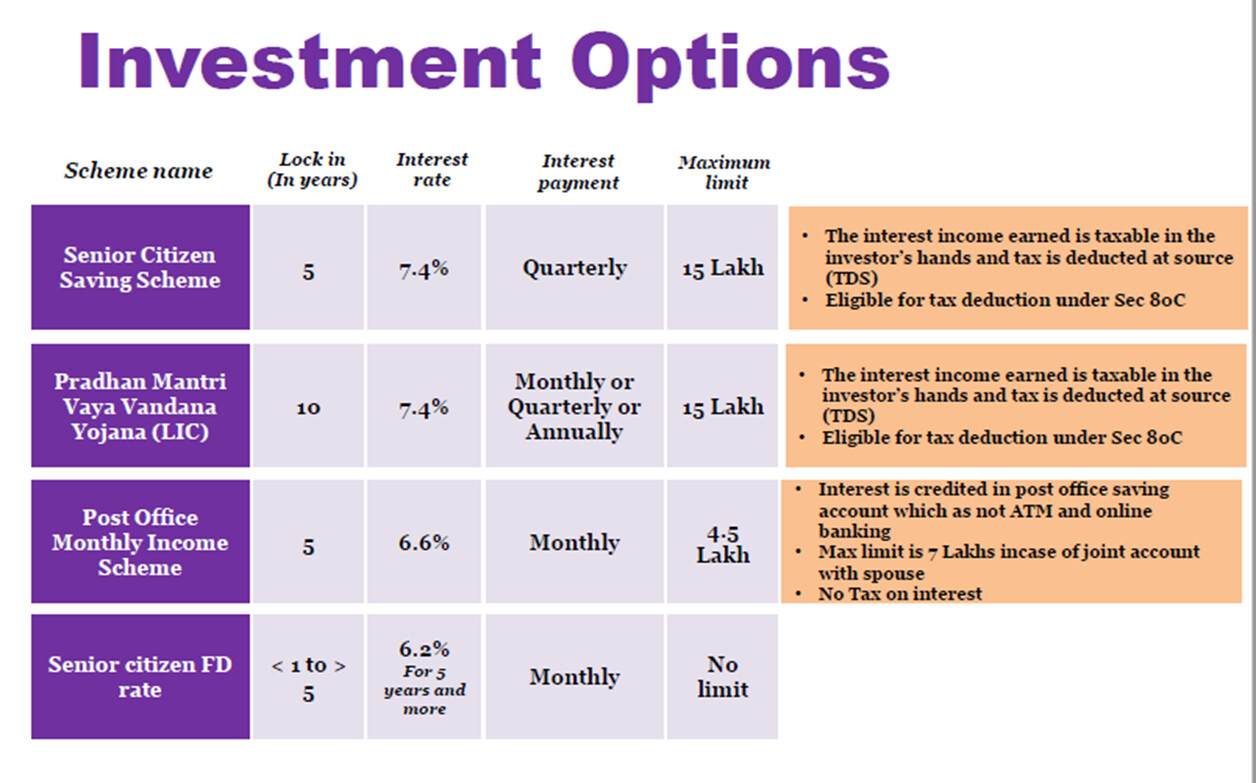

I am actively involved in the retirement planning discussion of closed relatives. One thing I realized is that, for a retiree who has never invested in Equity or for that matter any type of mutual fund, it is very difficult to convince (or may not be right to convince) to put more than 5-10% in MF/direct equity especially when corpus + pension is sufficient to manage with 7% kind of returns

Following are some of the options such investor can consider

These options only have interest rate risk. There is no interest rate lock-in and that is why yield can go down. Annuity products by Life Insurance companies offer products with Interest Rate lockin (offering 6.4% interest. Saral Pension) but discussion in which I was involved, people were not ready to lock in their money for long (which is true in case of Annuity)

This makes me wonder if Life insurance ex protection is a ‘Push’ product. There is a competition for each Life Insurance product except protection (Like Above table). Vis a Vis general insurance is a ‘pull’ product?

Foreign pharma companies fundamentally now do not.look that good. They are introducing their new products through their unlisted firms and using listed companies for marketing and sales which is not minority shareholder friendly.

Precisely that’s why protection is the true insurance…rest all are mixed products. Interest rate risk is significant over very long term so ( I am thinking loud), the benefit insurance annuity can give over such other gov schemes to the generation of early retirees is a fixed interest rate return over very long period of time…also an early retiree would not be eligible for most of gov sponsored products until he/she becomes a senior citizen…say those preferring to retire at 40 or even earlier to do something on their own with lesser income than their regular day job and want to have a small part of corpus in a fixed income for very long term … Thoughts welcome

I am from Insurance Industry. Contrary to popular belief," if one is from a specified industry, then he should invest in that industry", i am not in favour of investing in Insurance companies. Recent data shows that overall Indians put 6% of their assets into traditional Insuance savings products. We think that Life insurance companies are Insurance companies, but the fact is they are Savings companies, pseudo-banks for accepting regular deposits. Term Insurance products are important…but fact is that, people take term insurance under the impression of family protection…But 70% policies of Term Insurance get lapsed within 3 to 4 years. People lose motivation to invest in risk coverage products due to no maturity at the end of term. We talk a lot about low penetration of life insurance…but thats wrong. Real picture is, those who want to take policies, most of them have already taken policies. Accounting of Insurance firm is so tricky that a common person cannot fathom what is happening in Insurance company. LIC getting listed is Public sector with very big size, so rate of growth is not attractive. HDFC Life and ICICI pru, SBI life…even before not very good performance…I dont consider them as consistent compunders…Better to invest in such sectors, where you are more or less sure about Compounding over a long period. There is absolutely no moat in any General insurance company too …be it ICICI lombard etc…Considering the complexity and unsure growth of overall sector…better to stay away…

The IDFC Tax Advantage (ELSS) Fund is among the top five performers across time frames (6 month, 1 year, 3 year, 5 year and 7 year). What factors have led to this consistent outperformance?

The fund has always been consistent in its approach towards allocation across large, mid and small caps over the last 5 years even during the 2018-19 period when mid and small caps underperformed . This disciplined approach along with the fund’s positioning towards owning growth stocks at relatively attractive valuations has helped in generating alpha across longer time frames.

Axis long term equity – (Current XIRR since 2015 – 16.64%)

Some of your equity funds likeAxis Bluechip,Axis Midcap,Axis Long Term EquityandAxis Flexi Capunderperformed the category and benchmark in CY 2021 as value theme picked up. Do you envisage following a blend strategy or would stick to growth style in equity funds going ahead?

We believe that investment philosophy should be intrinsic to the funds that we are managing and cannot be changed based on different market environments – it will only cause confusion and make us miss out on the long-term trends . We believe that our approach has the best potential of capturing the long-term alpha from the Indian markets. That does not mean that it will not have years like 2021 when it can go out of favour. We remain committed to our long-term strategy.

The asymmetrical nature of equity tests patience like very few things in real life. First order of asymmetry is in the year wise returns itself and the second order asymmetry is different portfolios perform differently in those years.

The recent news on merger of HDFC and HDFC bank, goes well with the my original resaon of buying Kotak Bank. One of the key question I ask myself before buying stocks of any company is - If I have money to buy entire business, will I do that?

Whenever I ask this question incase of financials, I always think as a ‘‘Owner’’ of business; I will be comfortable buying a basket having strong distrubution muscle across the group. This is completely opposite to manufacturing - where I prefer ‘‘Focussed Aggression’’

Though I am year late, I will continue with my plan of buying HDFC bank

I admit that, price is impacting my psyche a lot… earlier i was thinking of starting with option 2 and then switching to 3. But now I am strongly believing in option 2. Bhav baghvan che!

NPA cycle is clearly behind us, balance sheets are clean and the growth appetite for the lenders is back. The new credit cycle has just begun and the question is how should I position my portfolio to take advantage of the same.

One way is to go beyond top 4 banks & top 2 NBFCs where I am comfortable about underwriting skills and management to ride the upcycle. It needs skills and efforts to invest and remain invested in these opportunities without losing peace of mind. I am not confident about my skills to identify these opportunities which - I believe – can create tremendous wealth in upcoming credit up cycle.

The second way – which I thought is more appropriate for my taste – is increasing the allocation to lenders in the portfolio while sticking to the obvious names – likes of Kotaks, HDFCs, Bajaj Finservs and may be ICICI bank. With this background I am seriously contemplating to build around 25 – 30% allocation to financials from 20% planned earlier. The current plan is 8-9% Kotak, HDFC Bank and Bajaj Finserv each.

If you are thinking of Just Financials, then it makes sense to invest into Bajaj Finance instead of Bajaj Finserve. because Bajaj Finserve has Life insurance as well as general insurance business along with bajaj finance as embedded together. If Insurance is required then in general insurance ICICI lombard and in Life insurance HDFC life are more suitable candidates. But for pure financial play, Bajaj Finance is enough…Your views Please

I am sticking to this thought process which I know is not solid. Personally if someone gives me option to buy out entire compnay in India. I will still buy a diversified company rather than just insurance company. I am aware,this argument is weak and I can change it any time. Never the less thats my thought process at present

Portfolio Diversification – Phase 1 to be completed by this year end

Unless Suprajit or Ajanta pharma moves up sharply, I am on a track to complete phase 1 of my portfolio diversification by the end of this year (If they move up sharply then it’s a good problem to have). My effort is make portfolio more robust in every cycle compared to previous cycle. Last cycle portfolio was a joke, compared to that I have a more balanced portfolio in this cycle. The need for the sound and balanced portfolio will increase in each passing cycle as I am no more ‘millennial’ and have more personal financial commitments than ever. I don’t want to attach any ‘’number’’ to the diversification as I don’t believe lesser number of stock guarantee more returns. My effort will be to add well run companies from the new sectors to make diversification meaningful.

For the any new company in the ‘core’ portfolio – Invest, monitor what management has committed, wait till they execute. once they execute successfully – average up or down irrespective of price provided valuation are sensible

For the any new company in the ‘satellite’ portfolio –bring down return expectations, stick to obvious names so that you don’t lose sleep averaging down and can aim to earn ‘behaviour premium’ over earnings growth. At the same time you don’t mind averaging up as the growth runway is large

In my opinion, diversification within a company is not a good approach. If you are looking for diversification then better get it through diverse companies operating in different niche. Each company should be very focussed and pure play of that industry. if a company itself is diversified in too many businesses, its very difficult to remain focussed and allocate all resources to all segments of businesses in prudent manner. I would always prefer to invest in 20 different companies who are pure play in each 20 industries , rather than putting money into just one company which is operating in 20 different business segments. This not only gives you diversification across sectors and industries but also diversification across management Teams. You get 20 different management teams, running the show rather than just one. I hope , I m making sense here.

Thanks for your feedback. Financials have ‘problem of plenty’. I am continusously thinking what is the best way to create 30 - 35% allocation in finance from my investible universe. which is - HDFC, HDFC Bank, Kotak Bank, Bajaj Finance. Bajaj FInserv, HDFC Life, ICICI Lombard and may be ICICI bank. I can only invest in companies having underwriting track record, thats my limitation.

Second thought which I always have (right from the first post on this forum) is might as well put lumpsump in Axis Long term equity which has the good combination of Financials as below. But I am restricting myself to put only SIPs and step UP SIPs in mutual funds

One of the reason for the cautious stance in financials is the is because of the mental scarring in the last cycle. For those who were active on twitter in the last cycle ( i am a lurker and will always remain one ) , following was one of the legendary tweet by Samyukta Joshi which she posted at the peak of the cycle. People mocked her, laughed but then from nowhere IL&FS crisis happened and I had to rub my eyes in disbelief looking at the prices

Though I did not suffer loss, mental scarring was huge and I carry that baggage of it till today.

Therefore even we are at the beginning of the cycle (unlike in 2017), i am not comfortable going beyond tier 1 financials. This is something i would like to improve going forward where rather than carrying a baggage, be prudent and swift to optimise the returns