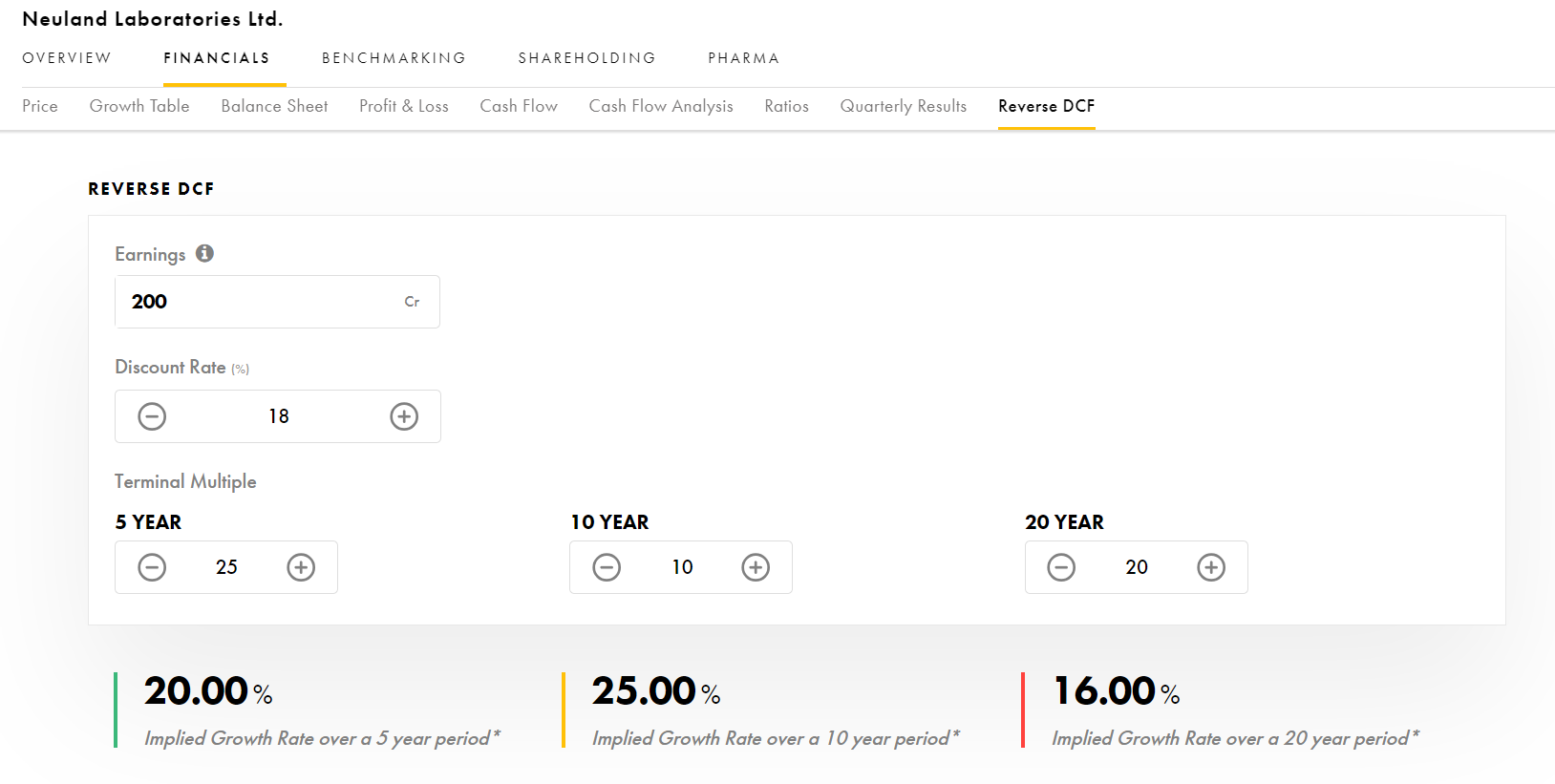

Management is very conservative, however the statements given by the management reflects the positiveness of the business…

Score 10/10 in almost all parameters:

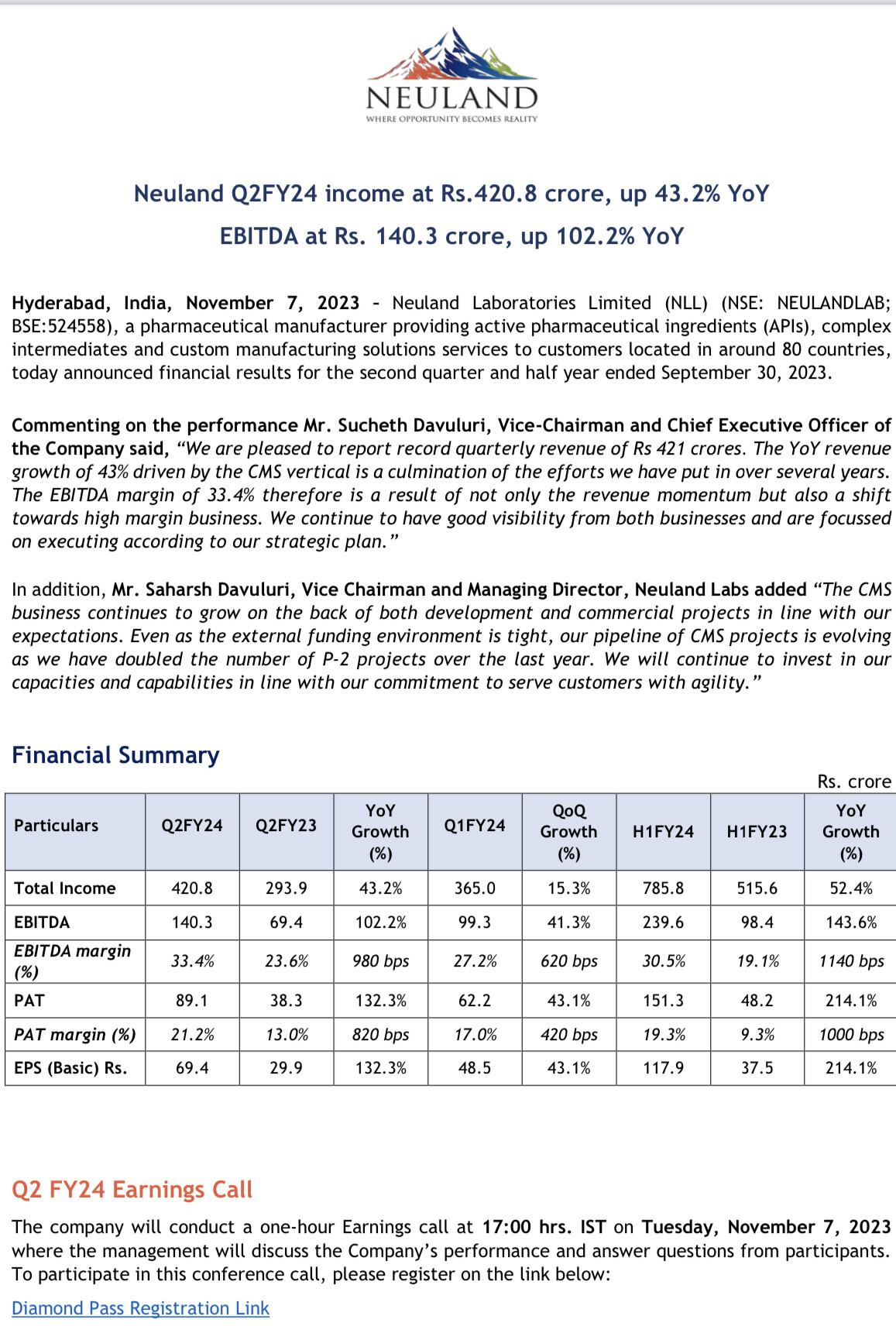

The YoY revenue growth of 43% driven by the CMS vertical is a culmination of the efforts we have put in over several years.

The EBITDA margin of 33.4% therefore is a result of not only the revenue momentum but also a shift towards high margin business. We continue to have good visibility from both businesses and

are focussed on executing according to our strategic plan.”

“The CMS business continues to grow on the back of both development and commercial projects in

line with our expectations. Even as the external funding environment is tight, our pipeline of CMS

projects is evolving as we have doubled the number of P-2 projects over the last year. We will

continue to invest in our capacities and capabilities in line with our commitment to serve customers

with agility.”

CMS segment

CMS revenues driven by commercial molecules. Significant contribution from molecules in the pipeline also

Prime segment

In Prime segment Mirtazapine and Escitalopram were the key molecules- H1FY24 Business and Financial Highlights

Specialty business

Specialty business driven by Paliperidone, Apixaban and Donepezil

Regulatory Audits US FDA inspected Unit-3 and issued EIR (Establishment Inspection Report)

Unit-I inspected by EDQM (European Directorate for the Quality of Medicines)

Free Cash Flow (FCF) generation and utilisation

Generated Free Cash Flow of Rs. 120.6 crores during H1FY24

Partly utilised to reduce debt by Rs 26.0 crores

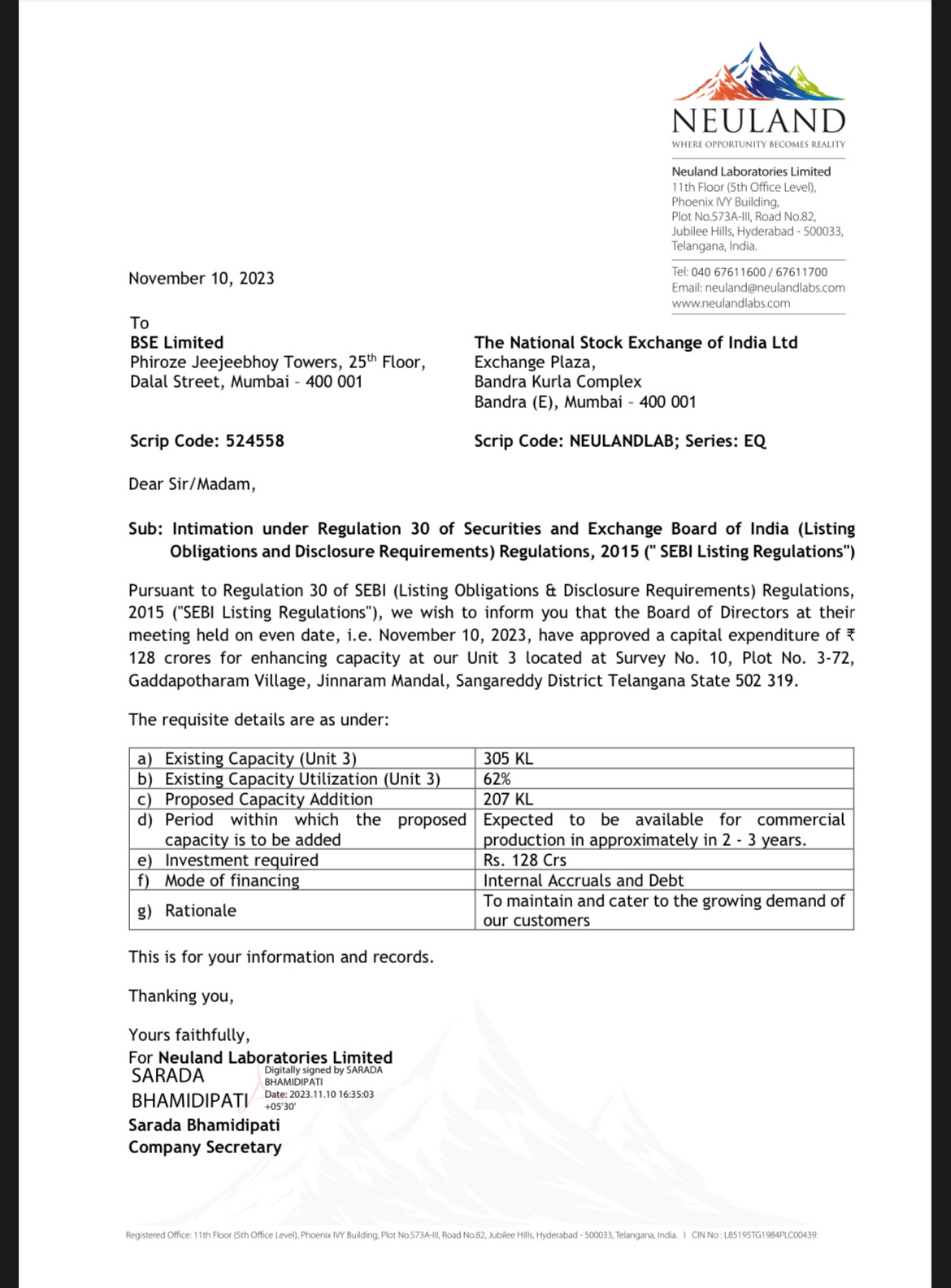

Capex Investment of Rs 43 crores for enhancement of future overall capabilities.

Working Capital

Reduction in working capital cycle to 102 days in Q2FY24 as compared to 148 days in Q2FY23

The CMS business continues to grow on the back of both development and commercial projects in line with our expectations.

Even as the external funding environment is tight, our pipeline of CMS projects is evolving as we have doubled the number of P-2 projects over the last year. We will continue to invest in our capacities and capabilities in line with our commitment to serve customers with agility.

Steady shift from low margin Prime to high margin Specialty and CMS segments

• CMS business caters to Innovator customers on an exclusive basis, developing and manufacturing APIs/Intermediates in line with rigorous

customer expectations hence is highly concentrated in terms of customers

• Specialty segment works on complex products and technologies, hence has a focused approach towards select customers.

• Pre-clinical to P-3: Neuland generates revenue by process research & development as well manufacturing quantities for clinical trials

• *Pre-Reg/Reg: Phase-3 complete; Molecules filed but not yet commercial (Earlier labelled as ‘Development’)

• Commercial: Neuland generates revenues by manufacturing APIs for commercial novel molecules for innovators

• Steady trend in molecules transitioning from development stage to commercialisation resulting in increase in revenue from commercial products.

Focus Areas

29

Continue to invest in R&D capabilities and manufacturing technologies to attract more

RFPs while improving conversion rate 1

2 Lifecycle management of commercial products

3 Continue to focus on molecules in Phase II and later stages of development

4 Continue business development focus on biotech companies

5 Diversify geographic focus.

Went through the current concal 3 times to get the sense of current and future prospects. Management is crystal clear about its vision and capabilites.

Company is now debt free and started generating free cash flows. Management is conservative yet efficient in capital utilization.

Retailers shareholding has come down from 40.73% in Dec 22 to 35.08% in Sept 23 , however one good thing is that retailers are the largest shareholders… hope they will hold on for longer period to compound the benefit if Company continues to perform in this way.

Disclosure: Invested from levels of 1100 and further added today for very very long term as a coffee can investment. Views are biased.