Intrinsic value is determined based on projections of future cashflows and discount factors. For cyclical commodity stocks, such calculations are not reliable as future cash flow projects are based on commodity cycles. When oil prices crash the earnings of these companies can turn negative and vice-versa.

I also thing discount factors for Indian oil stocks tend to be quite high given government interference and nature of the industry itself.

So … Mohit/Others

I would like to believe below 3 elements that may have gone unnoticed six months ago are now in focus ? :

Dividends from IOC

Income from NRL refinery

Projects like India-Bangladesh pipe & Indradhanush pipe

Oil India cmp have doubled since June-23, currently hovering around Rs. 500 from Rs. 250. What could be propelling this sharp, one-way trajectory ? Do you think there’s more steam left?

Has oil india started working already on to green energy ?

I’d also wish to understand cyclic business of oil india and current phase of it, in case someone may enlight !

It is still cheap. Expensive or cheap is a comparative thing. Compared to the other PSUs, and many private companies it’s earning is not really discounted. I have made some investment in this, Chennai Petro and IOL.

All three have risen substantially but to me still there is a lot of value left in these. Specially Chennai has impressive ROE & ROCE.

I am also hoping those who missed the bus in the Railways are going to make a beeline for these.

Meek !

The line seem to be growing already or it has grown ? how far you think it may grow ?

I continue to study and try to get answers on Oil India’s gas distribution, green energy and pipe business but cmp,to me, is moving too quickly.Even before any additional news comes up let alone results or even a concall or management commentary…While i am enjoying ride but its baffling !

The way the market moves, and I am new to these things, it seems it ‘discovers’ a sector, and then moves from top to bottom companies. Within the sectors too, it searches for sub-sectors.

So, within the PSU rally, first it discovered Railways, Banks, Power, and Defence. Not necessarily in the same order. And many of them were really cheap. But to me now, the markets have a tendency of going bonkers. IRFC going 4 or more times in six months. SJVN jumping from 40 to 146 in the same time, to cite just a few examples, showed this discovery. The madess is also reflected in BHEL, ROCE: 3.33 % and ROE: 1.70 %, being market’s darling.

I have tried to discover sane areas within the market’s frenzy, and here the Oil PSUs fit in. Chennai Petro is still at 4.8 PE. ROCE is 45.5% and ROE is 77.9 %.

In the case of OIL, P/E is 9.14. ROCE is 25.4%, ROE is 25.2 %.

PE of RVNL is already 38.6. P/E of IRFC is 34.6.

So, clearly, now the Railway PSUs are expensive, though today again there is a move in the RVNL etc. The Oil PSUs, and I have mentioned only two, are clearly cheap. There are many negative factors, like regulation, in the case of PSUs, but to me they appear cheaper despite these factors.

Green hydrogen, net zero, EV, AI, biofuels, renewables are themes that are fancied by investors. Many companies in small to very small market caps have seen their stocks getting crazy valuations just by being associated with such themes (regardless of fundamentals) due to several factors such as low liquidity, operator action etc

However for a large caps like Oil India such announcements don’t really mean much. Green hydrogen as a technology is in a very early stage with mass-scale economics yet to be proven.

We had L&T coming up with similar announcement last year which didn’t really excite market much. Stock did well purely because of excellent business performances in last few quarters.

So in the short-mid run Oil India’s stock will only react to commodity market trends and company’s performance in their core business, in my view.

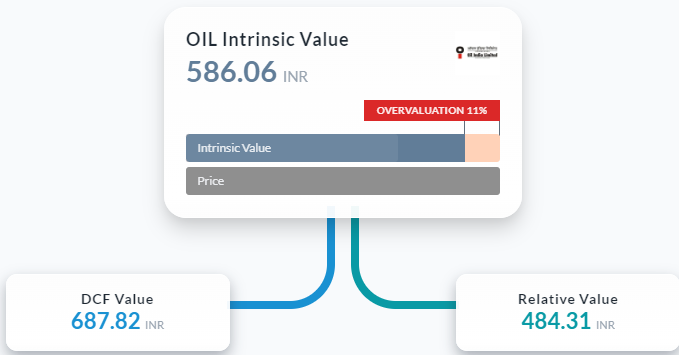

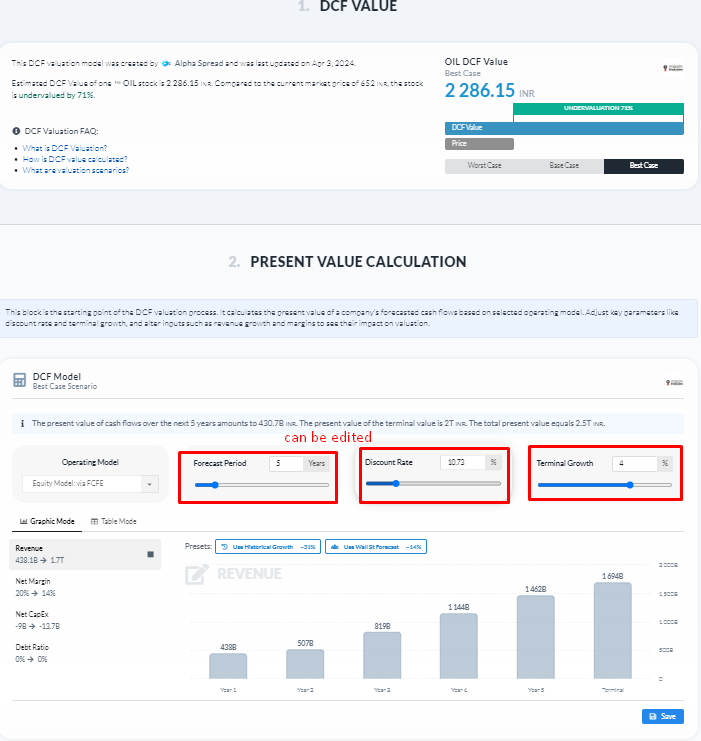

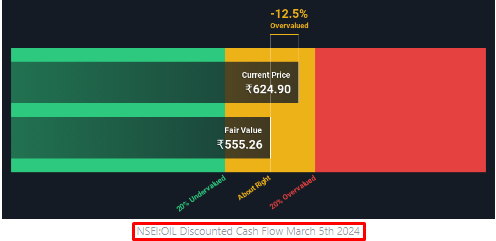

While oil CMP is hovering around Rs.650-660 which is higher than above calulated numbers, question - are the fair value calculations right ?..which one is right valuation of oil ?

At same time oil continues to exhibit strong up trend…question how far it can go ?

Oil exploration is the traditional business of OIL

and currently oil business does not carry a P/E more than 5-6.

Why Oil India is trading higher is for its Green portfolio - Renewables energy including BCG from bamboo , Hydrogen from coal , carbon capture , Green hydrogen etc aggressively.

Even Indian oil is aggressively in to renewables as above.

Both twin going forward should do well.

Indian oil is yet to capture market fancy because of its OMC cap and market is yet to value IOCL for its Green energy foray in a big way.

Discl: invested in both from.lower level. not a buy or sell recommendation. pl do your own assessment before investing

You can only apply DCF to the companies where you can forecast earnings with a certain degree of confidence and it’s very hard to do that for commodity stocks especially for oil companies. Simply Wall Street applies DCF and adjusts discounting factors based on the nature of the industry. It’s purely mathematical and doesn’t consider any sector or company specific dynamic.

When it comes to valuing commodity stock, I generally use my own metric which is average oil prices/average P/E in a particular year and compare that with historical trend. Based on that I find both ONGC and OIL to be quite expensive.

I work in oil and gas sector and have seen negative oil prices (during Covid) and some crazy up moves that can create extreme swings in earnings. Structurally, oil demand is forecast to remain flattish as per various estimates (IEA, OPEC) due to increasing EV penetration. I have also consulted with both OIL and ONGC and can tell you that they are not among the best managed companies and their operational metrics (e.g. cost/barrel, reserves replacement etc) badly lag the industry leaders.

So stocks like Oil or ONGC can be good short term trades as short term spikes in oil prices and current bull market are creating a demand for these counters.

Would like to see their reserves replacement metric. In any oilfield it’s easier to increase production by drilling more wells or doing lots of workover. Although that might give a short term boost to production performance, it’s not a long term answer to natural production decline which is natural for every reservoir. A company needs to continuously build its reserves through exploration or M&A or both.

ONGC by the way, a couple of decades ago, adopted similar strategy of drilling lots of wells (under pressure from government to increase production) in Bombay High field and that did a grave damage to the reservoirs impacting long term recovery.

It is a well known fact that we don’t have adequate oil Gas reserves in India. so exploration and digging may be often seen as a waste. it is like squeezing a dry towel to get water…Even oil Gas reserves in Middle East is not going to last longer- to get exhausted by 2050.

So, these 70 years old Navaratna PSU’s like ONGC & Oil India are not going to close down their shutters overnight. NTPC & Coal India are not going to close down its shutters just because coal is producing heavy carbons.

These companies are heavily investing in to renewable sources of energy in all possible forms , Solar, Wind, Syn Gas through coal gasification route , Carbon capture and a series of chemicals of utility from syn gas. And other renewables such as CBG, LBG, Green hydrogen , Green Ammonia etc to name a few.

Our Govt is going to encourage energy transition in all possible ways irrespective of any political power at centre with the objective of avoiding crude imports which currently stands at 85% of our energy requirements. Price volatility in crude is a permanent issue due to various reasons and that too crude is not going to be there for long… So energy security is something which any govt will encourage.

So if I buy in to oil india , ONGC , NTPC, Coal India …it is not for its business of fossil fuels …I am looking in to these companies from a 5-10 years perspective for the energy transition which have already started and these are the govt backed PSU"s those have financial muscle power to spend heavy capex and benefit from energy transition.

The exploration and production or coal businesses are very profitable at normal commodity prices. Also these businesses tend to have high entry barriers. You need lots of capital, highly qualified talent and access to mineral reserves which are typically owned by state companies in India.

But renewable is going to be a different ballgame. With Tata, Adani, Ambani, JSW etc getting into this space, going will be very tough for PSUs who don’t have the required execution skill, talent and culture to compete. Unlike Oil and Coal businesses where PSUs have had some entrenched advantages and also head start, in renewable, they will be starting from scratch and learning these businesses afresh without any real advantage of access to reserves.

Plus oil and coal commodities may not see the same demand but they will still be produced for next 50-60 years according to even most anti-fossil fuel forecasts. Which will make it even more difficult for companies like ONGC and CIL (especially the latter) to transition into renewable as they will have to get extremely efficient with their capital allocation and execution (and most of the PSUs are very bad at both).

We have already seen that with BP’s and Shell’s of the world, who after tall proclamations of getting out of fossil fuel business, have tempered their excitement and are now refocusing on their cash cow oil businesses. And these are world class companies, far superior to ONGC or OIL in terms of their capital allocation, technological knowhow and execution quality.

Bottom line, energy transition for sure is a reality but I don’t think winners in that space will be from PSU pack. I would bet on Adani, Tata or Ambani to make money for their investors. ONGC, NTPC, OIL will survive for sure, but not sure if they will thrive.

P.S.- By the way world is not going to run out of oil and gas reserves in next 50 years or even 100 years, especially the Middle East. There are plenty of reserves and yet more to be discovered. On the contrary experts are claiming a stranded oil scenario where world is going to leave a lot of oil and gas in the ground with transition to cleaner energy.

I also own Reliance , Adani , JSW , L&T., Tata …

over last two years , it has gone no where …not to my expectation…and stocks trade expensive.

…almost zero to minuscule dividend

Where as my PSU basket has given me 2x -3x returns apart from handsome dividend yield as passive income during the same period. Am happy with that.

It has played out well and I have got back much more than what I actually invested in PSU’s. And if I see , the renewable basket of PSU’s are increasing day by day and the pvt sector is lagging behind in renewable capex and all Pvt players be it Reliance or Adani are heavily debt ridden.They don’t distribute a single pie to investors in terms of dividend …look at adani stocks.

Today’s PSU’s are different than the PSU’s of past. Modi Govt is doing a lot of things to improve PSU profitability, divestment, atma nirbhar Bharat , heavy capex and so on. These are all zero debt companies.

While , so far so good , i still believe that the PSU will continue to do well considering the mouth watering valuation at which these are trading and handsome dividend yield they are offering. The only condition is policy continuance of Govt…The current Govt is monitoring PSU performance and even planning to hire CEO’s from Pvt sector where er required.

Regarding the Oil Gas reserves of the world that would last … you may please refer link below and there are many forecast 2050-2060.

Well, I am based in the middle east and consult oil and gas companies globally (have been in this industry for last 25 years) so I was giving you a first hand opinion about state of affairs but yes I am not that smart to contest some of these forecasts.

I dread what’s going to happen if oil runs out in 50 years. People who understand this industry through websites don’t know that oil and gas don’t just run our cars or planes or plants. 70-80% of the items we use or consume in our day-to-day lives have some oil and gas linkages. So I really hope our scientists find some substitutes for the sake of our kids.

Anyway, coming to main topic, not sure if I agree that Tata Power, Adani Group energy companies, RIL and L&T stocks have gone nowhere. On a 5 year basis they are all 2-10x (better than any energy PSU stock). Valuation wise even PSUs are not cheap anymore an they are all trading far above their historical multiples.

But may be you are right and may be this time PSU companies have turned the corner. Narrative looks very promising (although I have lived long enough to hear the same many years ago only to be disappointed) so I sincerely wish all the best to investors who are betting big on them.

Ok…So i am trying my hands on a giving an opinion, Its a general opinion and may not help in identifying pick among PSU Vs PVT names ! i am not an expert and certainly new to equity investment.

My views depend on experiences with.

1.The solar installations as an owner at the establishment where i work.

2.Hydrogen story and ESG projects.

Back then in 2019 the solar space(let say renewables or Electric Auto) started to boil,come 2023 i saw solar EPC contractors order book growing10X and loads of startup trying their hands on electric Auto .Together they made scooters a reality and lot of EV sceptics accepted and drove scooters. Hydrogen story in 2023 is seeing governments(mostly germany & India, some others at an extent) push to usher into new energy+chemical era.

The point is true to the extent that The gases-oil derivatives-petrochemicals-polymers are building blocks to modern daily use items starting from chemicals to plastics to pharma for households and gases to oil derivatives to petro chemicals for industries.(i mean any industrial product we can touch or think. 90% of household or industrial inputs would come out having an oil byproduct).

But i think the world is working towards making oil chemicals without oil(some i know are methanol,ammonia,peroxide,olefins) from hydrogen. So basically if that renewable chemical things happen…I think the world will go on without oil. (Shell,bp,Total,adnoc,aramco,KOC,NIOC,QOC …etc. would not want anyone to think the same though)

Now, to the point.As Electricity is one of the major cost component for any manufacturing/processing industry hence as the solar electricity costs drops(today its 5.35 Rs./Kwh) they all will benefit. PSU have been actively installing solar/wind in past and now they are investing in hydrogen. PSU as per me have strength at Gas distribution/ Piped oil transportation over pvt players.Some PSU have gave 2X in just 2 year(for ex. OIL India)

I’d request @1957 for his view, if any, why PSU can still rise quicker then Tata,Adani,RIIL or L&T ?

Thanks Hemant & LarryWink for valuable inputs.

I do Respect your views.

Whether a stock is overvalued or undervalued is subjective- views vary - it is the way in which you look at it.

Adani green for example carries a 12 months trailing P/E of 185. Fully debt ridden with 8 debt to equity ratio. No cash balance is possible after servicing the debts for next 1 decade or so. But for every trade , there is a buyer and there is a seller. only time can say who makes money!

Similarly Energy PSU’s like Oil India and ONGC trades at a P/ E of 7 to 8 with a debt equity ratio of 0.5. So , i am comfortable to buy at this price , though it is trading a higher than its historical average P/ E of 3-4. But when I compare with PVt players , I find there is a further scope of re-rating in PSU with down ward risk remaining limited.

Yes, PSU’s past was not so good and I guess history remains as history.This govt is trying to do something to build the economy as we can see from the results…whether it is railway, defence , or energy basket - Govt’s heavy capex plans and under Atma Nirbhar Bharat theme. PSU’s seem to be showing a good turn around and so also Mr market has given s thumbs up … energy transition being planned all over the world in a big way and in India it is the cash rich PSU’s who are leading the charge.

Having said that , i would keenly watch the election results and policy continuance and take a further call on buy sell or add to positions… For now I am comfortable holding my positions, though I have pruned my % position to reduce overall portfolio holdings.

Regarding the views on crude …I agree … it has been the integral part of our daily life …primary source of energy , Pharma, petro chemicals , fertilisers and the uses are endless.

But when the world has decided to do away with it …substitutes are already there. For example Hydrogen from electrolysis of water by solar wind is not only the primary sources of feed stock for power plants , but it is going to be the primary source of energy for transport sector - Automobiles ,trains and aeroplanes.

Starting from hydrogen and with help of carbon , all chemicals can be manufactured- Hydrogen can be an input in processes to produce chemicals such as methanol, ammonia, ethanol hydrogen peroxide, hydrogen chloride, aniline, cyclohexane, TDI and oxo-alcohols.

And TDI (Toluene diisocyanate) is commonly used as a chemical intermediate in the production of polyurethane foams, elastomers, and coatings; paints; varnishes; wire enamels; sealants; adhesives; and binders. It is also used as a cross-linking agent in the manufacture of nylon polymers.

And starting from Ammonia , you can produce a series of fertilisers such as ures, DAP, Ammonium nitrate, Ammonium sulphate , SSP. etc.

I am sure science is working to make it possible to produce everything you need from Hydrogen. And I guess the science was always there …but now these are being rediscovered and pursued rigorously - the only target is to tacke climate change , reduce carbon foot print

And as per latest development , synthetic e diesel / e-fuel can be manufactured out of hydrogen.

All good points and depending on one’s investment time horizon and risk apatite, no one is right or wrong in the market.

As far as I’m concerned I generally don’t go as much by narrative or future speculation as the management pedigree, their ambition and execution skills. Most of the PSU’s tend to have none. Their CEOs and top leaders rotate every 3-4 years and merit is not always the first criterion in their selection. They will only get as ambitious as government allows them to and having worked in a PSU like ONGC at the start of my career I know they are miles behind the private players like Reliance in execution.

And that will never change regardless of whichever government comes into power. And since government actions (OFS, price regulations, dividend increase etc) are always an overhang for PSUs, their multiples will always be lower than their private counterparts.

As PSU stocks have done very well in last 2 years, many investors who got into market in 2022 and invested in PSUs have reason to feel good about them. Recent price action has more or less closed the valuation gap and from here on any further price action will now be driven by earnings.