Please find below my writeup on the NMDC Steel Limited. Views invited :

This would be my First Topic and after going through the NMDC thread , I realised the need of opening a new thread for this ! Please be supportive and share your insights so that we can get more depth in this.

I was not able to find much on the net and would have to wait for the future reports of the company , so I tried to dig into the reports to get a fresh view . I have highlighted some pointers below :

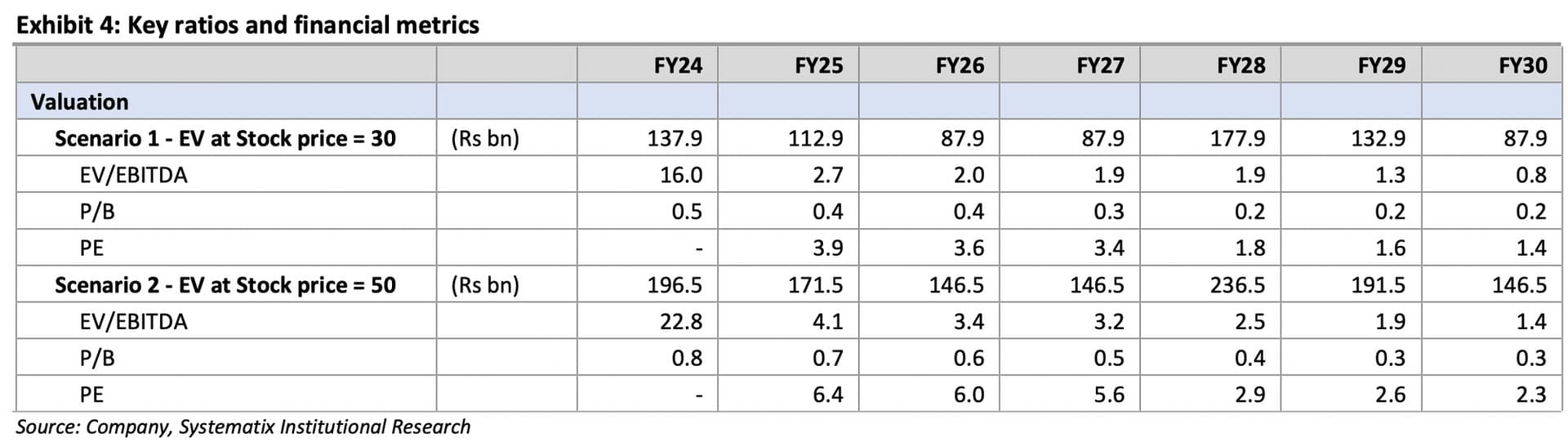

Note : The new entity will have a leveraged balance sheet, with the net leverage ((debt-cash)/EBITDA) of over 4.0x in the initial years, considering the issued and proposed NCD programme /bank debt of INR50 billion and the capacity utilisation of 50%-75%. However, the debt will be lower than that of other similar-sized steel plants.

I got this from the latest presentation by @Rakesh_Arora who I look upto in the steel segment !

( Would really encourage for your further view’s on this topic )

Hence, it seems like NMDC is going to take care of it’s child NSL which is a major positive I feel . But as mentioned above we will have to see how quickly the management get’s adapted to the new plant and it’s in & out working .

Thanks a lot for the read , hope I was able to add some value to this forum and my fellow investors🥂

While NMDC Steel is currently an events play. However in case the deal doesn’t happen or is delayed, one needs to track the date of commissioning of the steel plant. Also keep an eye on the debt the company is accumulating as this will impact the upside of market cap. Q4FY23 results become important from this aspect.

Thank you for starting a thread on this topic. Just a few pointers from my side:

The plant can be expanded to 6 MT as per the NMDC management without any further land acquisition.

I don’t have much information about this but from what I have heard through certain news reports, the pant is present in a Naxal area, and thus this is something that can drastically affect the operations of the plant. However, this is the reason why NMDC is retaining a 10% stake in the steel plant as they have high goodwill in that region. It would be great if someone can elaborate on this.

Lastly, I think in a reasonably good scenario the plant can be sold for 1 PB of around 20000 Crore.

Any guess how will the Karnataka election results impact the privatization focus of the government?

Typically 6 months prior to election, all discretionary policies take back seat. So this sale process has to finish by November 2023 at the latest or it will get pushed to post-election in FY2025. And current process does not look fast enough to complete the sale in the next 6 months. Is this a cause of concern?

Especially as steel cycle is going through challenges and NMDC mgmnt has no idea of how to run a steel plant and MEKON consultant is doing full O&M of a steel plant ‘for-the-1st-time’ (boiler commissioning faced significant challenges in 2022).

And delay in privatization will eat up the BV and increase debt at the same time as 1st year of operations should result in losses as only 1 MT will be operational (of the 3 MT).

txs - Ritesh

Disclaimer: Invested 0.25% of PF at 32ish and deliberating to sell or add further if more data point emerges

I don’t believe the Karnataka elections are going to affect the privatization at all. The plant is in Chattisgarh. And yes over there the INC govt has talked about bidding for the plant. However, I don’t believe that they will be able to beat the bids of JSW, JSPL, and Adanis.

Chattisgarh govt can complicate things here. However one of the interested bidder is JSPL who’s promoter is former Congress MP who is trying to get Chattisgarh govt to support his bid. In any case Chattisgarh elections are due in Nov’23 so something can happen earlier if they fear losing.

While don’t see any issues for the bids except political angle here. But timing is the only thing of essence here. I am hopeful that govt will try to do it before Chattisgarh elections due in Nov. But one can never be sure of these govt things

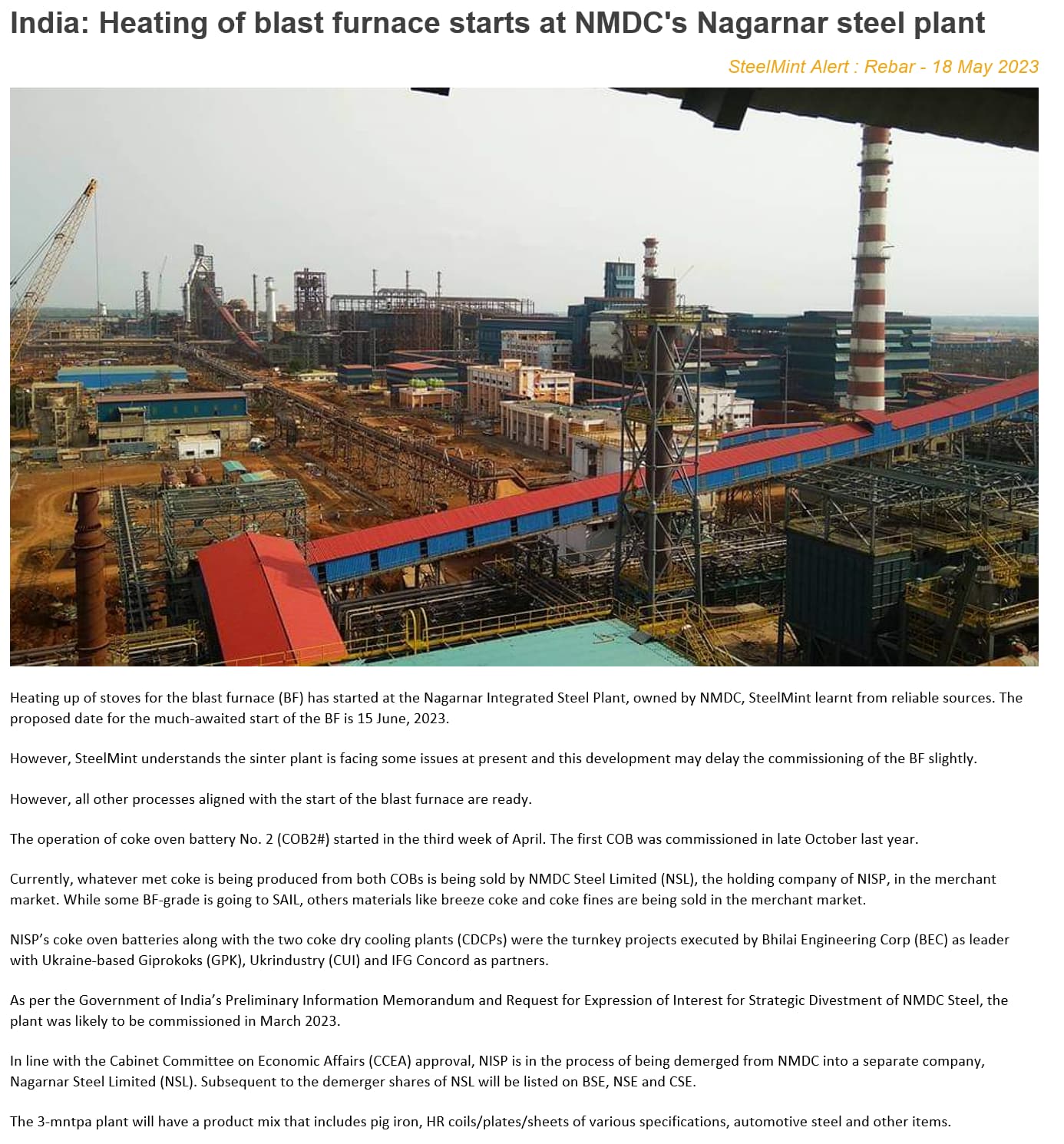

"Financial bids for NMDC Steel, which may fetch the government around Rs 11,000 crore for its 50.79% stake, will likely be invited after the company’s brand-new steel plant in Chhattisgarh becomes fully operational in June.

“Opening of the plant has begun with coke making, an official told FE, adding that the blast furnace too will likely be functional by June.”

There are certain businesses where government has its advantages, but steel making is not one of them. It is one of the really capital intensive industries and requires real smarts to keep making good incremental Capex decisions; Operational efficiency is critical. Longer it stays with the government, lower will be its value. If you chose to invest, invest on the buyer who buys the asset and not on the asset.

NMDC by itself isn’t a bad option: Mining is slightly more suitable for a government than a steel plant. There may be an aberration, but we don’t invest based on speculation. NMDC has great assets; Govt can earn significant revenue through royalty & stake with an efficient operator, but my bet is govt will continue to have it, to create “Chairman” posts…

I disagree on the logic of this though the conclusion that GOI should generally not be in the steel industry is something I too believe in.

Capex Heavy industry, no private player would do in a new area unless the GOI kickstarts it. By new area, a new location greenfield set up. JSW was less than 80 INR for years till it repaid its 20K cr debt and then it shot up. GOI spending money with intent derisks for other players to come into the same area. Target is 300MT and we are nowhere close to it at 110M now. Someone has to throw n 1-5B$ to show intent. Post set up of factory, historically PSUs have not done great unless in monopoly situation.

Good perspective. A few questions come up though:

When the private capacity is in multiples of PSU capacity, why do you suspect private players will not invest, esp when they can invest outside of the country, why not in the country?

Market projection 300 mt vs demand predicted by the market. Why do you think existing players will not invest when they see the opportunity?

Won’t the private players become even more defensive when the competitor is the government?

Is the Capex connected with policy uncertainties or technology uncertainties?

Why do you think existing players will not invest when they see the opportunity?

they may expand their current facility but new ones, they’d rather wait for GOI to put the roads, env clearance, and paperwork for the whole area before coming in.

Won’t the private players become even more defensive when the competitor is the government?

Yes but unlikely as GOI employees simply suck out the profits/unionise to make nothng profitable in the long run. Even highly successful monopolies like HAL, BEML, BDL dont scare private investment in defence and heavy industry

Is the Capex connected with policy uncertainties or technology uncertainties?

policy. Karnataka Gov has stopped all payments till review of infra work of prev gov is completed. AKA, reroute bribe to us to continue work.

As per the latest results provided by the company the book value comes around 58 per share which makes it.0.7x Price to book, Given the Co is ready for privatisation in near term and the likes of JSW steel bidding for it, it should atleast trade at 1x book value.

)

)