Usually I am a value investor. The first thing I look for is the stock’s PE and ROE/ROCE. This has also caused me to miss many momentum picks. For example the defence and the PSU rally has passed me by. The Railway PSUs have also failed to enthuse me.

As the FOMO becomes stronger, I have looked for a PSU which has good, if not excellent return on equity, and not sky-high PE.

I am learning, and my poser to the class is- have we ignored this hidden gem?

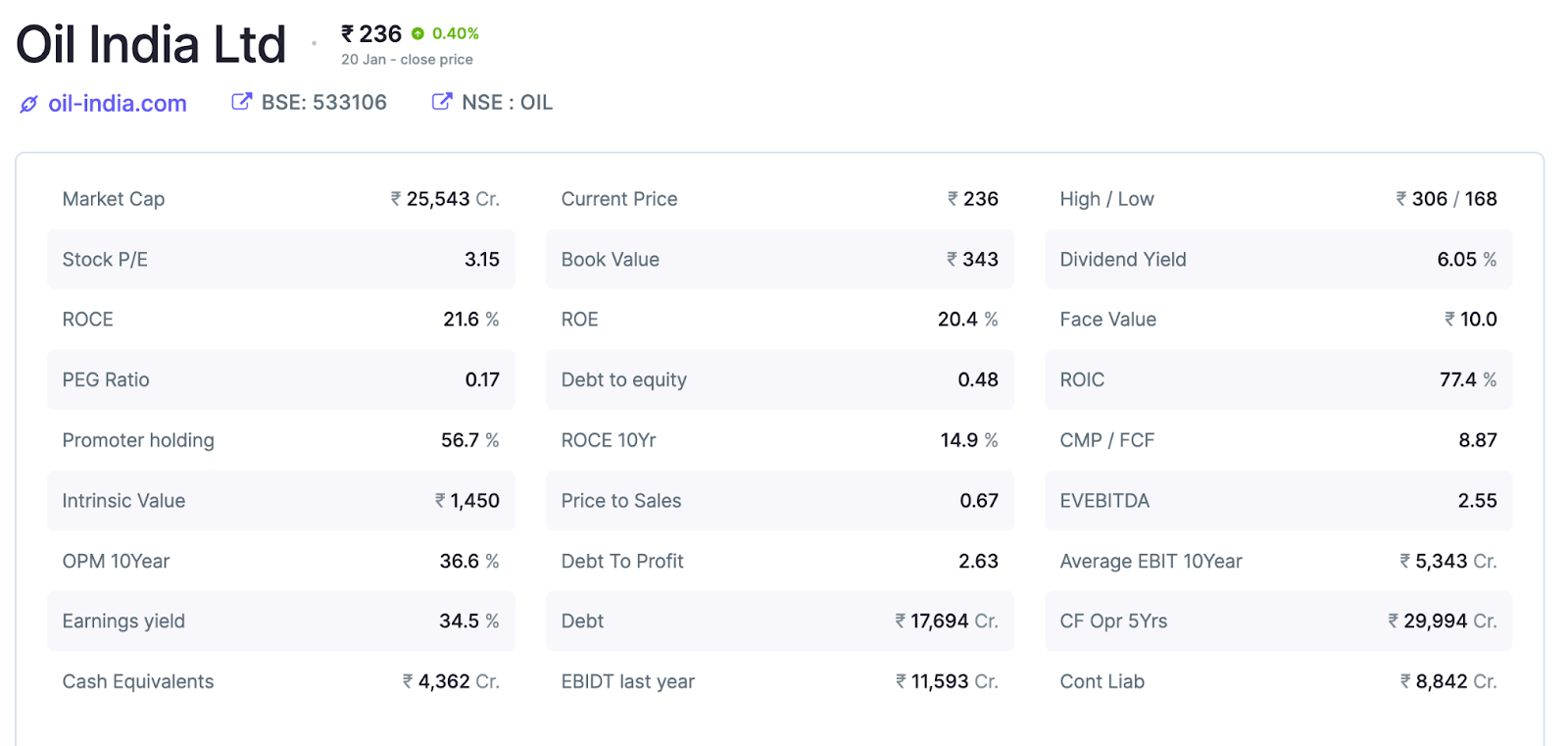

The basics first. The PSU has a Market Cap of ₹ 21,932 Cr. It is is engaged in exploration, development and production of crude oil and natural gas, transportation of crude oil and production of LPG. It also provides various E&P related services for oil blocks.

The sale of crude oil accounts for ~76% of revenues, followed by Natural Gas (18%), transportation (pipeline) (~3%) and others (3%).

The company owns stake in 60 blocks in India(https://www.bseindia.com/bseplus/AnnualReport/533106/66279533106.pdf#page=54) and 12 blocks in overseas countries like US, Nigeria, Venezuela, Russia, Bangladesh and others.(https://www.bseindia.com/bseplus/AnnualReport/533106/66279533106.pdf#page=58)

As on March 2020, the company has 2P (proven and probable) reserves of ~75 million metric tonnes (MMT) and ~60 billion cubic meters (BCM) of crude oil and natural gas respectively. Its overseas 2P reserves are ~25 MMT and ~22.5 BCM of crude oil and natural gas.

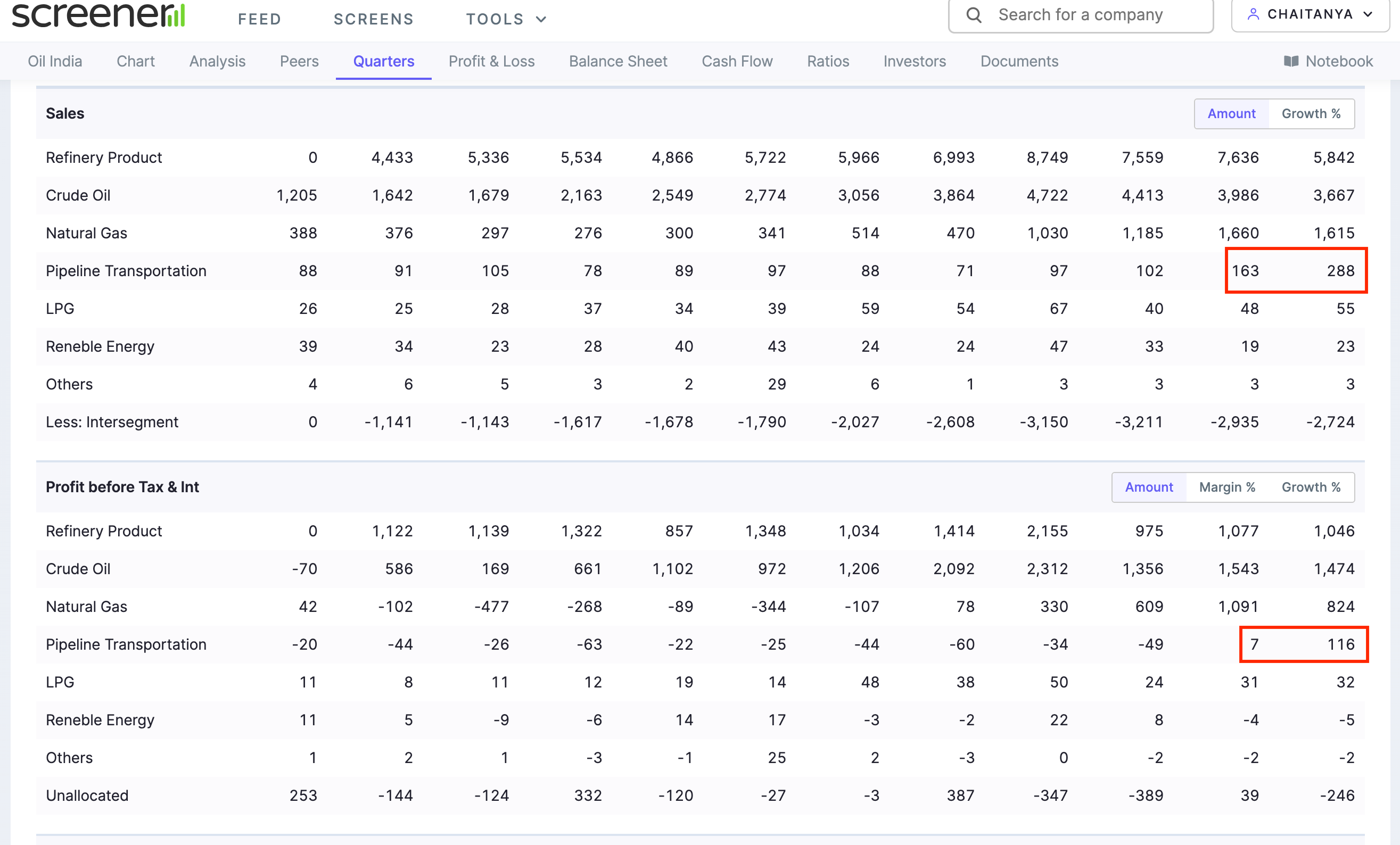

Reported Consolidated quarterly numbers for Oil India are:

Net Sales at Rs 8,258.72 crore in September 2022 are up 13.85% from Rs. 7,254.12 crore year to year.

Quarterly Net Profit at Rs. 1,896.19 crore in September 2022 up 64.65% from Rs. 1,151.63 crore in September 2021.

EBITDA stands at Rs. 3,043.39 crore in September 2022 up 22.7% from Rs. 2,480.42 crore in September 2021.

Oil India EPS has increased to Rs. 17.48 in September 2022 from Rs. 10.62 in September 2021.

OIL has also generated revenue of Rs. 131.67 crores in FY 2021-22 from its Renewable Energy Plants.

https://www.oil-india.com/Renewable-energy

As per the Company, the capex for the next year that is FY2023 is already locked out around Rs.4300 Crores. NRL, a subsidiary of Oil India, has on the extension project spent about Rs.3000 Crores, Rs.900 Crores in last financial year and current year up to December Rs.2100 Crores and this year the plan is to invest around Rs.3600 Crores that is another about Rs.1500 Crores will come in the Q4.

NRL total capex for this project for this refinery expansion is about Rs.28,000 Crores plus and for the target for current year cumulative target for the current year cumulative target is aroundRs.4500 Crores. Rs.900 Crores we have already spent last year. Rs.3600 Crores is the capex target for current year.

It has received a dividend of ₹242 cr from IOC, and from OIPL Rs.265 Crores. Dividend from NRL is Rs.265 Crores.

Risks

The reputation for sloth and inefficiency in the case of PSUs are the greatest risks in making an investment in PSUs. This could be one of the reasons for the investors in general not trusting the PSUs.

Secondly, the PSUs have no freedom to take commercial decisions. Recently, Govt by imposing the windfall tax on the oil companies. This resulted in the fall of their shares. Even withdrawal of such policies leaves the investors shaken as they fear that their well-thought investment decisions may come undone at the whim of the babudome. Similar thing had happened in the case of IRCTC also recently.

Why OIL India and why not ONGC

To me OIL appears to be more efficient in utilisation of the capital. ONGC’s PE at 4.67 is practically double that of OIL at 2.72. The ROCE of ONGC is 16.8%, which does not compare favourably with the ROCE of OIL at 21.6.

In any case, the story of ONGC is too well known. It is OIL which is crying for attention of investors.

Many well known brokers have recommended investment in this company.

JM Financial has recommended buying it with a target of ₹255.

HDFC Securities have a target of ₹255 too.

Prabhudas Liladhar has a target of ₹300.

Now the financials I always look for: the PE is 2.73. The ROE is 20.4%. Though not great, it compares favourably with many PSUs now being touted up. The ROCE is 21.6%.

Compounded Profit Growth

10 Years: 5%

5 Years: 18%

3 Years: 12%

TTM: 72%

The share is now submitted to the forum participants for a discussion.

Disclaimer: I have made a small investment today.

")

: Analyst Meet 2023")