I think Neuland is supplying either KSM or some API to Natco. I read somewhere but not able to locate the note now. Let me try once again

3 Likes

Yes At an EBITDA multiple of 10 ( which comes around 1500 price), the stock has come to a very attractive buy zone in terms of valuation.300 crs is double of June 21 TTM EBITDA. My calculations assuming 15% revenue growth Time period 3 years Revenue 1420 EBITDA @ 14% 197 crs EBITDA Multiple 10. This is very attractive if you consider the band for so many quarters in the past. In addition to this , I will see the Price Action ( as I have my tech indicators) and then start accumulating. As of now, at todays prices it has become attractive and I need to see the support at these levels to buy.

2 Likes

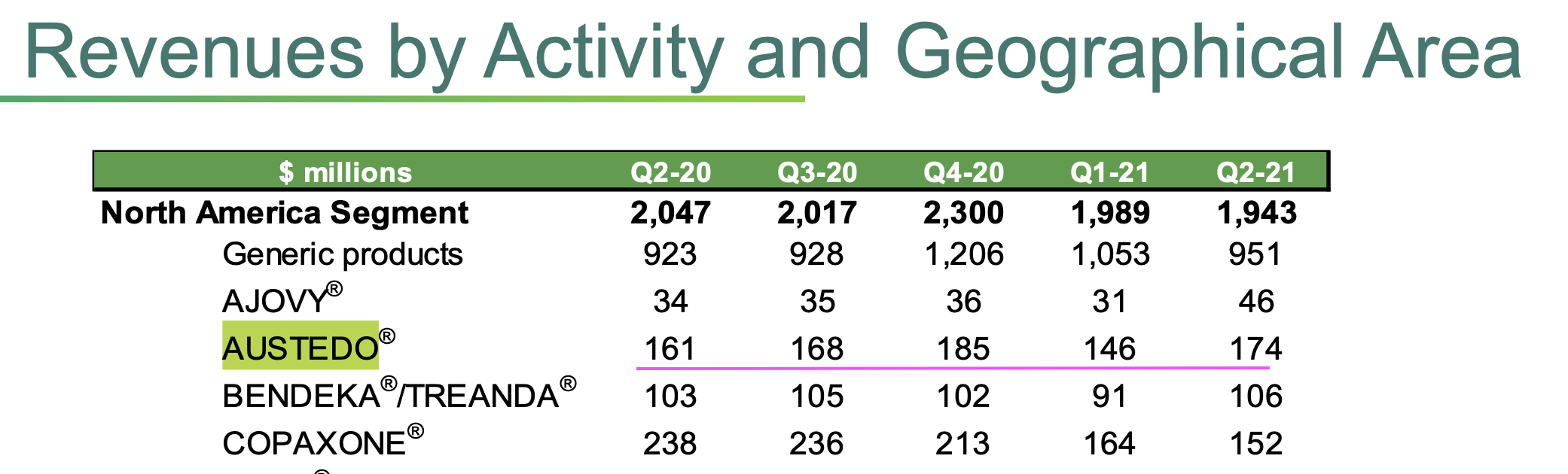

Looking at Teva Results for Austedo, for whom Neuland is the supplier for Deutetrabenazine CMS molecule:

They have a decent growth QoQ and YoY

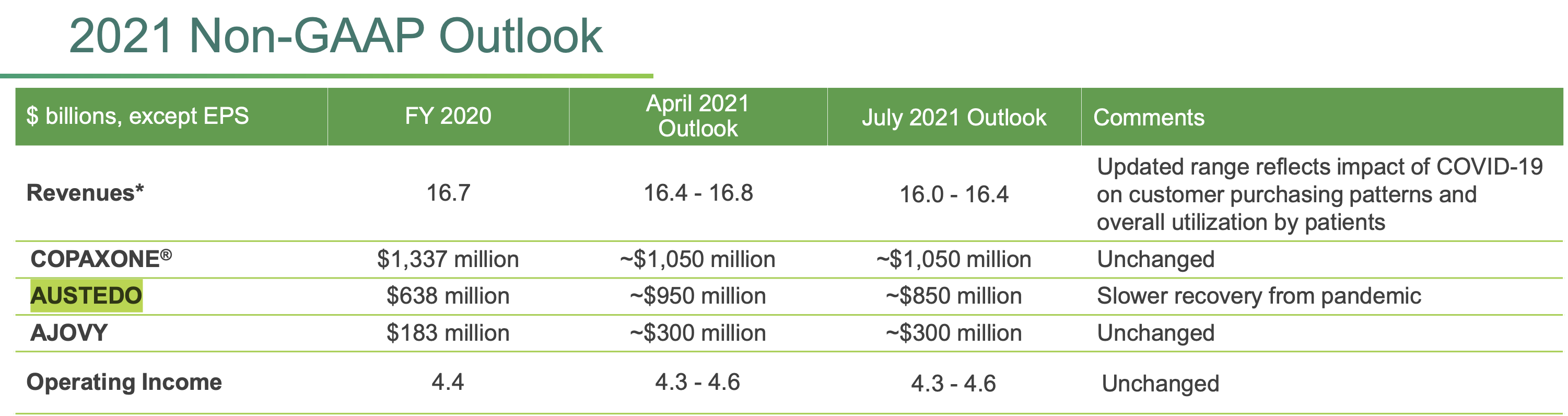

But the outlook from mgmt for 2021 has been reduced a bit due to slower recovery from Covid:

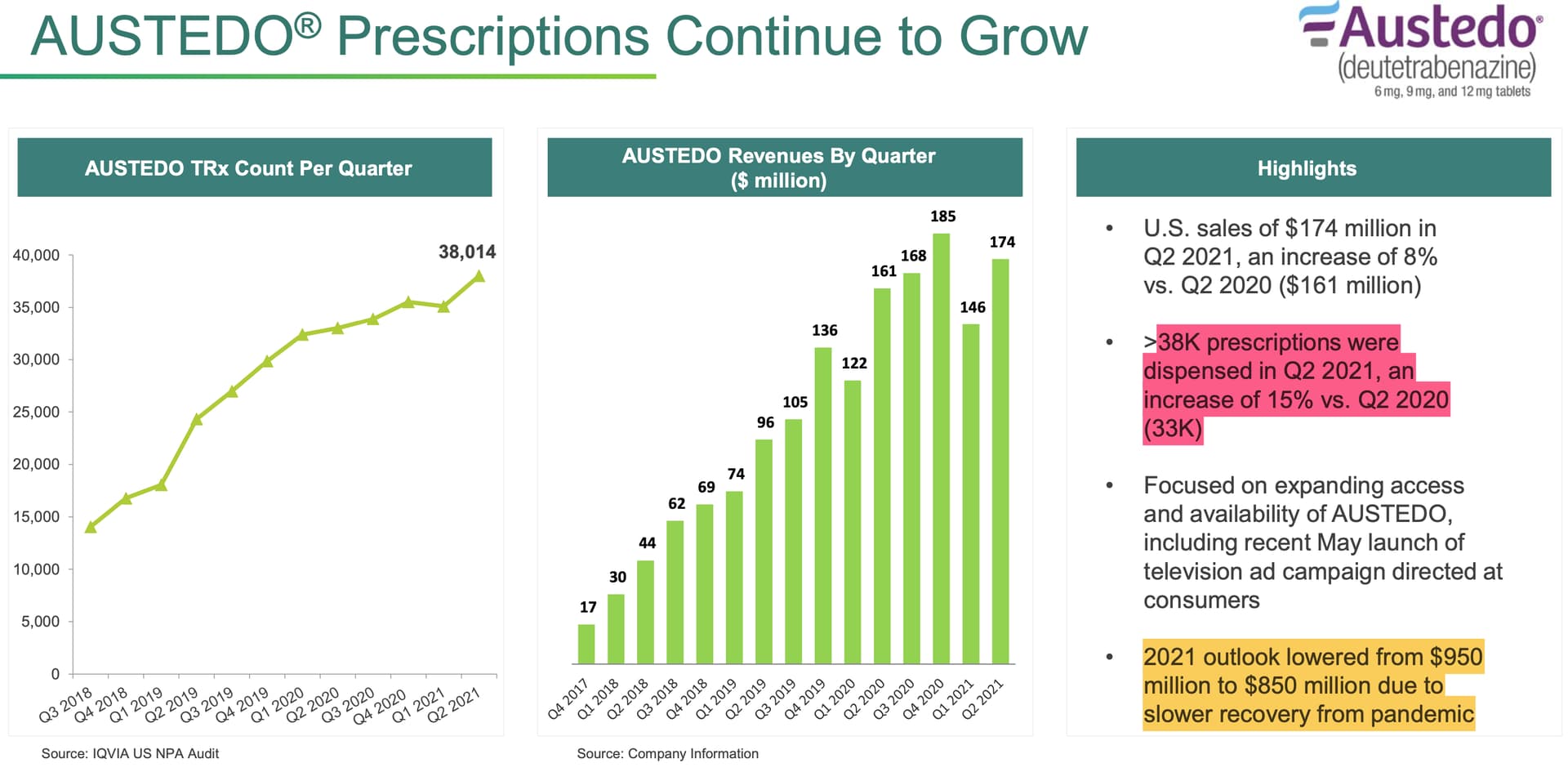

Detailed snapshot of the growth in Austedo since its 2017 approval

20 Likes

Credit rating update - reaffirmed

To gauge swings in PE ratio of neuland over last 5 years - there has been wild swings between 60 to 15 - three instances in this timeframe per below with median around 36.

Sums up mkt views on extreme optimism and pessimism.

On PE basis, We are standing midway in third correction after two consecutive under performance in quarters I.e. 60+ to sub 30, one more subdued quarter can take it to lower band of 15 PE. Recall that management wasn’t sounding confident on QoQ guidance but somewhat comfortable at YoY improvement though.

- Scenario 1 - cautiously optimist - Q2 results are likely lower than YoY but better than QoQ - EPS in range of 10 to 20, a midway 15 will put TTM PE at 66, based on commentary on outlook mkt may continue current rating and PE ratio of around 25-30, ( slightly better than current)

- Scenario 2 - pessimist - Q2 results are likely lower than YoY and flattish than QoQ - EPS in range of 10 , will put TTM PE at 60, given third qtr of subdued performance - commentary may not hold much value and market gives pessimistic case lower band of 15 to 20 PE - this could be a nasty LC Scenario.

Given history of company PE peaks and valleys - probability seems high for Scenario 2 - it’s pure play behavior speculation based on past patterns and probability, and may be completely wrong. Due respect to strong biz fundamentals and exciting possibilities for longer term - near term risks are visible( valuation).

Technical chart confirms pessimism with stock far below from 200 EMA levels( when markets are at peak)

Disc - Invested( with lessons learned)

19 Likes

Can any one please help me to understand the below

Is Neuland labs beneficiary of China +1 factor ? No one has raised any question in Concall on this and even management hasn’t commented anything on this piece ?

What is the market size of the Neuland products ? I understand there are bunch of products /projects under pipeline in unit 3 and we will not have any visiability on these at this stage. but how about the current products ?

Thanks,

2 Likes

Brother Why don’t you write the details here, I wish you will post details of fundamental changes not just technicals. For me fundamentally nothing has changed.

Disc: Invested & Biased

6 Likes

For me fundamentally nothing has changed

Can you please elaborate on this. Do you have details of their plan and forecast for the coming years. Markets are forward looking. I have held senior positions and the business plan only few will have access to which includes top investors .They will be the first to exit and YOU and I know come to know much later. Investing is also a game of probability. Also please note there is a difference between a stable business and expanding business. Again, we ordinary guys can visualize a market for JOCKEY but not for complicated business like Neuland. If you can just give me details of their molecule wise sales or CDMO details or their pipeline. Without these, how can you a form a reasonable opinion. Dont get influenced by the videos in you tube or twitter handles. Ultimately , the data matters. Do you have the data. A stable business you can take a risk by buying at a reasonable valuation ( HLL, Nestle, PII, Natco ,etc) but not a new business or an expanding business.

11 Likes

You don’t have to know the exact weight of a person to tell whether he is fat or not.

As, rightly said investing is a game of probability. One cannot decide the future of business with just 2 bad quarters.

One cannot get complete detail of the molecules in the pipeline and their sales opportunities. If you will only invest when he knows the exact granular details then one will not be able to invest in API and CDMO companies.

Sometime you have to give a business 4 to 5 quarter. If thesis does not works then it’s fine, you can exit that business.

5 Likes

On what surmise are you making this statement. Pls indicate if you have data.

Perception changes with the change in market cap. Neuland is one of the company who states explicitly their molecule pipeline and their stagewise progress. There will be lot of if and buts between progress at Lab and ultimate commercialisation. Even after commercialisation, not all drugs become blockbuster drugs. This is the risk this kind of companies face.

Market is designed to pass wealth from impatient to patient investors. And stock investment always carry risk. To be or Not to be is solely with individuals with their respective R/R.

Disc: Holding from lower levels and no transaction for the past 90 days.

6 Likes

I think this is a futile conversation as it’s almost too easy to predict a new low using recent lows as benchmark.

If Neuland trades in lower circuit tomorrow at any point in time even for a second, it will be lower than the recent low of 1454 and given the way small caps have corrected last couple of weeks - this is entirely possible.

I’d be interested if @sethufan is predicting a new 52 wk low or where the bottom is expected, please share the analysis for the same - otherwise these are just random predictions!

5 Likes

-

Sorry to say but i think just a few LCs won’t change its future and i am not telling by watching youtube videos or tweets but telling from my years of experience as an investor. LCs and UCs come and go, and i would again repeat its long term story is intact. Chart can’t tell anything, if chart would have unfolded the story, then only God knows what would have happened to fundamentals!

No body knows except management what’s really going on but I have made bet on 90% of the facts. 10% risk is everywhere and I am ready for that. But I would never make such a strong statement like new low is coming and all. Doesn’t make sense. Every small and mid cap stock is bleeding at this point, so nothing new here. We should just discuss the business here instead the stock price. If you have any business news per se we would eagerly welcome you to tell the facts. -

What’s stored in future is already described in details in all concalls and even risks associated with those. I won’t reiterate those again here.

-

Going by your logic, one can never invest in small and midcaps

23 Likes

It is very much public. He showcased his holdings in a webinar which has later on been uploaded on Youtube.

17 Likes

This is actually old interview, reposted in new channel.

link to original vedio

Hello Jay how to get this type of report for other companies?

Thanks

Thanks for sharing, Really helped, Must Watch!!

Given Q 2 results will be out soon, a good sign that thread is quite and noises have settled for all momentum chasing, a quick recap of Neuland and Market perspectives of it

Neuland has seen four peaks and troughs for last 12 years, with median PE of 30( we are there about currently), reasons for optimism and pessimism are similar to current cycle - 1-2 Qtrs of underperformance and followed by good performance.

Let’s look at long term CAGR

Stock price CAGR currently lags profit growth for all time periods. Esp TTM. If anything valuations are at fair range of spectrum.

Things to watch out for

- Revenue - need to do 250cr+ range to get back to TTM growth

- Margins - 15%+ has been the case in Q2 and Q3 21, Q4 and Q1 has been sub 12% --need to see it go back to 15%+

- YoY - Q2 21 has been one of the highest performance, YoY performance would not be easy to beat on both revenue and margins, QoQ beat and good H2 commentary will be required to stabilize

17 Likes

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=7a247822-3965-4493-8c27-5d01388adae3

Results

2 Likes

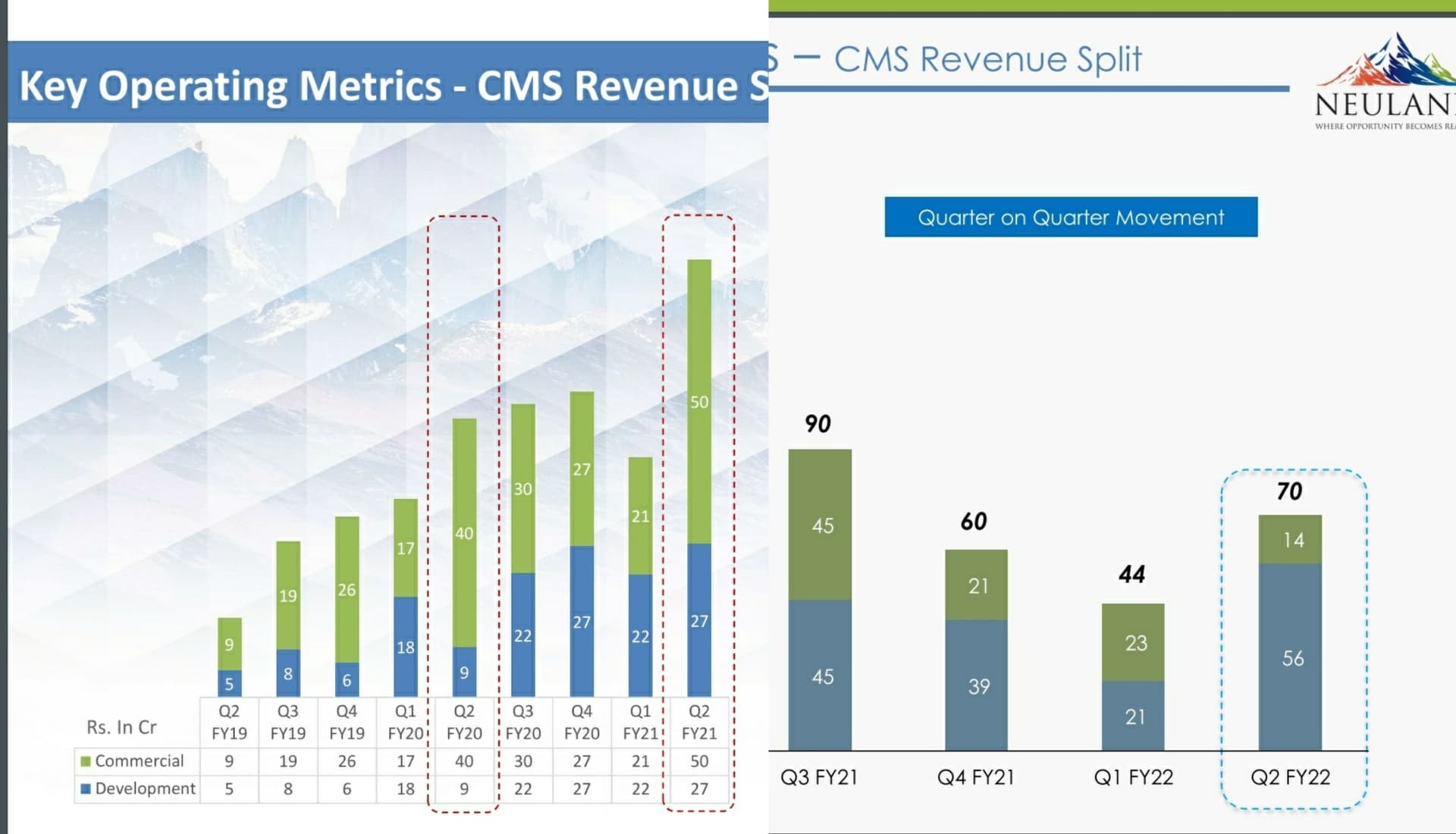

CMS commercialised molecules revenue

Q2FY21 : 50 Crores

Q3FY21 : 45 Crores

Q4FY21 : 21 Crores

Q1FY22 : 23 Crores

Q2FY22 : 14 Crores

15 commercialised CMS molecules in Q2FY21 to 18 molecules in Q2FY22.

Number of molecules have increased during this time frame, yet revenue has declined. What might be the reason for this? When a molecule get commercialised, volumes will increase right? Here, revenue of commercialised molecules are decreasing with each quarter.

6 Likes

Check the concall. They are guiding that Manufacturing revenues/supplies will be in second half of this year ![]()

11 Likes