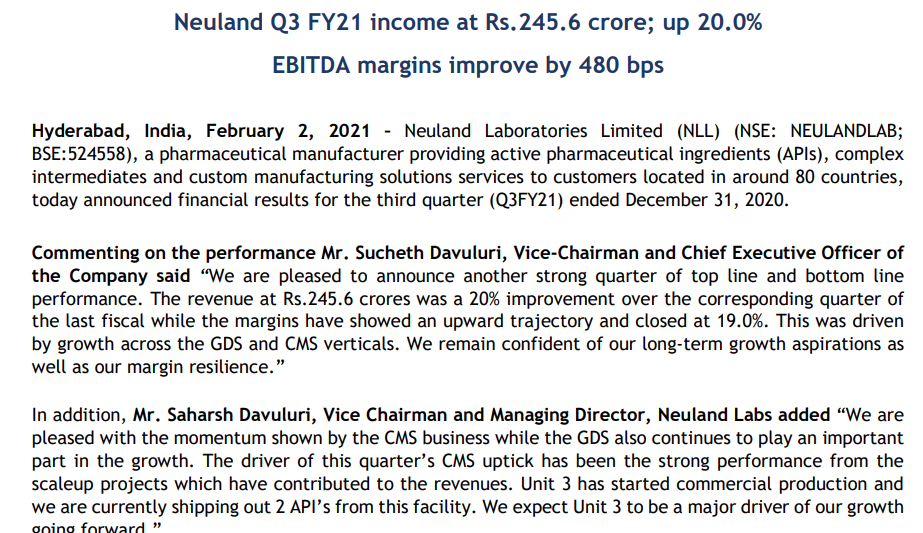

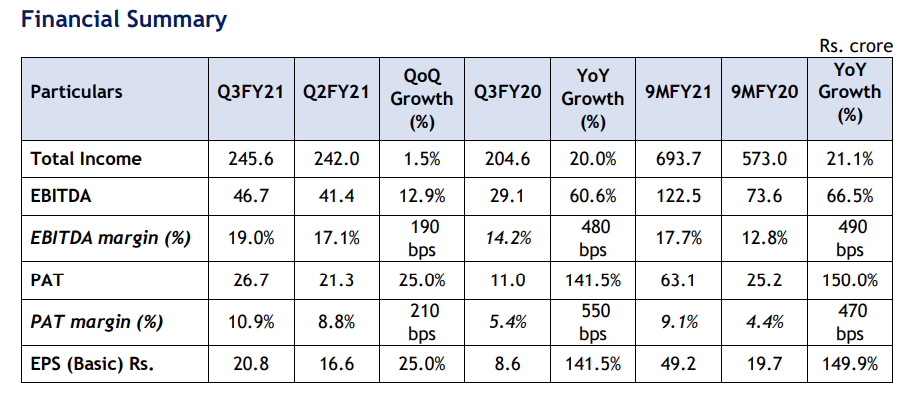

In my opinion, very good set of results from the company.

Good product mix especially with CMS (custom mfg.) contributing…

Both GDS and CMS have contributed per mgmt.-

Margins have started to expand, which mgmt. have been talking about for the past few quarters. Increase in margins:(YoY)

EBITDA margin by 350 bps

PBT margins by 520 bps and

PAT margins by 420 bps

Trigger for further growth - “Unit 3 has started contributing”

Continue to monitor - the # of molecules going into the Dev/commercial stage. Good to see the dev and commercial-stage scaling.

50% additional. Unit 3 has roughly same capacity as other 2 units. This information is there is one of the concalls (I think one of the FY21 Concalls).

Neuland had acquired a multiproduct facility (known as Unit-3) of Arch Pharma Labs Limited from JM Financial under insolvency process, in December 2017. This facility is spread across 12 acres and has a capacity of about 197 kiloliters for manufacturing APIs. It represents a 40% increase in terms of total manufacturing capacity for Neuland. It has five production blocks for API manufacturing as well as advanced intermediates manufacturing.

Unit-3 will be used as backward integration for some of its products, to reduce dependence on raw materials from China, and it will also be used to manufacture APIs for regulated markets after getting the necessary regulatory approvals. Unit-3 has started revenue generation from Q2FY20-21. The capital employed in Unit-3 is around Rs180 crore. For FY20-21, the management has indicated capex to be Rs90 crore which will partly be for maintenance and partly for capacity expansion. As per the management, considering the opportunities, there may be need for additional capex. It has already employed Rs57 crore for capex in the first two quarters of this year.

Source: Moneylife

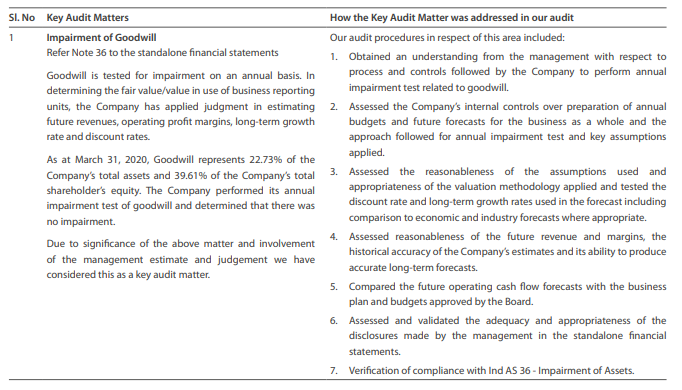

Company has been carrying a goodwill of 279.46 Cr on its balance sheet since many years. Any idea what is this amount stands for. Moreover, company not amortizing this goodwill and I found the following justification in the annual report. Company saying they are not amortizing goodwill and is mandatorily testing for impairment as per Ind AS 36. What happens if company start charging this amortization? IMO, This may dent the P&L hugely and of-course cash flows are intact.

[I am invested and continue to monitor] Does anyone know why Neuland originally said(as recent as November) that Unit 3 would be used for backward integration of key intermediates but has not gone ahead on this plan. Of late they are talking about sourcing key intermediates from India(instead of china) but not about bringing the manufacturing of said intermediate to Unit 3(which they mentioned they had the knowhow already[said in Q3 2019 Concall if my memory serves me right]). In the absence of serious backward integration Neuland(and most pharma players who depend on china) will be exposed to risk of intermediate price fluctuations(which has plagued the industry for the past couple of years).

Welcome thoughts from veterans.

IMO, not having the new unit contribute to backward integration is a completely operational decision : one needs to trust the management unless one has superior insight/experience/knowledge about running API companies. Backward integration is a double edged sword. One cannot backward integrate for everything: it can actually be margin reducing activity unless Neuland has any specific advantages. Also, each unit of capacity used for backward integration is a unit which would not contribute to top line growth.

Thanks much for the amazing work that you have done on Neuland.

I primarily had 3 aspects for my thesis on Neuland

Growth in GDS business

Improvement of margins in GDS due to Unit 3 backward integration

Niche API business(am considering CRAMS will be feeding high value API’s into this business)

Based on ongoing monitoring I am reasonably convinced they are on track to deliver great results on #1.

Of the above #2 is outstanding and since Neuland had made an announcement that they are planning for backward integration but did not find a single candidate for backward integration in the new site Unit 3 - this comes as a surprise. None of the conceals or notes above indicate Neuland’s clarification of why they did not believe any RM or intermediates qualify to be made in-house whereas they themselves had indicated so in several con calls.

Could this be because nobody asked them the question? In general, I’m not sure management would clarify each and every future predictions in concalls. Please feel free to email the investor relations with specific questions. Let us see what they say. . When one’s data changes, one changes their opinion. Estimates about the future are dynamic, and bound to be updated based on new data. We could try to hazard a guess as to why they chose not to backward integrate, but IMO best course of action is to email the customer relations. If possible to join the concall and ask the question directly to management.

For me personally, the improvement in GDS would come from

Scale: They get larger orders from existing customers. Fixed costs get amortized.

Process improvement: In fact this is one of the 3 key technical capabilities Neuland brings to the table (check out their brochure from their website)

On this question I think backward integration is something that we are looking at very carefully especially since the China situation erupted a few years ago and we had one financial year specifically where we got stocked out on Levetiracetam and we had huge financial impact. I think since then the organization has made strategic move on de-risking ourselves and as part of the de-risking strategy backward integration has been a key part of that strategy So, even I can share the broad numbers and may be Sucheth can throw more color on this, but compared to three, four years ago where we were buying may be 45% to 50% of our raw materials from China, today we are buying 20% to 25% of raw materials from China. Not all of that has happened because of backward integration, but some of it has happened because of our ability to find local sources to be able to do technology transfers, to be able to integrate them well into our supply chain. But yes, in certain cases especially where the products are very important and the sartan materials are complex. For example, SABAM for Levetiracetam or some of the other starting materials for our CMS project, we have intentionally used our unit-3 for backward integration and we will continue to use that strategy where it makes sense. What we do not want to do is blindly backward integrate on all our products because that is something necessarily may not generate more value or more margin going forward especially when you have seen a surge in good reliable Indian intermediate and sartan material suppliers.

Note that Levetiracetam is actually a GDS product. So, they have done some backward integration in Unit 3.

Again in very simplistic terms, if a KSM or intermediate would cost Neuland say Rs. 150 to manufacture but the same thing can be reliably purchased from an Indian company, with all the quality checks in place and integration in to supply chain can be achieved seamlessly, say for 80 or 90 or 110, why would they want to invest the time in their own unit and reduce the capital and resources that would get tied to it? On the other side say it would cost 140 or 145 or thereabouts, then probably Neuland can do their own cost-benefit analysis and implement them in-house.

Wanted to share my updated understanding of Neuland Labs. Up front apologize for the very long read. This post has been months in the making (please see Raw data sources section point 1 for why its been months in making). This is largely based on reading even more concalls, more ARs and also looking at Neuland DMF filings and Neuland Process patents.

The story of neuland can be understood in six broad strokes:

The change in business/product mix (Q).

The competitive advantage or the part of the business which makes it differentiated (Q)

The quality of the management (Q)

The growth in the underlying business (G)

The longevity of the business and the growth (L)

The valuation of the company (P)

In this post, i only spend time on the first 3 (quality) because in my opinion that part is most difficult to understand and requires a lot of reading.

The change in business/product mix (Q)

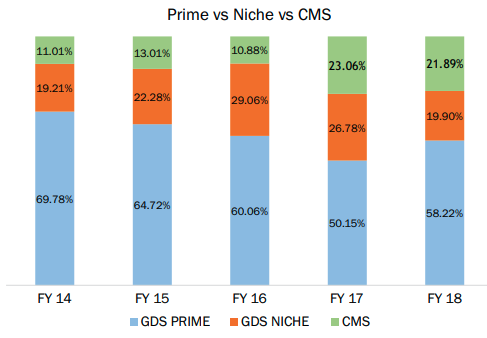

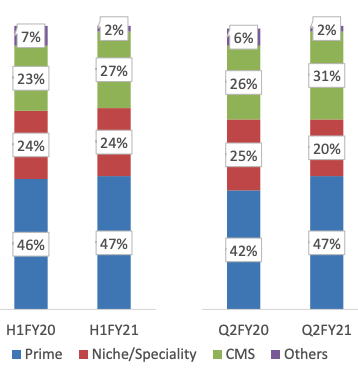

Neuland used to sell only Prime segment APIs (these are mature APIs, have been around for lot of time and have many competitors) in the beginning. Business mix is changing with low volume high value specialty APIs and CMS (CDMO) segment revenues rising. This is shown in graphs below:

Prime revenues used to be 70% in 2014 and CMS used to be 11%. In Q2FY21 it is 47% for prime and 31% for CMS. This causes an expansion in margin.

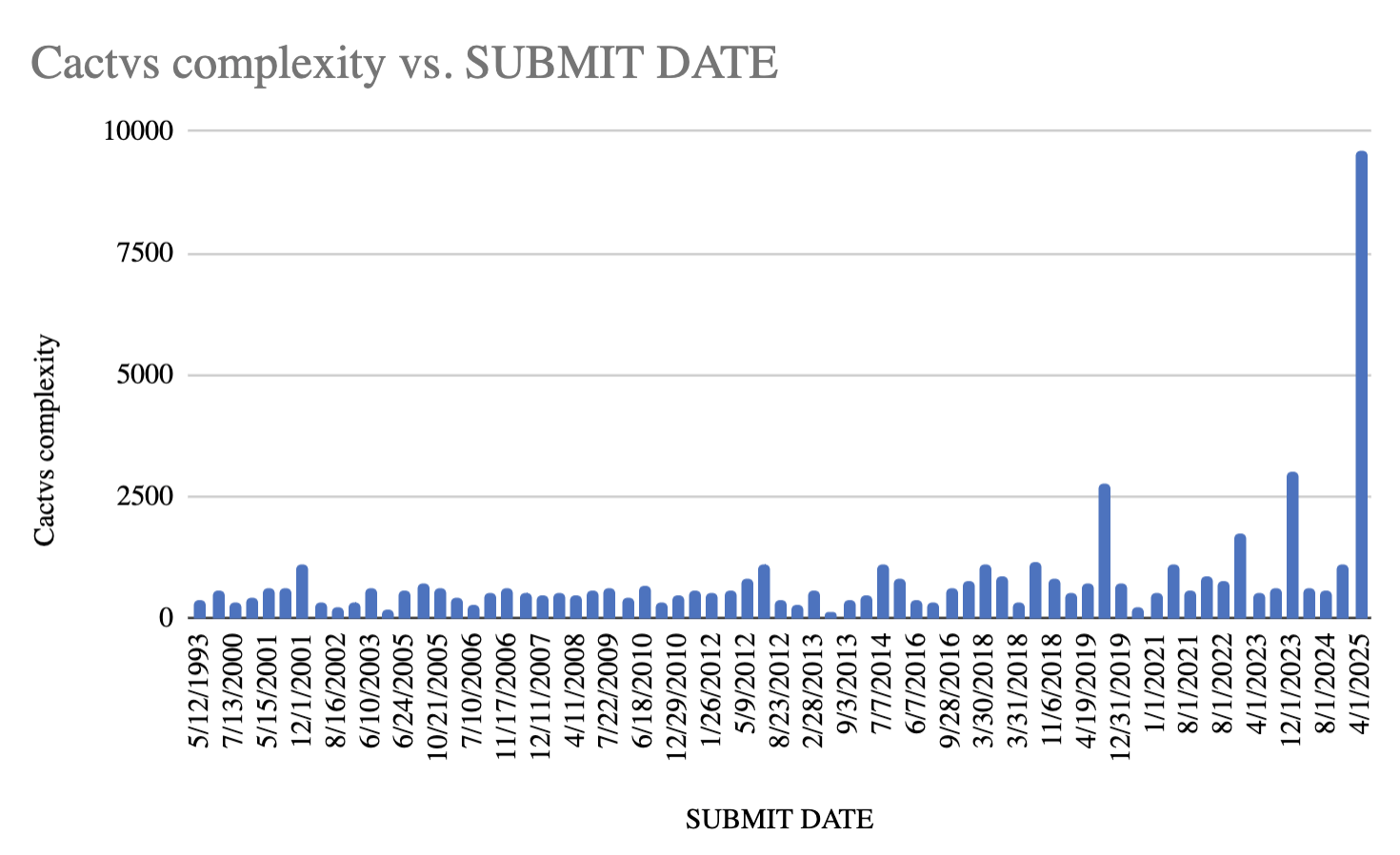

The next level of research I did is to go through the USDMF filings to understand the complexity of the APIs for which Neuland is filing DMFs. https://pubchem.ncbi.nlm.nih.gov/ has very good data on many aspects of each chemical including APIs and intermediates. That has a section on complexity of the molecule which is computed using the Cactvs model. I have plotted these as a function vs time. The molecules for which DMFs have not been filed yet were randomly distributed to occur once every 4 months (assuming 3 DMFs every year) to obtain following graph:

One can clearly observe that the complexity of the molecules for which DMFs are being filed is increasing over time. This serves as a further validation of the narrative of changing business mix towards more complex, high value APIs.

The competitive advantage or the part of the business which makes it differentiated (Q)

Neuland has been aggressively investing in building the right workforce. While sales only increased 14% from FY19 to FY20, number of scientists working for neuland increased 40% YoY from 200 to 282.

One of the best primary sources on Neuland’s competitive advantages is the brochure they have on their website. Neuland Labs has published peer reviewed article on PharmTech sharing a newly developed strategy to increase sample loading for peptides 12 fold compared to conventional Prep-HPLC techniques. High quality Science & Research is certainly not the hallmark of a commodity. Neuland has been investing into this space for over a decade. Imagine the scientific leverage which is building up here.

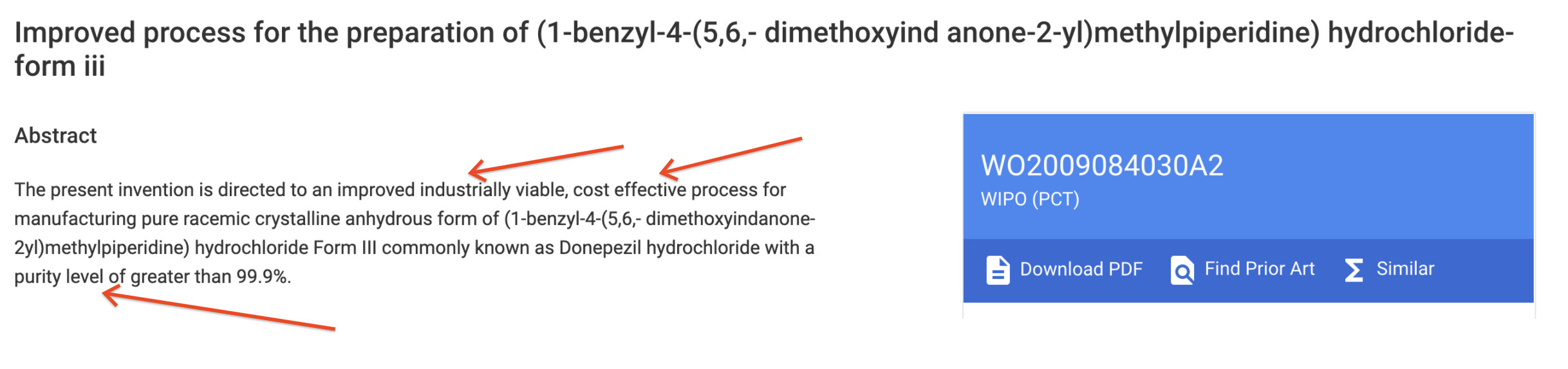

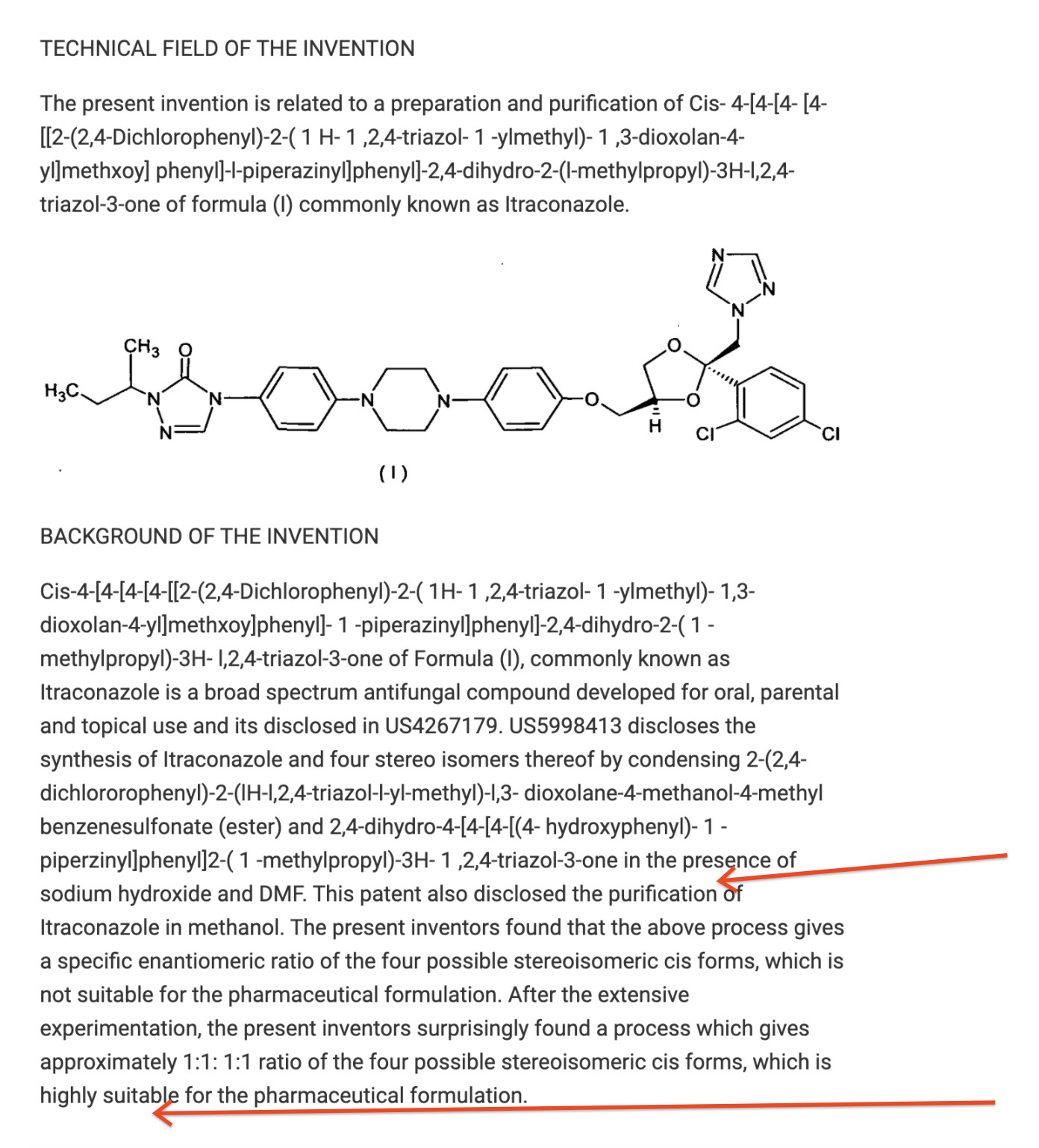

Even among the output (API) is commodity-like (prime APIs), a scientific organization finds ways to build a competitive edge. Operating leverage and scale advantages are benefits that any and every company would apply. But neuland has gone ahead and filed multiple Process patents for these APIs. These process patents demonstrate their appetite for applying their research acumen to improve the manufacturing processes and drive efficiencies:

“Industrially viable”, “cost effective”, “high purity”, “easy handling”, “eco friendly” are words we see repeatedly in the patents.

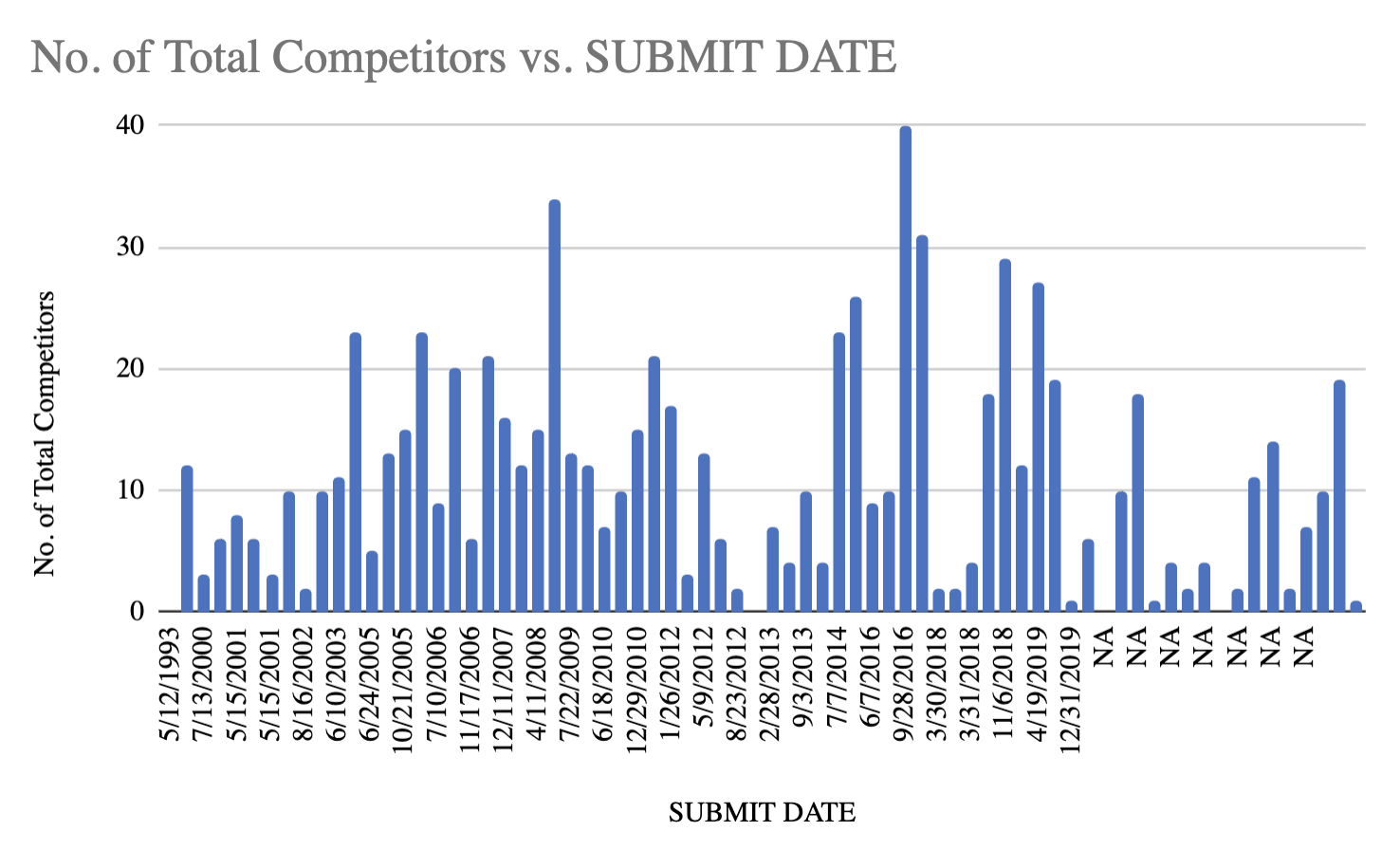

4. The newer DMFs have much fewer competitors. The ones with NA date, DMF has not been filed yet. Meaning that these are yet to come in the future. There is an element of time bias here but we can still see that newer molecules definitely have much fewer competitors than older ones:

The business suffered two severe down years in FY18 and FY19. A key part of how I judge managements is how they communicate in down years. Both these annual reports are a treat to read.

From the FY19 Annual report:

From the FY18 Annual report:

Every time the business underperformed, the management clearly outlined the problem, talked about concrete remedial steps and one can see them walk the talk as well through the various concalls. As i have outlined in previous posts, management has been very conservative in giving growth guidance which is another thing I like about the management. This is unlike many other API players who guide for 25% growth to come for many years. Another aspect of the management which i find appreciable is the compliance culture they have build at Neuland. In 30+ years of operations, they have been audited 30+ times by USFDA and have not had any warning letters. The compliance track record and culture itself is a huge competitive advantage for Neuland. Management has talked about how they conduct mock USFDA drills in order to maintain this trackrecord.

Open Questions/Risks

There are several things I still do not understand about the business. As per Warren buffet, risk comes from not knowing a business. To that extent these represent the risks in the business:

Looking at our 70 odd API molecules portfolio that we work on, why do we continue to file USDMF for APIs with 15-20 global competitors (eg: Sugammadex Sodium, Ticagrelor, apremilast, posaconazole) even after 2018? These APIs seem like the ones where competitive intensity is high and we should understand whether neuland has any unique or competitive advantages in manufacturing these molecules that lead us to filing these USDMFs.

Given that our CMS portfolio has much higher profitability and margins, why do we not spend all incremental capital on CMS business? Is it due to a limited demand for the capabilities or some other reason? We understand the business viewpoint of continuity for all existing molecules, but why do we continue to deploy capital into newer prime or speciality APIs which have higher competitive intensity and lower profitability?

We suffered loss of production in Q42018 and 2019 due to raw material shortages due to supply disruption from China. If the same issues were to repeat today, how much would our topline or bottomline suffer? Trying to get a sense for the extent to which this risk has now been mitigated with the strategic backward integrations, geographical multi-sourcing and fungible capacities.

Caveats

I have not analyzed market share size for molecules and molecule pipeline. I find these exercises not that useful. Look at this HDFC securities 2018 research report for Neuland. I quote: “Beyond two year time line, there are many lucrative API opportunities where NLL is working on. This list includes Sugammadex, Paliperidone, Posaconazole, Deferasirox, Dabigatran, Lurasidone and Bosentan. Some of these molecules are low volume products but could add meaningfully on EBITDA line”. Sugammadex today has 19 competitors. I do not think anyone has much skill in predicting market shares for molecules since we absolutely do not know how competitors pipelines would evolve.

Raw data sources

Here is the Neuland DMF Analysis google sheet. Thanks to @YachnaBhatia for the idea of setting this up and also helping populate a large part of this sheet. Rows marked in green represent molecules which we found to be interesting.

The data in this sheet is in turn derived from raw USDMF data.

Neuland brochure has a lot of good info on sources of competitive advantages.

The almost infinite number of articles on Neuland’s website which help clarify their business.

Sahil, manangement had clarified that it takes time to add new customers and gradually molecules move from Stage 1 to Stage 3 and then commercial production. Current capacity expansion should be good enough for the next 2 years apart from regular maintenance Capex and slight capex here and there.

All of that makes a lot of sense. my only question is: why deploy incremental capital towards prime APIs (incremental Prime API USDMF filing+production) which are low growth, more uncertain, higher competitive intensity and lower margin? It’s ok if company grows only at 10% topline and foregoes of the extra 2-3 prime APIs which i think is a sub-optimal capital deployment decision (unless there is some reason they want to deploy incremental capital into Prime APIs)

Sahil management has clarified that block 3 will help them optimize production. Now it will be interesting to see where they do incremental capex. From a capital budgeting perspective, whatever management had spent historically is a sunk cost and CMS business has scaled up just recently. Now, if management can keep making money in any incremental capex, only then it would make sense on spending on Prime API.

I think we will have to closely watch where they do capex in the next 2 years.

One of the key molecules under CMS segment is API for Teva’s Austedo (API name Deutetrabenazine) - which continues to grow very well. And Teva has given a YoY guidance for CY 21 of $950m which is 50% up YoY.