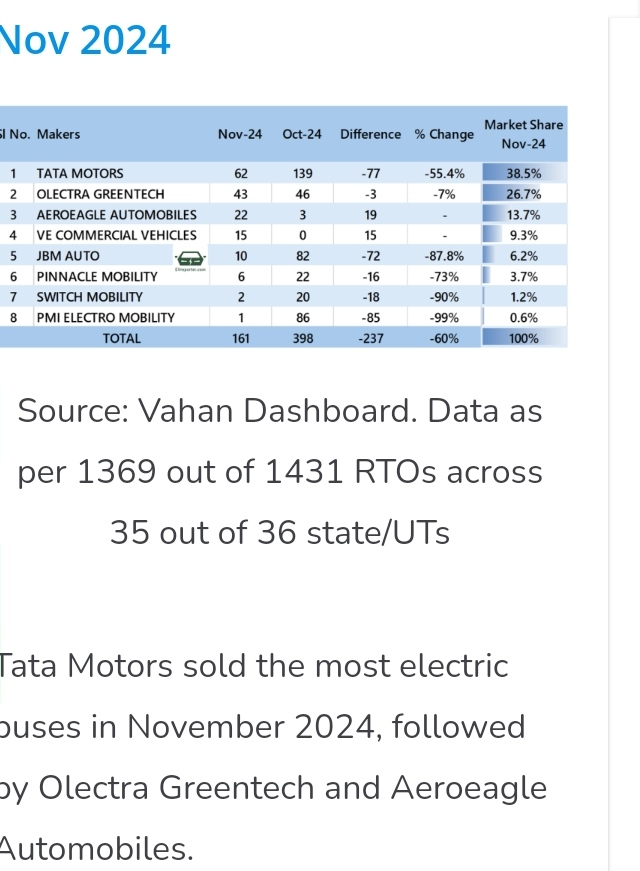

Nov vahan data is not encouraging/not reflecting any major change.

Detailed news.

Disc: reduced investment from 5% to 3% as I have doubts on execution and meeting the targets for H2

Nov vahan data is not encouraging/not reflecting any major change.

Detailed news.

Disc: reduced investment from 5% to 3% as I have doubts on execution and meeting the targets for H2

Vahan data doesn’t reflect the actual buses sold by the company, i don’t see any reason for less bus deliveries in Q3 as compared to Q2

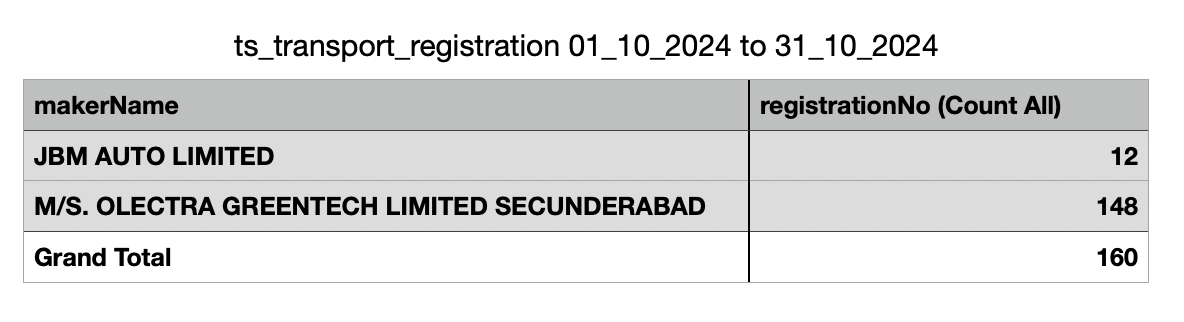

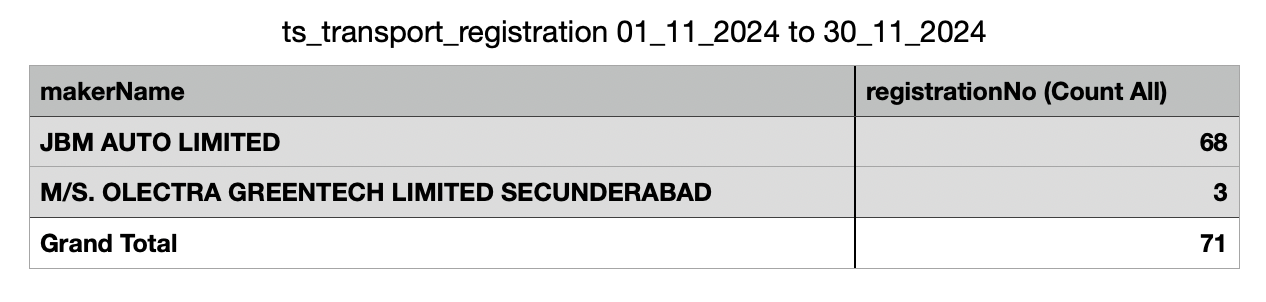

I know that Vahan doesn’t include TS (Telangana) data. So, I checked the Telangana state dataset (link), which shows that 148 buses were registered in October and 3 in November.

Thanks for sharing TS data, Its impressive number in October.

We can expect 450-500 number of buses sales in the Q3 at a rate of 150/Month, which should increase to 200/Month by Q4 end if things go as per the plan.

If you go through the previous concalls you can see that vahan data lags actual bus production as registration is done by state transport companies after receiving it through partner operations company. So TS data for October could be already convered in September,that is last quarter data.

There was serious security concern with Olectra greentech buses. There will be detailed enquiry on the recent Mumbai BEST bus accident soon. This can lead to many cancellation of the orders soon.

More Details:

Happy Investing,

Karthik

Disclosure: I am not having any exposure to this counter. I was tracking all the Electric bus sales and future growth prospect for EV industries.

The article you shared doesn’t say anything about Olectra’s fault in the accident. The driver was inexperienced with automatic transmission which might have caused him to lose control of the bus. Moreover, he seemed drunk.

Electric buses are the future. Drivers can’t dictate what they wish to drive. Either learn or allow newer generation drivers to take over.

I don’t see any threats to Olectra or its orders at all. I stay in Hyderabad and I see Olectra buses running around the city smoothly without any such incidents in the past.

Hi, this is not related to just “Olectra Greentech”, but for all electric buses and even for Indian Railways. This is for the betterment of our Nation.

In our country, a 12 Lakhs-15 Lakhs car can have advanced ADAS features and automatic braking systems. Teslas and Waymos of the world are soon going to make driverless cars in the next 5-10 years.

Then why can’t a state of the art electric bus which costs anywhere between 1.5 crores to 2.5 crores in India, have these features. Also why our trains which are for 100s of crores per set, don’t have these automatic braking or slowing features using cameras and lidar systems which can even see through dense fog. These features can help in avoiding so many unnecessary accidents.

Sometimes the sheer uncaring attitude of our companies and lack of innovation, upsets me. Specially if these features are widely available all over the world and are not something very tough to crack or implement.

Regards,

Amit Goyal.

Statistics on accidents from wet lease buses. Tata is doing better here

These may not matter. But if things are not very good in Mumbai, chances of general good opinion and repeat orders may get affected.

Good results, though topline slightly lower compared to Q2

Result link:

Insulator division contributed higher profit and topline compared to previous quarter and it is a silent revenue earner too.

As of now valuation cooled down to 85.4 PE, PB of 11.5 and market cap of 11,243 Cr. crores (down 15-17 % from previous quarter.

Delivery numbers: Number of buses delivered in Q3 is 282 (high value orders) and they are targetting to deliver 400+ buses in Q4 to achieve 1200+ numbers. Total delivered so far - 2440+ buses, highest in India. Thats 1/3rd of total of this year should come by this quarter. Current capacity is 200 buses per month, but optimisation is going to reach this optimum capacity.

Kms driven crossed 30 crore KMs from 28 crore KM. approx 5% of topline is AMC revenue and that will keep on growing based on KMs driven.

Other details - you can listen to conference call recording at https://olectra.com/wp-content/uploads/10029719.mp3

Disc: Invested about 2% of PF in Olectra and 1.8% in JBM. Both 6-7% higher than today’s closing price. Though EV plays less role, about 1.1% invested in Tata Motors at 10% higher than today’s close.

olectra_greentech_call_transcript_q3fy25pdf.pdf (194.2 KB)

generated the transcript of Olectra’s earnings call using our AI tooling at stockinsights.ai. Sharing it here in case anyone would like to read through.

I am quite disappointed with the Q3 execution, expecting a good number of buses delivery but its not happened.

Their slow Execution speed will affect the upcoming order also as they cannot deliver any buses of future orders before 2-3 years.

In this fast moving world nobody will wait for tthree years of delivery

Switch Mobility leading in supply of e buses last 2 months

Disc: Again back to 3% of portfolio each in Olectra and JBM by averaging down in recent downturn. Average buy price 15-18% higher than what it is now

As per current scenario Olectra may deliver similar number of buses like Q2 & Q3 and they may come with some other excuses in the con call for not meeting 200 buses / month target

It is turning to be hope investing. It would have been great if they release monthly data. I can see monthly data in Passenger Car segment, is it voluntary or by requirement? Why isn’t such data coming in for bus sales ?

Now only guess work. Current capacity supposed to be 400 buses per month. If current capacity rampup complete even by end of , 400 per month in March and 100 each in previous months, should bring the quarter production to 600 buses.

We may know only by mid to end of May when audited results of this quarter and year published. Any one attempted writing to management or investor relations ? Do they respond in this company?

I think it’s voluntary to share monthly sales data and not really a requirement.

for feb, olectra’s bus sales numbers are 66 (per vaahan) +10 (per TS data). don’t really get at what capacity they are operating currently or if there is any other blocker.