If you are worried sell what you hold. If you dont hold dont buy. Dont see what is the worry in either case ![]()

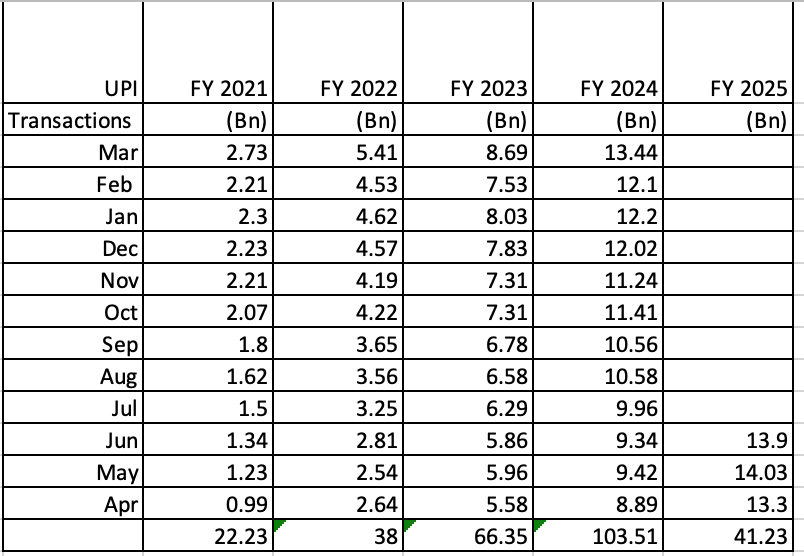

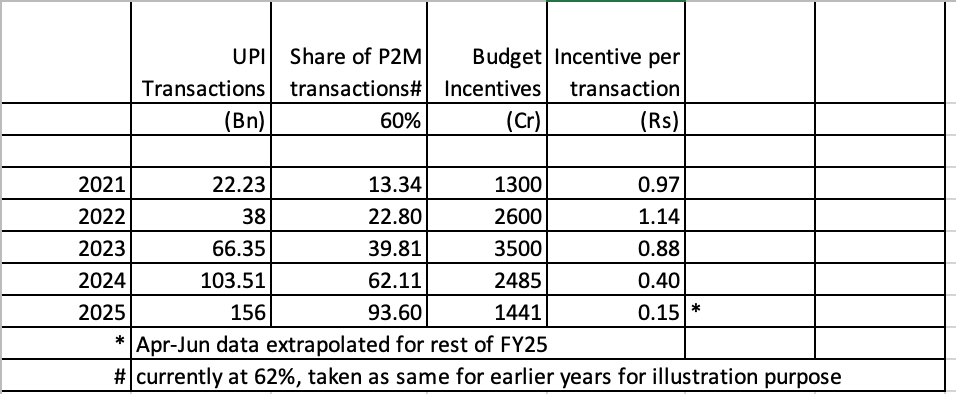

See the growth in UPI. Its a play on UPI.

As for your question if I hold? Off course I do…

If you are worried sell what you hold. If you dont hold dont buy. Dont see what is the worry in either case ![]()

See the growth in UPI. Its a play on UPI.

As for your question if I hold? Off course I do…

This platform for sharing your thoughts experience and knowledge of investing.if u don’t need any idea or valuation matrer or u think you are supreme why should u here.go see the the tv business channel makes everyday 500. Best of luck for you.

@Ajijmortaza Of course if the growth is not as per expectation the stock price will fall, that is true for any company and yes companies like NPST have more to lose if their future plans don’t go as expected.

Their PAT was 16Cr last quarter even if I assume they will do the same in the next 4 quarters their 1 year forward PE will be around 85 (5500/64). If they make 100Cr in profit forward PE become 55. For such high-growth companies estimating last year’s metrics vs 2-year forward metrics can make a lot of difference.

I would say do your own projections and see how these numbers look like 1 or 2 years down the line.

Disc: Invested and Biased.

TAM itself growing @ 100% CAGR for next 2to 3 years. Management guidance for this year revenue growth 75% to 100%. 1 year’s forward revenue= 380 core. With latest EBIDTA margin 35%, PAT can be anywhere around 100 crore and 1 years forward PE=53. A business growing at 80% CAGR and 1 year’s forward PE = 53. To understand growth driver, Check in your surrounding about use of UPI payment growth. Beside the UPI growth they are creating new product as future growth driver. Their peers are not listed and they are mainly in specific segment of UPI ecosystem. But NPST is creating complete solution which will enable them to serve most of the segment of UPI ecosystem. AI is going to be embedded in all their product and solution. Current growth is coming from product they have developed earlier. Currently they are developing product for future growth. I could not decipher their con-call to fully understand their product solution. however above is my basic understanding after going through their conalls. Disc. Invested and biased.

Hi Everyone

A query for those invested in and tracking NPST closely. Something I just started pondering on

Have a look at the underlying data on UPI transactions

Disclosure: NO investments in NPST, know very little, haven’t heard Concalls or done any analysis myself, but as is my wont, just trying to understand the sustainability part, first.

Can someone who understands NPST business/revenue model well, break it up for us. Q1 revenue split was TSP 20% and TPAP (PPaaS) 80%, right?

P2P - no one makes any money

P2M - GoI refunds NPCI and Banks (for capital spends, digital promotion?)

some banks NOT doing any Capex - decide to use NPST PPaaS infra and commit to sharing some/most of what they receive from NPCI and GoI

if the PPaaS pie is 100, How much comes from

I work with a fintech so have a decent knowledge of UPI Infra.

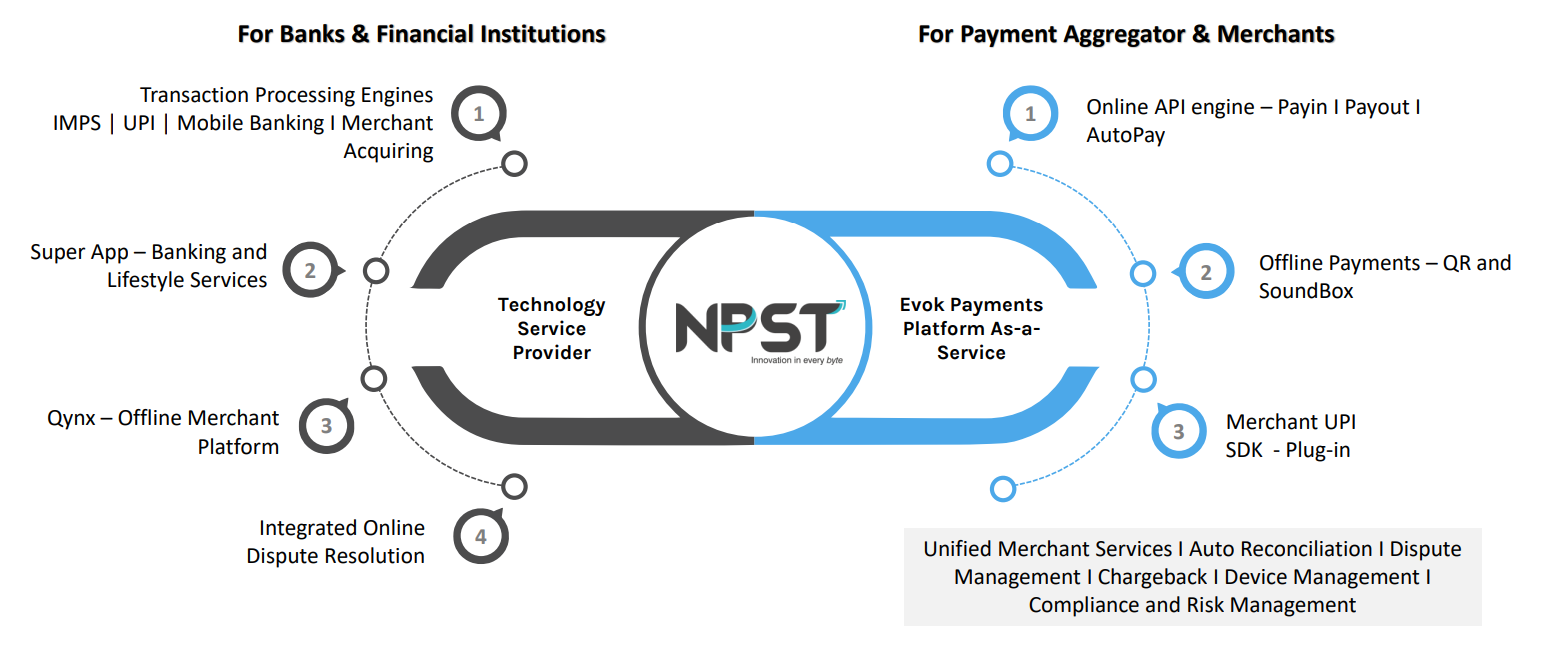

NPST has multiple products but is mainly divided into two customer segments.

For Banks/fintech: Think of it this way if I want to integrate UPI into my app I can either build the whole solution in-house or buy it off the shelf from companies like NPST. Now every company can not build an in-house UPI solution and hence the best way for them is to buy solutions from companies like NPST. Banks and Fintechs are mostly customers in this section. Also, there are a ton of smaller pieces in while UPI payments rail like UPI switch, Fraud detection etc, If a bank/fintech wants they can buy individual solutions as well.

For Merchants: These products are for merchants to receive the payments, manage the ledger, control fraud etc. They can be either through a soundbox that you typically see at a merchant, website, app etc. Here merchants are their customers and they charge merchants either on a monthly fixed rate or based on the no of transactions that NPST is routing through. Retail merchants do pay (I think Paytm charges 90Rs per month for Soundbox) not in the form of MDR but for the services they are getting.

So NPST revenue comes from their banks, fintechs, and merchants, not folks like us who use UPI. basically, they are a B2B company. Based on my understanding from their deck any solution that they provide to banks and fintech counts under TSP and solutions they provide to merchants or Payment aggregators counts under PPaaS. I am not 100% sure how they differentiate between TSP vs TPAP if someone can throw light on that it will be very helpful.

Here is their AR, which might be helpful to understand.[

SME_AR_24756_NPST_2023_2024_31072024233655[1].pdf (3.9 MB)

Agree with this, and also latest AR also confirms this. But they have some share which is as per the transaction cost (not sure about the percentage)

If you see above image, TSP is majorly License based or per login except Transaction Processing Engines.

On the other hand, for EVOK, Merchant UPI SDK - Plug-in might also be on pay per transaction.

Correct me if I’m wrong here, since UPI switch needs to be scalable based on number of transactions, I think this part is on pay per transaction model. Although, I’m not sure what is the revenue share of this particular segment.

Guidance given post FY24 below. Had guided for 75-100% growth for FY25

Comment post 1QFY25 results

1QFY25 revenue growth was 145% YoY and > 200% YoY on profits

Yeah, for the UPI switch it’s per transaction revenue for NPST, and the same for any kind of switch (transaction processing engines under TSP). Switch cost is usually very low (in paisa per transaction) but if you look at the overall level it will become huge and no of transactions is a lot. I am also not sure about the revenue share investor deck does not give details on this.

Exactly but given they’ve mentioned that they’re processing almost 6% transactions and it is a volume game, I think it’ll have a noticeable impact.

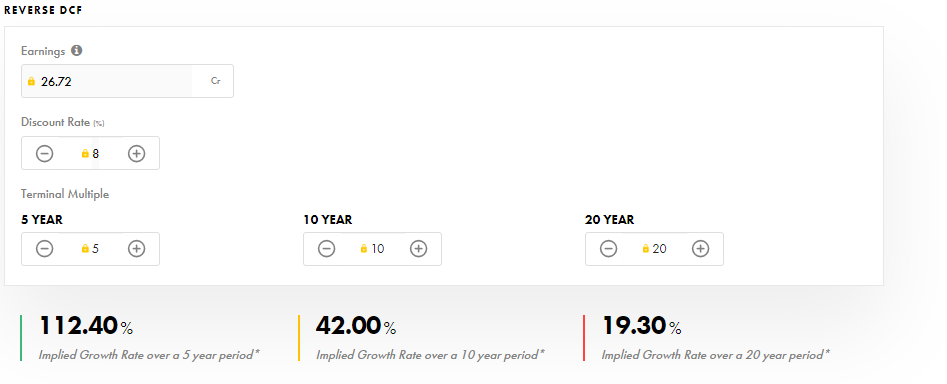

I honestly feel the valuation has gone through the roof. A reverse DCF would give incredible growth assumptions built into this price, at a PE of 152!

Can you please mention the growth assumption built into the valuation as per DCF Model

Few inputs from my understanding.

Yes. that’s the split, and TPAP/evok/PPaaS was about 40-50% at end of Q423. So clearly this piece is playing a bigger role in the incremental growth and that is what mgmt. envisaged from their early con calls.

I think for NPST the revenue comes from payment aggregators/clients. Who, in turn might be using the revenue pool of MDRs they receive for their payment services from all kind of payments including CC/DC/Online Banking. So there might be some cross subsidization and some part may be aided by govt. of India support (not sure how that get’s distributed to the payment aggregators.

Yes, seems like the gaming players are a good part of their revenue, they didn’t give the exact numbers when asked in Q424 call. From what i heard from industry sources the gaming players do give a MDR even on UPI transactions. GMV for the evok business itself has moved from 5k cr. to 10k cr. between Q324 to Q125 !!

I think, overall we should see MDR getting reintroduced some time in future. The payment system is moving towards UPI and it’s becoming more feature rich. It’s hard to reverse this value migration. only natural conclusion is, it won’t be free or subsidized for ever by Govt.

There is lowering of cost for the entire ecosystem from the adoption of UPI like like in ATM/Cheque/Cash printing etc…so someone will own the bill for this tech adoption. NPCI has done it’s part, now the ecosystem is blooming.

Good read on the topic of MDR https://www.financialexpress.com/business/banking-finance-mdr-continues-to-suppress-rupay-credit-card-growth-3432144/

Here are the implied growth rates based on reverse DCF per Tijori Finance:

Does anyone know when NPST is likely to come on to main board?

At the end of 2024-25 expected as per management commentary

How does listing on main board work?

Does sebi have some regulations or it depends ln management?

criteria like minimum number of years on SME board, number of share holders, net worth are applicable