commodity prices are taken care in scenario “Valuation with 2016-2020 as baseline”. Wherein i considered 60% fall in commodity price compared with peak (7500) in 2022.

3 Likes

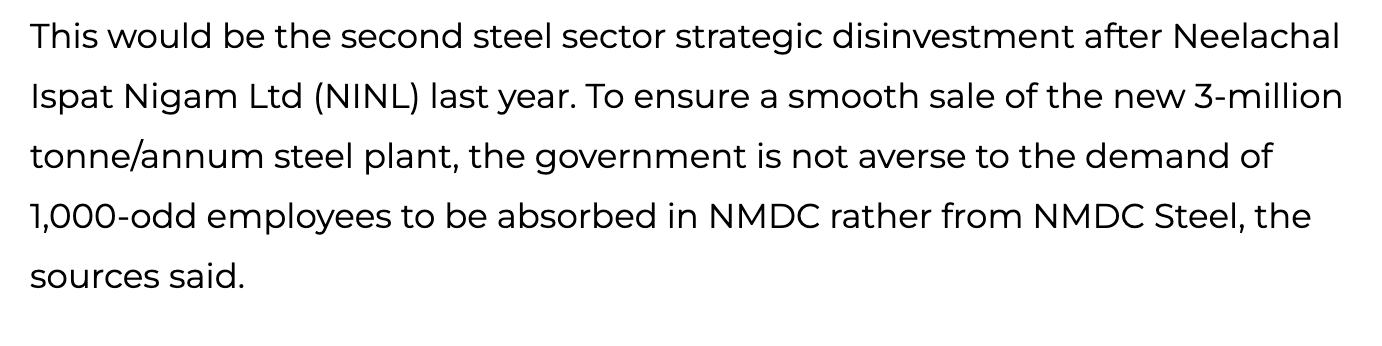

If NMDC absorbs these 1000 employees, this should be quite negative for the stock. Any idea about this situation?

Hello Everyone , after going through this thread I felt the need to start a new topic ( also as many of the fellow investor’s mentioned the need for it to be addressed as a separate entity )

Hence here is the New Topic on NMDC Steel Limited : NMDC Steel ( NSL ) - A Unique Demerger Opportunity

Please feel free to add your personal view’s so that we could grow together !

3 Likes

Summary of Q4FY23 concall:

-

Pricing pressure. International iron ore prices have come off significantly and might put pressure on NMDC to also reduce the sale price in the near term. However, NMDC is still cost competitive vis-a-vis imported iron ore: the sale price of NMDC iron ore is still between 10% less (for west coast) and 30% less (for east coast) than the landed cost of internationally sourced iron ore.

-

Management is targeting 46-50mnte of volume in FY24. The enhancement in production is dependent on i) enhanced efficiency, ii) normal monsoons and iii) capacity enhancement of Kumaraswamy mines from 7mnte to 10mnte. By mid FY24, enhanced capacity is likely to come on board.

-

Key projects currently on are: i) Pellet plant of Rs1200 cr, ii) laying of slurry pipeline ~Rs 1100 cr, iii) beneficiation plant of Rs 900 cr, iv) SP3 plant in Kirandaul at Rs 3000 cr, v) capacity enhancement in deposit 14 and 11C at Kirandaul at Rs1100 cr, vi) SP2 at Karnataka of ~Rs 1000 cr (already sanctioned and clearance received).

-

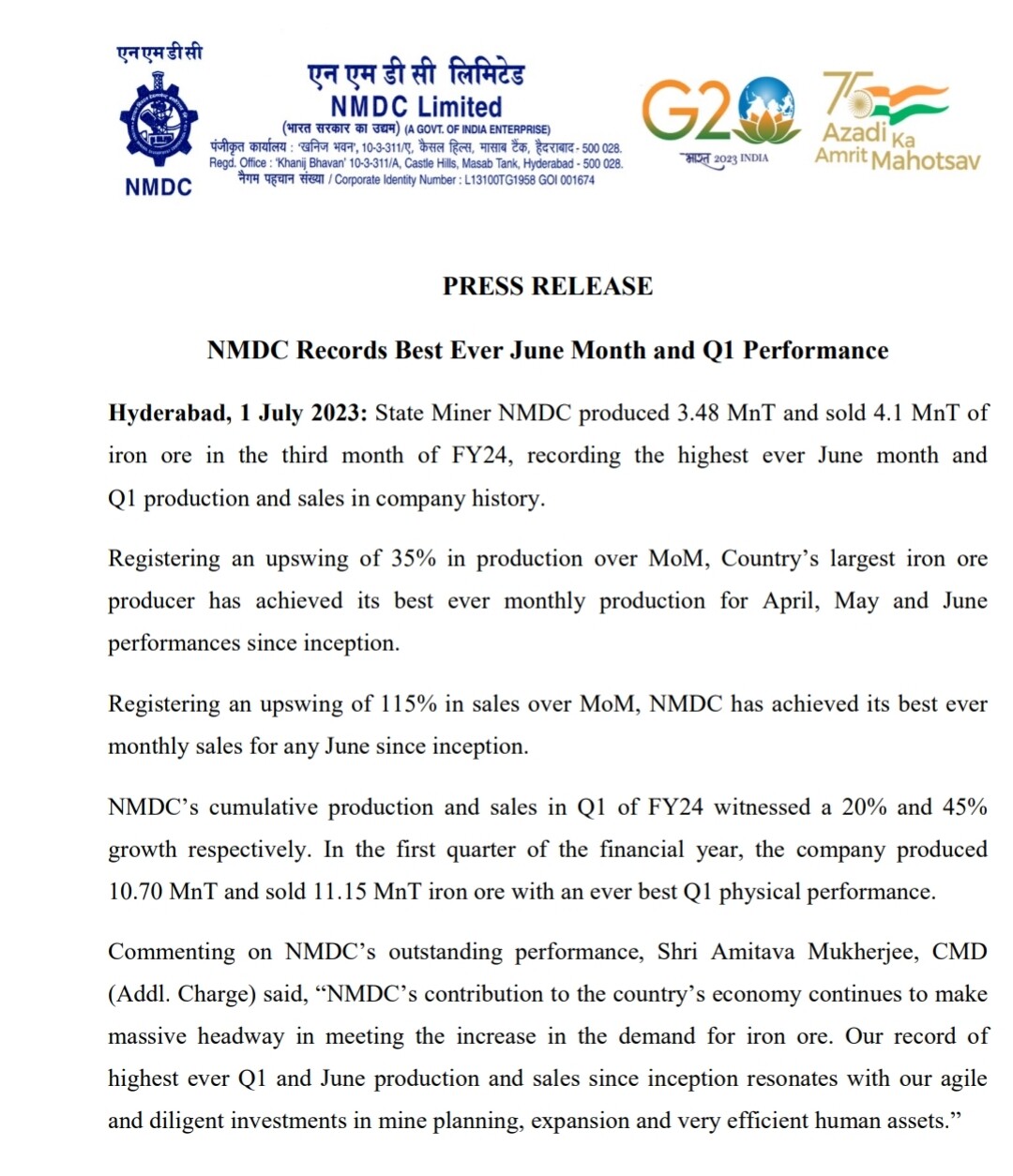

NMDC sold 5.5 MTin Mar23 (best ever) and also Apr23 was also the best ever. In May23, production and sales have been much better compared to prior years. Hence, management expects Q1FY24 to be one of the best quarters in terms of volume.

-

Domestic demand is sufficient to meet the increased production requirement.

-

Steel plant is expected to commission by June-end. All auxiliary equipment has been commissioned. When running at full capacity, the iron ore requirement of the steel plant will be about 5.4 MnTPA (=1.8 * 3 MnTPA ). The NSLNISP steel plant has a long-term agreement with NMDC for supply of iron ore and NMDC would anyway be the most economical way for the new plant to source iron ore. In other words, when NSLNISP is operating near capacity, it has the potential to boost NMDC sales by ~10%.

-

Kumarswamy mine was renewed in Oct’22. Hence, additional 22% royalty on sales

is applicable. -

Exports. Domestic realisation is always higher than exports.

-

During the quarter, NMDC reported exceptional income to the tune of Rs 1237.27 crore. Exceptional income includes a) Rs 957 crore from monitoring committee towards 10% of the amount withheld for the period January 1, 2019 to March 31, 2022, b) Rs 279.67 crore profit on strategic divestment of NINL (net off the gross amount of Rs 380.27 crore received against the amount invested in NINL of Rs 100.60 crore).

-

Iron ore sales realisation for the quarter was at Rs 4663/tonne, up 22% QoQ. EBITDA/tonne for the quarter was at Rs 1745/tonne, up 46% QoQ. For Q4FY23, NMDC reported sales volumes 12.4 million tonnes (MT), up 30% QoQ and flattish YoY.

-

Cash equivalents are roughly about 7000 crore which the management primarily wants to use for the aforementioned capex projects with payout to shareholders being secondary. Moreover, coal purchased for the demerged steel plant NSLNISP is a receivable of ~2540 crore recorded under non-current assets and the same is expected to be received from NSLNISP in FY24E.

-

Receipt of Rs 960 crore from Monitoring Committee. Apart from receiving 960 crore

already from the Monitoring Committee, NMDC still has roughly half of the amount yet to be received. Furthermore, the cash balance is expected to increase as the amount was received post Mar23 and hence, is not reflected in the balance sheet as of now.

14 Likes

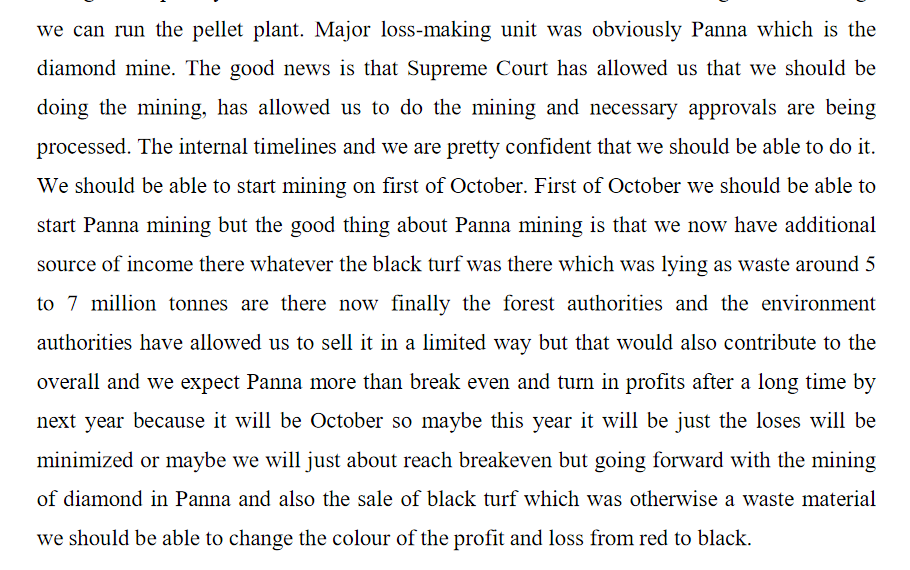

saw this bit in the conf call transcript. How much does this help in their revenues? A diamond mine?

I have no idea what kind of additional revenue it will produce/profits it will add to

1 Like

Nmdc Ltd: Nmdc Records Best Ever May Performance | Hyderabad News - Times of India (indiatimes.com)

Also Iron Ore prices went up over 3 percent the other day and is at a 7 week high. Might bode well for NMDC in the short term atleast

1 Like

Hey @Dinesh_476 , could you share the rationale for taking 10x PE multiple in arriving at valuations, given that other similar (mining) players currently trade in 5-9 x PE range?

Thanks @utsav31 for pointing this out. This is a commodity company and the mistake i have done is valuing it based on the PE number.

The ideal way to value this is based on the -

-

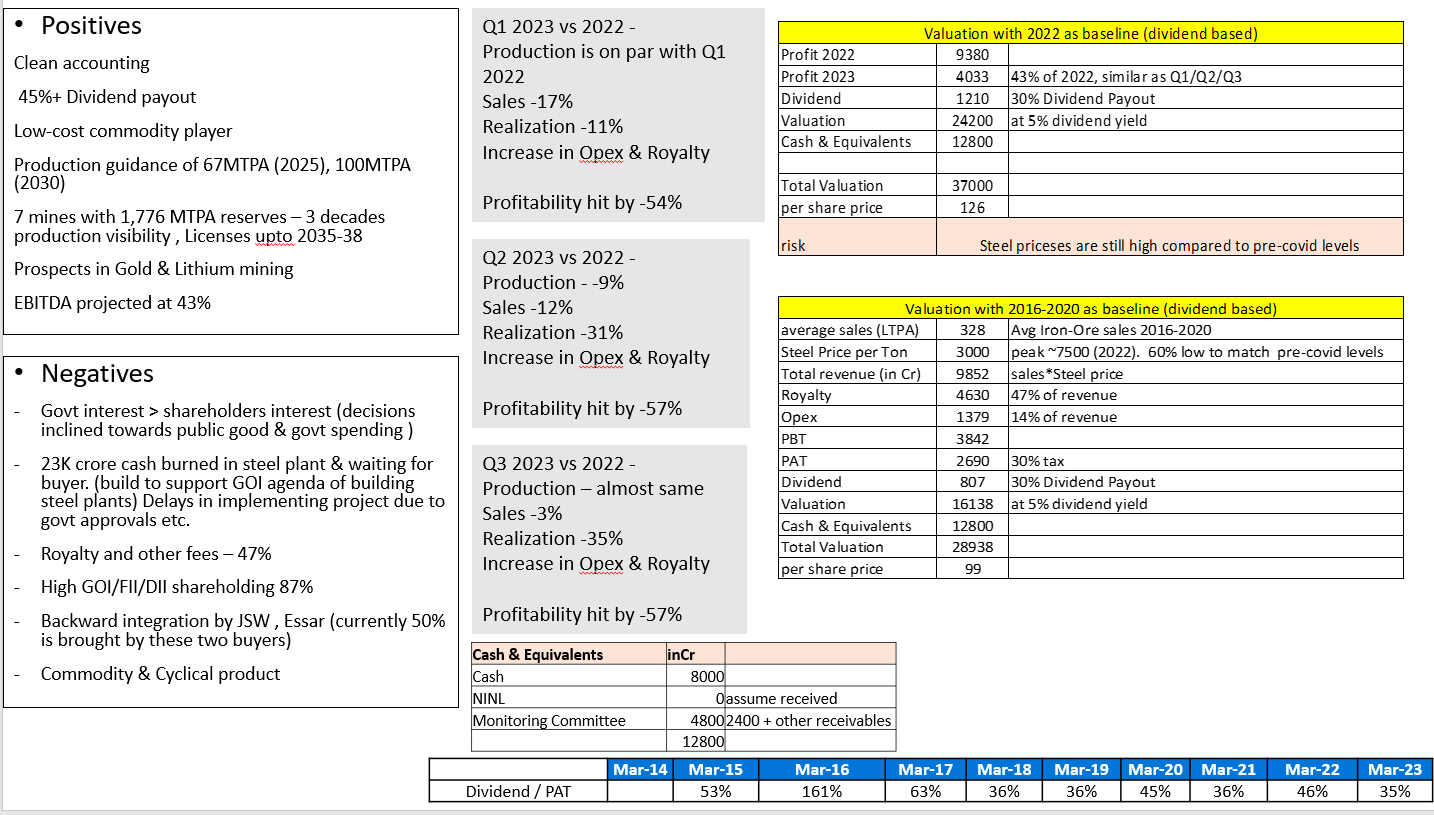

Book value. i.e we should invest when the price is less than book value.

-

As NMDC is dividend paying company and most of the dividend is paid to govt of india (61%). There will be assurance that dividend will continue to flow.

Dividend - Rs.14.74 (2022), Rs.7.76 (2021), Rs.5.29 (2020), Rs.5.52 (2019), Rs.4.3 (2018)

Moreover the prospects of the company remains optimistic. As they have large mines with useful life upto 2035, Low cost operations, low debt, One advantage of having GOI ownership is that the accounts will be relatively clean & scrutinized .

Below are the valuation scenarios based on Dividend -

6 Likes

Can you explain why high FII/DII holding is a negative?

Ideally, for a stock to become 5X or 10X in value, an investor should enter before the FIIs/DIIs. Once FIIs/DIIs start accumulating the stock, the price re-rating occurs as they buy in large amounts.

In this scenario, where FIIs/DIIs own a large percentage of shares, even if they sell a portion of their holdings, the prices get hammered in the short to medium term."

4 Likes

It is Correct. These type of divident stocks should be bought at low and be sold once it goes up in cyclicity. Since the prices of materials never remain too high for any mineral unless it is going to be extinct, that too in very near future… nmdc can be accumulated once price comes down.

3 Likes

Thanks @Dinesh_476 for the detailed working. Agree with you on the part that NMDC has good prospects, however, currently its trading above BV, hence limited margin of safety. Given direct co-relation with iron ore prices (which are expected to cool down due to macro factors), I would continue to watch the market.

Gold and Diamond mining are adjacencies which will take time to play out.

Disclosure: Not invested, studying

1 Like

Good collection of data and I agree with the analytical approach in general. Thank you for sharing. Moreover, I agree that the years 2016 to 2020 are a more reasonable (perhaps slightly conservative) baseline.

But I would like to point out a couple of things. Firstly the production of iron ore by NMDC has been growing (by fits and starts but growing nevertheless): from an average of about 335 lakh tonnes per annum during the three year period upto Mar18 to an average of 374 lakh tonnes per annum during the three year period upto Mar23, thereby implying a volume growth of 2.2% CAGR. NMDC has just yesterday reported increased production numbers but its not clear if that is sustainable. I would feel comfortable assuming volume of 400 LTPA on average during the next three years and given the increased production this quarter, would consider it a conservative estimate. Secondly, I think we should do an adjustment for inflation for the price of iron ore. So while the average price of iron ore during 2016-2020 was about 3000 per tonne, doing an inflation adjustment of 5% CAGR should imply an average revenue per tonne of about 4200 per tonne during the next three years. If I use the rest of assumptions as it is (namely royalty of ~47% of revenue, Opex of ~14% of revenue, 30% tax, 30% dividend payout, 5% dividend yield) I get a valuation of about Rs 138 per share which seems like a conservative valuation to me.

Put differently, my baseline forecast for the next three years is PAT of ~4600 crores per annum on revenues of ~16800 crores per annum. This means that we are assuming a PAT margin of ~27%, which seems very conservative when we look at the PAT margin during the 2016-2020 period which was significantly higher. Even if we completely exclude the cash on hand (which is > 25% of the current market cap), then the valuation of 138/- per share still implies a multiple of < 9x on the baseline EPS of ~ Rs 15.70 per annum over the next three years. Note that this valuation also excludes any potential upside from investments made towards Lithium mining in Australia or the recent news on Gold mining in Andhra.

Would love to hear other views and/or points I might have missed.

Disclosure: Invested.

17 Likes