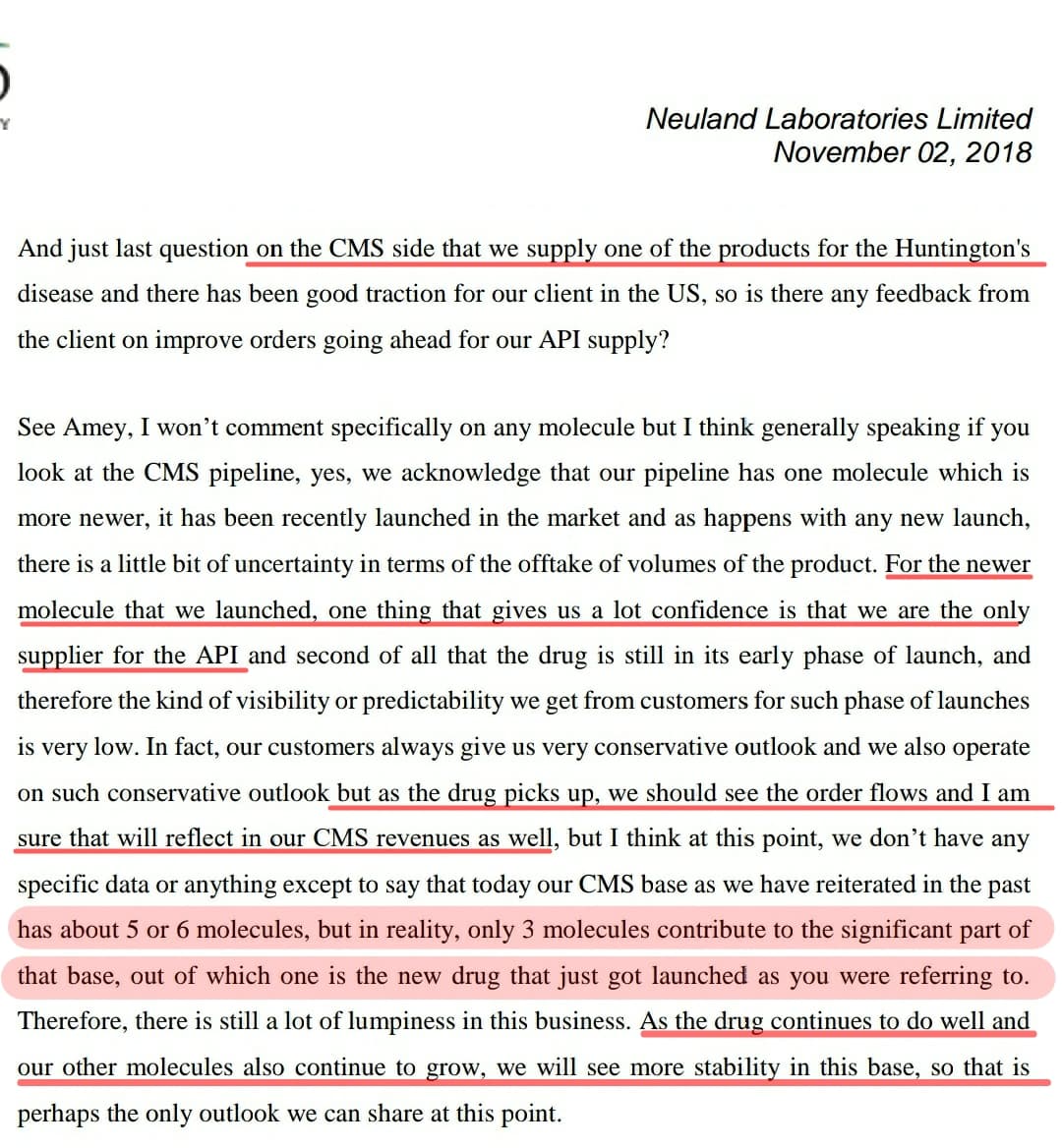

From 15:19 of the earnings call video

"Keshav kumar: So, I wanted to understand that, what would be the reasons to onboard a CDMO at the clients end at such a late stage, like, would we be a secondary or tertiary supplier. I mean, it’s absolutely terrific for us. But trying to understand from the clients perspective. What would be the reasons to go for such a late stage Tech transfer and all that extra regulatory stuff that comes with it.

Neuland : So we work with a lot of small to mid-sized companies Keshav and these are usually biotech companies and when they start their clinical journey in Phase 1, they typically start with a CDMO who they find easy to work with or probably someone that’s closer to home for them. And as they going through Phase 2 phase 3, and they see clinical success and they’re gearing up for commercialization, there they get business development folks on board, they get sales people on board, who actually start, you know, forecasting quantities… uh… prices. Start, you know, simulating the cost of the tablets and things like that.

That’s when companies actually formulate a strategy of what kind of an API partner, they need, what kind of batch sizes they need, what kind of annual output of API need they need. And in many cases, when they have that strategy, they’ll realize that their first source is not up to the task for doing that and that’s why they usually go for the right kind of CDMO. So in many of these cases, it’s a great opportunity for us as you said. But it’s also because, you know, a lot of these drug Discovery companies don’t know whether they will get commercialized so they don’t really know qualify someone who is suitable partner for them for commercialization. They they go with someone who’s suitable for them for their Phase 1 and Phase 2."

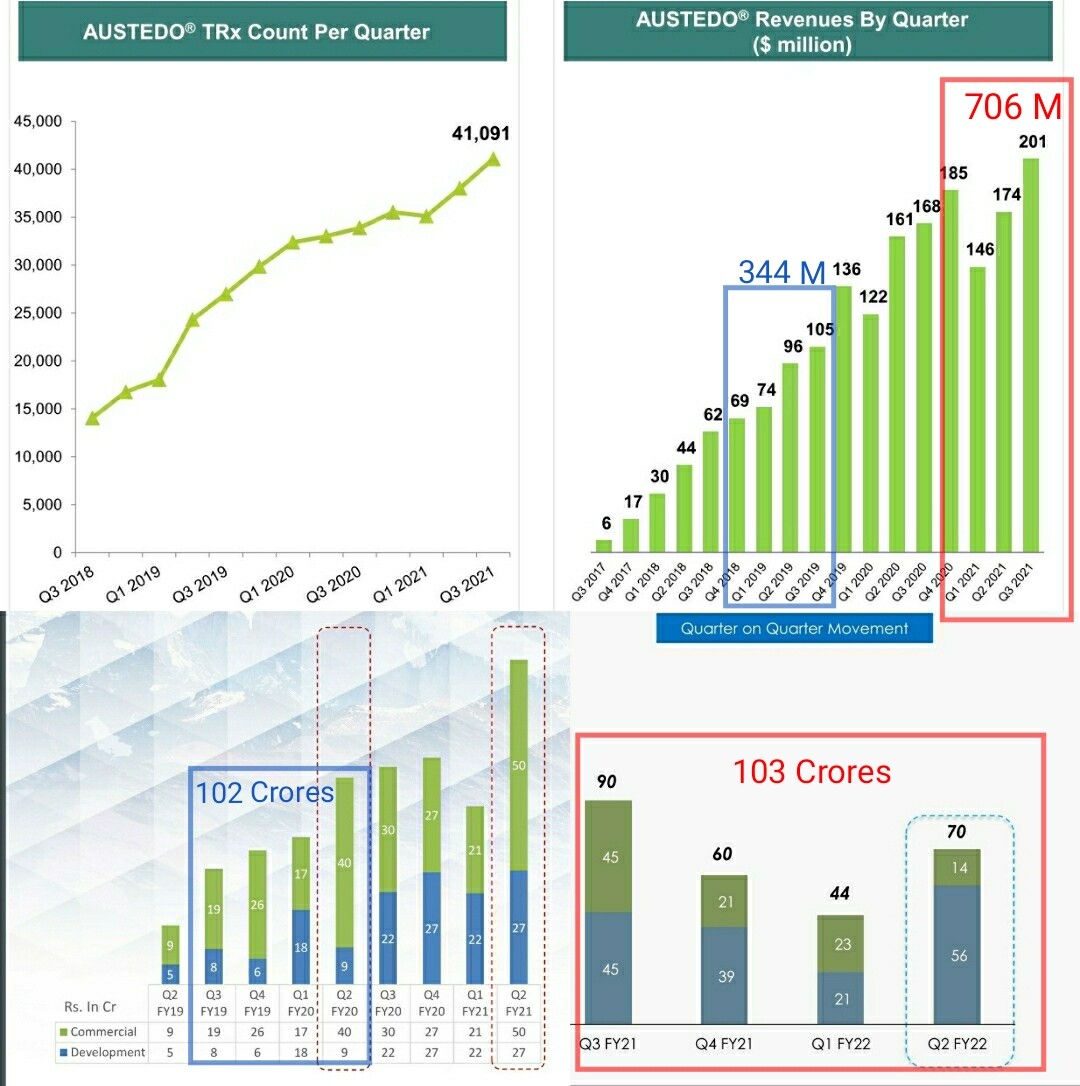

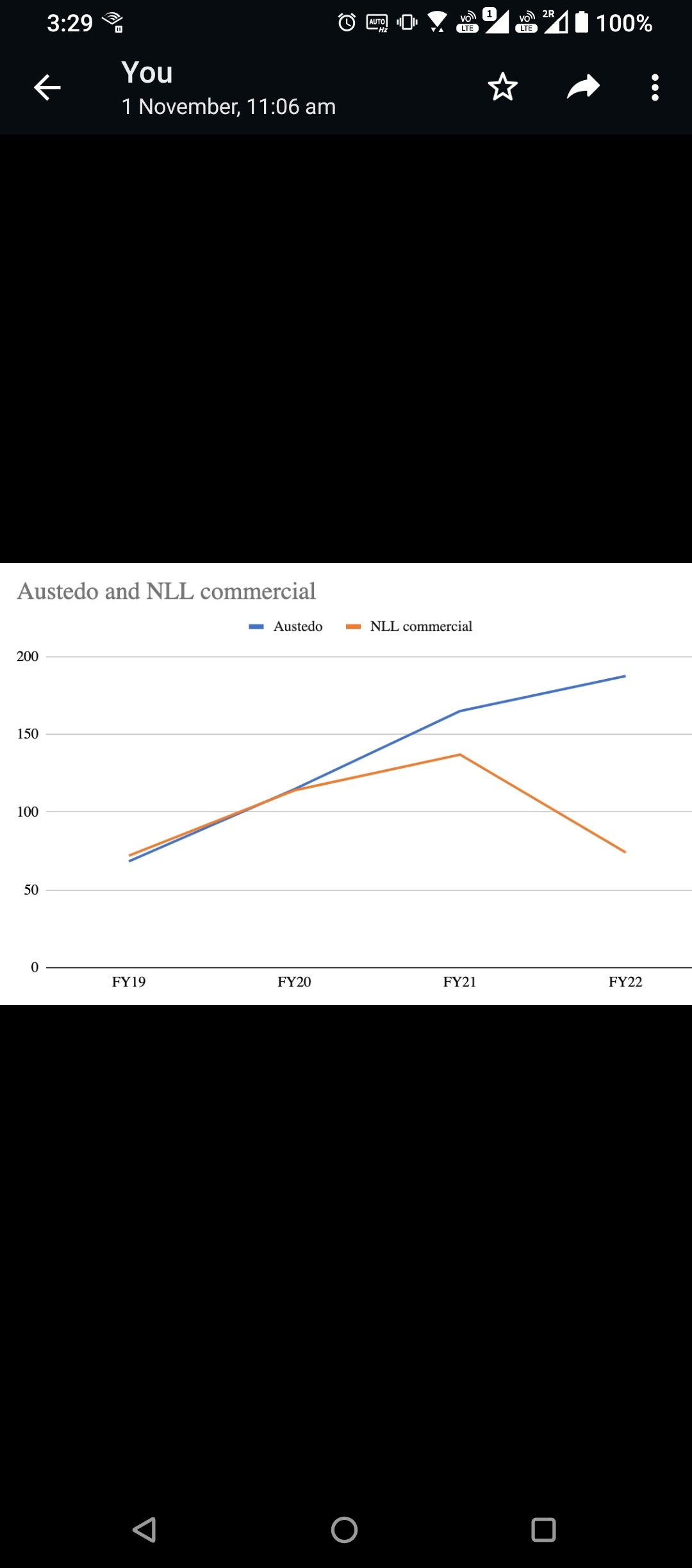

By what management has mentioned, there can be a possibility of Innovator moving away from Neuland as their first source of commercialised molecule and may have find another partner for the same molecule, right?

Quoting management-(“And in many cases, when they have that strategy, they’ll realize that their first source is not up to the task for doing that and that’s why they usually go for the right kind of CDMO”)

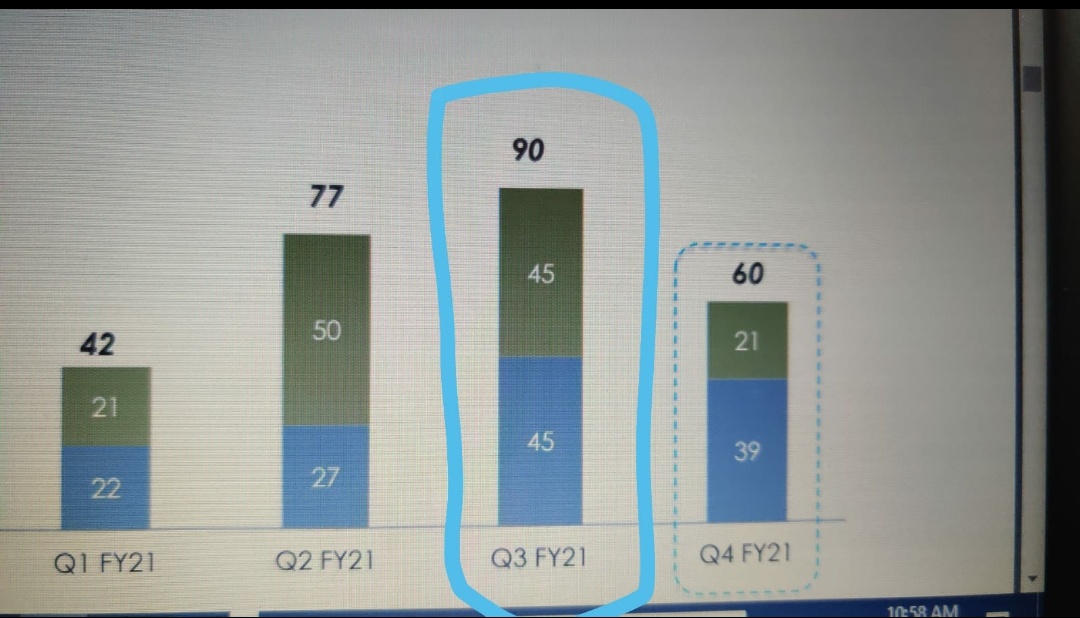

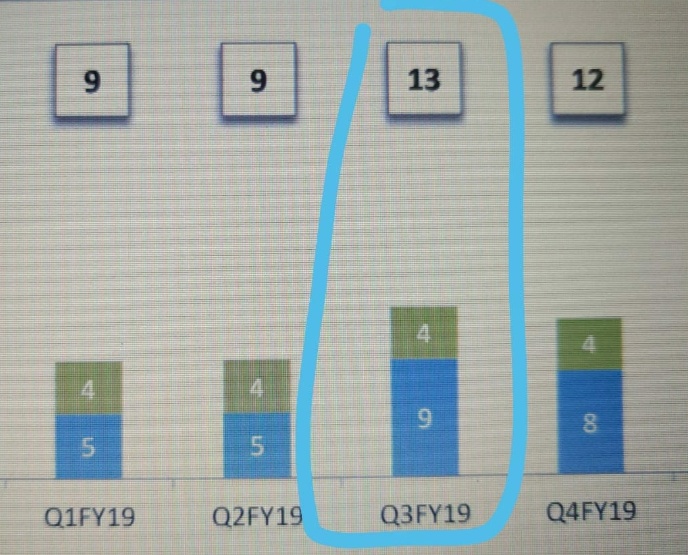

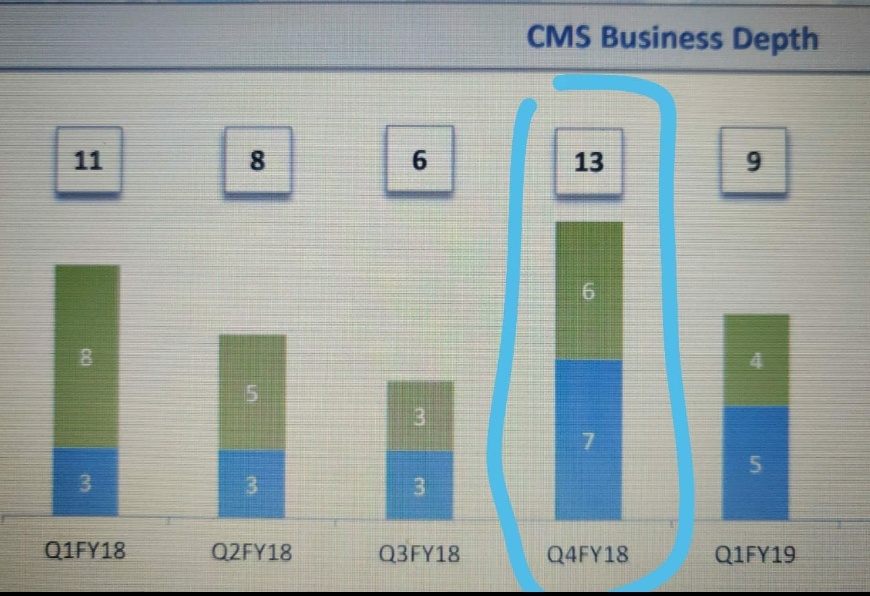

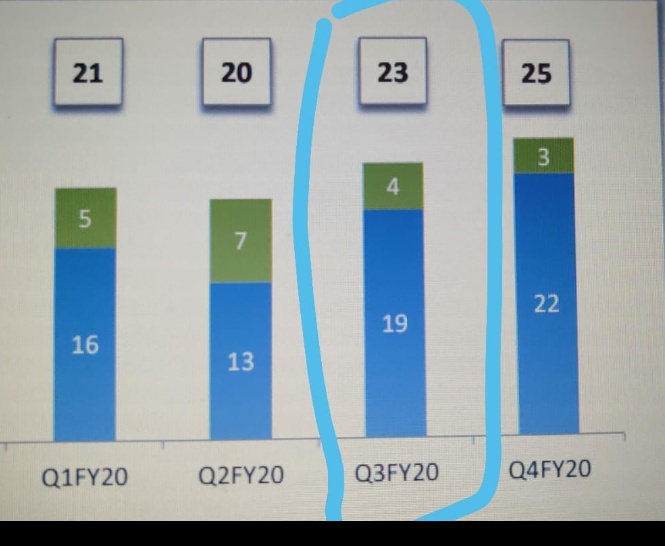

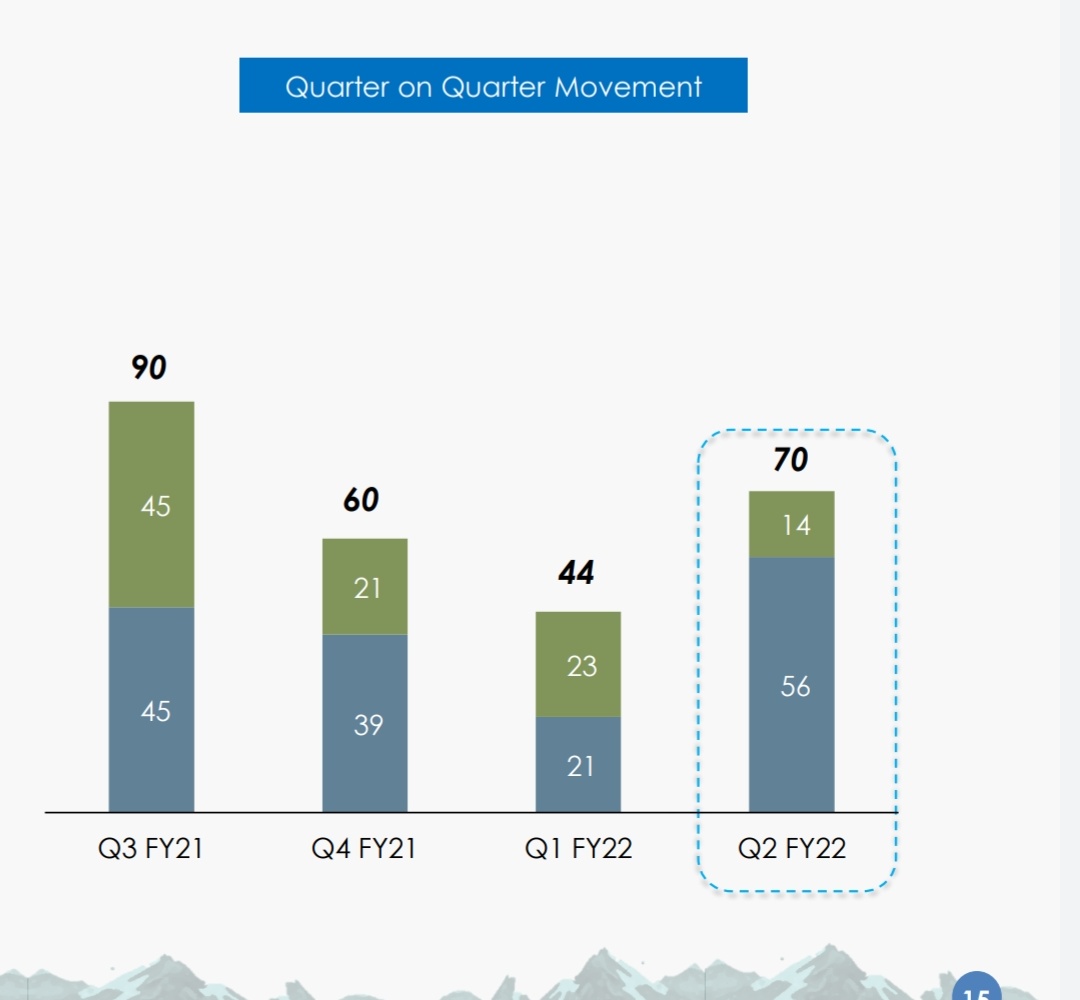

That may explain the dip in revenue of commercialised molecules over the past 5 quarters. What else can explain consistent fall in revenues of commercialised molecules? (General narrative is that, once a molecule get commercialised, then the volumes pick up and lumpiness goes away. Here it is not happening.)