I was going by the company reported ebitda margins which are generally the operational ebitda. My bad that I didn’t realise they had added the non operational real estate transaction gains to the ebitda. The one-off i was talking about was on the expenses side, not the real estate gains.

The real quantum of the one off on expenses side is ~15cr including 2 separate tax matters (income tax liability and nct settlement). Both of these are explained in the investor presentation.

The normalized operational EBITDA margins will end up being close to what company reported due to one-off gains and one-off losses which are roughly same in quantum.

IMHO a discerning investor’s expectations were always for a CMS business which is lumpy in nature. Until it hits a certain critical mass, there are bound to be QoQ variations. As the business mix changes more in favor of CMS and prime APIs reduce as percent of topline, the margins would become more stable as well. Until then, some lumpiness is to be expected, both in business mix and thus in margins.

To add there was clarification on the other income. They have sold some stake in property to fund expenses to be incurred on development of that property.

They have booked income from sale but have they recognized expenses to be reimbursed to developer??

Whether the belief of margin improvement is questionable or not, is the real question. I think basis the evidence we have, the reduction in margin is more because of lumpy nature of revenues for certain business, and is not an indicator of a halt on medium / long term margin expansion. This present correction seems like an over-reaction to me, which will happen in auction driven markets. And looking at the volume of pending sell orders, won’t be surprised if we have some more downside. Offers a good opportunity to enter / add.

Disclosure: Have a tracking position and will use this correction to add slowly.

Niche GDS: Quarterly revenue run-rate has been 50 crores (+/-10%) for the past 6-7 quarters. Idea was to grow Niche in GDS (high margin, more complex) and Prime (low value add) to have a low single digit growth, though the reverse has happened.

Capex: Where have the 100+ crores in FY21 been spent? The installed capacity as reported is 730 KL since FY18.

Tax: What results in the massive difference between cash tax outflow and accounting tax?

Hyderabad land: 1/ Revised area available for sale/lease is 170k sq. ft. What was it earlier? 2/ Does the 120k sq. ft. sold in Q4 reflect the payment to the developer for converting cold shell to warm shell?

Peptide API: Had guided to file for their own product in FY21, seems to have been delayed by 2y.

High growth in GDS business, stable growth in CMS business. GDS volume growth led by Levetiracetam ( for epilepsy ), Mirtazapine ( anti-depressant ) and Labitalol ( anti-hypertensive ). Speciality APIs had a diversified base of molecules - Dorzolamide ( Opthalmic use ), Deferasirox ( to treat Iron overload in body ), Entacapone ( to treat Parkinson’s disease ), Donepezil ( used in Alzhimers treatment )

CMS business - focusing on some key projects that are approaching commercialization. Key CMS geographies - US, Japan, EU. CMS business to be lumpy on Qtly basis. To show good growth on yoy basis. Unit - III ops gradually commercialized on product wise basis. To show good growth in next 3 yrs.

Replying to Questions by Sajal Kapoor on Chinese strengths and weaknesses in API manufacturing, management said the following - China was never strong in making complex or speciality APIs. China is strong in Anti-biotics and certain synthetic APIs and thats where their strengths are limited to. Eg - Propofol ( to induce sleep ) is complex to make, requires high compliance levels. Here the Indian manufacturers have a lot more credibility.

CDMO APIs in commercial production - total six at present. Their names and therapies were not disclosed due confidentiality attached.

Presently - 02 APIs being made in the new Unit - III. Will make more APIs here - both GDS and CMS molecules. Most new molecules will come up from Unit-III. Unit -I and II will only see de-bottlenecking of existing molecules and other modernization capex. Rest of the capex will be at Unit-III. Current contribution from Unit - III is minimal. Going fwd, it would be substantial.

Qtly increase in manufacturing and employee costs due initial commercialization of Unit - III and spending thereof.

Peptide molecules are a part of CMS pipeline. Over a dozen peptide molecules are currently in pipeline. Peptide facility is in Unit-I. Further peptide capacity will also come up in Unit-I. Two peptide molecules are nearing commercialization within the CMS pipeline. Two more peptides are a part of GDS portfolio that too are nearing completion.

Some CMS molecules are in Phase III and some have completed Phase III. But it takes time for them to be commercialized as these are for regulated mkts. Commercial success is another factor. A 2-3 yr time frame should be fair to commercialize the company’s pipeline.

Q4 revenues ( talking about CMS business ) are not indicative of what is expected in the future. Going fwd, things look far more promising on an annualized basis. CMS revenues for FY 21 were 280 cr vs 189 cr last FY. As new molecules get scaled up and commercialized, growth is expected to pick up.

The business Mix is expected to improve going fwd which should lead to better margins. Real picture should start to unfold in another 2-3 Qtrs as unit -III ramps up.

Neuland came with a decent set of numbers with healthy yoy growth but muted qoq.

The company has a good pipeline of molecules and many of them in late stages (a proxy for strength of the business)

The metrics weakened a bit this quarter but thats partially due to a one time expense and partly the CMS being lumpy.

Is this correct or not?

Well if we look at peers doing a similar cms business we can corroborate this.

Neuland might become more and more secular as the business scales up but till that time this may happen again.

Is future secularity an assumption?

yes and no both.

Yes because if we see 2016 onwards as and when cms revenues have started accruing to today we have seen better secularity so its an ongoing thing.

No because you cant predict the future of the molecules their utility and demand strength.

They have to reach a scale where they are getting orders for one or more products all the time ensuring consistent growing revenues which cant happen with the current no of molecules. Eg

they are producing the API for a drug called “Austedo” for use in Tardive Dyskinesia, a disabling condition that develops due to use of anti-psychotic drugs; so will the orders be on a monthly basis or few times an year?

(They have mentioned it many times about the aspirational neuland growing 20% annually with 20% margins)

Unit III capex and utilisation will need to be monitored.

Bottomline is The business has a decent track record, they are doing good stuff and should scale up but its going to take time.

Share price movement is a different story altogether.

Good that it ll become more anonymous as many will forget it now as too much public spotlight is one reason for such crazy uphill/downhill moves.

Discl: invested at lower levels. (This is my ustding of the business & I may be wrong)

Neuland available at 3x to sales…best not to overanalyse results. If you were bullish you cannot change your stance on the biz or sector over 1 quarter. Regardless I thought the numbers looked good year on year. In the pharma basket this looks the best for a re rating and can be a massive winner in the years to come.

You are right but It is already rerated. The question is whether they can maintain EBITDA margins going forward. The doubt caused so many discussions. Lets see in Jun or before that

You are absolutely correct the stock was re rated all the way up to 2800. The results were not up to the mark hence the massive correction which may not be over. Now excessive pessimism is building and it is not worth speculating on the price in the short term. If you believe in the business going forward and the industry then according to me it is a great value price. Please look at the molecule pipeline and the areas which Neuland is targeting. I can’t find any other company making inroads in these segment. The market wants results every quarter which is not possible. I would say it’s a great time for long-term investors.

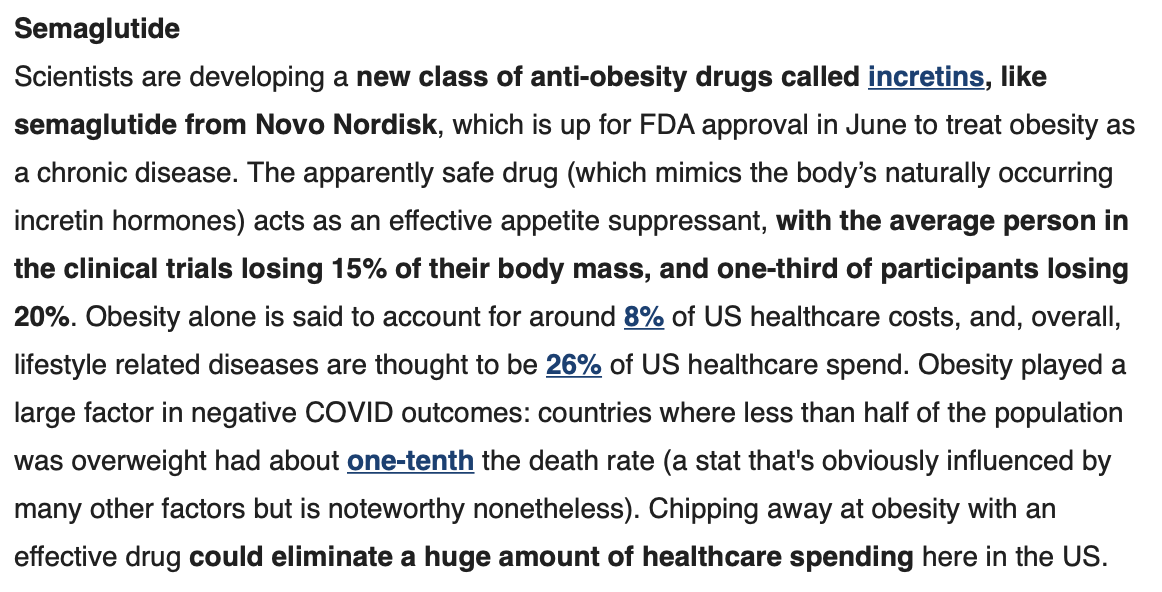

Semaglutide is an incretin as mentioned above, actually a Long acting GLP-1 agonist and is approved as an Anti- Diabetic Agent (Oral and Subcutaneous forms).

This is also being found relevant for other uses like obesity.

Neuland has received approval for Rotigotine CEP from EDQM. Rotigotine is a non-ergoline dopamine agonist indicated for the treatment of Parkinson’s disease (PD) and restless legs syndrome (RLS). Neuland is the first CEP holder for this API.

Sir, my first question is on recent disclosure to the exchange regarding downward revision of

some land agreement, area that we were supposed to receive, so if you can just throw some light,

you have sold some 120,000 square feet this quarter which we mentioned in the disclosure, some

complete picture on what is happening there?

"The background of this is that Neuland has a piece of land in Hyderabad which we had determined that we would not build our own facility over there and we had decided to enter into

a joint development agreement with a real estate company. As a result of that partnership, the

real estate company actually created a large piece of commercial real estate in which Neuland

was entitled to some square footage of the building. As per the agreement that we had with the

builder that square footage was in the form of what is defined in the real estate world as a cold

shell. Now that cold shell meant that the building would still need to incur certain investments

from us to convert it into a warm shell which would be for work involving false ceiling, ducting,

piping, etc., And as part of our agreement we had to pay or reimburse the builder certain amount

for these cold shell to warm shell expenses which the Board felt was better by actually selling a

part of the square footage of that building and giving the proceeds of that sale to the builder so

that you would not have to pull funds out of Neuland’s core business and that decision had

resulted in us having to reduce our square footage from the original building and by reduction

what we did is that reduced amount of square footage was actually sold back to the builder at

the current market price and the consideration that we received for that was what we reimbursed

the builder for converting the cold cell into the warm shell. So, I think as a result of this process,

which was disclosed on the stock exchanges, now whatever remaining square footage is there

about 1,70,000 sq.ft. or so, is warm shell that is ready to be occupied and is going in position for

the company for either a long-term lease or any other kind of occupation and the expectation

of the board and the management is to use the proceeds from such long-term lease or anything

for again investing into our core operations. So, that’s the background very broadly. I hope it

answers your question.

The valuation of this Real Estate will be around Rs 144 Cr@ 8500/- Per Sqft.

At conservative rental value of Rs 85/- per month the Annual income from this asset can be around Rs 17.34 Cr.

The Company can discount the future lease and get around Rs 100 Cr for its CAPEX and other requirements. (The future lease discount loan of Rs 100 Cr will be self sustainable as it will be paid out of cash flows of rentals received from lease).

A total of three manufacturing Sites - Unit - I, II and III. Units I and II have sucessfully cleared 15 USFDA audits. Unit III is awaiting FDA inspection and approval for commercial manufacturing of APIs.

Two business verticals -

(a) Generic Drug Substances - making generic APIs. Sub-divided into two divisions - Prime APIs - High volume and Mature APIs , Specialty APIs - Low volume and complex APIs

(b) Custom Manufacturing services ( CMS ) - catering to innovator pharma and biotech companies through exclusive contract development and manufacturing of NCE APIs

Current revenue breakdown -

Prime APIs - 47 pc

Specialty APIs - 22 pc

CMS - 28 pc

Others - 3 pc

FY 21 - Revenues at 953 cr, up 24 pc. Ebitda at 162 cr, up 54 pc. EBITDA margins up 340 Bps. Current Debt / Equity at 0.22 pc. Greater contribution from CMS and certain specialty business led to margin expansion. Company continues to focus on CMS without compromising on GDS business.

Company working to improve processes, yeilds and productivity. Concrete steps taken during the year for products like - Ezetimibe ( to treat high cholesterol ), Levetiracetam ( anti - epileptic ), Deferasirox ( prevents iron overload ), Donepezil ( to treat dementia ), Dorzolamide ( opthalmic medicine ) and Rivaroxaban ( anti-coagulant ) - to make them more competitive in terms of cost and availability.

Growth drivers for FY 22 - Strong CMS pipeline of 78 active projects with 24 in late stage development. Commercial production commencement at Unit - III. Already shipping 02 APIs from the same. Also gives them the headroom to accommodate higher volumes for molecules already being made at Unit - I and II.

In FY 21, GDS business growth was led by - Levetiracetam ( anti epileptic ), Mirtazapine ( anti depressant ) , Labelalol ( to reduce BP ) in the Prime segment and by Deferasirox ( to treat iron overload during blood transfusion ), Dorzolamide ( opthalmic drug ), Entacapone ( to treat Parkinson’s ) and Ezetimibe ( to treat high cholesterol ) in the Specialty segment. Company having 6-7 molecules in late stage development stage ( talking about Generic APIs ) - to be launched this year.

Prime APIs - total 15 in number. Imp ones - Ciprofloxain, Levetiracetam, Mirtazapine, Enalapril, Sotalol, Labetalol. Company aims to keep leadership position going in key molecules by investing in lifecycle management initiatives ie improving yeilds and productivity.

Specialty APIs - higer value, higher margin, complex molecules. Key company strengths - Chiral chemistry, Hydrogenation and inhalation products. Company makes 20 molecules in this segment.

Company aims to launch 18 more molecules under its GDS business over the next decade. Will file 05 DMFs over next 01 yr.

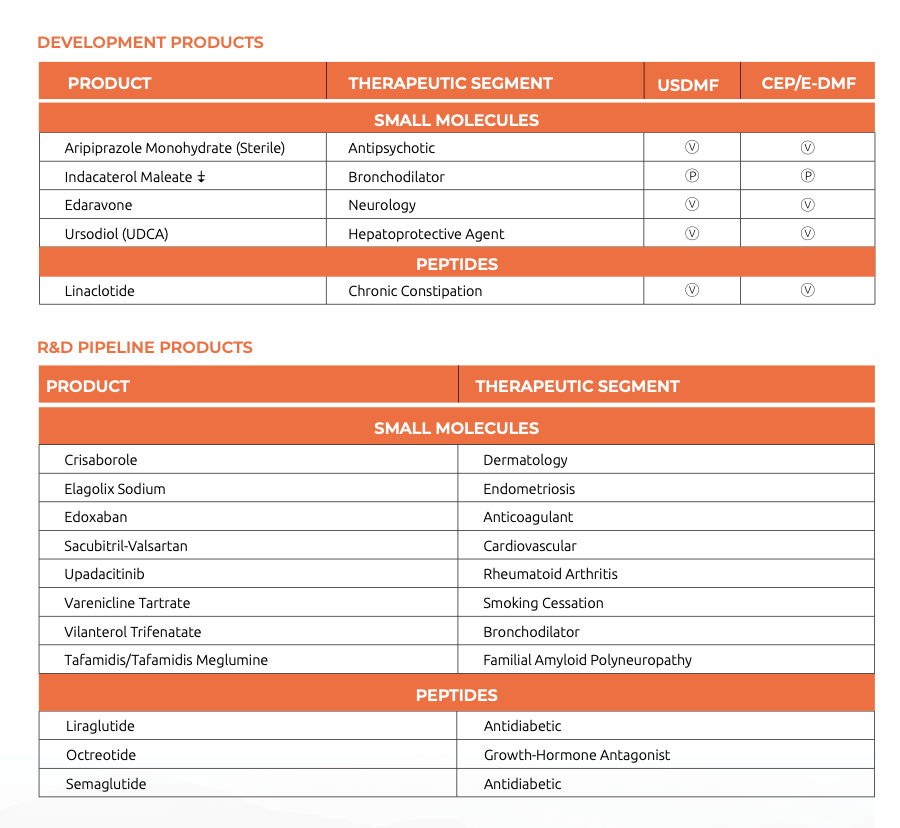

Three generic peptides - Linaclotide ( to treat irritable bowel syndrome ), Liraglutide ( anti diabetic ) and Semaglutide ( anti diabetic ) are in various stages of development.

New molecule addition in GDS business - Sugammadex ( to reverse neuromuscular blockade ), Elagolix ( to reduce endometriosis induced pain )

Update on CMS business - 78 active CMS molecules in portfolio, 17 of them in commercial stage, 20 of them in development stage and remaining extending from early clinical trials to phase - III trials. In recent years, company witnessing increased number of late stage molecules entering their pipeline - this being a good trend as failure rates are lower here. Significant progress made in 4-5 late stage products which are expected to be commercialized in next 12-24 months.

CMS business revenues for FY 21 at 269 cr, up 42 pc. Company also has a few peptides under development in the CMS division.

Dependence on Chinese imported RMs - down to 20 pc from 40 pc FY 18. Company aims to bring it down to 10 pc by FY 24.

[neuland]: Supported by our world-class manufacturing facilities and complex chemistry capabilities, we have become a trusted generic and new chemical entity (NCE) API manufacturing partner and supplier to some of the biggest names in global pharmaceutical industry.

[manufacturing]: Our facilities (Unit I and II) have successfully cleared 15 US FDA audits, a testimony to the reliability of our systems and processes.

[R&D]: Our R&D facility has proven its capabilities in carrying out a wide range of reactions, including bringing complex molecules with efficient processes to market; developing non-infringing processes; developing cost-effective routes; reducing impurities levels by better process understanding; and reducing effluent generation.

[CMS]: CMS segment description: Catering to innovator pharmaceutical and biotech companies through exclusive contract development and manufacturing of NCE APIs

[GDS}; uptick in GDS business was led by customer acquisition and our continued efforts in product lifecycle management

[CMS]: CMS business is seeing the fruition of our sustained focus on building strong customer relationships and the right pipeline of projects

[GDS]: The knowledge and skills of our R&D team also play a critical role in sustaining our market position in the GDS business.

[Supply Chain]: have been proactively pursuing supply chain diversification over the past few years to reduce our dependence on any single geography

[tech]: have been accelerating the integration of technology in our operations to leverage greater efficiencies.

[Human Resources]: actively looking at bringing the best global talent for strategic roles and providing them with the right kind of environment so that they can perform

[Sales]: We are working towards enhancing our customer base in our key markets of the US, Japan and Europe, especially in the context of our CMS business.

[management quality]: CEO: “ I address some of the key questions the reader may have. The endeavour is to communicate with transparency and provide insights to enable our stakeholders take an informed decision on the Company. ”

[business strategy]: an increased focus on growing our capabilities and our Custom Manufacturing Solutions (CMS) business without compromising on our Generic Drug Substances (GDS) strategy

[areas of improvement ]: there were delays in commissioning certain capital projects, which had an impact on the payback and the internal rate of return. Second, there were delays in executing a few R&D projects. Lastly, we had slightly higher than expected attrition for a segment of our employees.

[improvement made: capital works]: the delay in capital projects was in some part due to the non-availability of workforce at our equipment manufacturer’s site because of the pandemic, as an organisation we could have done a better job in anticipating those potential delays and taking steps to mitigate its impact.

[improvement made: r&d projects]: we have established more robust cross-functional teams, invested in skill development, hired more people, and strengthened our information systems for early identification of impediments and specific action, or resources, needed to overcome them. We have also improved our overall review mechanism so that our leaders can play an active role in enabling our cross-functional teams

[improvement made: attrition]: we have implemented certain SOPs and protocols, made the line managers more accountable, and set up additional communication platforms between the direct supervisors and people on the shopfloor so that the supervisors can better understand the issues at the ground level and take suitable action for their resolution. Additionally, taking advantage of the National Apprentice Promotion Scheme introduced by the Government, we have successfully onboarded apprentices, creating a strong chemist pipeline for shopfloor operations.

[operating efficiencies: gds]: the focus is on optimising processes, improving yields, and enhancing productivity. During the year, concrete steps were taken for products such as Ezetimibe, Levetiracetam, Deferasirox, Donepezil, Dorzolamide and Rivaroxaban to make them more competitive not only in terms of cost but also in terms of availability and capacity.

[operating efficiencies: project management]: strengthening of the Project Management Office to ensure that projects are completed on time and in full. The projects being handled by them relate to the new molecules that are being developed, whether under CMS or GDS vertical.

[operating efficiencies: customer feedback]: We have institutionalised customer surveys where the feedback from customers is shared across the organisation. Another focus area is our continued investments in green chemistry, which is leading to efficient use of solvents

[working with customer for demand forecasting]: our sales and development team stayed constantly in touch with the customers and regularly updated the demand forecast. Thorough understanding of evolving customer demand helped our manufacturing team to quickly adjust inventory to avoid insufficient or excessive inventory.

[risk management]: one of the reasons why Neuland was not significantly impacted by the supply chain disruption is because that risk was included in our risk register and appropriate response tactics had been formulated and implemented well in advance

[key growth drivers]: we operationalised Unit III, a manufacturing facility. we are prioritising optimisation of capacity for agility enabling quick flexible response to customer needs.

[key growth drivers : cms]: Our strong pipeline of CMS projects - currently 78 active projects with 24 in late-stage development, and the continued emphasis on targeting molecules in the later stages of the clinical cycle, position us well to grow our revenue in the coming years. Building deeper competency and capabilities in R&D will be essential to our growth.

[key growth drivers: gds]: On the GDS side, our quality-led portfolio is driving market penetration for both our prime products as well as our specialty APIs. We are looking at filing DMFs in products we are excited about, which will further bolster our product portfolio and present new growth opportunities. We are focused on quality conscious customers and looking to further build a product pipeline differentiated on technology

[gds growth]: In the GDS business, formed collectively by our Prime and Specialty APIs, growth was led by our ability to scale up products that command a strong market position.

[prime growth]: In the Prime segment, comprising mature APIs which typically face high competition, growth was largely attributable to the key molecules of Levetiracetam, Mirtazapine and Labetalol.

[specialty growth]: Multiple molecules, including Deferasirox, Dorzolamide, Entacapone and Ezetimibe, led the growth momentum in the Specialty segment and contributed to higher profitability.

[key growth drivers]: Led by the expertise of our R&D team, we are also focusing on bringing differentiated products to the market

[key growth drivers cms]: In recent years, we have witnessed an increasing number of late-stage projects entering our pipeline. This is a favourable trend for Neuland as late-stage projects have a relatively low-risk failure and a short commercialisation cycle vis-à-vis projects in the early development phase.

[cms commercialisation]: During the year, we have made significant progress with 4-5 late-stage projects which are expected to get commercialised by our customers in the next 12-24 months.

[cms clients]: We continue to pursue the right kind of opportunities to further grow our CMS business. In this regard, our long-term strategy has been to partner with emerging biotech companies. As per data from IQVIA, emerging biotech companies accounted for more than two-thirds of late-stage pipelines in 2018, up from 52% in 2003.

(Dmf filings): we have six/seven molecules that are in late-stage development, of which we are on track to file about 5 DMFs in the current fiscal, assuming there is no significant business disruption. As we grow our GDS portfolio, with particular emphasis on enhancing our differentiated offerings,

(New competency developed); Production of sterile APIs is a highly specialised capability that involves several complex processes. Our continued quest to raise the bar of our chemistry capability saw us develop processes for the manufacture of compliant sterile APIs,

(Value addition for customers): we have a strong understanding of the complications in large-scale production; in the case of our emerging biotech customers, who may not be best placed to envisage the full cycle of a product, we proactively share insights on the commercialisation phase even while their molecules are in the development stage.

(Product lifecycle management): During the year, various initiatives undertaken under product lifecycle management enabled us to scale-up our batch size, reduce cycle time, downtime and non-productive occupancy for our key products. We also came up with new ways to enhance our overall solvent recovery to minimise our impact on the environment

(Dependence on China): Our alternate sourcing policy has enabled us to reduce our imports from China from over 40% in FY 2018 to around 20% at the close of the year under review. We aim to reduce our dependence on China’s imports to 10% by FY 2024. Moreover, we have also reduced our dependence on any single external geography, with 11.8% in FY 2021 as against 21.6% in FY 2018/ previous year.

(Digitisation aiding regulatory compliance): Digitisation of data and automation of processes is driving better deviation management and greater transparency and traceability of data, thereby leading to improved regulatory compliance and efficiency

(Meeting regulatory compliance): All these focused actions are in line with our priority to ensure 24x7 GMP compliances across all our sites and be in a state of ‘all time inspection’ readiness.