PORTFOLIO UPDATE

CORE PF

| Stock Name |

Buy Price |

CMP |

Weightage |

Return |

Holding Days |

| LAURUSLABS |

340.79 |

387.15 |

40% |

13.60% |

3 |

| NEULANDLAB |

2100.01 |

3589.8 |

14% |

70.94% |

190 |

| SYNGENE |

682.35 |

805.35 |

11% |

18.03% |

162 |

| PRAJIND |

296.41 |

433.45 |

5% |

46.23% |

262 |

| ORCHIDPHAR |

552.27 |

575 |

5% |

4.12% |

62 |

| SADHNANIQ |

93.08 |

90.2 |

4% |

-3.09% |

105 |

| SYRMA |

346.72 |

494.65 |

4% |

42.67% |

127 |

| AXISCADES |

440.73 |

478.8 |

4% |

8.64% |

77 |

| DMCC |

307.08 |

332.8 |

3% |

8.38% |

112 |

| NEWGEN |

499.57 |

847.6 |

3% |

69.67% |

89 |

| SBCL |

146.02 |

652.3 |

3% |

346.72% |

162 |

| FLUOROCHEM |

2785.95 |

2789 |

2% |

0.11% |

1 |

| KOPRAN |

121.33 |

181.5 |

1% |

49.59% |

112 |

|

|

|

|

|

|

SECTORAL PF

| Stock Name |

Buy Price |

CMP |

Qty |

Weightage |

Return |

Holding Days |

| CIPLA |

1224.01 |

1222.25 |

21 |

19% |

-0.14% |

1 |

| DYCL |

509.47 |

591.45 |

50 |

19% |

16.09% |

1 |

| KAMOPAINTS |

343.84 |

194.4 |

73 |

18% |

-43.46% |

3 |

| REMSONSIND |

359.8 |

348.1 |

46 |

12% |

-3.25% |

1 |

| SUDARSCHEM |

529.63 |

524.45 |

27 |

10% |

-0.98% |

0 |

| UJJIVANSFB |

46.99 |

49.75 |

250 |

9% |

5.87% |

2 |

| SWSOLAR |

395.43 |

396.8 |

25 |

7% |

0.35% |

1 |

| DODLA |

763.36 |

741.4 |

10 |

6% |

-2.88% |

3 |

| IBULHSGFIN |

152.58 |

163.9 |

3 |

0% |

7.42% |

3 |

Added Gujarat Fluorochem

All credits to the FORUM :

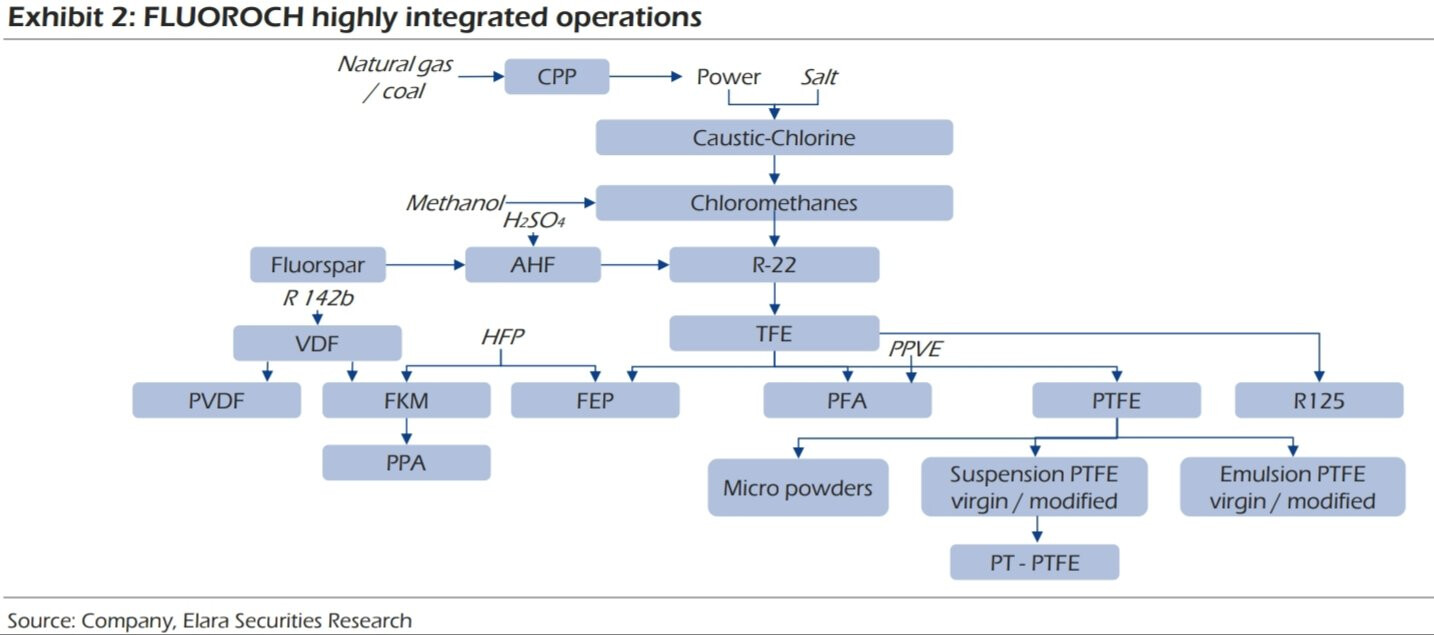

• Fluoropolymers are majorly used in very specialized applications which require non adhesive, low friction properties along with extreme heat, corrosion resistance, difficult weather and harsh chemical conditions. FP finds usage in automotive, aerospace, semiconductors, electronics, common household appliances. FPs because of their physical properties are also expected to find increasing usage in EV batteries and 5G where thermal requirements are significantly stringent.

• Fluorospeciality chemicals {FSC) are intermediates used in agrochemical and pharmaceutical industries. Company has commercialized seven molecules and is looking to add more. This segment has large growth opportunities and is a proxy to the growth of pharma, agro chem, electronic and polymer industries. Further, it is planning to incur capex for additional six products and has guided for its commissioning by end FY21. There is also a strategic need of both domestic and overseas customers to de risk from China.

• Refrigerant gases are no longer the focus area for FLUOROCHEM. FLUOROCHEM today majorly manufactures R22 as feedstock for FP. It still continues to sell R22 in retail and also as feedstock to agchem/pharma companies.

• Chloromethanes consists of three products Chloroform, Methylene Dichloride (MDC), Carbon Tetrachloride (CTC), as of now Fluorochem is the only producer of of MDC and CTC in India.

• Caustic Soda : Chloromethanes and caustic soda are in some ways a by product since the entire process of manufacturing FSC/FSP/Refrigerant gases requires significant amounts of Caustic/Chlorine/Chloromethanes. In the rest of the discussion, we will be majorly focusing on FPs and SFCs.

NEW AGE FLUOROPOLYMERS

• Battery chemicals

• Fluoropolymers

• Refrigerant Gas

Battery Chemicals

- LIPSF6 (Lithium Hexafluorophosphate)

- LiFSI

- LiFePO 4 battery (lithium iron phosphate battery)

or LFP (lithium ferro phosphate)

- Electrolytes

- NAF

- Phosphorous Pentasulfide

- PEM (Proton Exchange Membrane)

FLUOROCHEM

- PVDF

- FKM (Fluor elastomers)

- PFA

- FEP

- PTFE

- FLUOROPOLYMER ADDITIVES

REFRIGERANT

FLOUROPOLYMERS USES/APPLICATION

- TRANSPORT

- TELECOMMUNICATION

- SEMI CONDUCTOR

- ELECTRONICS

- RENEWABLE ENERGY

- MEDICAL

- CHEMICAL PROCESSING

- ELECTRICAL APPLIANCES

CAPEX/GROWTH

25 Billion capex for 2 years and 45-50 Billion capex for 3 years (primarily towards battery and PVDF) funded through internal accruals

BATTERIES SECTION :

- LiPF6

- PVDF

- Electronic Grade Anhydrous HF

• PVDF binders for Li- Battery Electrodes – Commercially available

• Indigenous Manufacture of Lithium Hexafluorophosphate LiPF6 required as Electrolyte component in Lithium ion Batteries.

• Manufacture and supply, initially by 2023, customized LiPF6 based Electrolyte formulations as per Customer’s recipe from our state of the art formulation facility, and eventually develop our own proprietary electrolyte formulations as performance products.

• Lithium batteries demand long-term reliability as well as chemical and electrochemical resistance in the specific chemical environment of Lion cells

• PVDF is electrochemically stable in the full range of voltage between 0 and 5 V vs Li+/Li

• PVDF is stable at high temperatures

• Compatible with most cell chemistries – NMC, LFP, LCO etc.

• Excellent solubility in polar solvents like NMP

• GFL has Plan under implementation to set up a scalable plant to produce 1000 TPA Electrolyte grade LiPF6 by end 2022 at Dahej, Gujarat.

• The plant will be scalable to expand to 2000 TPA by end 2024 and further to 4000 TPA if need be.

• GFL has been in Fluorine Chemistry for past three decades and has Technology for making Electronic Grade Anhydrous HF (AHF). Electronic Grade LiF will be made in-house starting from Li2CO3 /LiOH

• A State of the art facility to manufacture about 6000 TPA Electrolyte formulation will be set up in the year 2023 which will enable us to service our Customers with customized formulations as per their needs. This will be fully equipped with Testing facility for stringent Quality Control

New age industry vertical

EV – Expect to commence operations by September 2022

• Products – PVDF electrode binders, battery chemicals, LiPF6, additives, electrolyte formulations, battery casing

• Setting up an integrated battery chemicals complex

• Developed suitable PVDF grades for cathode binder application

Only manufacturer of LiPF6 as of now in India

• Lithium carbonate, phosphorus pentachloride – To make eventually

• Solvents – will be buying initially

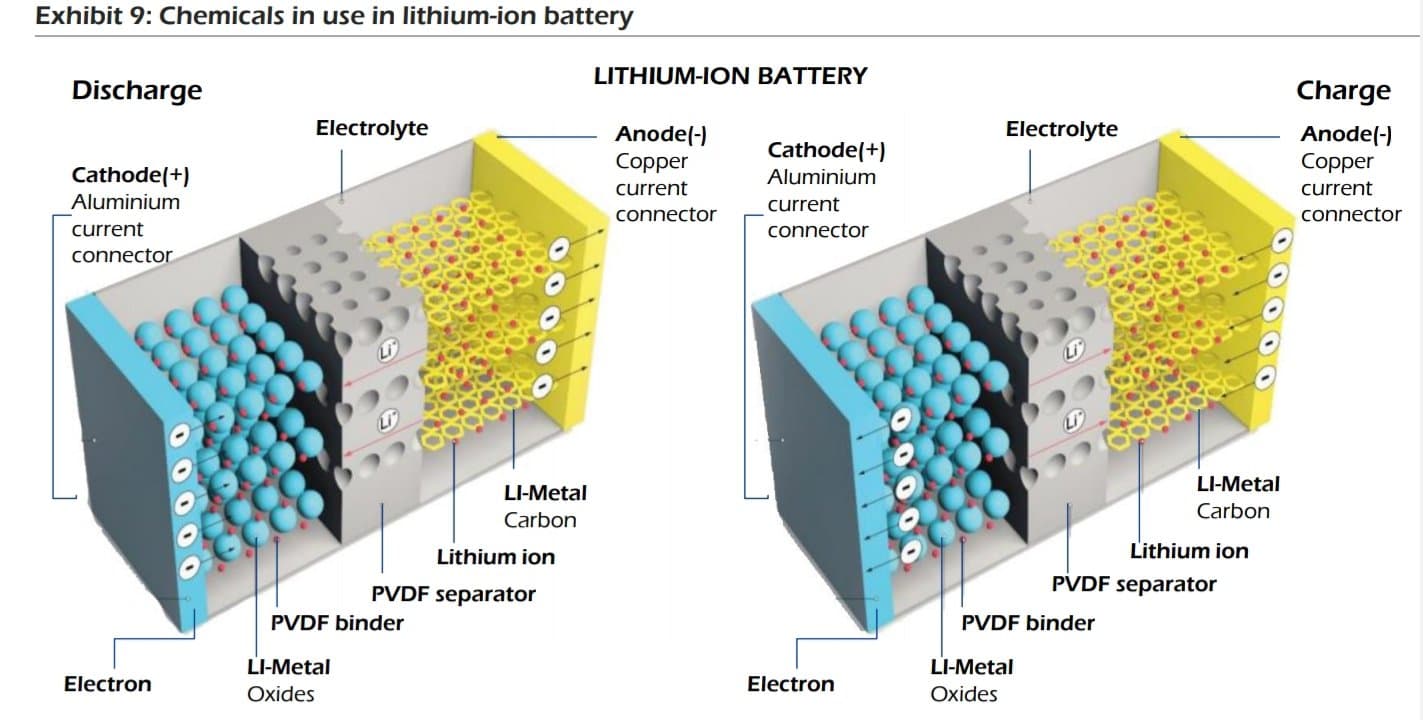

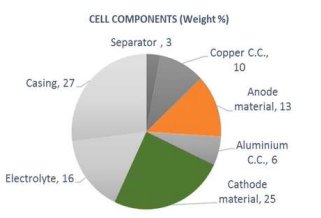

Key components of cell:

Anode

Separator

Electrolyte : It is a mixture of lithium salt in an organic solution. The salt used is LiPF6 .

Cathode

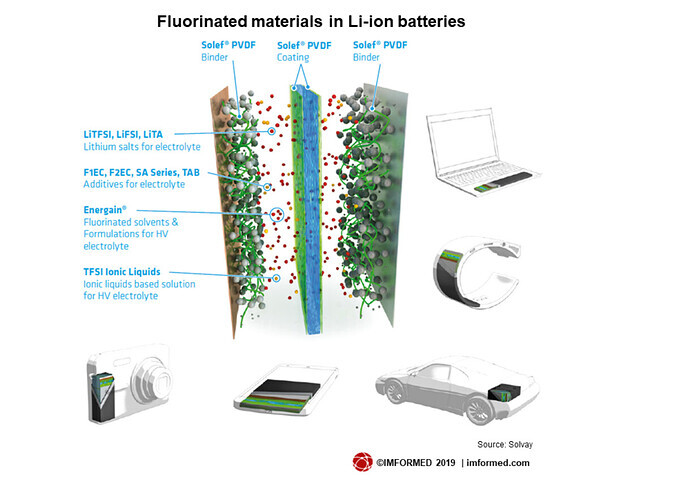

Usage of fluorinated materials in LI-ion batteries:

RENEWABLE ENERGY

Solar panels – PVDF film plant to be commissioned in FY23

• Products – PVDF film, Back-sheet

• PVDF film – Project expected to be commissioned in FY23, to cater to both domestic and international markets, backward integrated for PVDF

Hydrogen fuel cells/ electrolysers

• Products – Fluoropolymers (FKM, PTFE, FEP), Membranes, Charging Accessories

• Fluoropolymers are integral to the functioning of Electrolysers

• Fluoropolymer based proton exchange membranes (PEM) form the heart of fuel cells and electrolysers

• GFL with its portfolio of major Fluoropolymers is well equipped to cater to the Fluoropolymers required for the hydrogen electrolysers, fuel cells and charging stations

• Proton exchange membrane (PEM) – Taken up R&D to develop indigenous technology, to take 2 years

PVDF is needed in solar cell backsheet

It is needed for UV protection, extreme weathers and paint retention etc.

More the Fluorine content in PVDF, better are the results. Arkema claims 59% F content in their PVDF and hence superiority. We need to ask this question to management.

Better the backsheet, lower the maintenance and higher the RoI. So as solar industry matures in India and worldwide, PVDF film will continue to remain a critical component.

Very first thing is that PVDF is used in the EV battery electrode (PVDF binder) and also in separator coatings. GFL IESA presentation talks about only binder part and not coating part. Most likely, GFL would also have separator coating as well - but better to get this clarified from management.

All credits to the FORUM MEMBERS : https://forum.valuepickr.com/t/gujarat-fluorochemicals-a-hidden-fluorine-story/

PFA

PFA can be formed by conventional injection moulding or screw extrusion.

PFA can be molten

Advantages of PFA

• Because PFA can be injection moulded, more complex shapes can be made. This results in better Cv values in flowmeter bodies or the bodies for regulators for example.

• Because it is heat deformable it can be applied more easily as a liner.

• PFA can be heat welded. This property is used in flare and in bond fittings. Both flare and bond fitting provide a leak tight connection with minimal dead volume.

• Oleophobic (it drips off after contact with an oily liquid).

• Hydrophobic (in contact with water or a solution in water, this drips off easily. FPA stays cleaner, which makes cleaning of liquid systems easier).

• More transparent than PTFE and PVDF.

Disadvantages of PFA

• More expensive than PTFE and PVDF

• Absorbs more water

• Less resistant to repeated mechanical strain

• Lower maximum allowable temperature

Typical applications of PFA

• Laboratories, because of the chemical resistance and because of the good transparency of hoses.

• Long piping.

• Gas and liquid cabinets, especially with Ultra Pure Water and corrosive chemicals.

• Coating of chemical equipment, such as thermocouples, heating elements, height sensors and the inside of reactor vessels.

Because PFA can be processed via the injection molding technique, it is relevant to compare PFA to another fluoropolymer that can do the same: PVDF.

PVDF

PVDF is a commonly used plastic in systems. It has much better chemical resistance than many other plastics and is 30% cheaper than PFA.

This makes it a formidable competitor to PFA. In short, PFA is preferred over PVDF in applications where PVDF is not chemically resistant enough and when transparency is important.

Advantages of PVDF

• Cheaper than PFA (about 30%)

Disadvantages of PVDF

• Not transparent.

• Can discolor under the influence of certain chemicals.

• Not as chemically inert as PFA and PTFE.

• Smaller temperature range, especially less suitable for cold applications.

FKM : Doing more research !!

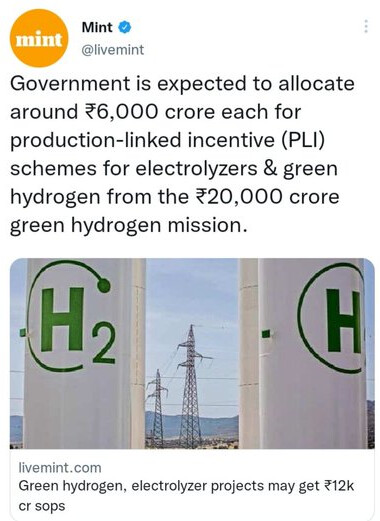

Govt to Allocate around Rs.6000 crs to each for PLI Scheme for ELECTROLYZERS & GREEN HYDROGEN

PROXY Companies like : GUJARAT FLUOROCHEMICALS(GFL) would be benefitting this

GFL’s FLUOROPOLYMER Products(FKM,PTFE,FEP,PEM) are used in ELECTROLYZERS & HYDROGEN FUEL CELLS

Hydrogen can be made by following ways :

- BIOMASS such as producing Methane and then catalyzing it

- PRAJ : Team is researching for hydrogen & more into bio space : they have partnership with multiple international client to build hydogen facilities and they are conceptualizing within internal R&D team

Shishir Joshipura, CEO & MD of Praj Industries Explores New Possibilities in Green Hydrogen : Shishir Joshipura, CEO & MD of Praj Industries Explores New Possibilities in Green Hydrogen - YouTube

- WATER ELECTROLYSIS : This needs electricity either Fossil Fuels or Renewables + this needs Polymers such as (FKM,PTFE,FEP,PEM)

- RELIANCE via Fossil Fuels

- ADANI

- GUJARAT FLUOROCHEM (PROXY)

- HEG/GRAPHITE (COMMODITY)

- DMCC (Company is doing R&D on boron compounds, which can store hydrogen)