Parag Parikh Tax Saver Fund

Factsheet -September 2022

NMDC Ltd. Minerals & Mining

1.87%

Factsheet - January 2023

NMDC Ltd. Minerals & Mining

1.32%

Parag Parik trimmed its stake in NMDC Ltd by 1.87 - 1.32 = 0.55%

NMDC Ltd. Minerals & Mining

1.87%

NMDC Ltd. Minerals & Mining

1.32%

Parag Parik trimmed its stake in NMDC Ltd by 1.87 - 1.32 = 0.55%

Just to correct you, weightage of a script in MF may change due to change in AUM or change in price of individual script without being change in Qty. PPFAS has neither added nor sold any share of NMDC in last few months as per their fact sheet.

NMDC steel listing on Monday

From this article, Analysts valued NMDC steel plant is of 17K Cr and Book value of NMDC steel share is 56Rs.

JSW and Arcellor will race to acquire the NMDC steel plant to expand there India Business.

NMDC has spent 22k Crore in setting up the steel plant.

JSW steel CMP/Book Value is 728/257 = 2.38 times.

Tata steel CMP/Book value is 112/88 = 1.27 times

so in my opinion the market price has to be more than > 57Rs.

Disclaimer invested 2.5% of my portfolio.

Is it common practice in the past, to increase export duty heavily as it was done during past year to curb export of iron ore and steel? I was trying to find such instances in the past.

With increase in Import Export imbalance, is this appropriate strategy, I have not understood this.

Indian exports have been decreasing substantially in the past few quarters, and it may create some pressure on Export based revenues. Though managing inflation is necessary but are there other ways to do this?

I am researching on this topic.

Disclosure: Invested in NMDC.

As discussed earlier in this thread, the NINL was sold around 10K crore for 1 MT plant. But with all the increase due to inflation in raw material prices and labour cost the replacement cost of a new steel plant will be much higher. So at a minimum, 30K crores valuation seems plausible. Here is an article that says the steel plant could fetch up to USD 4 billion.

However, whatever value they come up with, NMDC will have to cough up the dough for the 10% stake. So NMDC share holders will lose a little but gain a lot if they hold on to NMDC steel till the stake sale goes through. I don’t see how the govt will sell for a subpar valuation. However, probability of a good outcome seems better than 50%. Please note, just a novice here. Not an expert.

Disc: Hold.

I agree…It should fetch good valuations. Not just for the capacity but also because its near to the iron ore plant and is a new plant with new machinery etc

i hope someone can start a new thread for NMDC steel, now that its demerged…

This was probably the reason for the spike in price after 3 pm today

Is anyone aware of what this 10% amount will be?

This 10% which I should get, which I have paid over the last 10 years or more, amounts to about 2400 crore.

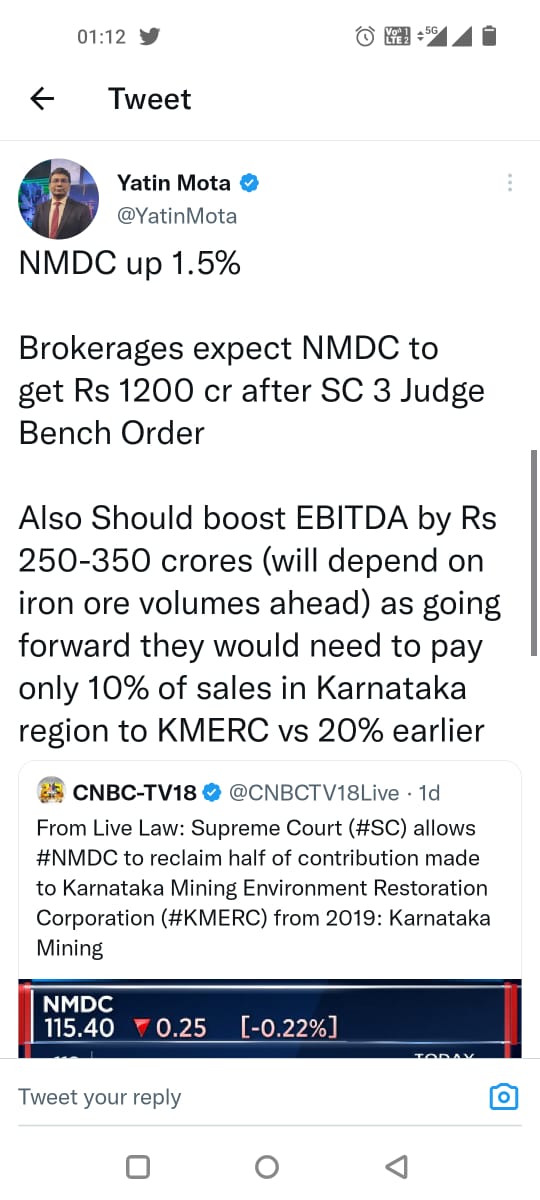

Karnataka Mining : Supreme Court Allows NMDC To Reclaim Half Of Contribution Made To KMERC From 2019

‘we direct the Karnataka Mining Environment Restoration Corporation (KMERC; the SPV) to remit amount at the rate of 10% out of the 20% which has been collected from the applicant from 2019 till 31.1.2023 and the amount shall be remitted within a period of two months from today, subject to further orders passed by this court pending adjudication on all issues. The applicant will continue to remit contribution at the rate of 10%’

Sr Adv Mukul Rastogi ‘This 10% which I should get, which I have paid over the last 10 years or more, amounts to about 2400 crore’.

Seems appx 1000 crore for 4 years… Now onwards KMERC will reatin 10 % inturn reduce the WC requirements as mentioned in AR.

This seems quite accurate. More than the windfall 0f 1200 crores, the 250-350 crores increase in EBIDTA seems like a good trigger as this directly flows to the PBT.

Can someone please explain why they have to continue to pay the balance of 10% even after Karnataka iron ore miners are allowed to sell privately and not through the KMERC?

** Commentary from IND-RATINGS **

The demerger of Nagarnar-based NMDC Iron & Steel Plant (NISP) from NMDC and its transfer to NSL was approved by all authorities on 6 October 2022. The appointed date of the scheme is 1 April 2021 and the effective date is 13 October 2022. NSL mirrors the shareholding structure of NMDC (government of India’s (GoI) shareholding of 60.79%, public shareholding of 39.21%) and shall be listed on BSE Ltd, National Stock Exchange of India Limited and Calcutta Stock Exchange. Furthermore, the formalities for the transfer of NISP’s assets and liabilities to NSL on a going concern basis as on the effective date of the demerger scheme is under process. The liability towards the NCDs issued by NMDC in August 2020 has been transferred to NSL, pending listing formalities.

There is an ongoing disinvestment of the GoI’s stake in NSL. The GoI shall divest its 50.79% shareholding in NSL, along with management control to a strategic buyer through a two-stage, competitive bidding process. A preliminary information memorandum and a request for expression of interest for the interested bidders was floated on 1 December 2022. As per the first stage, multiple expressions of interest were received on 27 January 2023. The second stage is under process. Subsequently, the GoI’s remaining 10% stake in NSL shall be offered to NMDC. With this proposed arrangement, NSL shall forego all the associated benefits allowed due to a public sector undertaking (PSU) status, which shall have a material bearing on the rating assessment. Further, the industry positioning and financial strength of the new buyer shall also impact the rating.

Considering the timeline for the process is uncertain, Ind-Ra will treat the disinvestment as an event and review the rating on receiving clarity on the new strategic buyer and its financial, operational and strategic linkages with NSL post the conclusion of the disinvestment under process.

Key Rating Drivers

Advanced Stage of Operations; Favorable Funding Pattern: The steel plant is in the advanced stage of implementation and likely to commence operations in 1QFY24. Of the total project cost of INR219.40 billion, 97.5% was incurred as of end-October 2022. The total capex has been funded by debt of INR29.26 billion till October 2022 and has an undisbursed loan of INR20.74 billion for meeting the balance expenditure and support liquidity post the commencement of operations, as the capex required is lower than the undisbursed amount. Ind-Ra estimates the debt/equity ratio to be favourable at 0.3x compared with other steel projects, requiring a substantially high proportion of debt funding.

Strengthening of NSL’s Business Profile: The proposed steel plant is fully integrated, except for captive iron ore mines for which it has a long-term tie-up with NMDC, assuring 100% availability of iron ore. The proximity to iron ore mines shall result in significant logistics cost savings. Furthermore, leveraging on NMDC’s long-term established relations with suppliers, NSL has an arrangement with coking coal suppliers assuring around 40% of the coking coal requirement is met. The balance shall be arranged partially by centralised quarterly procurement channels for key PSUs. Additionally, the plant’s operations shall be supported by around 25% captive power generation and the balance shall be procured from the state grid. NSL will be producing value-added flat products (hot-rolled coils), earning a relatively higher profitability than commodity products. MECON Limited has been awarded the operations and maintenance of the plant during the commissioning phase and subsequent operations.

On completion of the capex, the balance sheet of the steel plant will be significantly less levered than other steel manufacturing greenfield projects as the debt component in funding is less than 25% of the project cost. Although NMDC has infused more than the required equity in NSL, it is allowed to take disbursement of the full sanctioned limit as per the term sheet as reimbursement of capex. Ind-Ra assumes the plant will be ramped up in FY25, which will be the first full year of operations.

I don’t remember it correctly, but I think it was one of the management interviews from Jindal companies where they stated that the govt discouraged exports as it wanted to restore a demand-supply balance domestically. The objective was to lower the prices and hence inflation in the economy.

Has anyone studied Legacy Iron Ore…The Australian exploration company that NMDC has 93 percent stake in

Legacy Iron reports ‘outstanding’ gold intersections at Mt Celia project (smallcaps.com.au)

Is this something that can add some positive surprises/growth for NMDC?

Annual report of Legacy Iron Ore

annual_report.pdf (legacyiron.com.au)

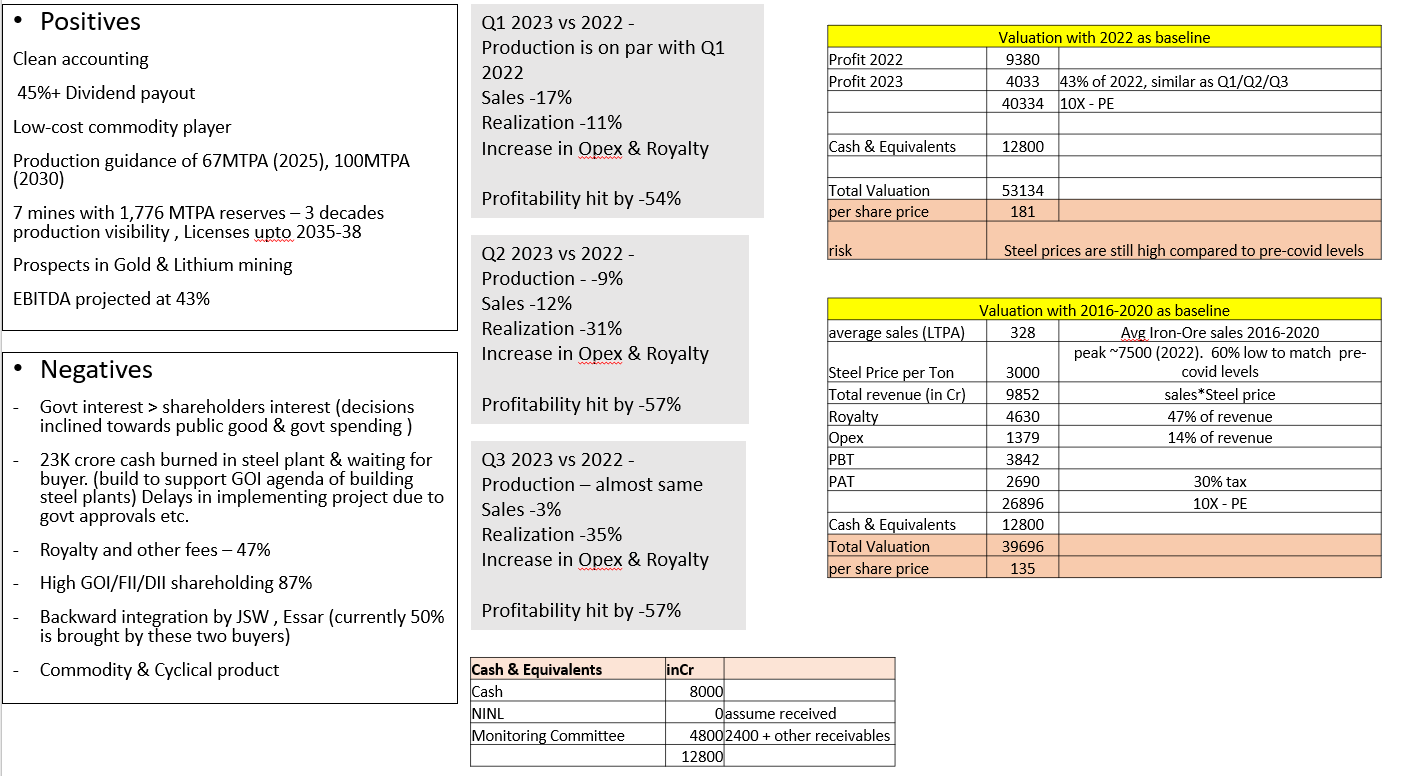

Very simplistic, conservative and nice valuation @135.

If commodity cycle (inflation) cools down, won’t the valuation fall or do you think it’s already baked in CMP?