Thanks

Dinesh_476 and Sheekhuj for your detailed analysis, Looking at NMDCs past history its better to monitor how large the capex is for Investments in Lithium and Gold, keeping iron ore prices and other expenses as assumed ,all our valuations hinge on Cash reserves, and dividend yield.

Plus the gestations and vagaries for any Govt projects.

Any other views are welcome.

1 Like

How would the latest discussion on linking ore prices with LME impact multiples for NMDC? Is there an expected impact?

Any idea, what was the issue? The article just says, unethical behaviour.

1 Like

This is actually a very positive news for psus . Since the mistrust in psus was only because of this babu attitude of their management. If management is kept in line then they are all gems with very good income generating asstes.

9 Likes

On August 14, 2024, the Supreme Court ruled that states could indeed collect taxes on mining activities retrospectively from April 1, 2005 .

Any one studied the severity of impact on mining companies ?

1 Like

During concall, management informed that the impact would be around 35 crore. They also said their agreement with its customers include a pass through clause. So no major impact for them.

2 Likes

Thanks . Surprised why the mining stocks has been beaten so much!

1 Like

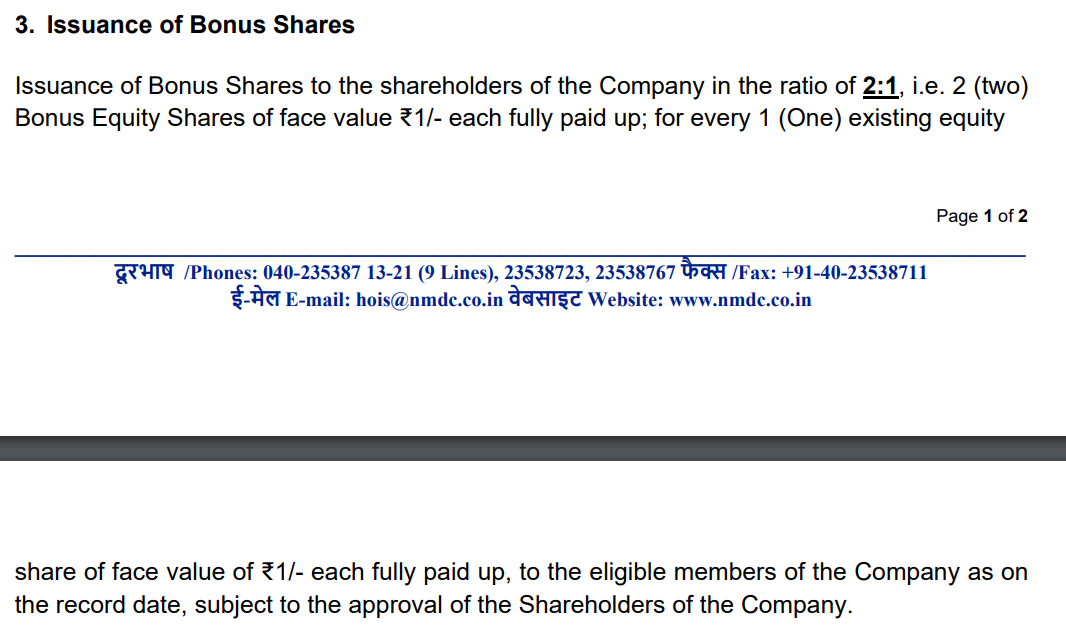

do you know the outcome of this?

Yes, board approved a 2:1 bonus issue on 11th November. Also, today there was an EGM to approve the issue of bonus shares and it has been approved by shareholders.

Record date will be announced in due course of time.

2 Likes

Key Details of the Bonus Share Issue

- Bonus Ratio: 2 new shares for every 1 existing share.

- Record Date: December 27, 2024, which determines the eligibility of shareholders for receiving the bonus shares.

- Deemed Date of Allotment: December 30, 2024.

- Pre-Bonus Share Price: Approximately ₹210 per share.

- Post-Bonus Share Price: Adjusted to around ₹70 per share (illustrative) after the bonus issue.

The total investment value for shareholders remains unchanged immediately after the bonus issue, despite the apparent drop in share price due to the increased number of shares in circulation. For instance, if a shareholder owned 10 shares at ₹210 each (totaling ₹2,100), after the bonus they would own 30 shares at ₹70 each, keeping their total investment value constant.

Implications of the Bonus Share Issue

Market Capitalization

The market capitalization of NMDC remains unaffected by the bonus issue. Before the adjustment, if NMDC had 1,000 shares at ₹210 each, its market cap would be ₹2,10,000. After issuing bonus shares, with 3,000 shares at ₹70 each, the market cap still equals ₹2,10,000. This adjustment is purely mathematical and does not imply any loss or gain in value for investors.

Trading Dynamics

Shares began trading ex-bonus on December 26, 2024. This means that any shares bought after this date will not qualify for the bonus shares. The adjustment in share price may lead to temporary fluctuations in trading volumes as the market adjusts to the new pricing dynamics.

Tax Considerations

Bonus shares are not taxed upon issuance; however, when sold later, they will attract capital gains tax based on their adjusted cost price. Investors are advised to keep accurate records for tax purposes.

Dividend Impact

Post-bonus issuance, while dividends per share may decrease due to a larger number of shares outstanding, the total dividend payout by NMDC is expected to remain consistent. This reflects the company’s ongoing commitment to rewarding its shareholders.

This bonus share issue represents a strategic move by NMDC to enhance liquidity and reward existing shareholders while maintaining its strong position in the iron ore sector.

The recent 2:1 bonus share issue by NMDC Limited will have a significant effect on the company’s equity capital. Here are the key points regarding this impact:

Effect on Equity Capital

-

Increase in Total Equity Shares: NMDC will issue approximately 5.86 billion new equity shares with a face value of ₹1 each as part of the bonus issue. This will effectively double the number of shares outstanding, increasing from about 5.86 billion to approximately 17.58 billion shares post-issue[1][3].

-

No Change in Total Equity Value: Although the number of shares will increase, the total equity capital in terms of value remains unchanged immediately after the bonus issue. The market capitalization will stay the same since the share price is expected to adjust accordingly following the issuance of bonus shares[2][5].

-

Impact on Earnings Per Share (EPS): With an increase in the number of shares, the earnings per share (EPS) will likely decrease unless NMDC’s net income increases proportionately. For instance, if the EPS was ₹6.66 before the bonus issue, it would be halved to ₹3.33 post-issue if earnings remain constant[2].

-

Liquidity Enhancement: The bonus share issuance is expected to enhance liquidity in NMDC’s shares, potentially attracting more retail investors and increasing trading volumes[2]. This can positively influence market perception and investor interest.

-

Regulatory and Market Considerations: The timing of this bonus issue coincides with market pressures due to proposed tax changes affecting operational costs in Karnataka, which could impact profit margins for NMDC[1][3]. Investors are advised to consider these external factors as they evaluate the long-term implications of the bonus share issue on equity capital.

In summary, while NMDC’s equity capital will see an increase in the number of shares, the overall financial impact on total equity value remains neutral immediately after the issuance, with potential long-term effects on share performance and investor sentiment influenced by market conditions and regulatory changes.

3 Likes

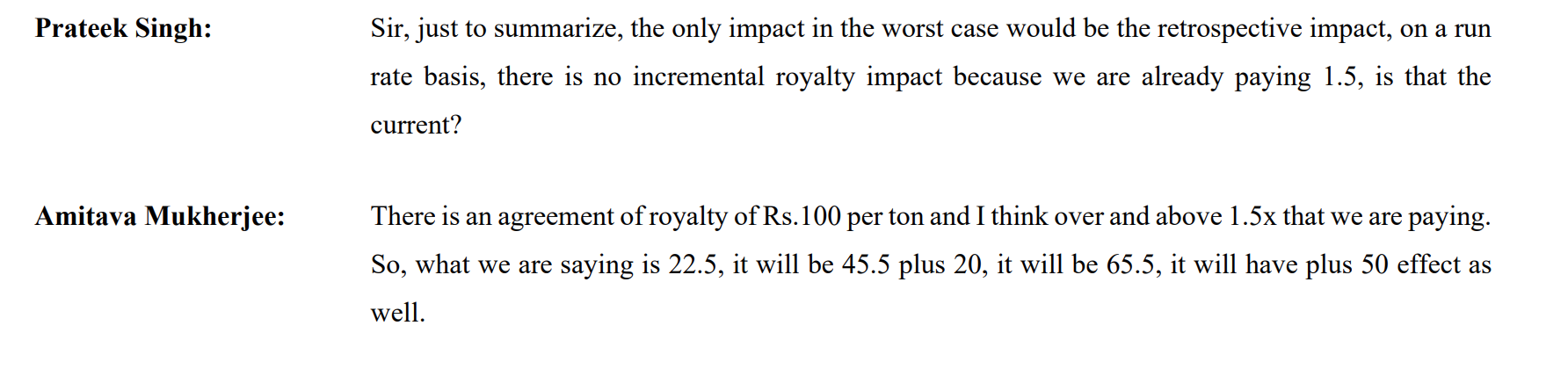

Given the recent hike in royalty in Karnataka, any idea on how the margins are going to get affected?

1 Like

Here are a few findings -

- NMDC has recently moved from internal pricing to IBM pricing which is inclusive of base price, royalties and taxes

- As per the MMDR act, NMDC has to pay 1.5 times the royalty on the Karnataka mines i.e. 1.5 * 15% = 22.5%

- This has been in effect since 2021 and NMDC seems to be already paying this. Probably, the additional royalty item in the P&L statement refers to this.

- The additional royalty is on top of the IBM pricing, so it cannot be passed to the customer

- The 100 rupees land tax on the Karnataka mines seems to be an additional burden which I am guessing will be around 160 crores for FY24. However, this should be paid retrospectively since 2005 (on one of the websites saw that this value is around 700 crores which is a one-time payment)

Net-net, don’t understand the knee jerk reaction that caused the stock to crash by almost 25%.

2 Likes

NMDC good Q3 FY25 Results.

Increase in Revenue.

Concerns:

Increase in Royalty Expenses.

and New Contingent Liabilities such as follows:

The Karnataka Legislature passed the Karnataka (Mineral Rights and Mineral Bearing Land) Tax Bill, 2024, in December 2024. However, as of the date of publishing results, it remains a bill, pending the assent of the Hon’ble Governor of Karnataka.

If enacted in its current form, the company may be liable to pay taxes retrospectively as per the specified rates in the bill. Considering its current status, the estimated amount of Rs. 13,510.90 crore has been considered as a contingent liability. The Governor’s request for clarifications and ongoing stakeholder discussions indicates that changes are likely before enactment.

As per the terms of Long-Term Agreements and Auction Notices, any statutory duties, levies, or taxes introduced in the future are recoverable from customers/bidders. Once the bill is finalized, the company will evaluate all available legal recourses for recovering these charges from customers I bidders.

2 Likes