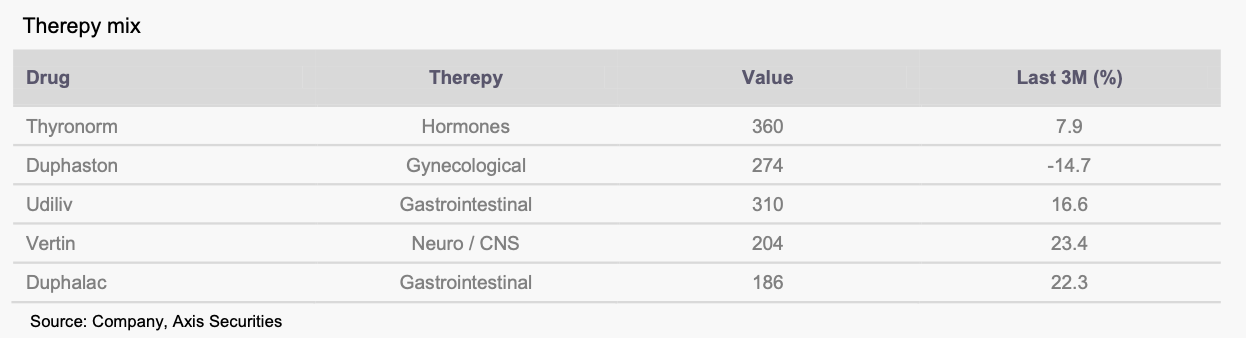

So all companies face competition (except google :)) but some good comapnies over a period of time try to create a strong moat either through processes, research & development, operational efficiency and many more things. Same is the case for Abbott India.

New launches

Abbott India is continuously expanding its portfolio and trying to bring newer products to Indian markets. There were 100+ launches in last 10 years.

Contribution of Power Brands

Here is how their power brands have grown/de-grown. So despite strong de-growth in one of the power brand, Abbott India managed to grow in Jan-Mar 21 quarter

Long-term performance of power brands

Margin Improvements

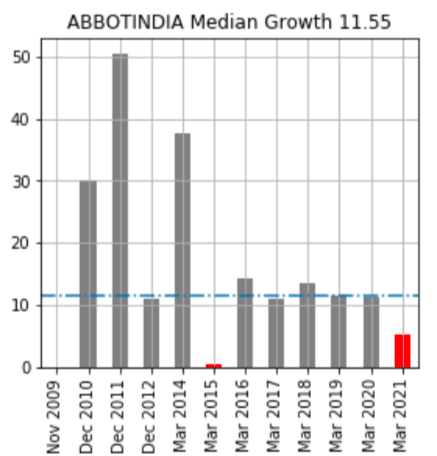

EBITDA margins have recovered from lows of 11.8% in FY14 [due to inclusion of one its top brand (Thyronorm) under price control] to 21.4% in FY21.

A good thing to observe is that despite challenges such as pricing control on Thyronorm and high competitive intensity in one of the power brand, the company is still managing to grow or stay flat. The business model is still intact with debt free balance sheet and favourable industry dynamics.

When others are fearful on a wonderful business it is time to be greedy.

Disclosure: Invested in Abbott India.

1 Like

Great thoughts Ishan. Only thing I feel is there is not much fear as such for Abbott. Real fear will be when - 2 brands get challenged at the same time or 1 gets challenged and 1 comes in price control. Revenue falls by 15% and EBIDTA falls by 30%, these are real challenging times and very difficult to keep on adding during those times

I have experienced same with Ajanta - all risks struck at once - Africa Insti sales hit, currency challenges in africa and asia market, dermatology degrowth and US business front ended cost. That was a real fear when EBIDTA is down more than 30 - 40%. It was very difficult to keep on adding during those times. All I could do was hold existing position.

2 Likes

How to select Mutual Funds

I am a big fan of mutual funds. I will complete 6 years of investing in mutual find this year and experience has been really good so far. Some of the reasons why I like mutual fund are

- Superior risk management and sound portfolio creation

- Easy to implement dollar cost averaging

- Easy to average up in bull times

- Easy to average down in bear times

- Can easily absorb large capital

- Possible to invest in multiple styles of investing

- Highly transparent

Most of time investors are disappointed with MF giving lower returns. I believe rather than focussing on better returns if I focus on being better mutual fund investor, returns ‘zuk marke piche aayega’

There are two aspects of being better MF investor – better behaviour and better MF selection. Behaviour part is discussed widely in various forums but MF selection part is the less talked about. MF selection is usually arrived by looking past 1/3/5 years returns. There is a lot to MF than just returns and Arun – Eighty Twenty Investor has explained the process of MF selection really well. His writings have very high influence on my thought process, He also maintains live mutual fund SIP portfolio which is 2.5 years old

Following three parts articles series explains his though process of MF selection which I have found very useful and I implement same thought process in my mutual fund portfolio

How to select equity mutual funds the eighty twenty investor way – Part 1 (Link)

How to select equity mutual funds the eighty twenty investor way – Part 2 (Link)

How to select equity mutual funds the eighty twenty investor way – Part 3 (Link)

2 Likes

If we use Maths then the probability of any one event happening (price control or power brand faces high competition) is very low. If you extrapolate then the probability of any two events happening simultaneously is even lower.

Definitely, the valuation at which you can own such business when two negative events have happened will be extremely lucrative but so is the probability of such a scenario to happen.

Source: Wisdom of Great Investors – Quotes | Davis ETFs

If we take a look at the last 10 years history then there are two years namely 2014-2015 and 2020-2021 where the company has failed to post a growth of 10%.

So another way to think about your expected scenario is to invert. When would Abbott’s revenue fall by 15%? You would come to the conclusion that maybe three such events should occur and not two. How much compounding will I lose by waiting for the scenario to happen? ![]()

You might say to look at other side of the coin if I invest, how much money will I lose if such a scenario happens?

I feel such risk management is better handled by creating a portfolio of stocks. Even if Abbott is facing a 15% revenue loss, other businesses in your portfolio should be able to nullify such impact.

1 Like

Agree Ishan with your view points. Beyond a point I can not do much about company specific risk. Best is to hand over that task of risk management to ‘Portfolio’

Gyan Aert! I have exhausted all the topics (Except one left for portfolio construction). Also, my knowledge acquisition rate is low. That’s why there is a risk that the reader may find the next post (s) ‘’gyaan’’ than a solid knowledge. Nevertheless, it may give some inputs around behavioral aspects.

Following process Vs following my intuition

Last week I was listening to a live YouTube session by Parimal Ade. I was interested in what kind of questions people are asking. Though most of the questions were related to an individual stock, there was one point discussed which drew my attention. The point was simple and obvious but still very important. It was about following a ‘’process’’ and not your ‘’intuition’’ to avoid errors and to enjoy the benefits of long-term compounding. It made me think about what did I do so far and why?

The journey so far:

Phase 1 - Process was thrown out of the window

I realized, till today I have followed anything but my intuition. Concentrating in one stock, owning a portfolio of 3 stocks are the hallmark of intuitive decisions. Why did I follow my intuition and not the process –

- The first reason is I did not know what is the right process

- Second, the more prominent reason was – When I started my journey, I had very small capital and my focus was on converting small capital to sizeable capital by taking ‘’risk’’ and not by following process. The belief was ‘’taking risks’’ will help me achieve the goal of sizeable capital quickly. Following “process” felt more bureaucratic and my ‘’intellectual ego’’ was making me lean more and more towards intuition

Phase 2 – Thanks to Mutual Funds, the importance of the process was understood

Fortunately, I never stopped my SIPs even after leaving India. After the first few years, looking at XIRR, I could sense and feel the importance of continuing SIP. ‘’Compounding’’ was slowly starting to show its effects on the MF portfolio. It is when the importance of having a sound process dawned on me

Phase 3 – Current phase – Trying to identify the process and believing less on ‘’intuition’’ (am I?)

I am currently in the midst of identifying the process (Portfolio and execution approach). ‘’Intuition’’ is still luring me – I have not ‘’rebalanced’’ my portfolio, Suprajit’s allocation still more than any robust process would allow. Sometimes I feel, ‘waiting to identify portfolio approach’ is just an excuse to satiate my cravings for the following intuition!

Phase 4 – Robust process and no intuition

Hopefully one day!

3 Likes

Hello,

Loved your posts.

What risk you may increase with intuition would probably be lowered by your honesty

I face the same problem, each time I think of enforcing a process, I recall the Lord whispering in my ears “You’re the chosen one”. Probably one of the toughest “soft” skill in investing is coming out of this illusion.

Cheers

5 Likes