Can someone guide why Q4 is their seasonally best quarter ?

5d684d98-57af-42a2-9dc7-07f8dcef906c.pdf (5.6 MB)

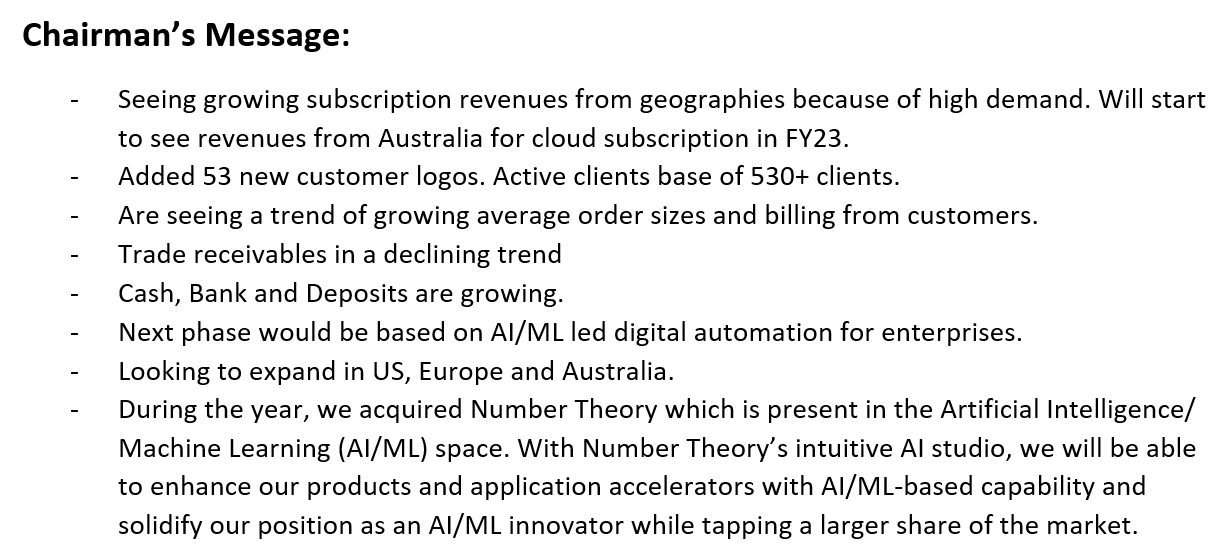

Q4 results uploaded and are seasonally their best quarter this year too. More info in tomorrow concall at 11.00am

Newgen’s results more or less as expected. Further thrust on subscription and SaaS revenues from EMEA/US/APAC (outside India) markets in the coming years is a key monitorable. As per concall, GSI partnership seems to be working well too, though it would have been nice for the company to include a slide with numbers - similar to last year.

40% attrition is huge. However, this is an industry wide issue.

Newgen Investor Presentation Q4 FY22 FINAL.pdf (2.3 MB)

As per Q4 FY22 results & full FY22 results,

The good parts are

- More than 20% growth in subscription revenue.

- Growth in Middle East market & entering into Australian market

- Gross margin of 70% in subscription segment

- Guidance for PAT margin in the range of 18%-19% going forward

The negative parts are

- Abnormal attention of 40% which is quite high despite it is industry wide trend. Subsequently, order backlog is also there which is possible due to attrition

- Despite employee cost went up, unable to mitigate the attrition

- Unable to grow much in US markets

Don’t you all think the performance in the USA large cap market is a little underwhelming? I think that will be the only market that would give this company an exponential growth and the management seems to be shy of reporting any numbers on development in that market.

Valid question but given the size of the company and the impact of Corona and also its recent tie ups with GSI, can give 4-6 qtrs for the company to prove its mettle. Note that Indian companies are still on the path to be recognigized as good software “product” vendors. The entire industry over the last few decades has largely been a services play. However, Newgen being a horizontal Saas player, I would expect the company to show further increase in topline.

Came across this interview of the CEO on CNBC talking about scaling revenues to 500 million dollars in 5 years which would be more than 5x of the current revenues.

Has the management laid out any plans or strategy around it, or is it just an ambition as of now?

Looking for more details/ discussions around it from the concall/AR.

[mgmt talking about it around 5:40]

Nasscom insights tech talk highlights tremendous opportunity and high growth in low code/ no code platform and rates Newgen as global leader.

After the recent correction, at current prices entry valuations look much more reasonable in context of potential growth outlook. Disclosure: invested.

• Into mission critical software, increasingly less discretionary & more essential spending. High value obtained by enterprises relative to price paid to vendors. Higher lock in potential, once adopted. Clearly this space has grown strongly over past 5-6 years and is expected to continue as penetration rates are so far not high.

Appian:

“Low code had been there. And – but pandemic has really act as a catalyst and increased the urge of companies and our customers to go digital, but it showed us data has to be in cloud. We needed a unified platform, and we all had to work from a workplace remote as well as get the work done with minimum workforce. So all this together kind of act as a catalyst. And we are seeing an increased demand in the last few years.

Pegasystems:

“2016 was the year I think we were $25 million or $30 million. We’re now over $300 million of revenue, right? had very consistent and steady growth at around 20% for the last 5 years. Our growth rate before we move to the transition was kind of somewhere in the low teens, kind of in the 12% to 15% range. we put a lot of investment in the business over the last couple of years to see if we could push that up higher, push that to 25%, push that to 30%.”

“When I started at Pega, we were – as many of you are aware, we were a largely perpetual business, not exclusively a perpetual business. We did have some term contracts. We also did have, I would say, a kind of a smaller Pega Cloud business. It was – it was somewhere in the $25 million range of ACV at that time. We did not talk about ARR or ACV at that time. It wasn’t that we thought it was unimportant, it’s just – the market was a little different 6 years ago, 10 years ago. And we made a really big kind of shift in the 2017 time frame. And that shift was to move to a subscription business. we have this almost crazy large opportunity for Pega compared to our size, right? We – if you just look at the companies that we’re competing with in their size, we’re in those markets, right? Huge market, as I said. I kind of look at this and I almost say, is it 50? Is it 65? Is it 100? Is it 150? It kind of doesn’t matter, right? It’s so big compared to us being a $1 billion-plus company that the opportunity is huge.”

• Large opportunity to mine customers once through the door, execution is key. Leaders like appian, pegasystems, box highlight opportunity & success they are currently seeing & demonstrating in gaining a larger share of the client wallet. While growth in no of active customers is relatively muted for newgen, they have seen decent traction in upselling so far. Bodes well for high Roce & lower cac over time. Successfully getting into the door is critical.

Appian:

“So we have overall price raises. We have triggers on heavy usage for any of those nominally free components. So those will be the primary ways. But we’re also using the leverage we get from the other components in the suite to upsize the existing customers that we have sold.”

“So our other lever doesn’t have anything to do with raising prices. It has to do with discovering business and sparking new demand. Process mining, in particular, is great for that. But also just to be able to say, if you’ve got a system, why don’t you add our RPA instead of someone else’s. It’s more convenient, right? It’s already compatible. It will upgrade together. I think we have a footprint expansion plan even as we have a price increase plan. And we continue to see strong pricing power, and we watch for that.”

“if you never added another logo, what’s the revenue runway within the current installed base? Like what’s the current penetration of revenue you think within the current installed base? actually think we have a fantastic runway ahead of us, even if we never added a new logo. But the real beauty of our position is we’re going to add new logos. one of my favorite things about this business that we generate so much value. With each application that we put down, the customers are delighted. The usage is – grows faster than revenue growth and that’s – it’s our challenge is just to monetize all the value we’re creating.

I take care not to offer true enterprise licenses for this reason because the value we can create keeps going up. With every new application, with every new user, there’s always more you can do with this platform. So I’m reluctant to sell the future at today’s prices when it comes to usage licenses. So could we grow, if we didn’t add new logos? Yes, we could. Would probably pretty well, too.”

Pegasystems:

“we are very, very focused on driving 75% of our growth from clients that we’ve already got. a large percentage of our growth actually comes from existing clients, that is a lower – it should be a lower cost of sale than actually selling to new logos. So if you’re selling – the majority of cost in an enterprise is to get your foot in the door, to get the organization. we’ve struggled with efficiency in our go-to market. you’ll see us kind of shifting to really focus on where we know we can really kill it, which is with large organizations that understand our value that largely, we’ve done business with in the past. ”

“have an enormous amount of white space in our customers. if you looked at our top 20, 25 customers and asked how thoroughly penetrated we were in those, you would conclude that we were under 25% down trade. We could grow easily several hundred percent without adding a single logo. We have about 800 logos, ballpark 800 clients. Less than 200 of those spend $1 million with us. And many of them could spend $20 million, $25 million, $30 million with us. Some of them can spend $100 million or more with us. Just – if you just do the math, like it works out that you probably have years and years of actually booking potential for us, like more than 5 years, maybe 5 years, right, of runway to be able to just grow those 800 logos.”

• US: recent efforts made to increase share yet to play out materially in revenues. Caveat here is in the past, we have seen smaller IT cos struggle for an extended period of time into scaling up revenues from developed countries. It’s a large growing market but also a highly competitive one. Perhaps they are unsuccessful and ramp up is slower. They have a growing market & a relatively smaller scale/base on their side. While players like newgen, appian, pegasystems are focused, niche low code, bpm players over the past 2 decades, it’s only in the past 5-6 years this space picked up strongly in growth rates & into the mainstream. Many vendors already exist, and more & more software cos over the past couple of years now talk of low code and are building/looking/acquiring for capabilities. Enterprises consolidating their IT vendors from say 10-12-14 to a handful who can deliver a single unified comprehensive platform, means there is always a risk of niche esp smaller guys losing out more incrementally. Management commentary but not nos so far have been strong, hopefully they deliver in the times ahead.

Appian:

“So the question I had is low code 4 years ago was only a term kind of you guys Now, everybody uses it. [indiscernible] talks about it. Smartsheet talks about it. ServiceNow has something and then they do process mining with. [ Salona’s ] obviously, Microsoft has something and I can’t, so every software company that they [indiscernible] low code.”

“at 2020 and you say, well, that’s the year that low-code took off, low-code is a thing right now, it’s a thing in mission-critical applications”

“Though the interpretation of the definition of low-code is still an issue, and different vendors may call themselves low-code but really represent very different products. We believe in low-code for mission-critical applications. That’s more difficult, it’s more valuable. So our traditional long-term competitors, Pegasystems, we’ve been competing with them for more than a decade. And so we still see them more frequently than any of the other companies that you mentioned in our competitions. However, there have been new groupings that come up recently, right? And so we see Mendix, Outsystems and Microsoft as one grouping and ServiceNow and Salesforce is another grouping. And each one of these has something to offer, for sure.”

Pegasystems:

“funny because low-code as a term has sort of caught on now. The low-code space, it’s full of lots of companies. I would say that a lot of the competition about what I would describe as the kind of very low end, is not actually, I don’t believe, going to compete with what our core value prop is, which is to be able to help organizations that are working with mobile product lines, multiple types of customers, multiple geographies”

• Newgen has been relatively quiet when it comes to acqs & instead prefers to build capabilities organically. 1 key selling point to enterprises is having a common unified platform, some acqs can get hard to integrate into one’s existing platform. Acquisitions have been rampant across competitors as they have looked to fill missing spaces.

Appian:

“low-code automation cannot be solved by one piece of technology. There are multiple components which needed to come together, business, low-code platform, RPA, AI. And what are customers is kind of expecting from a partner like us and all of us sitting here is kind of being the advocate to select the platform.”

“And we find ourselves in competition with them based on certain types of customers, generally, customers who are a little bit less feature-sensitive, right, who don’t demand quite as much in terms of security or scalability or power. Many of these products are really stuck at the low end, however, of the market and unable to move up. So some of them, for example, don’t have testing or can’t connect to external databases, or that sort of thing. They’re more of a developer tool really than a low-code product. Others claim to be low-code, but they’re really pretty code-intensive. They’re forcing you to do a lot of JavaScript development or APEX development or something like that. So there isn’t a good straight ahead rival for what we offer today in this market, lot of big names, lot of great marketing, and a lot of popularization going on of low-code, which we appreciate very much, but we don’t have a direct rival who shares our virtues.”

“create a fleet of functionality as a single stop end-to-end process manufacturing factory, without having to buy any product, without having to go to all the headache of multiple pieces, the way to do this would have been to buy 1 product for process mining, another one for workflow and a third one for RPA and maybe a fourth for AI and perhaps one for document processing and get your business rules somewhere, stitch this all together and try to make a functional product, it’s because of all these parts because it’s too complicated. This is the turning point of the year for us but I think it’s the turning point of multiple years for our industry as well. I think that our – we’ve taken a turn now that our competitors are going to have to follow, So there’s recognition, these components belong together, but having a partnership is not the same as having them as a single SKU, a single contract, a single support line. And so I don’t believe our industry is yet taking this is serious. We have taken it serious we’re going to make them”

Pegasystems:

“It’s the single architecture that we’ve been evolving for years. we talk about low-code. And there are lots of companies that talk about low-code, and they had different focus and they had different set of functionalities. Over the years, you’ve seen lots of different process mining companies we’ve acquired. We wanted to make sure that there was a technology that we can actually unify the architectures that fits into our offering that is not going to be a separate product, a separate solution.”

• Margin expansion potential: Across the space, cos are getting a larger chunk of revenue growth through Sis, hence lower implementation & higher subscription revenues. This does take away a chunk of revenue opportunity away from cos, but necessary to get end traction from enterprises for which Sis already have entry points, so margins naturally are poised to go up as mix shifts to higher margin subscription sales over time. Upselling resulting in higher client wallet share aids margins.

Appian:

“services will continue to shrink as a percentage of Appian’s revenue, and yes, it’s going down to the 20s. And I think that every year, it’s going to be smaller than the year it was before, toward because we want to elevate partners and leverage their influence in major customers.”

“continue to feel that pricing in our industry is both confusing and inefficient and so improvements on pricing models are possible.”

“I’m just curious how you’re thinking about the potential pricing lever over the next few years? We’ve got a lot of ways to capture higher prices, but that is our intention. As we add pieces to our suite, we raise the suite price. Now we do that while saying that RPA is free and process mining is free, but only a nominal amount of it is actually free. And if a customer becomes a serious user, one of those functionalities, also IDP, also portals, any one of those trigger cost increases, if they use it in a substantial manner.”

Pegasystems:

“Consulting revenue it is as a percentage of overall revenue slowly and very intentionally shrinking. approaching 70% gross margin. 70% is not the end point. We’ve talked about getting to 75%.”

• Many of the larger dominant guys who are materially bigger than newgen have been posting losses since many years, unlike newgen who is very profitable. Heavy equity funding led amidst strong growth seen. Recent quarter’s commentary suggests that onus is now shifting to profitability, guiding to lower S&M costs, higher operating margins, and lower burn.

Pegasystems:

“Is there a change in the thinking going to this a little bit, maybe slower economic environment to shift more towards profitability? the timing looks like that was tied to maybe inflation and so it really wasn’t. We had a little bit over invested in go-to-market and weren’t getting the higher growth from it in the face of what would be a harder economic climate to accelerate growth than what it was a year ago. So the combination of those things really kind of made me realize that I need to be very, very disciplined. this is the time to now see our profitability. This is not the right time for us to go running into brand-new markets or running down market or other types of things, which you might do if, in fact, a rising tide was raising all ships.”

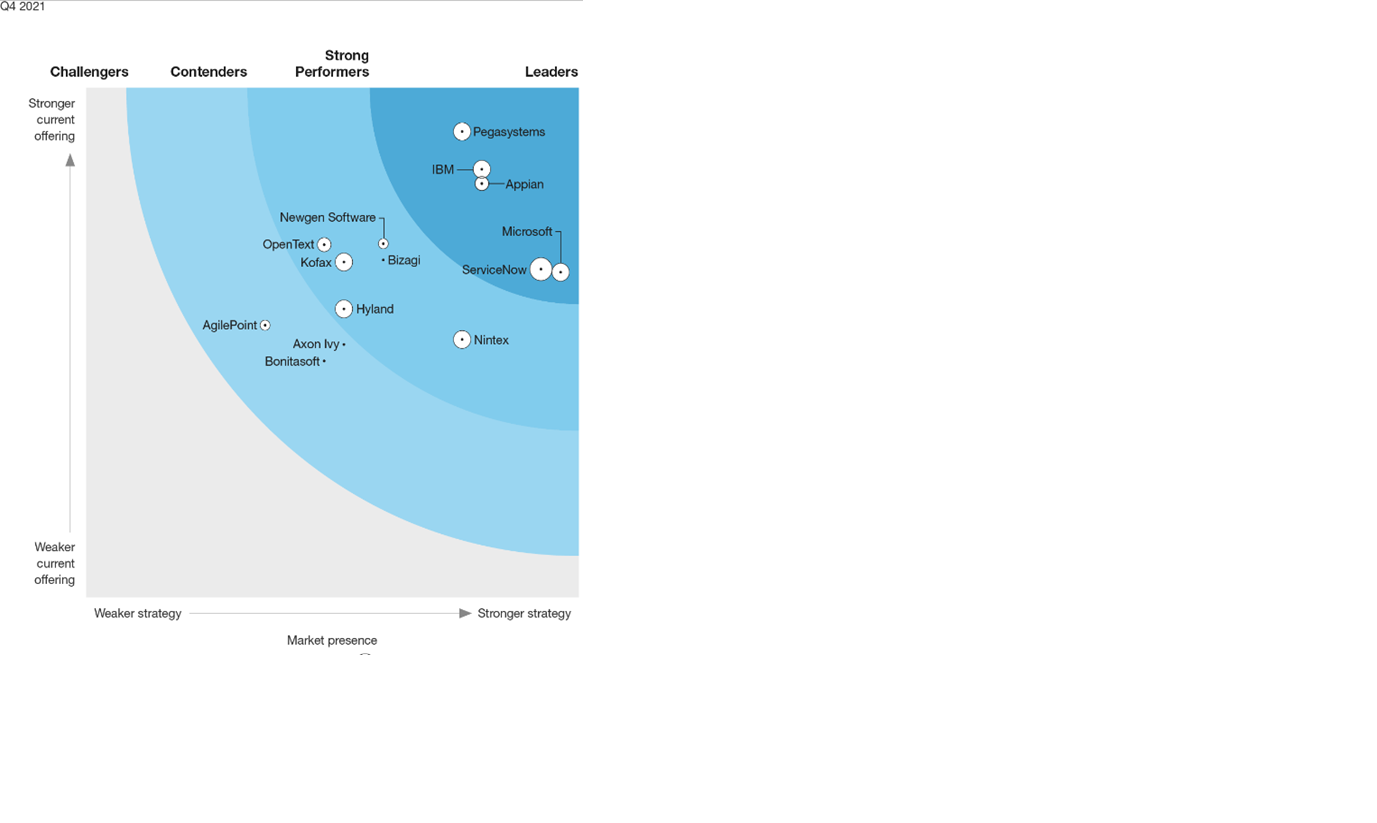

• Gartner, forrester ratings: got included in Gartner magic quadrant for enterprise low code application platform for first time in 2020.

Gartner magic quadrant for Content services platforms: 2017 niche, 2018 challenger, 2019 challenger, 2021 visionary.

Gartner magic quadrant for enterprise low code application platform: 2020 niche, 2021 niche

Gartner magic quadrant for Intelligent Business Process Management suites/Business Process Automation Tools Market: 2017 visionary, 2019 niche, 2021 niche

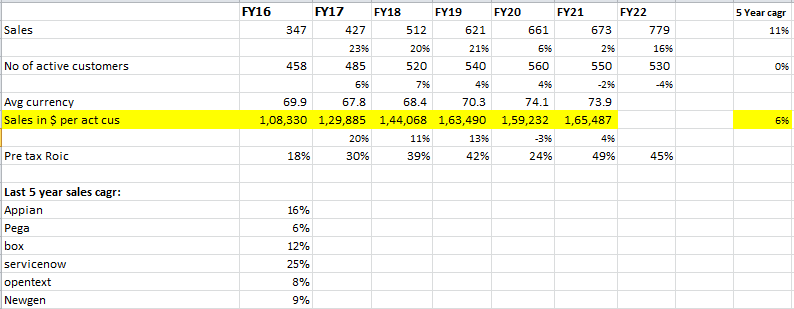

Overall there is opportunity, however lot of things can go wrong in execution too. Management seems decent. Margin benefit of last 2 years from low travel cost will fade away. Broadly, at current price it’s at 25-30x pe on FY19/FY20 & 15-20x pe on FY21/FY22. On 1 year fw EV/S:

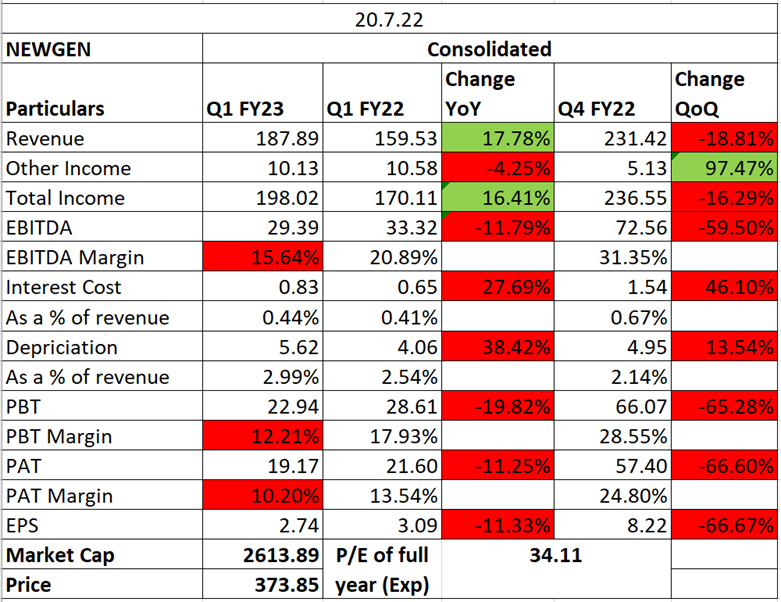

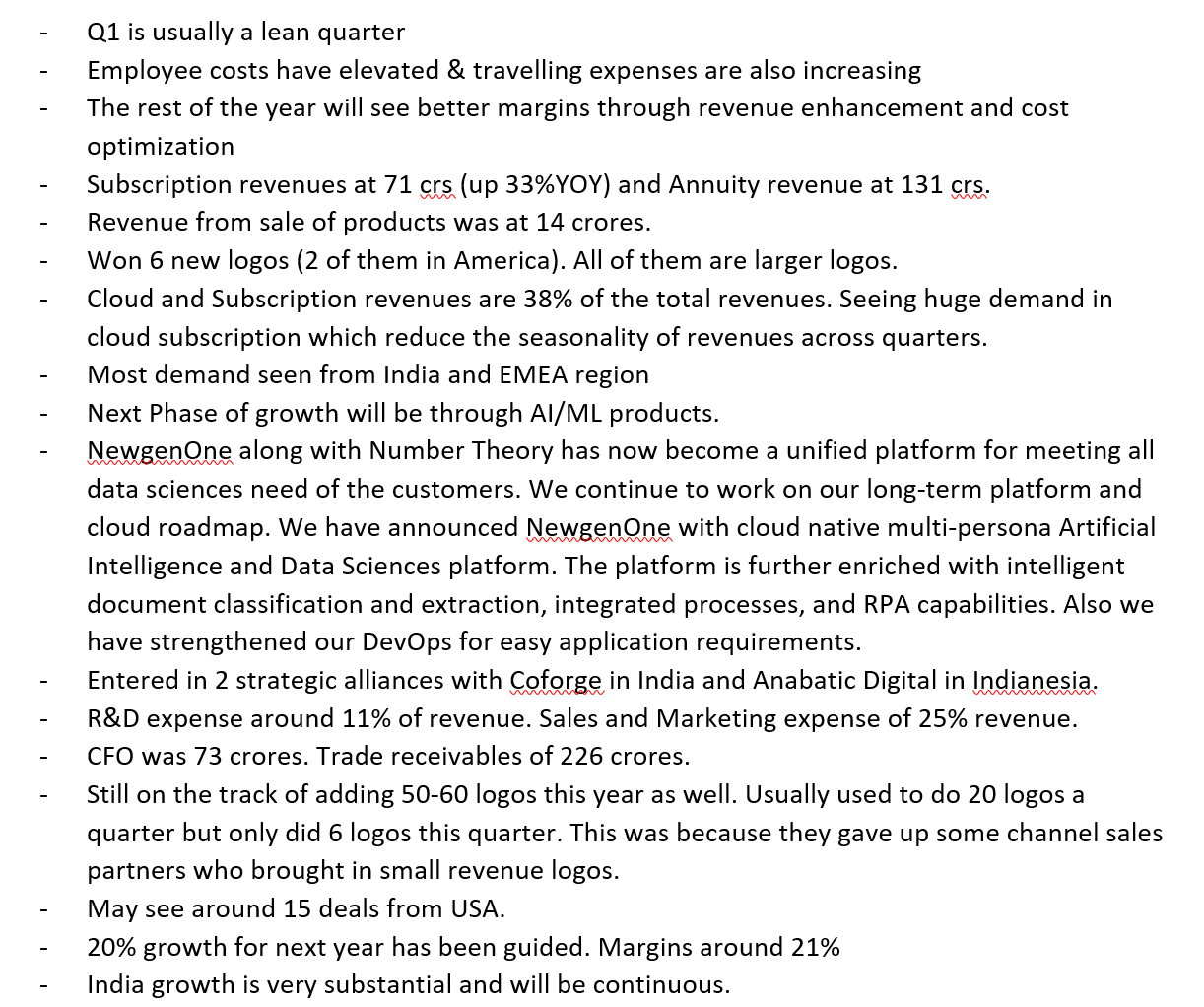

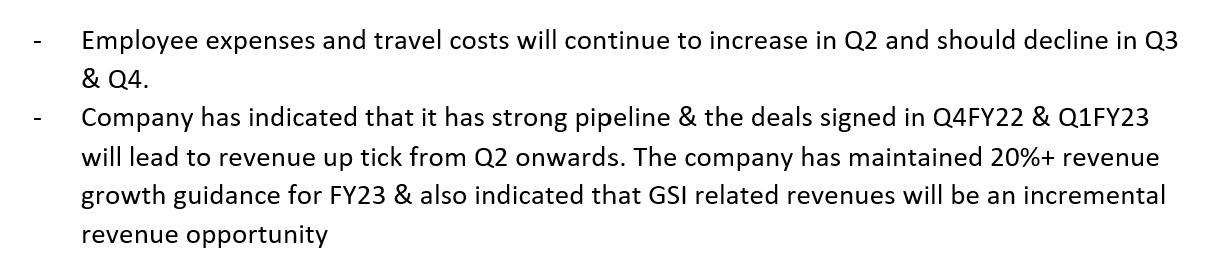

q1 fy23 results: -

q1 fy23 investor presentation.pdf (4.4 MB)

Happen to listen to the concall just out of curiosity (had already exited Newgen for a better opportunity) Some good questions asked.

IMO the numbers need a better look to understand the actual product sales growth in the past years given their different revenue models: Saas, Upfront license and deferred license (annual). A vendor would always be happy to get upfront license fees for his product since it puts more cash in his hands. But instead it seems Newgen is getting pushed to offer deferred license. This does not seem inline if the product truly commands good market value. A glimpse of FY22 results show around 65% contribution from sale of products to the top line while the remaining 35% from development/services job.

As newgen has seasonality business it will have good revenue in Q3 & Q4 than Q1 & Q2.

Their US business is bleeding - profit from that geography declined by 25 cr in H1FY23 over H1FY22. Otherwise things look in line with the expectations and the topline continues to post decent growth.

They are changing their strategy in the US. Hope will grow better in the US once the relevant strategy in place.

How are they doing that? Do you know any specifics about that?

One of my very good friends always praises about the tools called no code tools and how he build marketing pages on no code tool. This got me researching into no code and low code tools. A company called Newgen provides the enterprise version of low code tools. A thread:

- When we think about TCS or MPhasis, these companies are IT service providers. They do not own any platform. In fact, they cater to the client’s requirement based on their unique needs.

- Enter low code tools which say that just install my platform and install your custom workflows and apps in the matter of days. How does it help organisations?

- Lower TAT, high customisation without any added costs. Think of Shopify as a low code platform. You can modify the banners, change the user journeys on your website etc. without hiring a developer to do this work for you

- Coming to Newgen: Their products are primarily categorised as Enterprise Content Management (ECM), Business Process Management (BPM) and Customer Communication Management (CCM)

- BPM: These tools automate the standard business processes. Think of it like automation of customer onboarding, vendor onboarding, claims processing, loan disbursal, web portals and forms etc.

- For Newgen, this integrates seamlessly with ERP’s and also able to extract information from different documents automatically without writing code. In terms of customer experience, you just upload aadhar card and the portal will tell you the loan eligibility

- CCM: This is where the unified customer communication is leveraged by banks and insurance companies across web, app notifications and SMS based on the custom workflows. For eg., send the congratulatory SMS to the customer on successful loan approval

- ECM: Traditionally companies have to rely on manual workforce to vet the documents and maintain its backup and sanctity. Newgen, with its image processing algorithms, is able to vet the docs, extract the relevant information and pass it on to the relevant business process

- With the focus on its products clear, the different revenue streams of the company include sales of products (21%), ATS/AMC charges (25%), Implementation charges (16%), support charges (28%) and SAAS revenue (10%)

- India constitutes 28%, APAC 14%, Europe 31% and USA 27% of the total revenue of 770 cr. Among the sectors Banking and financial services constitute 62% of revenue, government services constitutes 15%, insurance and health constitutes 7% each

- Coming to the recurring part of the revenue, ATS/AMC, SAAS and support constitutes annuity plans. SAAS is a per user subscription charge whereas AMC is on annuity license basis. More the license more the ATS/AMC. These constitutes product profile margins of 90%+

- Support charges are the service charges and hence gross margins are 60%+. Regarding GTM, the company has 300+sales and marketing staff primarily focussed on Asia and APAC. They target the client using low value deals post which they increase the ticket size from the clients

- Regarding Europe and USA, there had been a lot of churn due to low paying propensity of mid level clients. Hence newgen is focussing on fortune 2000 clients who would be recommended newgen via GSI (global system integrators)

- Coming to R&D and marketing expenses, these constitute 10% and 24% of the revenues respectively. R&D is basically categorised under employee expenses and marketing expenses are also a part of P&L. Hence both of these are not amortized

- However, the benefits of these are accrued in the future customers and their annuity. Hence during the high growth phase, the bottomline tends to get deflated in such a business. But gone right, it would be a high free cash flow business since AMC does not incur much expenses

- Hence the standard metrics like ROCE, ROIC and ROE may look subdued now due to long term investments accrued in P&L

- The company has been able to grow its sales at 14% CAGR from 2013 to 2022 from 200 cr to ~800 cr while the profits grew by 16% CAGR from 36 cr to 164 cr

- Due to the partnerships with Global system integrators (like Accenture etc.) where the payments are done automatically through their systems based on GSI’s terms, this tends to get reflected in their cash conversion cycle

- But over-dependance on GSI could lead to loosening of pricing power by Newgen. This is something which is acknowledged by the management in the recent concall as well

- The company is led by Mr Diwakar Nigam who has been leading the solutions with banking and insurance since 1993. Currently the company is headed by Mr Virender Jeet who has been with the company since its inception

- The SAAS based tools require the very high innovative DNA otherwise someone else can come with deep pockets and dislodge you. Newgen is having 44 patents in terms of advanced ML capabilities

- They do not use open source image processing API’s. Rather they have built it on their own and integrated it with ECM. Newton has started making forays in Gartner and Forrester, the recommendations of which are heeded by the global CIO’s

- The no code enterprise market is valued at $40bn. The company, after championing banking an insurance, is making its foray in healthcare. It aims to grow its toppling at 4000 cr from the current 800 cr in the next 6 years

- One of the reason why the big tech or companies like Accenture, TCS won’t enter this field: Proprietary patented technologies is the big cost advantage. The moment you switch to big tech API’s, your costs balloons

- A low code platform primarily for banking and insurance needs the deep expertise for 25 years. Many companies will find it hard to compete with them on product use cases as well as costs. Recently they launched a trade finance platform for banking as well

- Regarding their competitors, IBM, Oracle are capable of business process management but the ease of integrations with newgen along with solving additional use cases leads to newgen beating the competitors. Reference: https://www.gartner.com/reviews/market/business-process-automation-tools/vendor/newgen-software/alternatives

- Coming to Free cash flows and ability of the company to convert their profits to FCF, the company generated a good cash and is able to convert most of its profits to cash. Here is what the graph looks like as attached

- The company does not have much related party transactions. However a red flag is presented in the form of the following: Why Mr Nigam is taking such a hefty salary even though he is in advisory role?

- Coming to valuations: Considering that sales and marketing expenses would be abated in the long run, with discount rate of 20%, 13% and terminal rate of 7%, the fair value comes at 377 at 25% Margin of safety

The thread can be found here: https://twitter.com/manujindal2803/status/1607254868791816192