On your last point, agree its an important one, but we don’t know how accurate it is. I remember in one of the concalls, they had mentioned that with some they have a fixed-pay method, with some its a variable one. Its possible that if volumes increase with fixed-pay one, we might see a fall in this %. I am not sure I can read a lot into the numbers changing for this metric, though it helps get some idea on how things are progressing.

Dont have the answers but it looks like this discussion on NPST on valuepickr has caused the stock to correct from Rs 3500 to Rs 2400.

1 Like

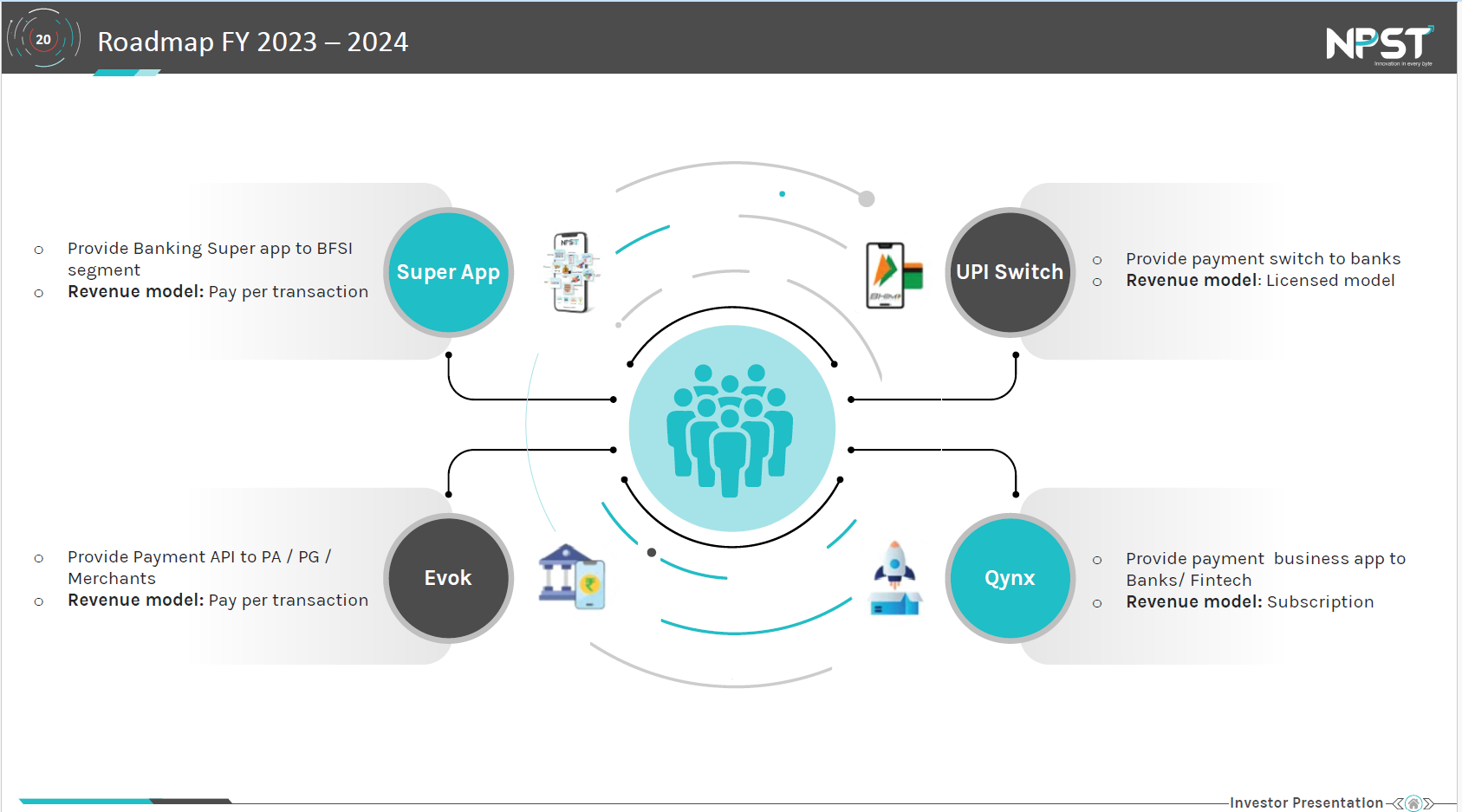

Can you post the snippet from the call please, which qtr? Even as of Q324, this is what their presentations carried and my understanding is evok has only pay per transaction.

1 Like

See the video from 20:00

he says the same thing, right ?

In evok, it’s purely pay per transaction.

In TSP there is combo of both, but for this discussion now, we can ignore TSP.

2 Likes

I have 2 small queries:-

- NPST has products named payjoy and qynx(maybe more), which are already brandnames of other companies. So would those companies allow NPST to use these names? AFAIK, NPST has no connection to those companies.

- Has NPST said something about distribution of its products like qynx sound box? I think they don’t have enough employees for that as of now. Similarly for other merchant solutions distribution, either they partner with some bank etc or maybe increase their staff. Are we aware of any such move?

I am new to this, so please be understanding if my questions sound stupid.

Edit : Also found that the TimePay app does not have very good reviews and infact the ranking on monthly UPI apps has been going down in recent months, from 29 to 34 currently. Volume and transaction value both are down. However, in itself it won’t probably lead to any difference in revenues(unless it charges platform fee like Phonepe).

2 Likes

2-3 points to note are -

- Small merchants are not ready for MDR and most likely MDR for P2M transactions will not get implemented in the near term.

- GoI pretty much wants to promote BHIM to break duopoly of Google Pay and Phone Pe.

No question was asked on government incentives. NPST call on Oct 21, PayTM on Oct 22 - hopefully some clarity will emerge.

7 Likes

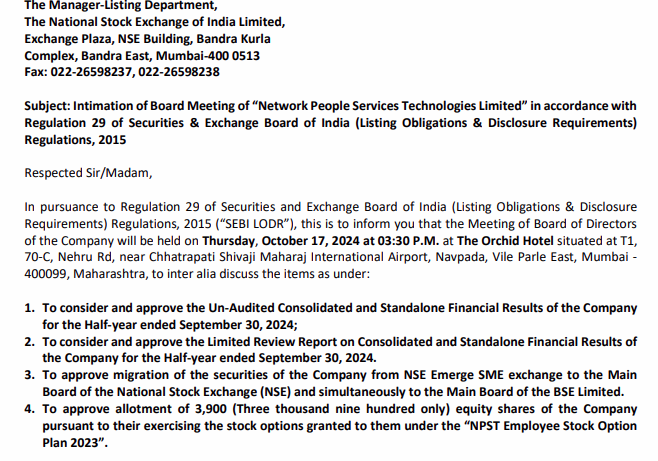

Likely to move to the NSE and BSE mainboard soon

1 Like

Plus, after October lot size being reduced. I understand that main board would happen sometime after that. Real price discovery would perhaps happen on main board.

1 Like

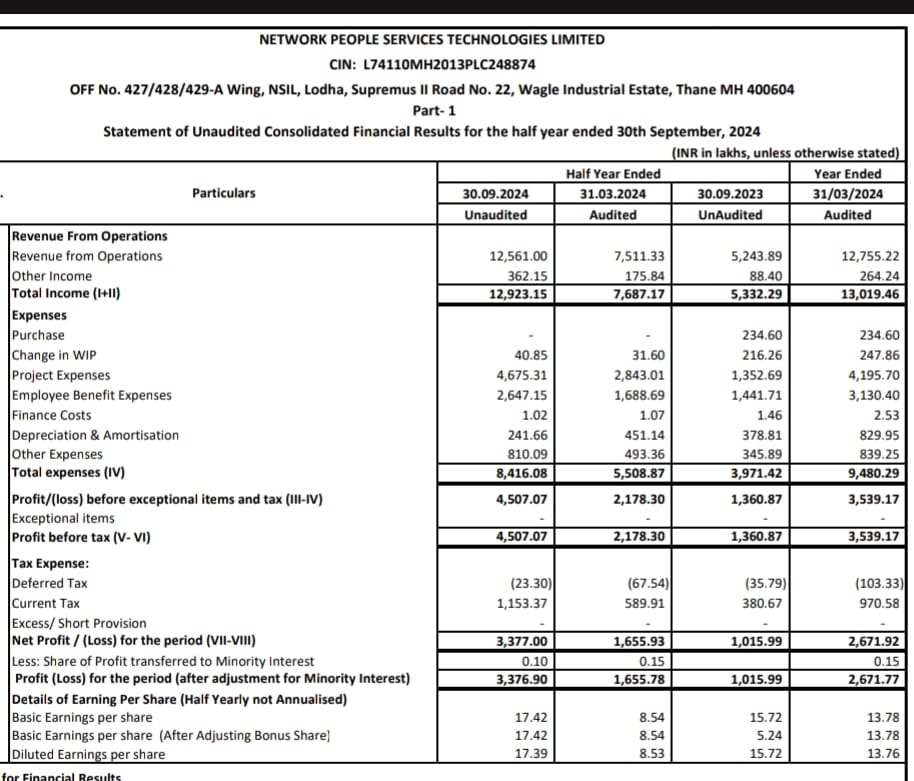

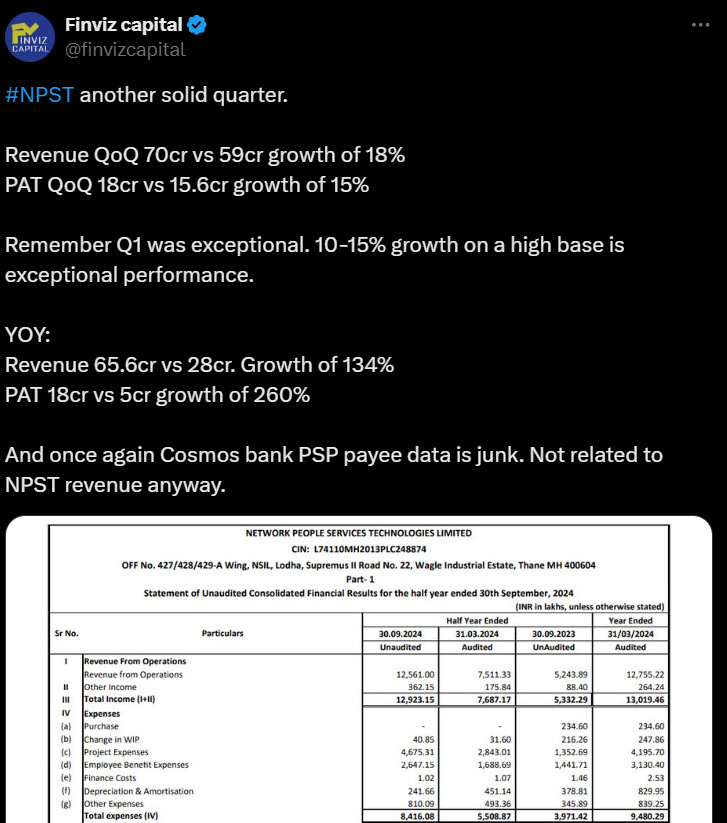

Mind blowing results. it’s saying our understanding of the link with cosmos Payee PSP nos. angle is perhaps not correct. Now, let the mgmt. explain the nuances in the call.

5 Likes

H1 EPS is 17.39 against Fy 24 full year EPS of 13.78 (adjusted for bonus) already 26% more and a full H2 to go…if they keep up with the 15% per qtr growth, we may see them with 44Cr profit in H2 or an EPS of 20

lets see whats in store as far as Management commentary on 21st Oct.

Cash too has doubled from 61 Cr in Mar 24 till Sep 24! Feeling good about the performance.

9 Likes

Did anyone attend the results concall today. If yes, any takeaways?

1 Like

joined the call. Didn’t get a chance to raise the 2 questions i had noted.

- My question is with regard to evok/ppas segment. Kindly explain in layman terms, how the revenue flows to NPST for this segment. Like who pays to NPST, and one level up the chain, who pays to the ‘payer to NPST’ and so on. This question comes from concerns around 2 topics. a. Govt. reducing incentives for digital payments ( are we a big beneficiary of that?) b. Reports around merchants not willing to pay MDR to for upi payments.

- My understanding so far is, the evok transaction volume are a subset of cosmos payee PSP nos. and mgmt. had also hinted the same in earlier calls. But we see that comsos payee PSP nos. as reported by NPCI website have seen a sharp decline in last 2 months. In fact cosmos has gone from being in Top 10 to out of Top 15 rankings in psp volumes. But as of Q225 we don’t see this impact evok nos. significantly. Has anything changed on ground which investors should worry about? How would you define the relation between cosmos payee PSP nos. vs evok transaction volume.

Call recording is already available on youtube. Apart from normal updates around product development, one significant update is, Mgmt spoke about on-boarding 2 more sponsor banks in addition to cosmos. Could this be already in action and hence we see the impact on cosmos nos. ?

1 Like

Inside NPCI: How Dilip Asbe, MD & CEO, NPCI built India’s most innovative fintech (youtube.com)

A recent interview…and way ahead for UPI …Interesting

2 Likes

• FY25 growth guidance 75-100%

• For FY26 will give guidance by March 2025. From the time we begin a year till the end, there are a lot of changes and a lot of opportunities we didn’t anticipate. Like, when I say interoperability in internet banking, that’s not something which was even there in our commitment or guidance in the beginning of the year when I spoke to investors. But that has come right now. So it is only good to have the guidance coming in at the right time.

5 Likes

After the earnings call and all the updates the company is doing great in a sense. But is this PE justified.

For a small cap even is the PE of 200 how is this justified.

What is the future growth after this if am buying this stock now even for 2-3 years.

What is the price appreciation that will take place, or will it consolidate for the earnings to catch up. The company is great and all but just the valuation and timing to enter a company is not as good in my view. I mean 200 PE, where is the PE going to go after this point

To view this in StockEdge, click StockEdge - Analyse Stocks in Indian Markets NSE and BSE

1 Like

The idea is that it will grow for 100% yoy for a few years as it is a small and innovative company in a very big and fast expanding market. Current PE is 120 based on TTM, but forward PE based on latest results would be 75 and factoring in the growth of next 2 years, it could be maybe 15-20. Some could say 2 years growth is factored in, others could say 5-6 years of 100% yoy growth is left before it comes to 50-60% growth trajectory thus current PE is actually low. You are basically betting on the capacity of the management to manifest their words.

13 Likes

I think we are underestimating features like shadow ledger. This kind of features actually make the product valuable on whole another level.

2 Likes

can you please elaborate this a bit … will be helpful to gain some more perspectives on this company

1 Like