Only dependence on Austedo may flatten growth like ibubrofen in IOLCP. I just believe their peptide bet may pay off and if it does it could be 5x in 5 years…Disc invested

1 Like

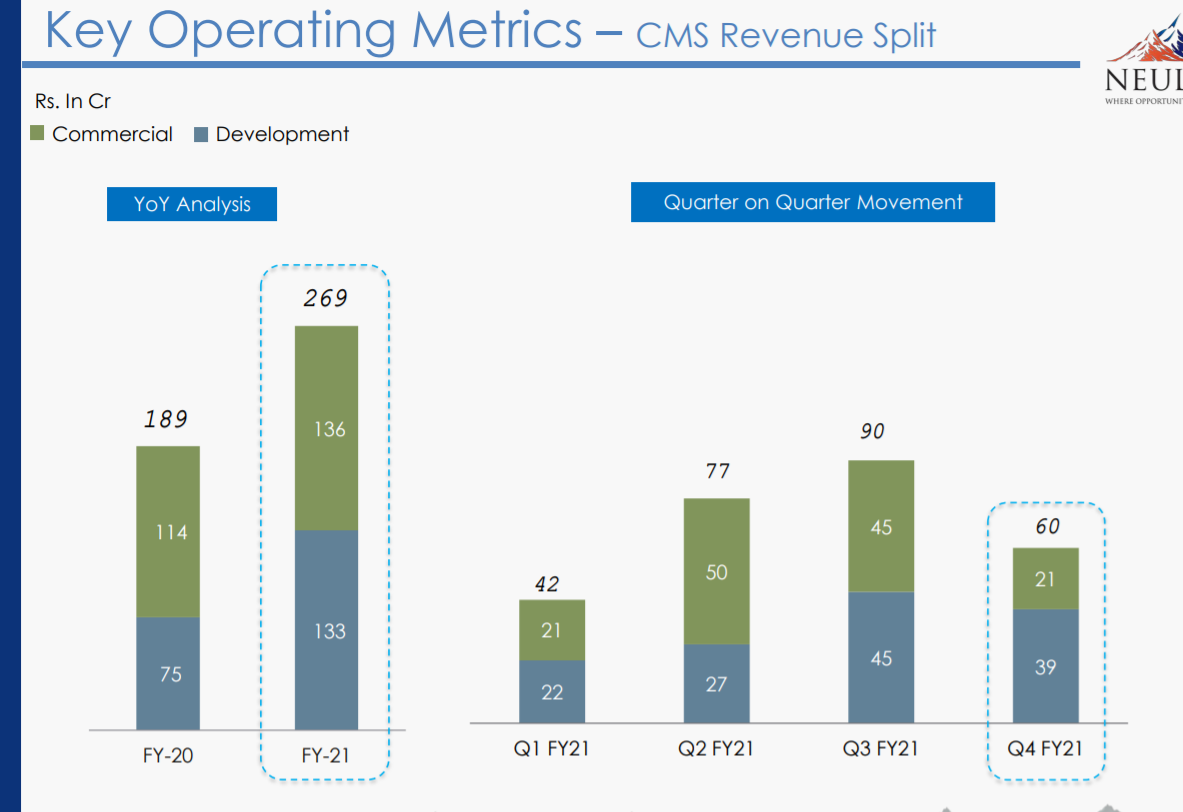

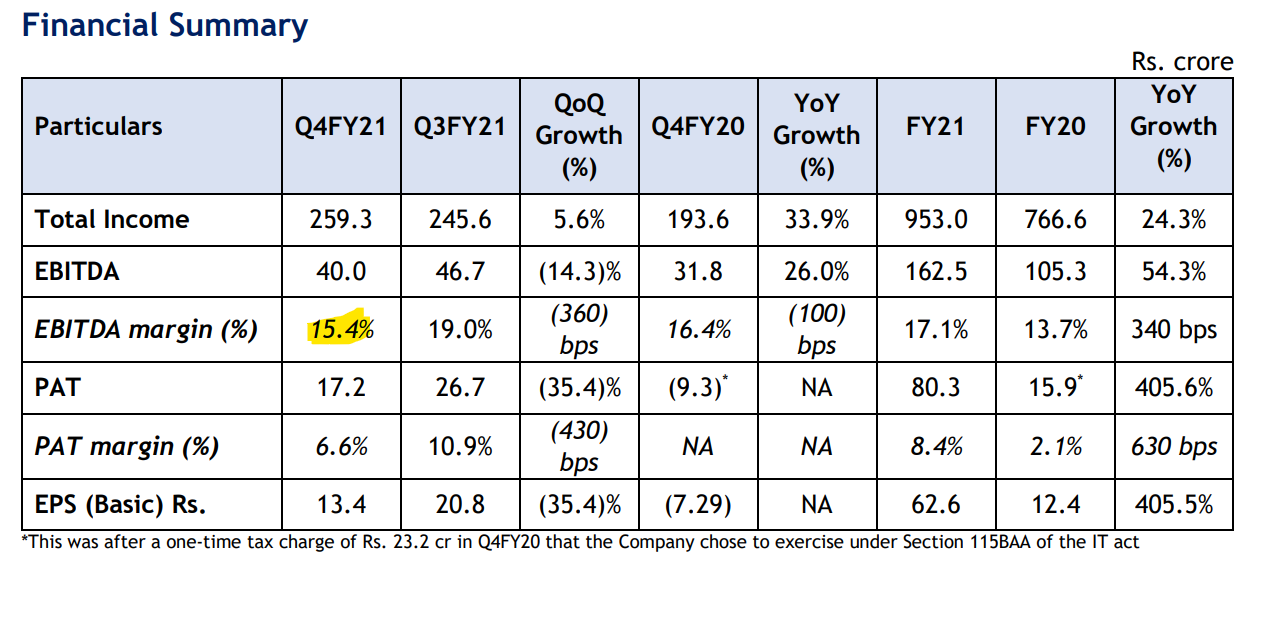

Company has announced consecutive another strong quarter Q3FY21 of top-line and bottom-line performance. The revenue at Rs.245.6 crores was a 20% improvement over the corresponding quarter of the last fiscal while the margins have shown an upward trajectory and closed at 19.0%. This was driven by growth across the GDS and CMS verticals. The company remains confident of its long-term growth aspirations as well as its margin resilience.

• Total income increased by 20.0% in Q3FY21 on account of secular growth in GDS and CMS.

• Prime segment continues growth led by Levetiracetam and Mirtazapine.

• Speciality business had a stable quarter led by Deferasirox and Dorzolamide.

• CMS business witnessed growth in scale-up projects and higher projects coming up for validation.

• Two APIs shipped from Unit III.

• Filed DMF for Donepezil Base with USFDA.

• EBITDA margin increased by 480 bps from 14.2% to 19.0% in Q3FY21.

• Increase in PBT margins by 540 bps and PAT margins by 550 bps.

3 Likes

Capacity Expansion Plans to cater opportunities

So currently for the year 2021, the company is roughly at around 80 crores of investments and they have a plan to basically evaluate certain CAPEX proposals that are in the pipeline in the range of 50 to 60 crores in this year. So it depends how a particular molecule looks like if it makes the attractive business investment. For the next year also, the company has a similar kind of investment plans because the business is looking attractive for new propositions.

1 Like

Future Outlook

Company has already developed peptides like Linaclotide. The company is efficiently working on peptides like Liraglutide and Semaglutide and these are having huge commercial value going forward. These peptides being fairly complex in nature, the timelines for development for filing a DMF are longer.

Typical small molecules take anywhere from 3 to 9 months to file a DMF whereas the complex peptide-like Liraglutide or Semaglutide could take 2-2.5 years. But given that the opportunity is fairly large and the company is excited about these molecules and hopefully, the company is having few interesting partnerships on the generic peptide side.

17 Likes

Neuland has a big amount of its assets in the form of goodwill (>20%). While it is artificially reducing the RoCE, doesn’t it pose a risk in terms of future profitability once company decides to impair it? For a company with annual PAT of 80 crores, goodwill of 280 crores is a huge amount. Isn’t it a big risk from Investors’ point of view?

Disc: tracking

3 Likes

Markets generally are not that concerned about good will impairment as what I have seen as it does not affect cash flow. But they may decide to impair it if the businesses that were acquired are not efficient as it was thought out to be, which is not a good sign.

Do you have any data with regard to the asset turnover ratio both before acquisition and post acquisition and also the asset turnover ratio of the acquired entities (i.e. subsidiaries). If the ROA is improving then they may not impair goodwill as the acquisition has worked for them.

Please provide the data if you have as it will be helpful.

2 Likes

Neuland Labs CRISIL Credit Rating Update: https://www.bseindia.com/xml-data/corpfiling/AttachLive/9accfe08-baf7-49e7-9175-5353f3933f81.pdf

The thesis behind the rating:

Neuland is expected to sustain its healthy growth momentum backed by its established market position and diversified product basket and established clientele. Neuland has developed more than 300 processes and 75 APIs and has filed over 898+ Regulatory filings in the US (55 active US DMFs), the European Union (EU), and other geographies.

Revenues grew to Rs 764 crore in fiscal 2020 from Rs 667 crore in fiscal 2019 and are expected to sustain the momentum in FY21. Improving scale and a strong portfolio of products will help sustain the improved operating margin at 16-18%.

Annual cash accrual is expected to be over Rs 110 Crore. Adjusted Net worth increased to Rs 428 crore as of March 31, 2020, from Rs 417 crore in the previous year and is expected to improve to over Rs 800 crore over the next two years. Gearing was 0.61 times as of March 31, 2020. Despite capital expenditure (Capex) of Rs 250 crore over the next two years for business expansion, gearing is expected to improve to 0.45-0.5 time range due to high accretion to reserves.

Source: CRISIL Credit Ratings

7 Likes

[Neuland Labs Business Analysis| Reaching Critical Mass - YouTube]

Another good video from SOIC people (Kudos to their knowledge, efforts & research behind making these videos)

Discl: Not invested yet

13 Likes

https://www.neulandlabs.com/blog/2016/12/04/api-manufacture-deuterated-molecules/

https://twitter.com/punitbansal14/status/1383714387857272832?s=20

2 Likes

In the tweets that follow the above tweet on Deuterated molecules, the company’s twitter handled is also tagged. The company then tweets a 2016 blog written by the MD. Playing to the gallery?

4 Likes

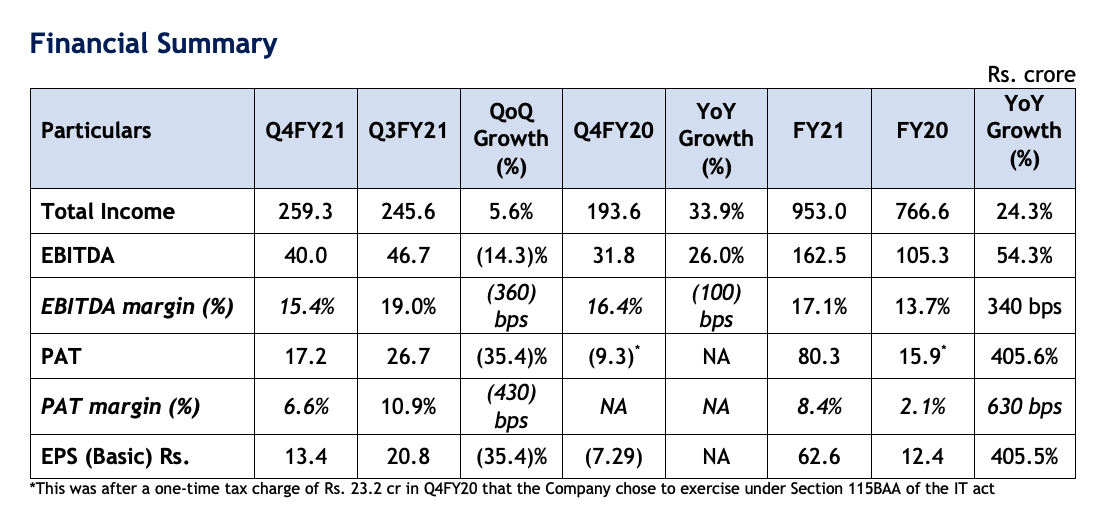

Q4 Results. https://www.bseindia.com/xml-data/corpfiling/AttachLive/96c02733-1c97-4eb0-b4f1-50c05f396ba5.pdf

| Neuland Consolidated | INR Crores | |

|---|---|---|

| Q3 | Q4 | |

| Revenue | 245.39 | 244.70 |

| Reported PBT | 31.94 | 24.39 |

| Add: Depreciation | 10.40 | 11.14 |

| Add: Finance costs | 4.44 | 4.58 |

| Reported EBITDA | 46.78 | 40.11 |

| Add: Income Tax VSVS Settlement | 9.50 | |

| Add: NGT Settlement | 5.40 | |

| Less: Real Estate Income | -13.09 | |

| Adjusted EBITDA | 46.78 | 41.92 |

| Adjusted EBITDA Margins | 19.1% | 17.1% |

Flat Revenue and Drop in Margins.

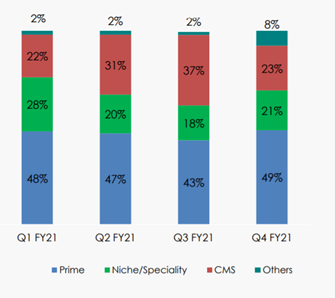

CMS revenue lower QoQ due to fall in Commercial segment.

Which has affected the Revenue Mix

Which in turn affected margins along with higher RM sourcing costs

4 Likes

CNBC Often messes up their numbers. Please consider using authoritative sources like company presentation. The correct EBITDA margins are here:

Source: Company Q4FY21 investor presentation.

3 Likes

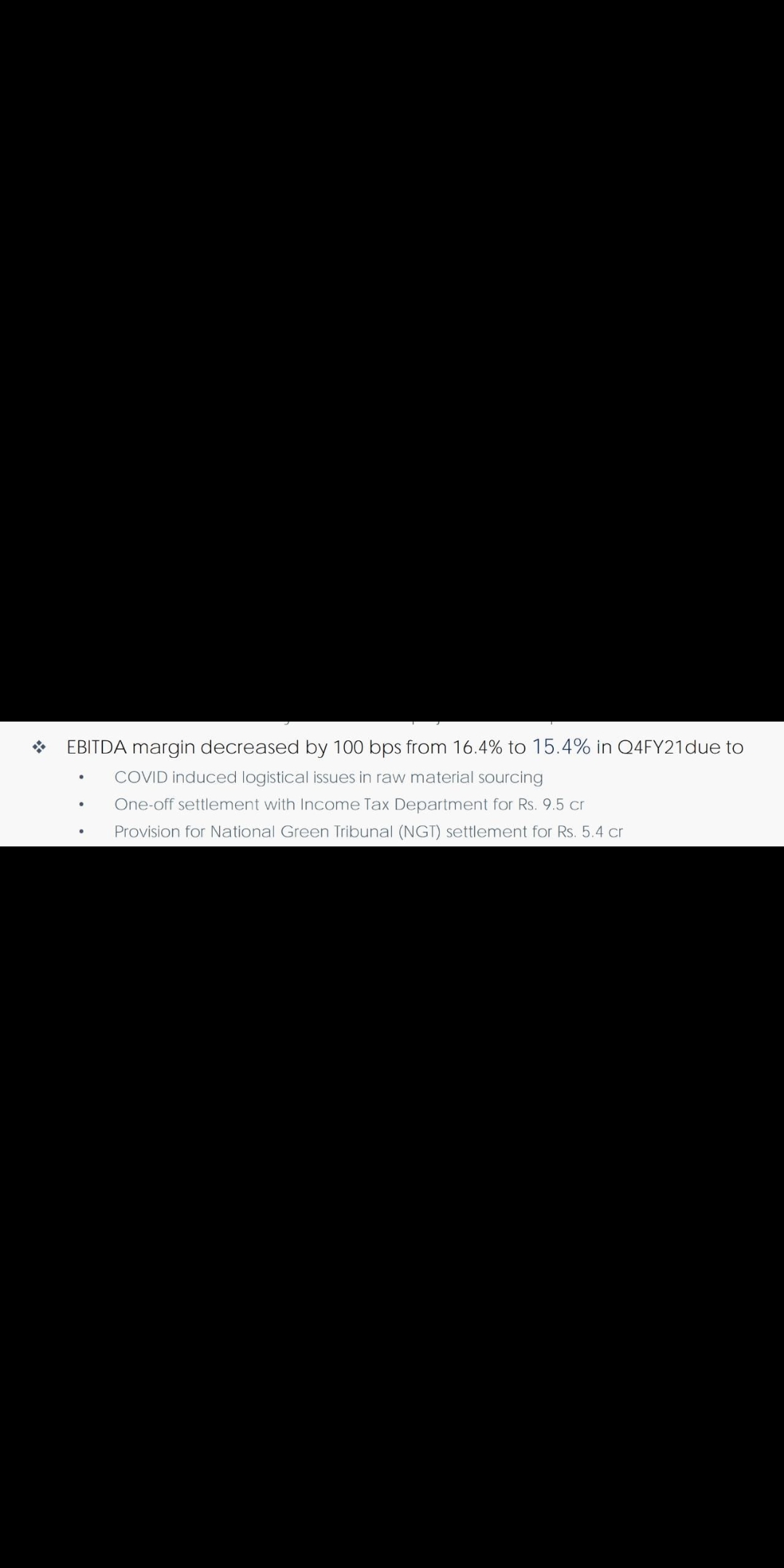

Q4FY21 concall Notes

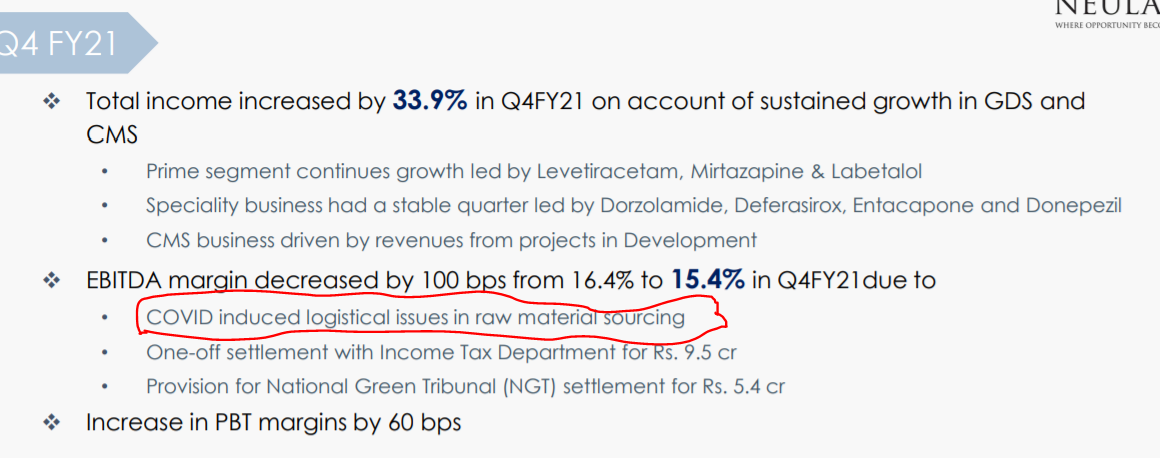

- (EBITDA margins): RM sourcing faced logistical issues due to Covid-19 lockdowns. Plus a couple of one-offs with respect to income tax and NGT settlement.

- (Why Propofol does not face more competition): China has never established itself as a credible source for complex molecules. Propofol is complex to make. Requires a very high level of compliance to manufacture it regularly.

- (Unit 3 status): 2 APIs commercialized from Unit 3. Unit 3 is where we will create more API capacity for future business. Unit 1 & 2 will see minimal investment (debottleneck). Unit 3 will see volume increases. Unit 3 will have similar asset turns to unit 1 and unit 2.

- (Manufacturing and employee costs): in Unit 3, We are recruiting many employees and there is a period of up-fronting of manufacturing costs as well which is showing up. Cost structure is the same.

- (Pricing): GDS pricing is referenced to competition. CMS are long-term contracts and pricing is flexible, we can negotiate prices by passing through certain costs. In CMS, when we are primary source, margins are higher, for secondary source, they are a bit lower.

- (Peptides): Most peptides are part of CMS PF. 12 out of 78 projects are peptides in CMS. Peptides capabilities are in Unit 1. Will further augment peptide manufacturing in this year. 2 CMS peptides are close to commercialization. 2 peptides under development in GDS. Will create further peptides capacities in Unit 3 when needed.

- (supply chain): We are making it robust. Don’t want to stop sourcing from China. Want multiple suppliers. Shorten the supply chain.

- (CMS molecules commercialization): We can expect some good part of commercialization to happen in 2-3 years time. We cannot provide more exact timelines. These molecules are late stage molecules and are in various stages including validation stages.

- (R&D spends): 5%-7% of our total spends are on R&D. For CMS it is charged to the customer.

- (CMS): Better to look at it in an annualized basis and YoY not QoQ or quarterly.

- (margins guidance): We expect business mix to continue improving and improve margins. Also expect more operating leverage to kick in.

- (Capex guidance): As of right now, we see similar kind of capex requirements in FY22. Will evaluate upcoming projects and evaluate the ROI and then make more concrete decisions regarding capex.

My Thoughts

I am quite happy with the Q4FY21 results. Key takeaways for me:

- The normalized operational EBITDA margins were 15.4%. The one-off gains (due to the sale of real estate) get balanced out by one-off losses due to settlement with income tax and NGT (both ~15cr). Ex of the one-offs. The EBITDA margins dropped a bit due to the change in business mix (much lower CMS contribution in this quarter).

- CMS pipeline is looking very robust. Molecules under development have gone up from 12 to 14 in just 1 quarter. Many of these are peptide molecules. When reasonable commercialization happens in the next 2-3 years, the CMS revenues would increase substantially.

- Some of the manufacturing and employee costs are front-loaded due to unit 3. This is also great because it implies better operating leverage kicking in in FY22 as unit 3 gets commercialized.

Edit:

Edited first point to point out correct ebitda margins based on multiple subsequent posts by people. Thanks for the corrections.

Disc: Invested. Full PF here. This is not a buy or sell recommendation or investment advice.

21 Likes

Thanks for posting. If adjusted for one offs, I feel margins are fine. Topline has done well despite CMS not contributing. This shows other segments have contributed. With CMS, the feel the revenues are lumpy and you cannot do Qx4. This even Dr.Chava had said -

Dr. Satyanarayana Chava: You cannot multiply the Q4 by 4 in Synthesis business, because there is one order executed in Q4 and we will execute the similar order in the Q4 of FY2021 also. The order book is like that. We make that intermediate for about six months and supply in one go so same thing happened in FY2019 also

4 Likes

I must say you’re quite fast in taking down and uploading the notes

I agree with your thoughts. The Q4 results cannot be termed ‘bad’ in any sense. The long term story is completely intact. The stock price correction was simply not anticipated, prolly will reverse tomorrow.

I’m not sure if this was answered, but any clue about the bifurcation of the 105 crore capex b/w the capacity increase in Unit 3 and facility upgradation in Unit 1 & 2?

It would also be interesting to see the therapeutic concentrations of the late stage molecules as Sajal Kapoor-ji asked.

2 Likes

The difference is because CNBC hasn’t considered the Other Income element (from sale of land) I believe to calculate EBITDA margin. Where the company presentation has considered Other Income. Thanks for posting the con-call notes.

1 Like

Does one time settlement with IT department reflect in EBITDA as said by management ? I thought it affects only PAT

It was most definitely anticipated, when valuations run up too high for high growth businesses, anything apart from extraordinary results lead to significant short term corrections.

Examples include Navin Fluorine domestically and Amazon internationally. Amazon grew high double digits on a huge base yet the stock took a plunging.

Nothing wrong with Neuland, the story is intact but sometimes in the short run valuations leap forward and pace faster than fundamentals do. Hence the correction.

D: Not invested, tracking

5 Likes

To my understanding, had they accounted it as tax expenses, it would not have affected EBIDTA. But thay treated it as Other Expenses hence the effect on EBIDTA.

1 Like

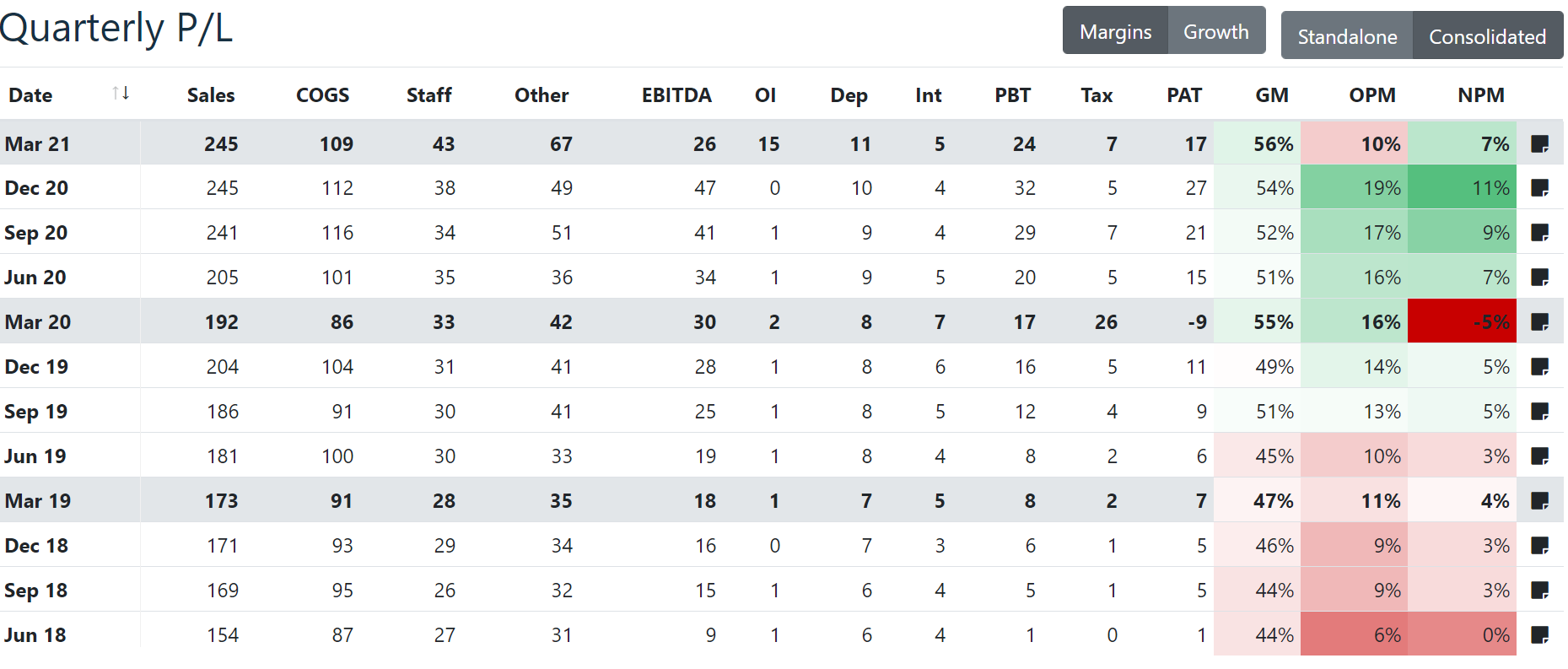

This can’t be right. The one-off is an addition to the topline, so if it is ignored, margins should be lesser not higher

From the standpoint of having a comparable EBITDA (operational EBITDA), the company perhaps shouldn’t have used the other income in its topline as it is misleading.

Especially since the “Other Income” reported is a one-off from a real-estate transaction

If you ignore this amount in the topline and then calculate the EBITDA, the margins are at 10% (see the OPM column)

CDMO businesses are lumpy and uneven so this might be nothing to lose sleep over but having a proper understanding of the numbers reported is important.

One more thing to keep in mind is that the narrative was towards improving and sustaining of EBITDA margins than in the past (From 10-12% levels to 20% levels). When a business improves margins from 10% to 20%, the corresponding improvement to return ratios is dramatic and sometimes even valuation switches from P/E to P/S when margins are higher and stable. When that belief gets questioned, we must recalibrate valuations and our expectations accordingly.

Disc: Have traded in the past (Have a much reduced position from that trade)

P.S. Noticed the 9.95 Cr tax settlement included in Other Expenses. Looks like this will bring the EBITDA margins up to 14.49% if ignored (while also ignoring the real-estate transaction from topline). So this is most likely the accurate number from the main line of business.

33 Likes