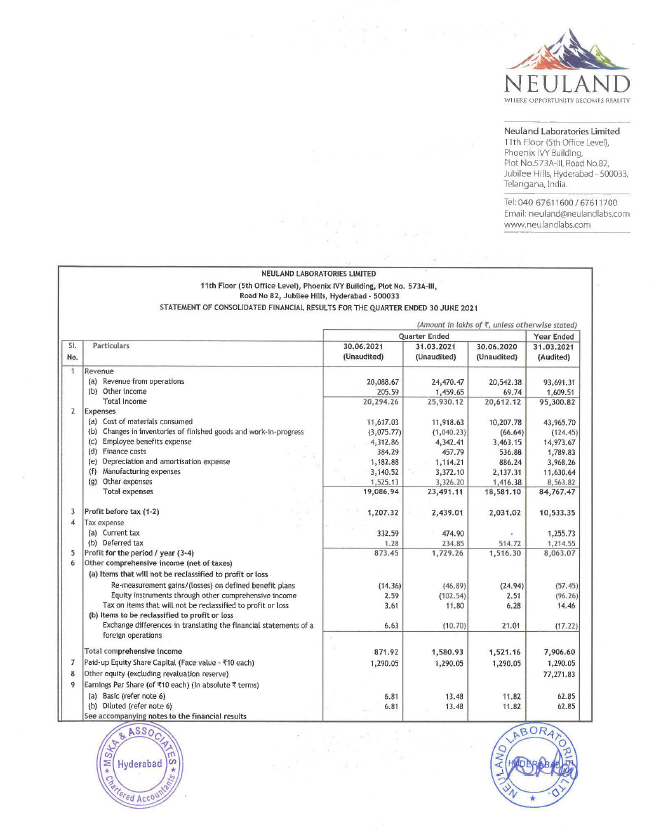

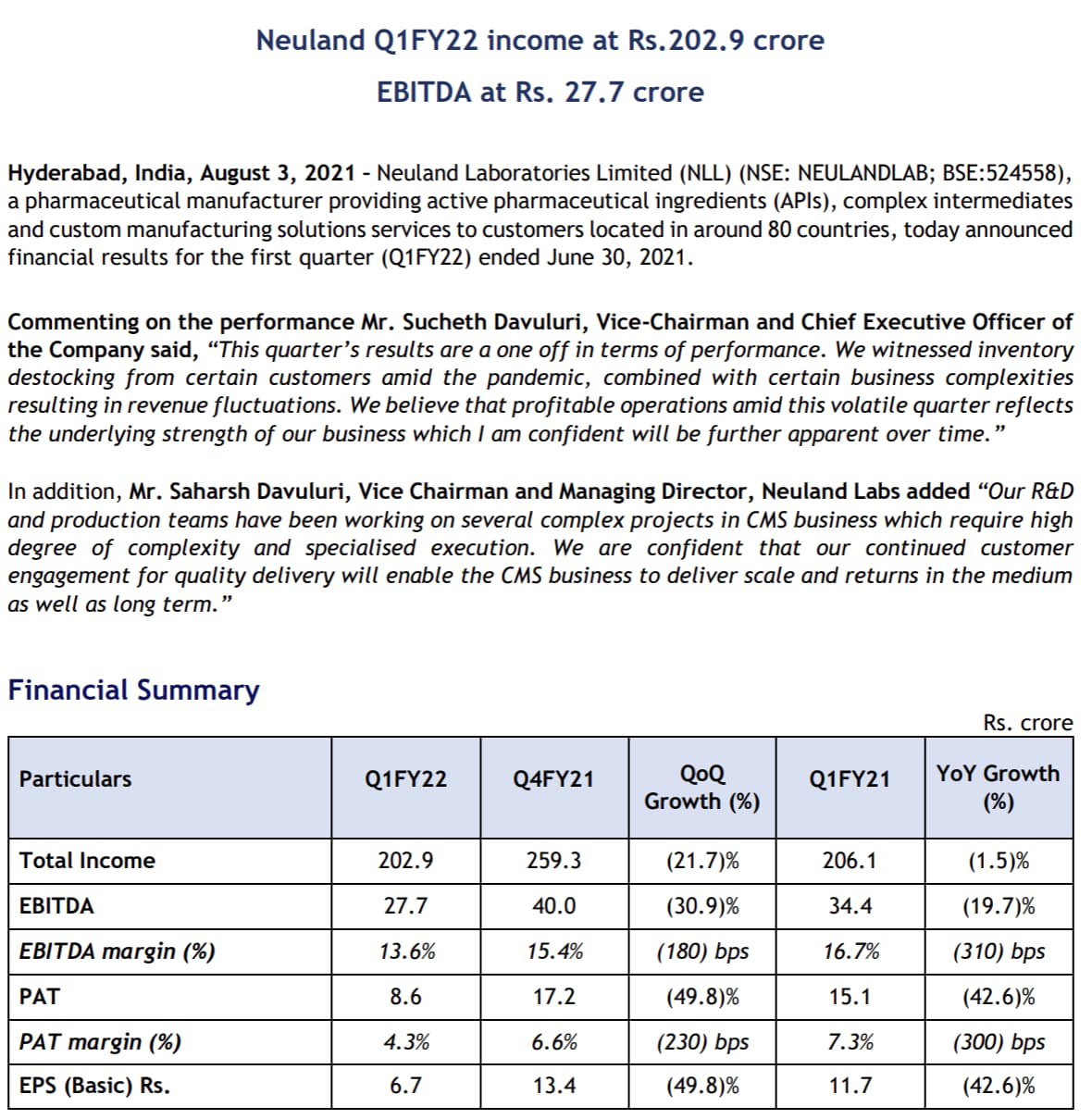

Neuland Q1 2022

https://www1.nseindia.com/corporate/NEULANDLAB_03082021144116_SEINTIMATION3Aug2021TOFILE.pdf

Looking forward to the concall for clarifications.

One bad quarter is an abberation. Consecutive bad quarters may not be treated well by Mr Market. Inventory destocking and business complexity is too vague afaik.

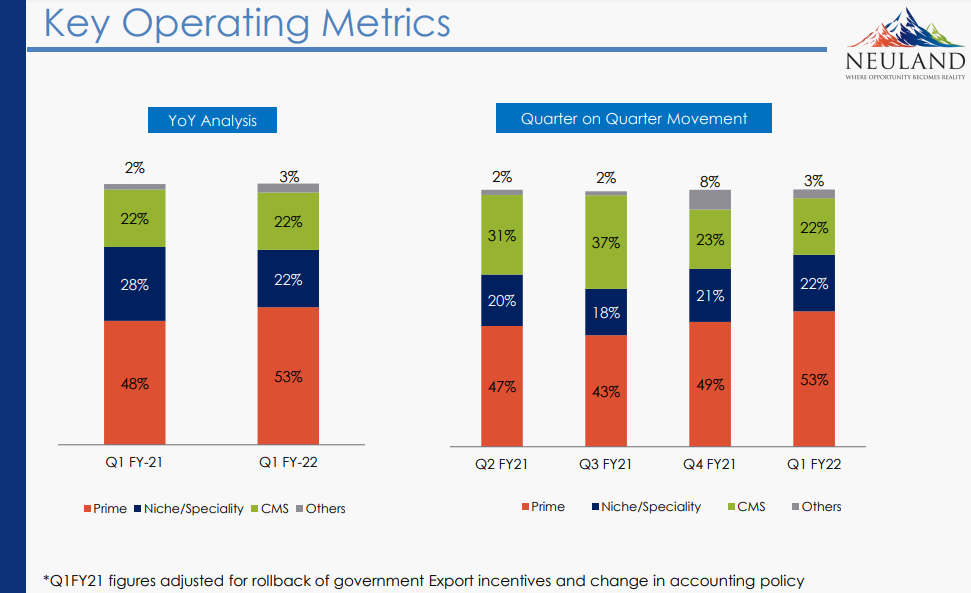

Margin reduction and increase in prime API contribution not good too.

May present an opportunity.

3 Likes

Again a disappointing quarter, management makes tall claims and fails to deliver. These kind of quarters separate boys from men. Neaulnd was unable to pass increase in raw material cost to the end customers, this shows the products they are selling are commodity type api’s and customers can source them from the other producers who can sell it for a bit smaller price. The valuations may not sustain for long If they keep writing useless blogs but fails to concentrate on business.

10 Likes

Concall Notes

There was an impact on rising RM prices. Up front costs for certain projects. Execution has been slightly delayed in some CMS projects due to the complex nature of the project. Delivery is also delayed. Many steps are 1-2 steps away from commercialization. Complex chemistries involved. Being scaled up for 1st time in our plant. To make sure processes work well, we are seeing some extension of timelines. Closely collaborating with customers. Anticipate scaling up these projects. Exciting prospects for molecules. Destocking is temporary in nature. Nature of CMS means that revenue gets lumpy.

Have started commercial supply from unit 3. Unit 1 and 2 running at optimum capacity. Significant ramp up in capacity utilization of unit 3 in the medium term.

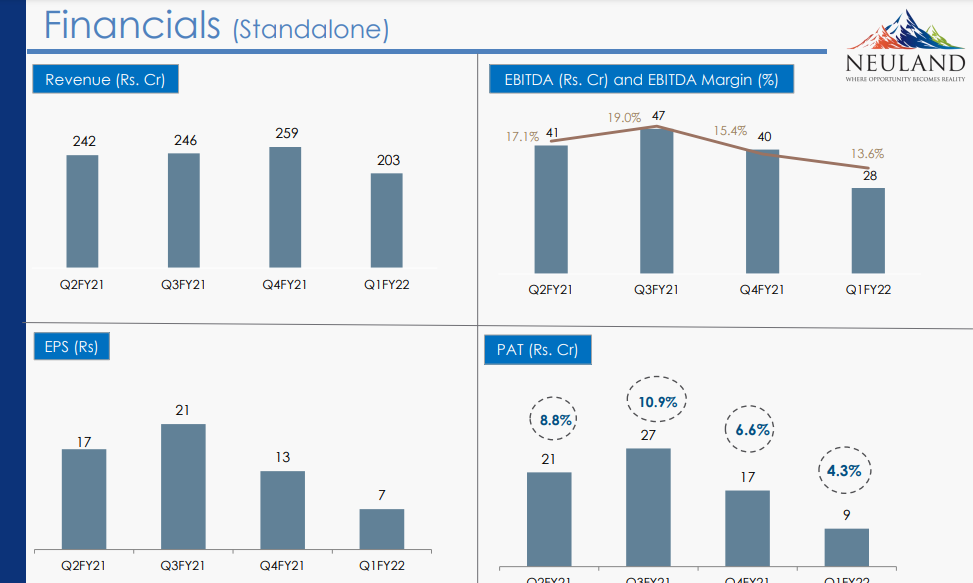

This Q performance was an outlier.

Unit 3: We are moving existing commercial products to Unit 3. All our new projects are also going to unit 3. Timelines of projects and customers does not always align with the quarter boundary. Unit 3 will contribute significantly in this financial year.

Whatever short falls we faced in Q1, projects are delayed, slipped to Q2 and Q3.

15-20% topline and 20% EBITDA margin guidance in medium term (5 year average).

Number of molecules is increasing. So probability of success is also increasing.

Want to become market leader in generic molecules where we enter.

There has been a lul in the last few Q in DMF filings. We expect to have significant 6-8 API filings in next 2-3 quarters across multiple geographies (specifically targeting US and Europe).

Raw material prices: solvent prices have spiked across industry. Price trend is declining.

Unit 3 is commercialized, so ramping up is adding costs. Revenues have not ramped up well right now. Operating de-leverage.

Semaglutide is exciting. Advanced project. Opportunity to be 1st source for generic market. Expect validation to be complete by End of FY23. Exploring exclusive and non exclusive partnerships.

40-50% capacity utilization for unit 3 by End of year.

For the next 2-3 years, unit 3 is enough to scale up. We are being careful to look at various scenarios. 100cr of capex every year. Includes maintenance and capacity enhancement, upgradation capex.

Some molecules in pipeline which could be 100cr per year in nature if it is successful.

4-5 exciting molecules in CMS will get commercialized in next few years. 2 could be very successful.

bilastine lost patent and has that impacted CMS revenues? Cannot confirm or deny due to confidentiality.

As CMS scales to 300-400cr lumpiness would reduce and would have more stability.

We have molecules where we are primary supplier, we have molecules we secondary supplier. As primary supplier we get higher margin but lower volume as secondary we get slightly lower margin but higher volumes.

Its a clear part of our strategy we want to gain market share while being lowest cost producer. R&D for Lifecycle management for existing molecules for making process more efficient. Levetiracetam etc margin has increased.

Lot of CMS molecules we are dealing with in CMS are complex multi-step chemistry, in process monitoring, control etc. Go into new drugs. Customers come with anticipation that we can scale up to higher level. Challenges on process chemistry. Challenges which are difficult to visualize in lab. Customer appreciates the challenges faced and understand the delays.

My take: definitely good volatility in the quarterly results. Exciting times ahead for CMS which is and will be quite lumpy. Right now hurting on the downside, but same CMS lumpiness can also help on the upside when upside volatility comes. This is not the sort of biz where one can really track quarterly numbers. Volatility is the friend of the informed investor. Every investor must make up their own mind regarding business and stock. This is not a buy or sell reco. Business execution is never an ever increasing function of time. There will be down quarters. And that will separate the men and women from the boys and girls in the investor community. Commodity nature of prime segment has been known to everyone that tracks this business and has studied it. If that comes as a surprise to anyone, clearly they haven’t done their homework.

Disc: Invested, biased

36 Likes

If more molecules in CMS are expected to be commercialized, would’nt EBITDA margins be higher than the 20% guidance provided for medium term. Conservative projections or provisioning for potential delays in commercialization?

the question is how much can we believe the management. They seems more interested in extracting money from the company through huge rentals like 20 lakhs per month than focusing on execution of projects. what is the need to pay such huge rent? we tend to write off such things when we have biased view but it gives negative vibes about the integrity of the management.

5 Likes

Is there way to find out more on this 20 lakhs rent per month . What is being rented . I could not find anything more on this from AR.

We cannot take stock price movement as indication of inside trading. Even laurus stock price went down before results, only to go up after results.

What the management stated in the past and what they achieved (they don’t talk the walk!)

**** May 2016 management commentary phrases extracted from the call:

This mid-term vision of reaching Rs.1,000 crores and 20% EBITDA margin by FY’18

aspiring on a long term basis at 20-25% revenue growth

[ACTUALS] FY 2018 Revenue: 527 crores , margin 10%

May 2017 management commentary phrases extracted from the call:

We have also mentioned that we believe our EBITDA margins will move from the 14%, 15% to a 20%

I think I would remain committed to saying that on a three to four year basis we will grow the business at 20% year-on-year and EBITDA margins as a result of that will improve to closer to a 20%

[ACTUALS] FY 21 Actuals: 13% revenue growth vs 20% revenue growth promised earlier. **16% EBIDTA margin

**May 2019 management commentary ** phrases extracted from the call:

I think over a period of three to four years I think we can say that, targeting revenue growth of in the range of 15% to 20% on average

I think our EBITDA margin have been even typically approximately two years ago at about 16% or so,

we think we can move towards the 18% - 19% EBITDA margin over the next one or two years

MAY 2020 management commentary

The EBITDA margin also stood at 13.7% which was roughly 450 basis points higher than the margins of the previous year.

MAY 2021 management commentary

EBITDA margin stood at 17.1% for FY’21, higher by 340 basis points for the same period for the reason stated above

We have also undertaken CAPEX of around Rs.105 crores for FY’21.

We know the actuals for FY20 and FY21

[Disc:] Not invested

55 Likes

Nothing wrong with the business and this company needs to be evaluated on an annual basis not on qtrly basis. I agree the valuation is expensive and getting corrected by this fall. It is still growing if you consider annual and valuation becomes very attractive when it comes around 1500. I will buy for long term. I have understood the business not in its entirety but to the extent of developing a conviction to buy around that level. The focus needs to be on what they do with the business not on EBITDA margin. If business is going to be good, financials will follow.

14 Likes

It would be great if you can explain the ‘Expensive’ valuation here? Company has TTM (including June’21 quarter) sales of 932 crores and Net profit of 74 crores. Despite this bad quarter, company has grown its Sales at 13% and profit at 21% annually over last 5 years. The current valuation is 2150 crores meaning P/S ratio of 2.2 and less than 30 PE ratio. Is it expensive?

10 Likes

In my view, P/S should be looked together with EBIDTA margin. A company with EBIDTA margins close to 10%, resembles to commodities, like Tata steel, JSW steel etc. Even with lower EBIDTA margins market was awarding higher valuation on the expectation of high growth which clearly have not sustained in previous two quarters, and EBIDTA margin has come down again.

Disc. Have a small tracking position.

4 Likes

Thanks for the reply. I had taken a small position in this for tracking but could not give much time. But I did listen to the recent concall and the management repeatedly talks about few molecules which are in pipeline and becoming commercial soon. Also the additional revenues in next quarters will come from third unit. So things will turn quickly for this company if they walk the talk on account of lower base.

But if its only the talk and the pattern in similar to the past, then market becomes skeptical of its prospects.

1 Like

Historical figures is of no use . they just help to understand the company. Markets are forward looking . No sales growth this qtr. Negative EBITDA growth for 2 consecutive quarters from a double digit EBITDA growth since Mar 19. I always look at the band of the EBITDA Multiple vis a vis the growth but not at a particular point of time like the pe of 32 you said. Same way MCAP/sales. Standalone analysis is not good and it can make one biased. EBITDA growth of 19% vs 32 pe is definitely expensive. Mar 20 number EBITDA growth 56% Vs pe of 20 Vs EBIDTA Multiple of just 3.31. The price was 261. Anyway the long term story is good as I stated above and I follow my price points as per my TA to add more.

6 Likes

I’m not sure, if this has been brought up earlier but I was just going through the shareholders of Neuland Labs at the end of FY21 and I was surprised to know that Natco Pharma holds 7,000 shares in the co. Mr VC Nannapaneni holds 10,000 shares and Mr Rajeev Nannapaneni holds 4,000 shares. Not sure whether this is due to the confidence they have in the company or because they’re friends…

3 Likes

Does the fall in share price is primarily due to impact of Q2 results or any change in fundamentals of the company? The recent release of investors presentations looks bright and promising and recent fall looks attractive with 26 PE. However, the continuous fall on share price atleast 5% on everyday seems concerning and not sure where will it go and stop…

1 Like

As you rightly mentioned, Investor Presentation points out a wonderful future. The long term story is still very much intact. Just a couple of quarters here and there.

This is just a transition period where shares are moving from people with borrowed conviction to people who actually studied and formed conviction for themselves.

3 Likes

Going by the management’s guidance of 15% revenue growth over long term (assuming 15% is achievable this year as well), one year forward EV/Sales stands at ~ 1.8. Assuming, the full year EBITDA margin at 17%, the EV/EBITDA would be ~ 11.

When the market is raging with all kinds of high valuations, I feel the current kind of valuation for a business with multiple long term growth tailwinds is very lucrative.

3 years down the line, if they do manage to grow in line with their target (which as per them is conservative). Revenue would stand at 1500 crores and EBITDA (margin 20%) : 300 crores. Market wouldn’t be afraid to give a higher multiple at that stage. Don’t want to get into stock price translations according to the performance…

Disc : Invested since lower levels. Forms the biggest chunk of my PF. Have added today.

6 Likes

@phreakv6 had a important point to make …

Change in Shareholding is good indicator of what might happen to any stock

June 2020 to June 2021

- Promoter , FII and DII all have reduced their holding

- Retail / Public has increased their holding from 34.12% to 43.85 %

The valuation had gone too high for comfort … Business may be stable but price extremes are possible on both sides …

1 Like