Going forward, If GLP-1 is the preferred first line of treatment, and their prices crashing, will that be a serious challenge to metformin based drugs?

Transfer of Company’s property situated at Nanakramguda, Hyderabad, Telangana, admeasuring 1.75

lakh sq.ft. by way of perpetual lease to various parties, for an overall consideration of Rs. 117.96

Crores, subject to receipt of requisite approvals. The said transaction does not fall under the ambit

of related party transactions.

Company will recieve Rs 118 Cr which it can utilise for its CAPEX and R&D

3 Likes

Descent set of results from Neuland Labs. Management commentary sounds bullish. Details shall be known in the concall.

Disc : invested.

6 Likes

Neuland Labs Q3 concall highlights -

Massive EBITDA margin improvement YoY due better product mix and greater contribution from commercial CMS operations

Retired debt worth 111 cr in past 9 Months

Recent business momentum likely to sustain over medium to long term

Gross margins in Q3 even higher than Divis’s gross margins despite lower contribution from CDMOs. Management believes, these margins are sustainable

Current RM procurement percentage from China at 25 pc

Capacity utilisation at Unit-1,2 at 80-85 pc. Unit 3 at 60-65 pc.

Unit 3 adding more capacities

Commercial contribution from CMS business at all time high. Likely to be higher going fwd

Current balance sheet,cash flow position at all time high

Company seeing higher enquiries in CDMO space

Quality of CDMO pipeline is healthy

Capex for next year - roughly 100 cr ( maint + expansion )

Company looking to expand R&D facilities in about a couple of years

Disc: invested, biased

21 Likes

4 Likes

Unbelievable results

They ve hit the ball out of the park

4 Likes

Truly unbelievable - on forward PE looks 10

3 Likes

Can’t annualise qtly results in CDMO business. But can safely assume a PE of around 20 or so. Details shall be avlb post concall

4 Likes

Results are well above the expectations:

As per management:

“We are happy to state that our focus on R&D and project management saw us achieve our highest

ever profitability margins in FY23. We executed a number of CMS projects during the year resulting

in the business recording significant growth and contributing close to half the Q4 revenues. > We

expect this momentum to continue in future as well on account of new customers increasingly

accepting Neuland as a well regarded CDMO

We crossed several significant milestones in FY23 with business driven by ongoing growth in the

high margin Specialty and CMS business. The performance of this fiscal reflects the various

initiatives we have taken in line with our strategy over the last few years, playing out now. > We

believe that this puts us in a strong position as we look to consolidate the healthy momentum

going forward.”

8 Likes

All time high numbers, majorly driven by CMS

Imp - As per my understanding, numbers may not be consistent on QoQ basis as they mentioned many times in last conalls. However they are going great YoY.

From Investor Presentation -

Steady shift from low margin Prime to high margin Specialty and CMS segments

• CMS business caters to Innovator customers on an exclusive basis, developing and manufacturing APIs/Intermediates in line with rigorous customer expectations hence is highly concentrated in terms of customers

• Specialty segment works on complex products and technologies, hence has a focused approach towards select customers.

1 Like

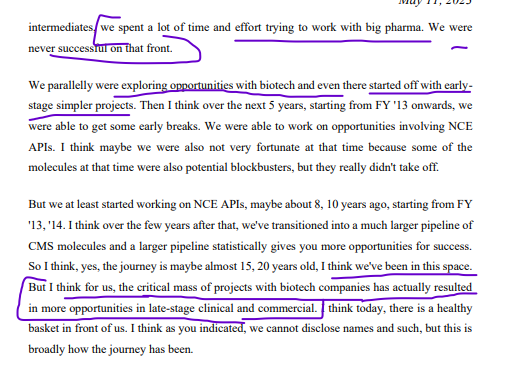

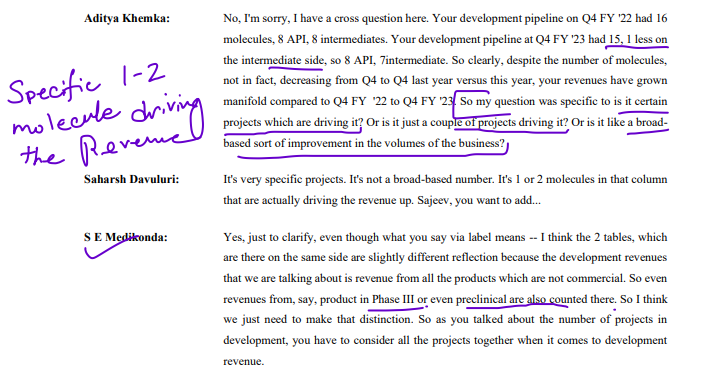

At present, they have 15 molecules in development phase and 21 in commercial phase ( not counting 51 molecules combined in Phase-1,2,3 and pre-clinical stages ). Greater clarity on these 36 molecules ( development + commercial ) wrt their revenue potential in the concall shall be the thing to watch out for.

If the management guidance is upbeat, Neuland may be in for a re-rating.

3 Likes

The street is also not expecting that the Company will repeat this kind of number but definitely the trajectory has to be maintained…20% growth with 20% margin will be required for making it a long term compounder and which the Company is seems to be capable of…

2 Likes

Neuland labs imp points Q4 FY23 con call:

Commenting on the performance Mr. Sucheth Davuluri, Vice-Chairman and Chief Executive Officer of the Company said, “We crossed several significant milestones in FY23 with business driven by ongoing growth in the high margin Specialty and CMS business. The performance of this fiscal reflects the various initiatives we have taken in line with our strategy over the last few years, playing out now. We believe that this puts us in a strong position as we look to consolidate the healthy momentum going forward.

We are happy to state that our focus on R&D and project management saw us achieve our highest ever profitability margins in FY23. We executed a number of CMS projects during the year resulting in the business recording significant growth and contributing close to half the Q4 revenues. We expect this momentum to continue in future as well on account of new customers increasingly accepting Neuland as an established CDMO.

Specialty business

Specialty business growth driven by Apixaban, Paliperidone along with Ezetimibe, and Donepezil

Revenue contributions

CMS revenues driven by commercial molecules some of which have transitioned recently. Significant contribution from development revenue also

Segment development

In Prime segment Mirtazapine, Ciprofloxacin and Labetalol were the key molecules

Portfolio Strategy

Filed 3 USDMFs - Tafamidis, Voxoletor and Voxelotor Co-crystal

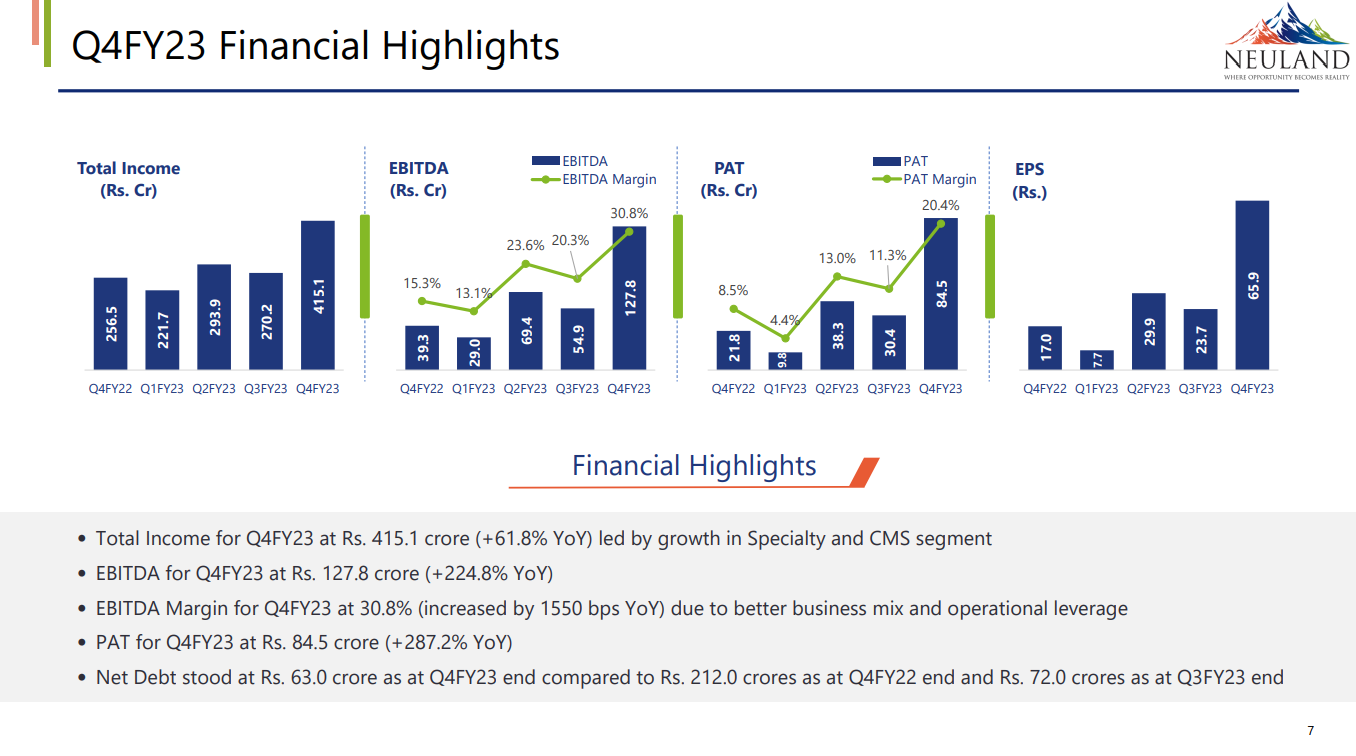

Total Income for FY23 at Rs. 1,200.9 Crore (+26.0% YoY) led by growth in Specialty and CMS segment

• EBITDA for FY23 at Rs. 281.1 Crore (+94.8% YoY)

• EBITDA Margin for FY23 at 23.4% (increased by 830 bps YoY) due to better business mix

• PAT for FY23 at Rs. 163.1 Crore (+156.7% YoY) due to slower increase in depreciation compared to increase in EBITDA

• Debt/Equity stood at 0.12x due to retirement of Rs. 113.6 crore borrowings (net) in FY23

• Net Debt stood at Rs. 63.0 crore as at FY23 end compared to Rs. 212.0 crore as at FY22 end

• Steady shift from low margin Prime to high margin Specialty and CMS segments

• CMS business caters to Innovator customers on an exclusive basis, developing and manufacturing APIs/Intermediates in line with rigorous

customer expectations hence is highly concentrated in terms of customers

• Specialty segment works on complex products and technologies, hence has a focused approach towards select customers

CMS projects as at Q4FY23 :

- At present, they have 15 molecules in development phase and 21 in commercial phase ( not counting 51 molecules combined in Phase-1,2,3 and pre-clinical stages ).

- Business will remain lumpy & nonlinear, clear shift however is towards CMS (specialty business)- 45% contribution

- Positioning of Neuland has improved for clients as we have been able to transit from clinical to development- speaks about our capability

- Utilization in unit 3 will improve & we should be able to deliver on current momentum gained

- Performance in Q4 does not indicate one off & is in direction of vision

- Customer needs is center focus of our business

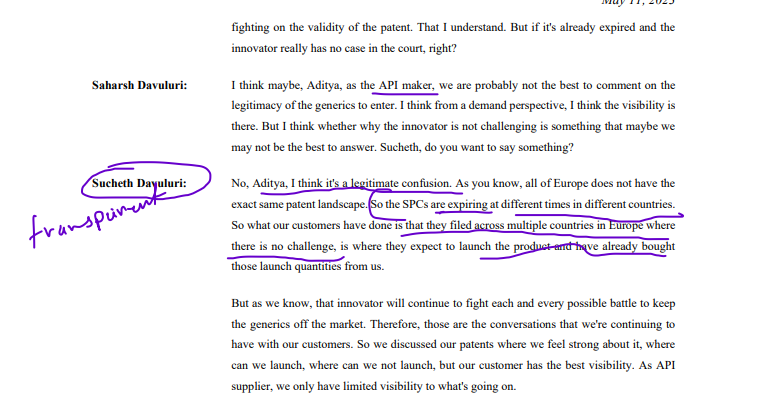

- Paliperidone- innovator is fighting for patent to not be classified as generic, however as supplier to clients of innovator we don’t see any slowing in demand, innovator will try his best to protect patent

- 1st two plants at 80-90% utilization & 3rd at 64% utilization, similar is expected coming year, next couple of years growth can from using capacity here & additionally de-bottle necking

- Surge in Q4 is due to advancement of clinical + commercialization of couple of molecules in cms space

- 2 molecules are likely to be commercialized next year, which can be blockbuster. Have strong pipeline for growth in terms of molecules

26 Likes

Extremely good set of results. Kicking myself for not buying more at 1500. The margins are at all time high. Is it a good time to atleast partially book some profits.

My rationale Q4 is a seasonally good quarter hence unlikely to repeat. Some profit booking and then re-enter again at lower levels.

Suggestions invited.

3 Likes

I don’t think that’s a very good idea. U know something that the everyone else also knows. Its better to just stick around when u are obviously holding an absolute gem at non expensive valuations.

That’s my personal opinion.

4 Likes

I would suggest to listen the Q4 concal 3 to 4 times before making any decision to sell. Management has not given any guidance as they understand that the nature of business. The business will remain lumpy but management has unequivocally suggested that Q4 results are not one off and FY 2022-23 figures can be taken as base figure and there will be growth in FY 23-24 and also that trajectory of the company and business is in upward direction…

Disclosure : Invested for long term

13 Likes

The following screen shots are pretty much telling the narrative

Management’s integrity/ calling spread a spread)

Management is also well aware of the situation

Success of molecule is not in the hand of Neuland, but they are keep adding in late stage that’s the beauty of the business

No inorganic growth that shows the confidence of the promoter

This will be repeated as the nature of the business is lumpy even YOY & management accepts it

18 Likes

US FDA captured 3 minor observations under Form 483 for Neuland Labs in Unit 3. Unit 3 had only gone through Desktop inspection by the US FDA till now but it seems this is an in-person inspection done for the first time. Unit 3 is where most CapEx is being focused towards from FY’24 and beyond.

I saw the past Observation 483 being raised for other facilities of Neuland Labs and the manner in which they were handled. Nothing concerning came through. The markets too reacted decently in the past by not showing a severe decline/dip.

I tried checking the US FDA website if any details have come through regarding this particular observation but I could not find any.

Does anyone have any intel on this?

Disc: Invested for the long term, my thesis for Neuland is ethics and clean management

Neuland_Labs_Observation_483.pdf (267.8 KB)

5 Likes

2 Likes

There are 3 observations under Form 483 and management has advised that they are minor in nature.

As per my understanding the Auditors post inspection will issue EIR (Establishment Inspection Report).

The report along with other things will have observations under 483.

This report will be reviewed by US FDA authorities and based on it action will be classified.

The FDA inspections may be classified as:

- List item No Action Indicated (NAI)

Voluntary Action Indicated (VAI), or

Official Action Indicated (OAI)**

in the increasing severity order depending on the outcome.

When no Form FDA 483 (Inspectional Observations’) is issued, the inspection is classified as NAI.

When a Form FDA 483 is issued, it may be classified as VAI or OAI depending on the significance and severity of the deficiencies.

An FDA 483 observation is a notice that highlights potential regulatory problems, while a warning letter is an escalation of this notice .

You need to respond in writing within 15 days of receiving both a 483 and a warning letter.

OAI classifications may lead to further regulatory actions including Regulatory Meetings, Untitled Letters, Warning Letters, Import Alerts, Injunctions and Seizures. Irrespective of the classification, each inspection will have an Establishment Inspection Report (EIR) written by the FDA investigator and a copy will be sent to the firm as per FMD-145 (Field Management Directive). The investigators are also expected to report significant discussions with the firm management in the EIR.

A Warning Letter constitutes official but not final, agency action.(Observations will be classified Official Action Indicated), OAI, whenever a Warning Letter is issued** . This procedure provides greater consistency and uniformity in the classification system and regulatory policy.

As the managment has claimed that the observations are minor in nature and also depending on the corrective actions and reply submitted by the Company, it is likely that the classification by the FDA should be VAI and not OAI.

I would request any Pharma expert to advise the implication and way forward.

(How much time it takes for coming out of VAI and what is the impact on revenue and operations from the unit where VAI has been initiated)

Disclosure: Invested with a long term view of 3 to 5 year.

13 Likes