Established in 2013 Network People Services Technologies Limited (NPST) is a Fintech Company focusing on Digital Payment Solutions like UPI, IMPS, Mobile Banking & Wallets to Banks and Payment Companies.

NPST is an authorised Merchant Payment Service Provider, approved by NPCI, providing payment solution to aggregators, merchants and users across various segments. NPST operate as “NPCI Approved Merchant PSP” digitizing Merchant acquiring space under the brand name of "TimePay”.

Currently, the company is providing its services under two verticals i.e. Technology Service Provider (TSP) and Third Party Payment Application Provider (TPAP).

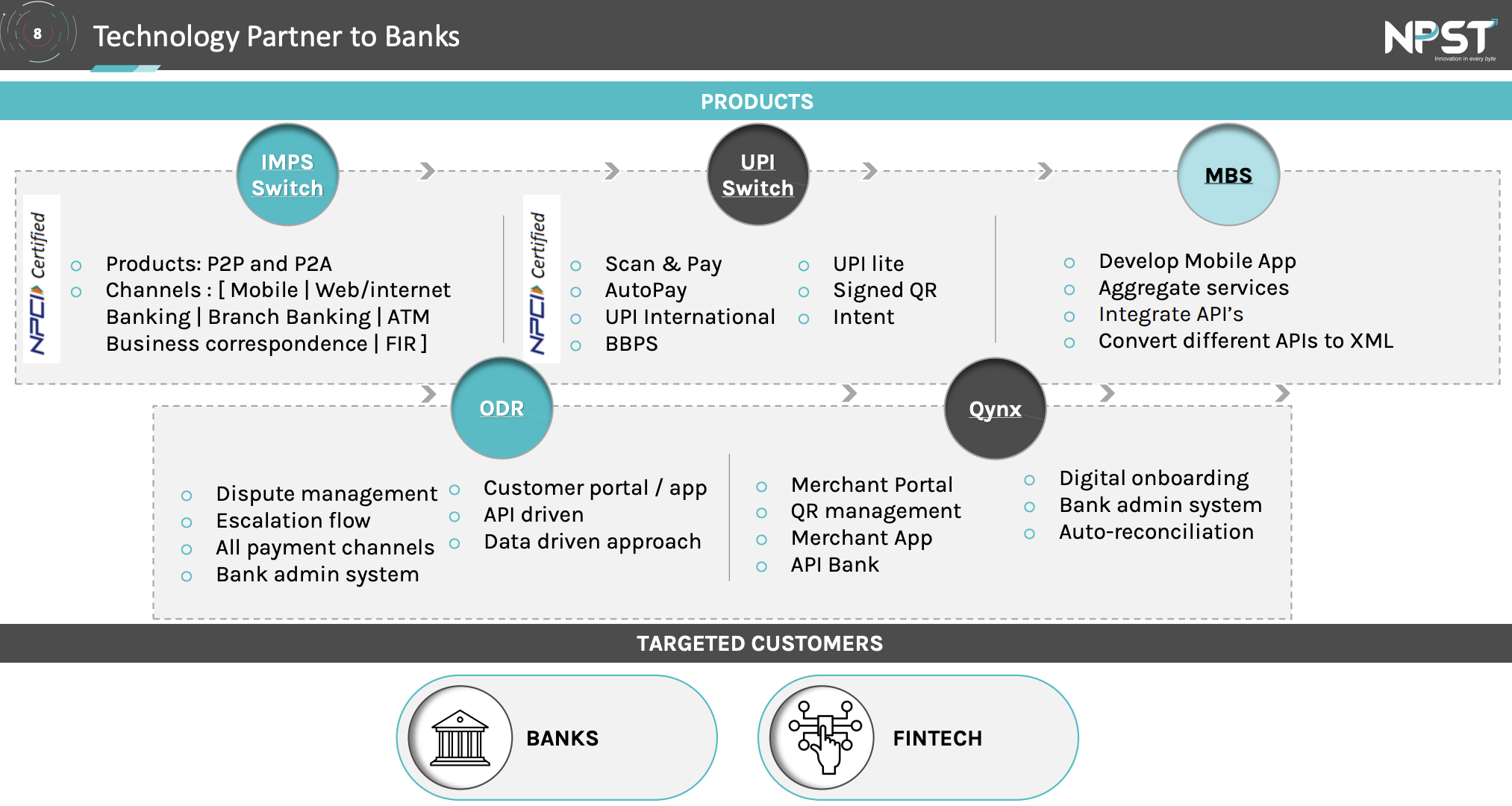

Technology Service Provider (TSP) (For Banks & Financial Institutes)

- Switch Products IMPS | UPI | Mobile Banking Solution (Revenue model: Licensed model)

- Super App – integrated Mobile App for Banking services (Revenue model: Pay per transaction)

- Qynx – Merchant switch (Revenue model: Subscription): Qynx is a Digital Merchant platform for banks that provides a complete suite of services and products to manage and operate Merchants of various sizes and categories. The solution provides an end-to-end product stack to digitise your merchant network and increase revenue potential through digital offerings. A must-have product for banks & fintech to create merchant stickiness to acquire new business.

- ODR

Third Party Payment Application provider (TPAP) (For Payment Aggregator and Merchants)

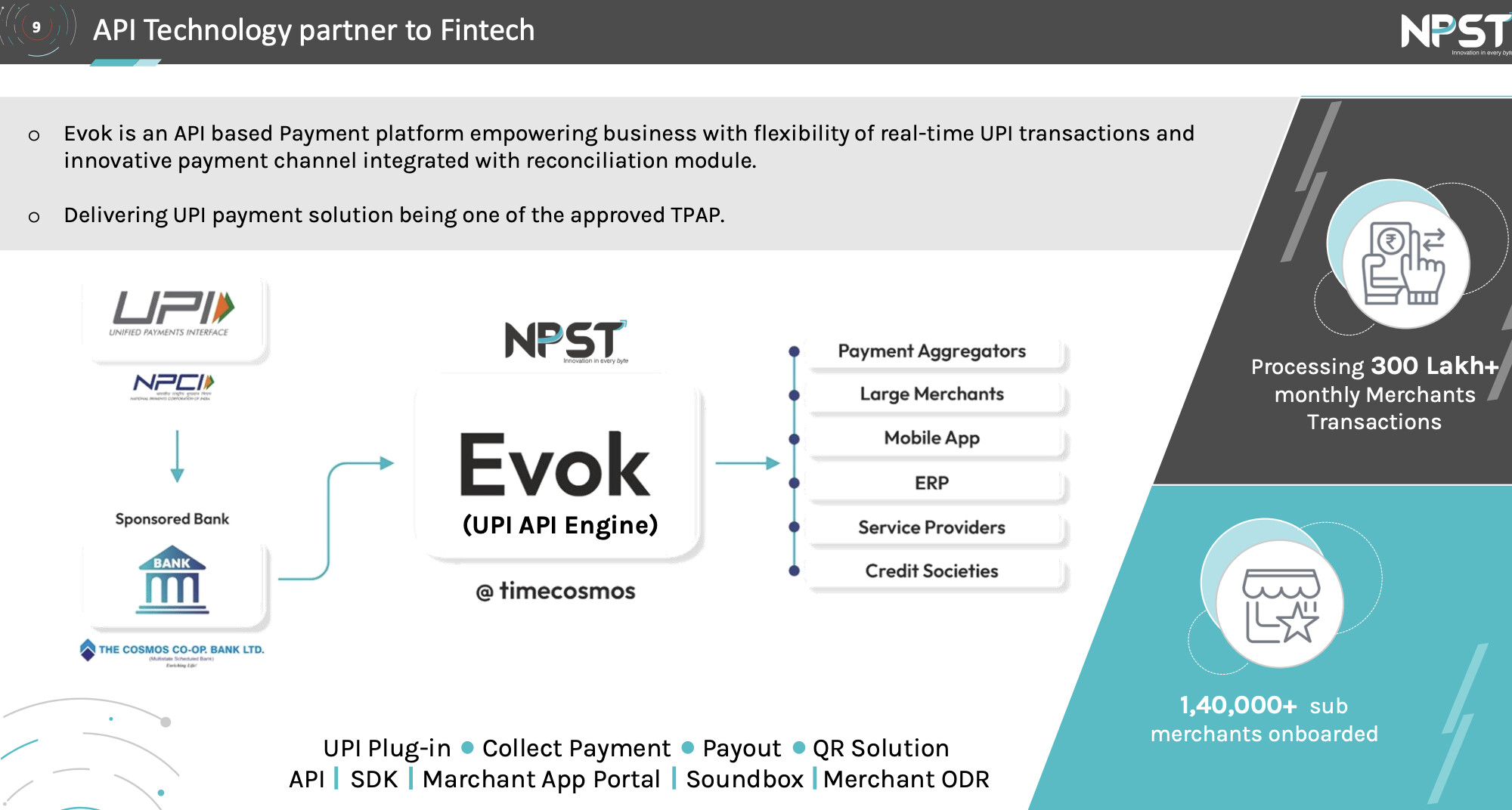

- EVOK - UPI (API) engine (Revenue model: Pay per transaction): TimePay Evok is an API based Payment platform empowering business with flexibility of real-time UPI transactions and innovative payment channel integrated with reconciliation module. Delivering UPI payment solution being one of the approved TPAP.

- UPI plug-in

- Payout solution

- Merchant ODR

Notes on Timepay app: this is actually called the payee business, where we give the APIs to our merchants or payment aggregators, where the sponsor bank is Cosmos. As part of this ecosystem, it is mandatory that we have a PSP application in the market. So, it was a mandate piece due to which we actually brought that application in market. We never promoted. We never pushed it, because our focus was always this API business, the merchant business.

API business (EVOK): when we give the API, we give it to payment aggregators and payment gateway on the bank platform. So, we play a technology API role in this particular segment. And those who are authorised to acquire merchants in market, or those who are merchants in market, those who need collection technology on UPI, or they need collection API, where they can collect funds for the services and the goods they sell in market. Or, re-sell those things, like payment aggregators and payment gateways.

So, these are the guys who take services from us. In order to do that, in order to manage the platform, right from the compliance, the reconsideration, the technology fees, the infrastructure, and the support system, the operations, there is a whole gamut of business that has to be built around it. And there is a cost around it. So, for that, we charge our payment aggregators and merchants on a SaaS model.

And I would say that those who are in merchant aggregation business, there are 30 odd accounts that we have in this particular segment, including something like PayG, EaseBuzz, or we are already in the final stage with Cashfree. So, these are the guys who would be using our services.

They have processed 4200 crore volume via their API in this quarter. It is only 0.1% of the total API business.

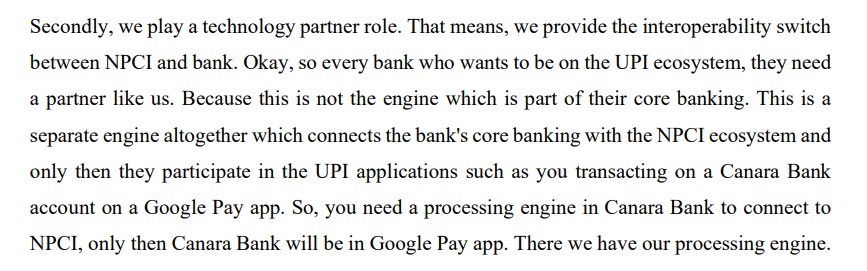

How NPST helps banks as TSP? We provide the interoperability switch between NPCI and bank. Okay, so every bank who wants to be on the UPI ecosystem, they need a partner like us. Because this is not the engine which is part of their core banking. This is a separate engine altogether which connects the bank’s core banking with the NPCI ecosystem and only then they participate in the UPI applications such as you transacting on a Canara Bank account on a Google Pay app. So, you need a processing engine in Canara Bank to connect to NPCI, only then Canara Bank will be in Google Pay app.

Revenue Split: Two third portion is from Evok business and one-third is from other business.

New area of growth:

- When we acquire new bank accounts for example in UPI Switch, so whenever we have a new business around UPI Switch that is where our contribution to this particular percentage you mentioned will increase so State Bank of Mauritius India Limited is one, one account around UPI Switch we have acquired.

- Qynx which is a merchant acquiring platform.

- If they can acquire e-commerce or gaming customers then their revenue may increase with API business.

Extra Notes:

- Launched 6 products in the Global Fintech Fest. Got a lot of inquiries. Going into POC stage with some customers.

- They got State Bank of Mauritius India Limited order in this quarter. It’s a big order that will have an impact across TSP as well as API business.

- Launched “Super App Canara ai1” with 100 Lakh+ User Base

- Processing 390 Lakh+ Daily UPI Transactions as TSP for Banks

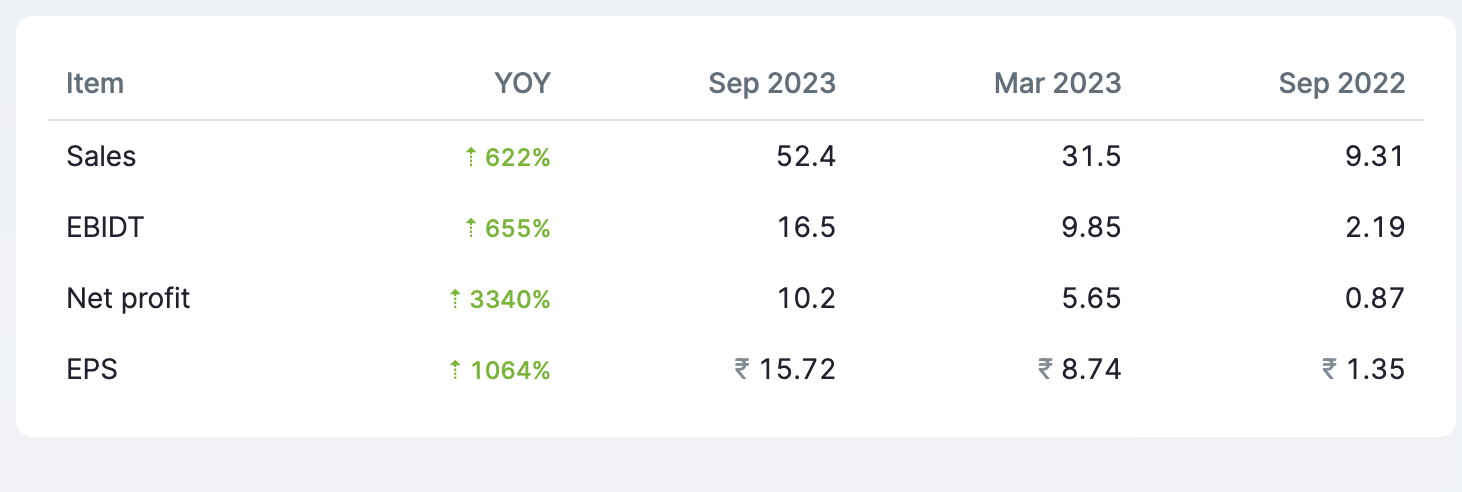

Results:

Risks:

- Business is a little complicated to understand.

- HDFC and SBI already have their partners. They control the real volumes in the market.

- Government banks might be the only probable customers for their super app business.

- Technology might become obsolete with time. NPCI keeps on introducing new tech.

- Overpriced at 85 PE.

Investment Rationale:

- Technology business growing with the UPI volumes.

- They have an aspiration to achieve the top five digital transaction volumes in India in the next 5 years.

- Currently they are handling 0.1% of the API volume. They have ample room for growth.

- Management has relevant industry experience.

It would be great if people from the industry could share more insights on this API business (EVOK). As far as I can understand this is an actual area of growth for them.

Disclosure: Not invested

Current Market Cap: 1300 cr.