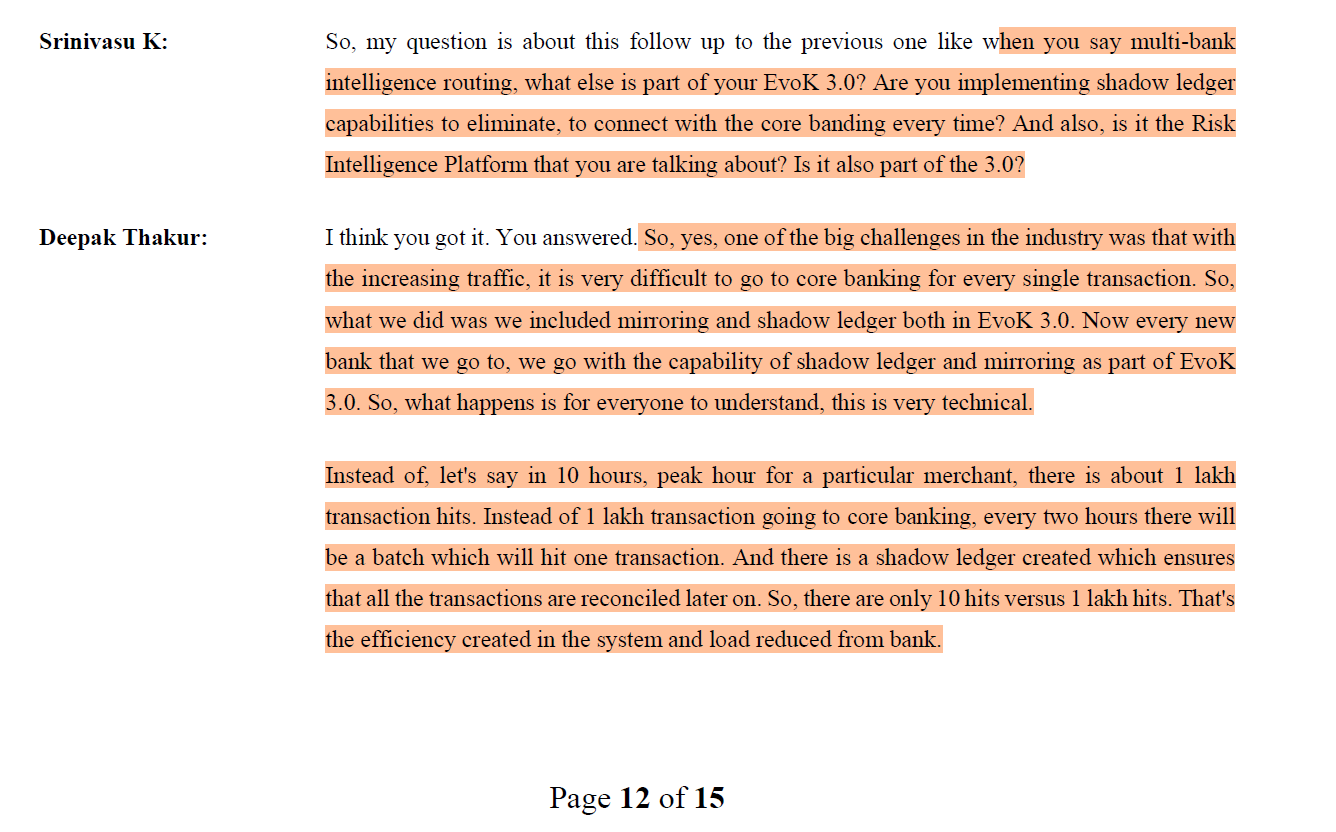

Mgmt. answered question related to shadow ledger in the last call.

3 Likes

Hey, I am a software engineer and I have worked in fintech and the scale these banks and npst are working at is no joke from engineering pov.

Example of shadow ledger:

Imagine a busy toll booth on a highway where thousands of vehicles pass through every hour.

- Without a shadow ledger, every vehicle passing through the toll booth needs to communicate with the central database (core banking system) to check its balance and deduct the toll fee in real-time. This process creates a lot of traffic (load) on the central system, especially during peak hours.(As for each transaction and database lock of some sort as to be made which reduces performance)

- With a shadow ledger, the toll booth keeps a local copy of account balances for all the vehicles expected to pass through that day. When a vehicle pays the toll, the booth deducts the fee locally and records the transaction.

Later, at regular intervals (e.g., every 2 hours), the booth sends a summary of all transactions to the central database to update the official records.

So instead of million hit to databse servers we can get away with a few hundred depending on the configurations.

With Rupay cards being pushed with ability of using upi this segment is going to increase volume as well over time plus overall upi load will increase.

Always throwing money at expensive servers is not an option. Smart solutions like these can actually be the MOAT of EVOK going forward.

Management seems to have very good handle on industry challenges and oppotunities.

I have written and thread on overall business but feel free to reach out if any specific product or technical details seems fuzzy.

Note: This link has just skimmings of the business and growth story

Disclaimer: Invested views may be biased.

8 Likes

A shadow ledger is only a technical detail, it does help NPST in handling the high traffic , but calling it a MOAT is far fetched. There’s nothing in it that any other competitor can’t implement (or maybe they have it already), and from a business point of view the value it provides would be minimal.

5 Likes

Maybe but I have not come across any competitors mentioning it(Based on competitors mentioned in concall).

It’s implementation is not straight forward with such stringent compliance norms and unacceptable downtimes in banking industry. A single batch failure can be catastrophic. One failed transaction is one thing but thousands not so easy.

As these transactions have to be compatible with forward and backward dependent systems. Often a nightmare to handle as third party systems don’t always act the same way one expects them to.

Simple example of refunds if the batch failure occurs or something goes wrong in bulk refunds then what? manual team verifies and processes each transaction?

Sounds easy in my perspective but implementation and then getting approvals is another story all together and ability to pull this on this scale is something else.

Also to have these kind of features the initial software architecture has to be very flexible and well thought out if not it often hinders make shift solutions hence acting as entry barrier.

Business impact not so sure how that would translate but yes definitely makes sales pitch much more effective.

A similar process is being used in upi lite.

3 Likes

the technical difficulties apply to any financial transaction, implemented by any IT company, so all other banks serviced by myriad of other IT service providers have handled these challenges already.

As for competitors mentioning it, there aren’t many in the listed space and even if there were, shadow ledger is not something worth mentioning.

NPST discussed this only because an analyst specifically asked this in his question.

If this was a competitive edge surely they would mention it themselves .

Mindgate for example handles the largest banks in the country, SBI, HDFC, Yes bank, to name a few and surely they’ll have something similar to handle the volume of traffic these banks command.

4 Likes

I come from IT background with 25+ years supporting FS clients. Shadow ledger definitely helps, but it is something that most if not all their competitors would be having. It definitely is not a MOAT.

3 Likes

Surely if mindgate has something better than that would be a great selling point for them.

These upgrades like from evok → evok 2.0 → evok 3.0 are expensive and require lot of effort on both ends. New integrations with banks also the same. Seeing the effort required its just becomes much more scrutinezed decision by the banks.

Now for all upi based systems going forward 2 challenges are there first good service in low bandwidth conditions and second handle the surge in traffic which is expected to grow a lot over upcoming decade.

Maybe right now shadow ledger is useless but if I were to choose a partner shadow ledger would seem really enticing to me. Of course if partners like if Mindgate offer similar solution then its a different story.

Evaluation paramters in decreasing importance according to me would be.

1 : Current basic requirements(All partners support them right now i guess) example Zero downtime, fault tollerence, backward compatibility and so on.

2: Future scalabilty → If I have shadow ledger and similar feature I can rest easy. Any vendor which cannot promise future scalability is easily out of race.

3: Good to haves

Again reiterating I do not have list of similar solutions to handle scale from different competitors. I have worked in fintech as a developer it’s a pain to even manage single transactions. Making these async or batched is nightmare and the ability to pull it off successfully in a highly regulated env is a feat in my view. That is why I am sceptical regarding availibility of such features with other players. This kind of feature on scale 7-8% of national upi traffic takes future insight and planning you cannot write some code or microservice to suddenly support it.

I view it as a great value add and would help them win lot of new banks and maybe help with better pricing power. But these are just my views here can be wrong.

2 Likes

I agree, I have worked as a Product Owner in Fintech sector for long and some of these features are amazing. Also, the management seems forward thinking and adapting to rapidly changing technology.

I don’t have much info about competitors so unable to share deeper insights and would request if anyone has insights on same to please share.

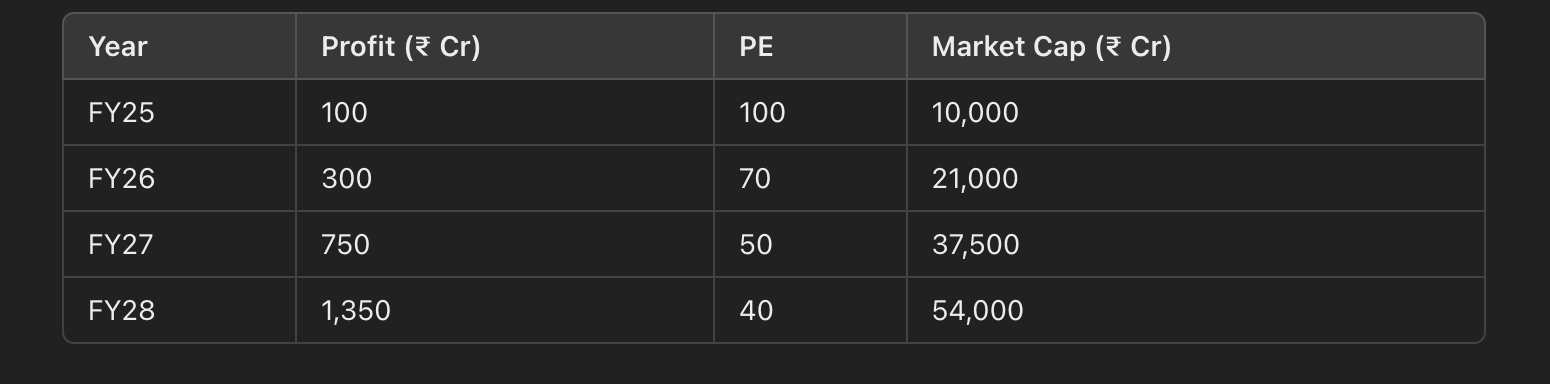

Here are some of calculations:

Current PE-114, Profit ( TTM) ( Sep '23 - Sep’24)–50 Crores, Market Cap-- 5700 Crores

FY’25( Projections based on Management Commentary)

Profit - 85 Crores, PE- 100, Market Cap—8500 Crores

FY’26 ( Projections based on Management Commentary)

Profit-- 150 Crores ( 80% growth over FY’25), PE- 70, Market Cap— 10,500 Crores

FY’27 ( Projections based on Management Commentary)

Profit — 240 Crores ( 60% growth over FY’26), PE- 60, Market Cap— 14,400 Crores

What are the flaws in this projection?

I feel considering industry tailwinds and strong management this is doable.

2 Likes

Trend has been to promise 100 and deliver 200 to 250% atleast for the last couple of years.

So i feel it will go like 100 percent for rest of h2 on base of h1, then 200% for fy 25 then 150 for fy26 and 80ish for fy 27.

Although it has to be taken with bucket full of salt. As upi is very sensitive to regulatory and Monetary policy changes. So it has to be perfect scenario for fy28 projections of 50k plus mkt cap company.

1 Like

NPCI international is in talks with 10 other countries for the UPI and Rupay stack after partnering with five other countries

3 Likes

Each to his own I guess, but I’m not comfortable picking a minor technical detail in NPST’s tech stack and calling it a MOAT. Blindly assuming that this well known technique has/can only been implemented by NPST is too much of a stretch to me.

Again , I’m not underplaying it’s usefulness, but it’s just not a MOAT for me.

2 Likes

This, to my mind is the MOAT for us investors IMHO. To have a management which knows their job, is aggressive, and also takes care of investors is a rare combo, that too in a small cap.

4 Likes

Agree, that is what is attracting me to this company. They are publishing quarterly results and doing con calls which is rare for a company on NSE Emerge. In fact I have noticed that many companies on main board don’t do concalls.

Disclaimer: Not invested but tracking closely

2 Likes

In matter of few quarters, whole industry may like to move to shadow ledger, if that’s the logical thing to do, to handle heavy traffic. These are the kind of things, a tech. player has to do to keep being relevant in the industry.

This is not something that will only be implemented by NPST. Safe to assume other players having much larger market share are equally capable and it’s matter of time everyone will do. I don’t see others switching to NPST just because they have implemented shadow ledger feature first. There may be 100 such nuances in the tech that we as outsiders may not be aware of. Surely not in the MOAT category IMHO.

5 Likes

Exactly. It is not easy to move entire system away from one vendor to another and companies won’t do it unless they have some legal requirement or some major issue/benefit in terms of cost and reliability. In industries requiring high reliability, they use very old tech too(like 30-40 years or even older) because they don’t like to fix what ain’t broken(pardon my Americanese).

Secondly, as Raj ji says others will likely come up wit it, by poaching talent from NPST if they have to. However, the moat is for existing customers, They are not going anywhere. Also, any new bank will seriously consider NPST given not much pricing difference.

On an unrelated note, I see they have become serious on their payment app. I have it and the number of offers and notifications has seen an increase in last 1-2 months. Maybe it is due to festive season, but I hope they are seriously focusing on this. This is where growth can come rather easily imho.

4 Likes

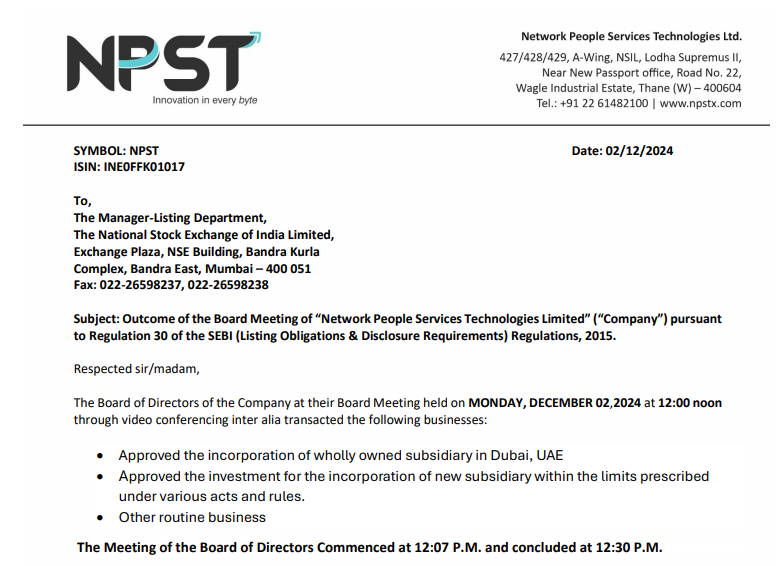

NPST has approved incorporation of a subsidiary in Dubai. If UPI goes global, NPST will have some part of the pie. Dubai(DIFC) is anyways a Financial Hub for MENA with an emerging fintech hive. So, NPST may offer other products to the banks and institutions there. It remains to be seen which specific opportunity pushed them to take the plunge at this particular moment.

12 Likes

I want to preface by stating that I only came across NPST recently and still trying to understand the business. After doing the usual research (call transcripts, annual reports, this thread, etc.), I am impressed by management quality, profit margins, return on capital (incl. those on retained earnings) and growth potential (including offshore expansion).

I do have some questions that I would appreciate if anyone can share any insights:

1. How many more Indian banks can NPST become a TSP? They have about 15 banks and management seems to be adding a couple every year. I understand that large banks already use some other providers (Mindgate, etc.) but does NPST have any chance to get one of the large banks as a potential customer in the future?

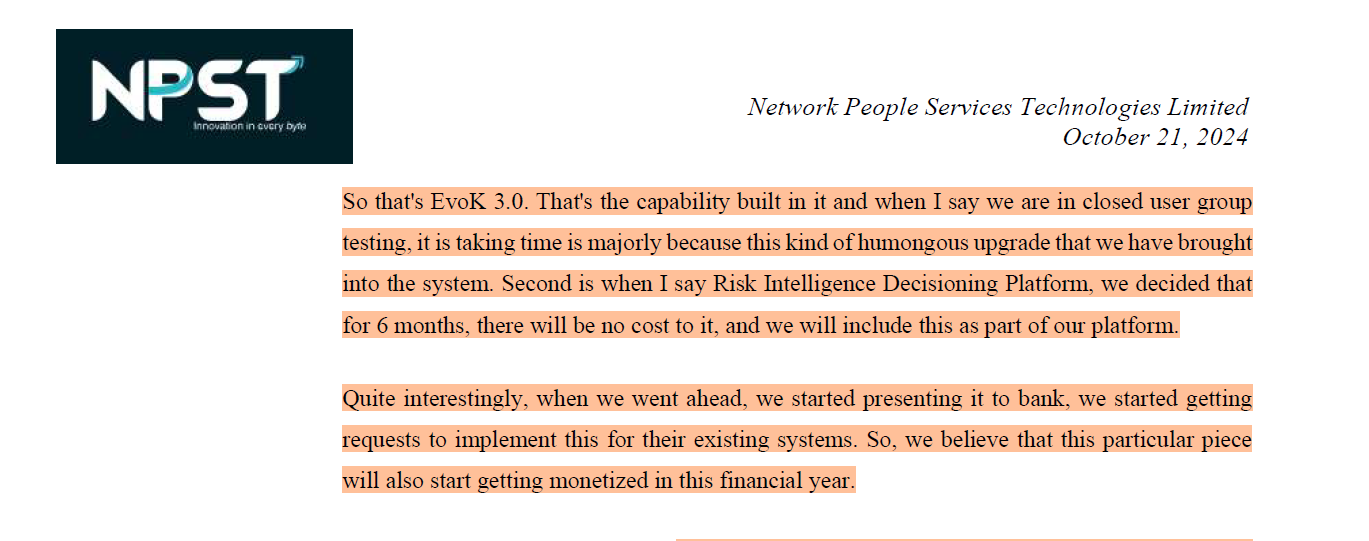

2. How long NPST’s lead in providing end-to-end UPI solutions last? I could be wrong, but it seems NPST’s competitors are catching-up. Here is the quote from the CEO from most recent earnings call – “When it comes to going back to your question, competitive edge, please understand that in last three years, we have evolved from being on the platform business. We have evolved from being purely a technology delivery company to also creating operational excellence and at the same time also building the compliance and the regulatory text that such companies require to operate in this space. So, while the other companies would be in a version wherein, they are still building the platform, we are actually building regulatory requirements, compliance requirements, operational excellency. All of those pieces are added to our stack right now. That is what is Evoke 3.0. So that’s the edge.”

3. How high are the switching costs for NPST’s core products (Evoke, Superapp, Qynx, UPI Switch)? In general switching software/technology providers is a costly business but this holds true more in certain industries than others. This may not be the best analogy, but is Evoke for merchants/ payment aggregators as good as say, what Bloomberg is to investment banks, hedge funds, etc. Also, what’s stopping one of their bank customers (TSP business) to do a tender at the end of the current contract?

4. What happens when a sponsor bank goes under? I understand that NPST needs a sponsor bank to connect to the UPI rail but what happens if the sponsor bank goes under? I suppose they would have some sort of Business Continuity plan where they would switch to one of the other banks but obviously not disclosed anywhere. Anyway, I am keen to understand what happens in those circumstances.

5. How much is their revenue per transaction in switch and merchant business? I couldn’t find this information, but I am interested if anyone has tried to work this out

4 Likes