Virender Jeet have mentioned in the concall (as in the prev threads). They are pursuing for higher ticket size as they will help the company to grow faster with meaningful client additions.

1 Like

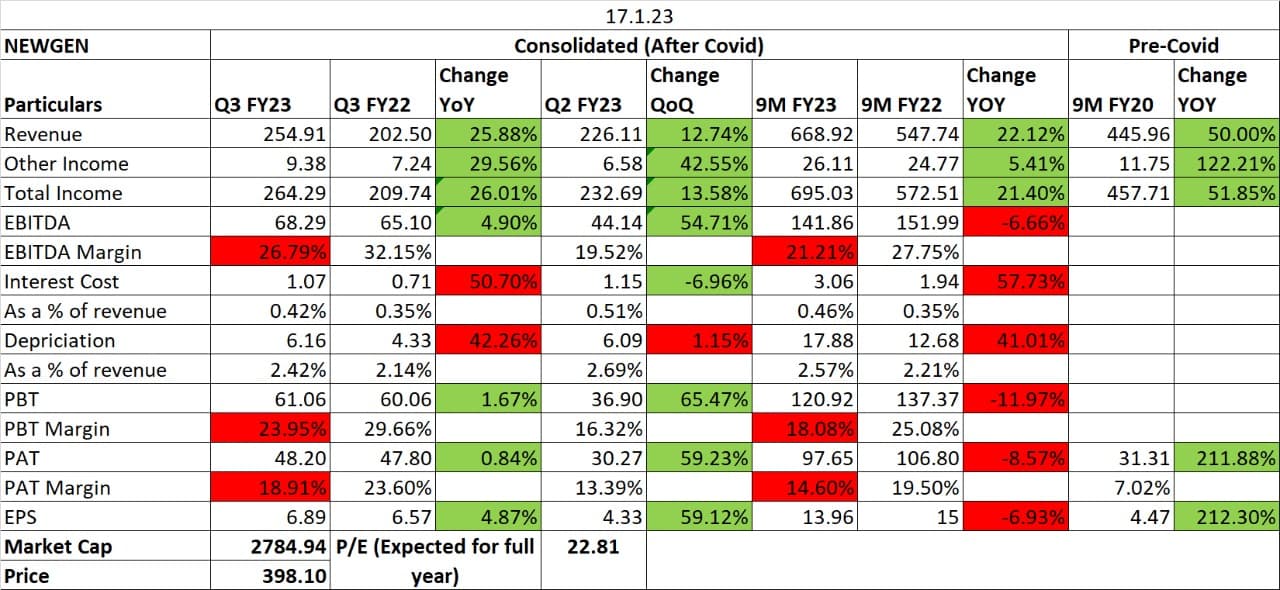

Q3- 22/23 Results out.

Revenue - 16% YoY growth.

1 Like

Unless traction in US picks up, growth can slow down going ahead, nos have held up so far due to India, Emea & inherent annuity business aiding. Ex-US geographies itself management has been clear, cannot sustainbly grow in size from wins in these geographies, already existing material Mx. I like the management but this is something that will be hard and needs to be shown in execution.

Entry multiples are seemingly very cheap today, however contingent on good growth playing out which has become unclear over past few qs due to lack of traction in US.

2 Likes

Concall summary

1 Like

In Q1 it was guided better margins through revenue enhancement and cost optimization. There is revenue enhancement but margins haven’t improved at all which is causing an effect on profitability.

-

In Q1, they guided that it has strong pipeline & the deals signed in Q4FY22 & Q1FY23 will lead to revenue up tick from Q2 onwards. The company has maintained 20%+ revenue growth guidance for FY23 & also indicated that GSI related revenues will be an incremental revenue opportunity. Revenue has increased until Q3 FY23. Revenue growth guidance has also been maintained. GSI related revenues to increase is still in the guidance with focus on mature markets USA and Australian subsidiary.

-

In Q1, they guided that Employee expenses and travel costs will continue to increase in Q2 and should decline in Q3 & Q4 but they still continue to be on the upward trajectory. The company indicated that in the short terms, operating costs are likely to see some upward trajectory on travel costs normalisation as customer meetings are critical for the growth as well as sales & marketing costs.

-

20% growth for next year has been guided. Margins around 21%. Margins are around this level at the current stage in Q3 FY23. The company continued to aim to reach US$500 mn revenues in the next five to six years, which includes GSI contribution as well inorganic contribution

-

Q4 is seasonally strong quarter and are seeing that attrition has fairly stabilized.

-

Once, mature markets start contributing to revenue, margin expansion will happen. (Same as Q1 guidance).

-

Guiding margins at 22-23% EBITDA and 17-18% at PAT level.

-

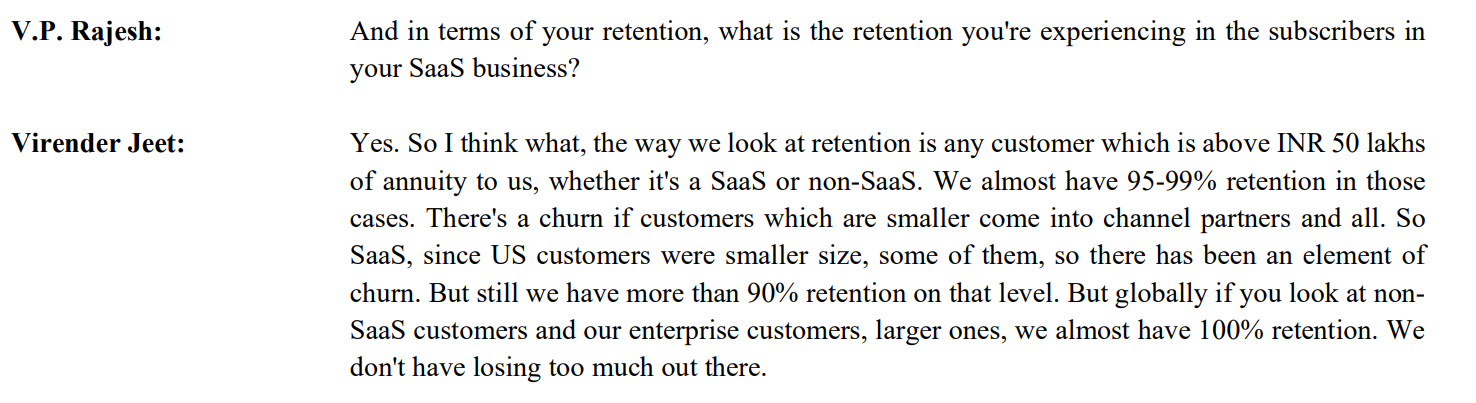

Logo wins have been subdued. But they are gaining traction in subscription revenue which should help in better consistent revenues.

-

They are targeting 10 deals per year from GSI region. The company also indicated that due to its strong customer relationships in the market, growth was likely to sustain, going forward.

-

The Trade Finance Platform has been gaining traction as the deal size is huge.

4 Likes

I have a question on the customer churn.

In FY18, the company reported 520 active customers (defined as the customers which are billed in last 12 months). The company has continuously added 40-50 new logos every year since then. Why, then in Q3FY23, the company reports only 530 active customers?

If the customer base is sticky, why is the logo addition not reflecting in active customer numbers? Does this mean that older customers are no longer invoiced after sale and implementation? The normal practice I have seen is that the enterprise customers do enter into AMC/support contract with the product supplier after implementation for ongoing technical support/product support issues etc. So they should be invoiced at least once a year as per my basic understanding.

If the older customers do not contribute to the revenue, wouldn’t this become a treadmill situation where the company needs to keep acquiring new customers every year in order to keep growing the topline?

What am I missing?

2 Likes

Anand, this is the important question. I have been growing sceptical on this aspect in the last year.

This is the only reason my allocation has not increased.

I wrote to IR asking them about it a year ago and I got some vague answer.

I did not have the energy to chase it.

Newgen can take off if their churn came down close to zero.

Disc: invested from lower levels.

1 Like

While I have recently started studying the co, the answer might lie in their strategy when they said that they were consciously cutting long tail of customers where cost of acquisition did not justify the sales output. These customers were not giving them repeat business.

3 Likes

Q1 FY’24

Revenues: INR 252 crores, up 34%

Growth lead by :

-

APAC : 46%

-

EMEA : 38%

-

U.S : 36%

-

India : 25%

-

Seasonality factor decreased by increasing Annuity revenues

-

Annuity revenues: INR168 crores, comprising 35% of total revenue.

-

License revenue grew 1.9 times compared to Q1 last year.

Customer Growth:

- Added 13 new logos across geographies in Q1.

- Digital account opening solution to

- Privately held bank is Americas region

- Lending origination and management solution to

- Leading diversified business group in Saudi Arabia

- Trade and Supply Chain Finance Solution to

- Leading financial institution in the UAE market

- 35 crores 5-year deal

- 1 of the Indian public sector banks for new offering in Trade Finance : The project execution immediate

- Large part of this revenue will come in the next 18 months, part of this revenue, which will follow up ATS/AMC

- Expanded opportunities in banking, insurance, and government segments.

- Execution of the deals will start from Q2,2024.

Product

- Platform :

- Modular design

-

Advanced AI capability

- Adding AI/ML capabilities in process automation for suggestive and prescriptive intelligence

- Lending solutions with the AI/ML based auto decisioning and no touch, low-touch strategy

- Recently launched trade finance solution, we are again using our AI-based strategy for extracting data from paper images and PDF docs.

- Exploring the use of generative AI in products and solutions.

- Plans to launch several products in the generative AI area.

- Generative AI road map for the next 12 months

-

Cloud-first approach

- All these platform will enable organization to deliver superior customer experience, operational excellence and business innovation

-

Newgen ONE

- Newgen ONE : This tools helps to build, deploy and manage applications, building automation silos and streamlining the processes.

- It allows development of attractive portals with very little effort, facilitate end-to-end integrated processes at enterprise scale

- Produces better applications using low code principles

Strategic partners

- GSI : Global System Integrators

- Consulting firms

- Technology partners for enhancing capabilities and largely marketplace partners like Mambu and Guidewire

License Sales : There’s a kind of a pushback from market from traditional subscription and SaaS sales but the current reality what’s happening is that the perpetual license business for past 3 quarter are being strong.

-

Perpetual

- Expect substantial level of perpetual licenses again in this year

-

Annuity

- This business is close to about 55-60% of the revenue - going ahead this will expand up to 70%

- The revenues are deferred

- Perpetual deals coming in, and they were coming across all territories, including U.S.

- This year to be very strong on licenses

-

Subscription

- U.S. sales are subscription-based sales

- Expect substantial level of subscription licenses this year

Newgen strong foot holds

- BFSI : U.S. regional banking sector facing cost pressures but still demand for Newgen’s products.

- Tier-1 Banking doing extremely well in India, Middle East, APAC

- Growth led mostly by

□ Onboarding people to the bank

□ Lending money to the bank - Midsized banks : particularly a smaller end of the midsized banks are struggling

- Trade finance a focus area with potential deals in India and the Middle East.

- Insurance sector also strong

Attrition/Employee Cost

- Significant decrease in attrition rate compared to the previous year.

- Increment cycles are divided across 3 quarters. April, June and predominantly January.

Investments:

- Heavy investment in technology and sales and marketing initiatives.

- Maintaining cost discipline.

- Other expenses increased to INR75 crores, primarily due to marketing and sales initiatives.

Cash Flow:

- Net cash generated from operating activities: INR 57 crores.

Margins:

- Expecting healthy margins with EBITDA around 20%

- PAT around 17-18%.

15 Likes

I have been holding Newgen since an year or so. From my understanding, the promoters gave a guidance of doubling revenue in 3-4 years. It was doing well at the PE of 20-25, what could be the reason behind recent re-rating? Has the guidance for revenue and margins been updated? The last qrtr result was also at par, nothing out of ordinary.

1 Like

Nothing extraordinary has happened, these are markets, they punish sometimes on extreme downside and sometimes there is such euphoria on upside and it starts looking absurd. It was at 15 PE once now near 40 without much change in fundamentals. Disc: Invested and looking carefully on signs of euphoria ending.

5 Likes

quite confused should I book profit now. Invested at elevated level. Nearly 40 percent gain made. felling like double edge sword , if i book the profit will the long term opportunity will be missed.what is ur opinion in this type of situation?

1 Like

Book 20 percent and keep balance for very long time(10 years plus). Story is perfect and will have its bumps in between to keep adjusting your sold 20 percent position

1 Like

Newgen reported excellent results.

Revenues at Rs 293 cr in Q2 FY’24, up 30% Q2 YoY; Profit after Tax at Rs 48 cr, up 59% Q2 YoY

New logo addition:14

Revenue and margin expansion, was well received by market today.

To take decision of booking profits on P/E is tricky. Growth may continue for coming time also. Best time to sell growth stock is when growth slowdown.

Disclosure: Invested

6 Likes

Another 5% today, has anyone gone through the concall? What is the guideline from Management? How long till the price tips over to over expensive category?

Holding from 400 levels, small investment.

No buy/sell in last 3 months

3 Likes

Management is optimistic for H2 and market is pushing stock prices based on this and latest bonus investment. If results come as per management concall than markets may continue to re rating the stock as market is always forward looking.

I am also invested significantly from lower levels and booked 20 percent profits around 900 levels.

I have kept the balance fr long term as I am convinced with long term story and I don’t have any other investment options in equity.

1 Like

The management is confident about Newgen’s Marvin platform helping the hyper-personalization of customers. As per the latest updates the company stated that customers expect personalization and uniqueness for their banking needs. NewgenOne Marvin is a Gen AI platform focused on customer experience, operational efficiency & business innovation.

I feel that it may further re-rate up to the level of 1600, due to the following facts of Newgen Banking AI, NewgenOne Data Science platform, some of the wins in the past.

6 Likes