Hello All,

Is there any news of UPI transactions to be charged below 2000 Rs which is causing selling pressure ? Any one having detailed idea about this and impact on NPST?

Its for card not on UPI. In fact if that happens it will be beneficial and more push for UPI.

BTW, the GST is on merchant charges which is 1% to 2% (might be slight more which I am unaware) of transaction value. So GST will be on that 1%-2% of charges. Not on transaction value which seems to be confusion going on.

it is for credit card and not on UPI. I think it is consolidating and new move will come after result.already up 30-40% from last quarter result date

Consistently hitting LC for the past week. Couldn’t find any negative news on the Internet

Anyone know what’s happening?

Investors must have been bugging them with queries. They’ve posted an explainer to the exchange.

“As we move forward, we are also happy to confirm that our annual growth guidance remains unchanged.”

https://nsearchives.nseindia.com/corporate/NPST_19092024185945_NSEIntimation19092024signed.pdf

Disc - I am not invested in the company, and I am negatively biased. I do track the company, but I have not done deep dive - so please take my view with a bucket of salt.

UPI: Payment firms in a fix as UPI, RuPay incentives dry up - The Economic Times (indiatimes.com)

One of the things that has happened in Budget for FY25 is that incentives for digital payment promotion has gone down to 1441cr from 3500cr.

As of now, both P2P and P2M transactions are free. Then how does NPST and Sponsor Bank (say Cosmos Bank) make money?

The answer one can get is by reading conference calls, presentations of PayTM. PayTM recognized digital incentive payment in Q4 of every year.

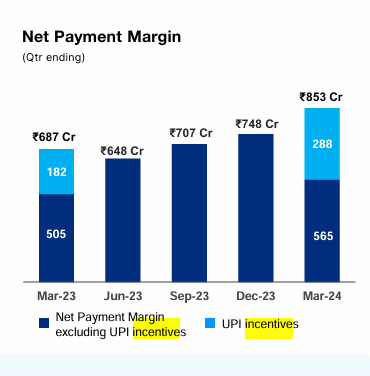

You can see that PayTM earned 182cr from digital incentives in FY23 and it earned 288cr from digital incentives in FY24.

Below image re-affirms that P2M transactions receive subvention from government.

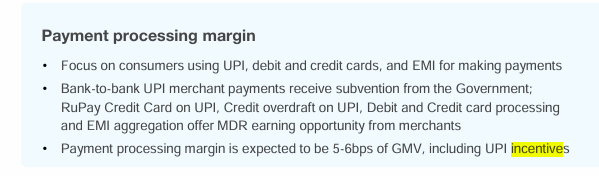

PayTM also earned some money through MDR. It lists the categories where MDR can be received - RuPay Credit Cards on UPI, Credit Overdraft on UPI, Debit & Credit card Processing, EMI aggregation offer.

So, considering these things, following are few points to ponder over -

-

Cosmos bank is entitled to subvention money from GoI based its market share in P2M transactions. Cosmos bank does not want to commit large capex to NPST. So what cosmos bank has done is that - they have agreed to share some portion of incentive with NPST.

I am not clear on accounting - but it looks like NPST recognizes the revenue upfront and probably Cosmos bank pays upon agreed rate to NPST. Then Cosmos bank receives the amount from GoI in Q4 and everything works out. -

Currently industry or investors are assuming that GoI incentives will grow in proportion with UPI transaction growth.

GoI has, at least for now, not agreed with this and has reduced allocation from 3500cr to 1441cr. From GoI point of view, they have done the handholding to bring the industry to this stage. But from hereon, industry has to find ways to make money. MDR on transactions above 2000 is one idea. Eventually, Industry demand for incentive growth can be 10,000cr or more and Budget simply would have no appetite for this kind of outlay. -

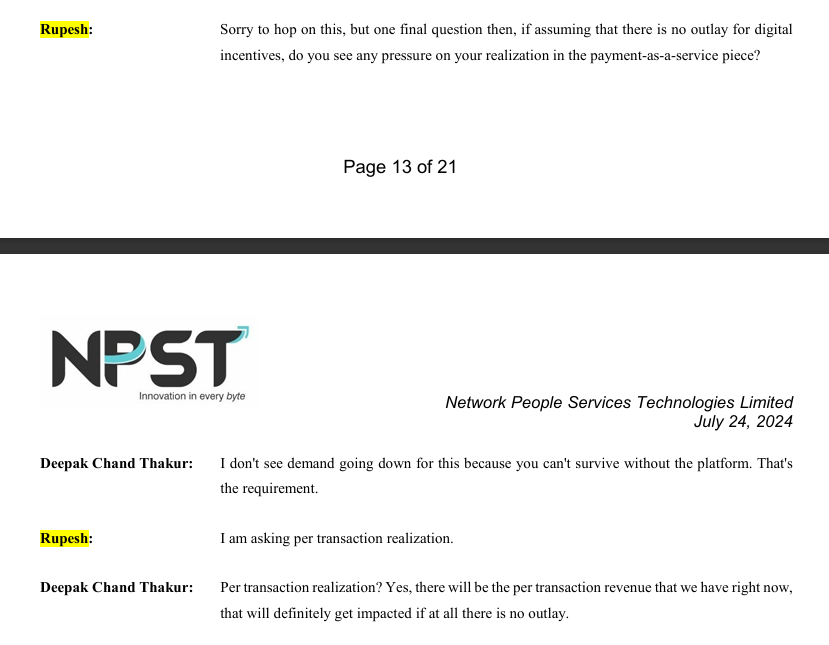

I had asked this question in Q1 conf call. Management has confirmed that if outlay gets reduced, per transaction money they charge to Cosmos bank will get reduced.

PayTM Q1 call had already happened prior to budget. But there are news articles after the date and VSS talks about becoming profitable “without digital incentives”

Paytm sees no impact of lowering UPI incentives on its path to profitability (newindianexpress.com)

The question investors of NPST should ask themselves are -

- What is the probability the GoI would backtrack and increase the budget of digital incentives? Would it continue in FY26, Fy27 and so on - even if it happens in say FY25?

- What percentage of NPST revenue is from MDR categories that are mentioned above in PayTM presentation?

Hope this helps.

Good point Rupesh but I wonder why analyst and big investors weren’t worried about this back then vs acting suddenly now? Why is the reaction so late?

If the low value transactions are not incentivised the govt will basically kill the digital cash economy. They wanted to remove cash and make everthing digital so that then can have a 100% white economy and also be able to track fin transactions. They are using all this data in multiple ways, tax evasion, payments tracking etc. So somehow this whole story is not adding up that they claim that the critical mass for UPI has come and small value transactions need to be taxed. This will only lead to the old way of working, cash economy will start flourishing again. Indians are very smart and will stop reduce usage of this, cash circulation will increase.

I think the following stat is quite worrying as per me.

Check this: https://www.npci.org.in/what-we-do/upi/upi-ecosystem-statistics

Filter Top 15 PSP volumes for July and Aug. Check the “UPI Payee PSP Volume” for Cosmos bank which is the main sponsor bank for NPST. There is a drop in volume from 297 million txs (July 24) to 60 million txs (Aug 24). Drop of 80%. This points to some big issue at Cosmos.

Also, note prior to May’24 the volume at Cosmos was growing inline with the other PSP players. But what explains the sudden jump from May 24 - 70 million txs to Jun 24 - 260 million txs?

Payee PSP - Under this function a bank can onboard a customer/merchant & allow them to receive money basis allocated UPI ID or raise a Collect request. It is also known as beneficiary PSP/resolving PSP.

In the last press note I guess they have explained the reason as per below.

Additionally, we are implementing policy upgrades related to processing and merchant acquiring on our existing EvoK 2.0 platform to align with evolving industry and regulatory standards. While these upgrades are essential for the platform’s long-term success, we anticipate some short-term impacts. However, it will pave the way for long term growth.

Main question to predict future growth potential for NSPT is how much MDR contributes to revenue and PAT?

If this is under 25%, growth numbers may be impacted a bit, but given their guidance of 75% growth, it would still be able to grow at 55-65%. If revenue from MDR contributes around 50%, then worried about them meeting their growth projections.

I was just checking the link and see that its only 2 months that the volume is high i.e. July and June @ 297 mn and 260 Mn tx, prior to June the Tx is in the same range as in Aug, in fact it is higher in Aug than in Apr and Mar.

Its possible that there was a surge in June and July for some reasons.

You are right.

This is the trend since Jan.

Cosmos Bank

Jan 43.80

Feb 44.02

Mar 44.71

Apr 61.64

May 71.19

Jun 260.4

Cosmos Coop Bank

Jul 297.65

Aug 60.039

Thing to watch out for is, market would be looking for a explanation for this sudden change in trend, because it’s priced for growth (isn’t it ?) If there is a rationale explanation, then this could be a good buying opportunity?

If management explanation is true (short term blip in revenue due to ongoing up-gradation process of EvoK 2.0 platform which will help them in long term revenue growth) then this was a great buying opportunity. Q2 - con-call is going to be very interesting. Before con-cal stock may have bottomed out for now

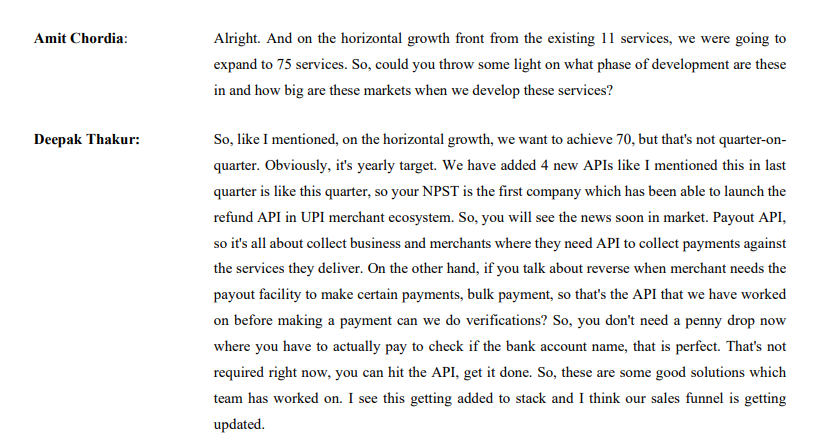

The revenue growth is going to come from adding new products as well. If we take a look at the concall of Q1 FY23 then management has guided thar there are 70 products which will be live in next few years from the 11 which was till Q1 FY23.

I believe its not just the UPI transactions which will drive the growth but new products also will be contributing in the growth.

Disc: Invested

This is just same data that I have posted on twitter before.

Q2 revenue is well over q1 of 60 cr. but can expect that as a min guidance no

Rest everyone is free to take their own call but one month of drop cannot be compared to previous and make assumptions.

Could you post the twitter link ?

My thoughts

- There is a long term story and then there is a medium term one. In long run, the other products might be more relevant. In the medium term however, we have to take note that, 80% of the current revenue (last Q) came from evok and this contribution grew from around 66% in Q2’24. All said and done market is giving such fantastic trailing multiples as it’s discounting the evok;s growth trend of last few qtrs to continue.

- If there is a question mark raised on the evok business segment’s growth then we have to sit up and take note. The reduction in govt. incentive was the first dent. then this revelation of Cosmos Payee PSP Nos for Aug.

- Can the shift from evok 2.0 to 3,0 have caused this reduction in volume for Cosmos? I doubt it, because NPST is bound by agreement for 99% uptime (Page 194 Rhp) . New version of software are typically not deployed by such disruptions in a industry as critical as dealing with payment systems.

- NPST’s share in the fees earned for providing the evok services to cosmos is 75% of what cosmos earns from merchant. So it’s very much like disrupting your own services not just a service to a customer.

- I am not able to figure if there is a seasonality aspect to the evok nos. or some other aspect that we are missing.

On point number 2, looking at past data, the number for Aug doesn’t seem to be the anomaly, but Jun and July are. Seems odd, this should be clarified in the next con call maybe.

On point number 3, the press note says policy upgrades for Evok 2, not version upgrade from 2 to 3 , would cause the blip. Since they’ve explicitly said a blip is expected, we should clarify this as well.

Hope they know what they’re doing and won’t try to disrupt the momentum ![]()