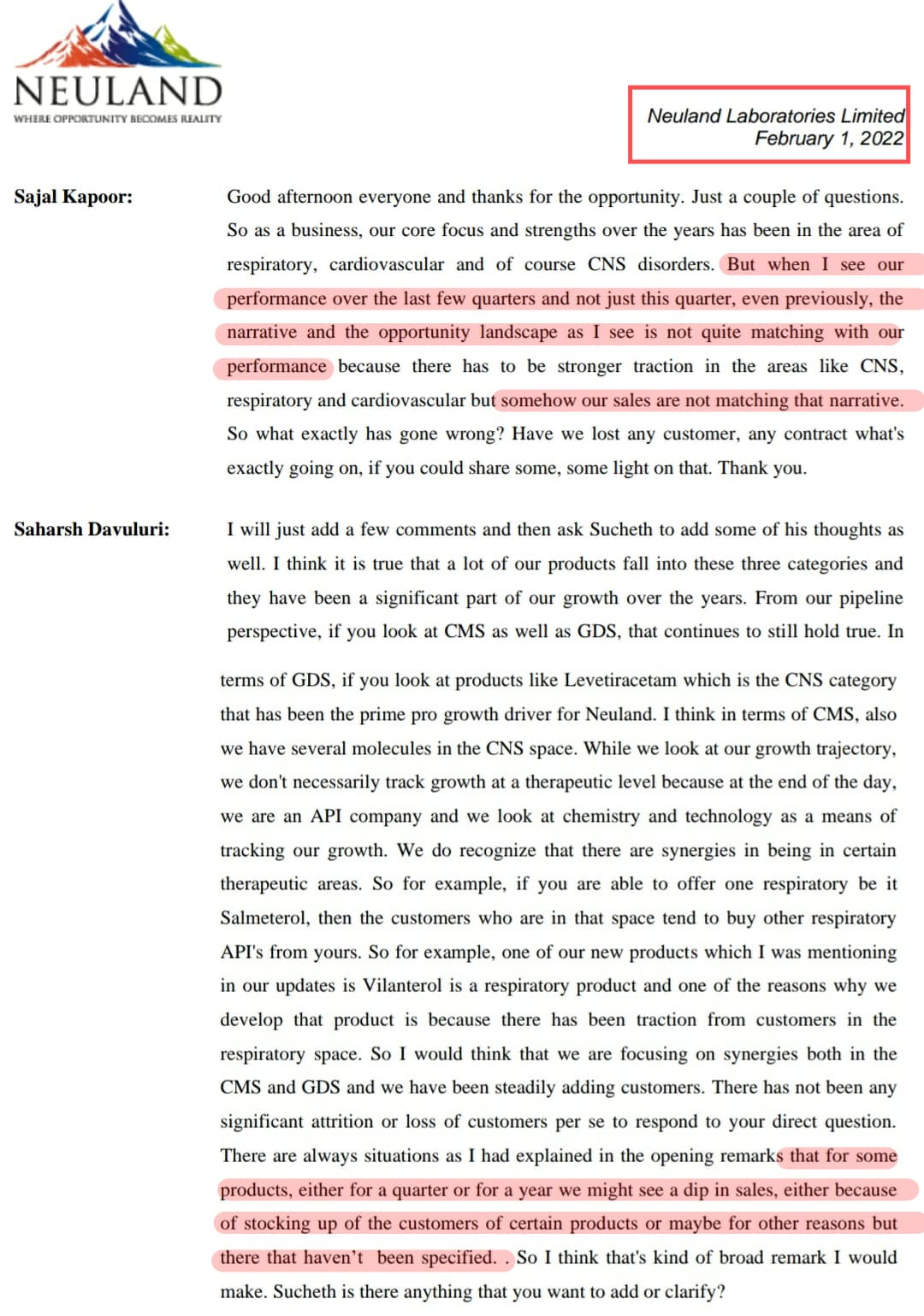

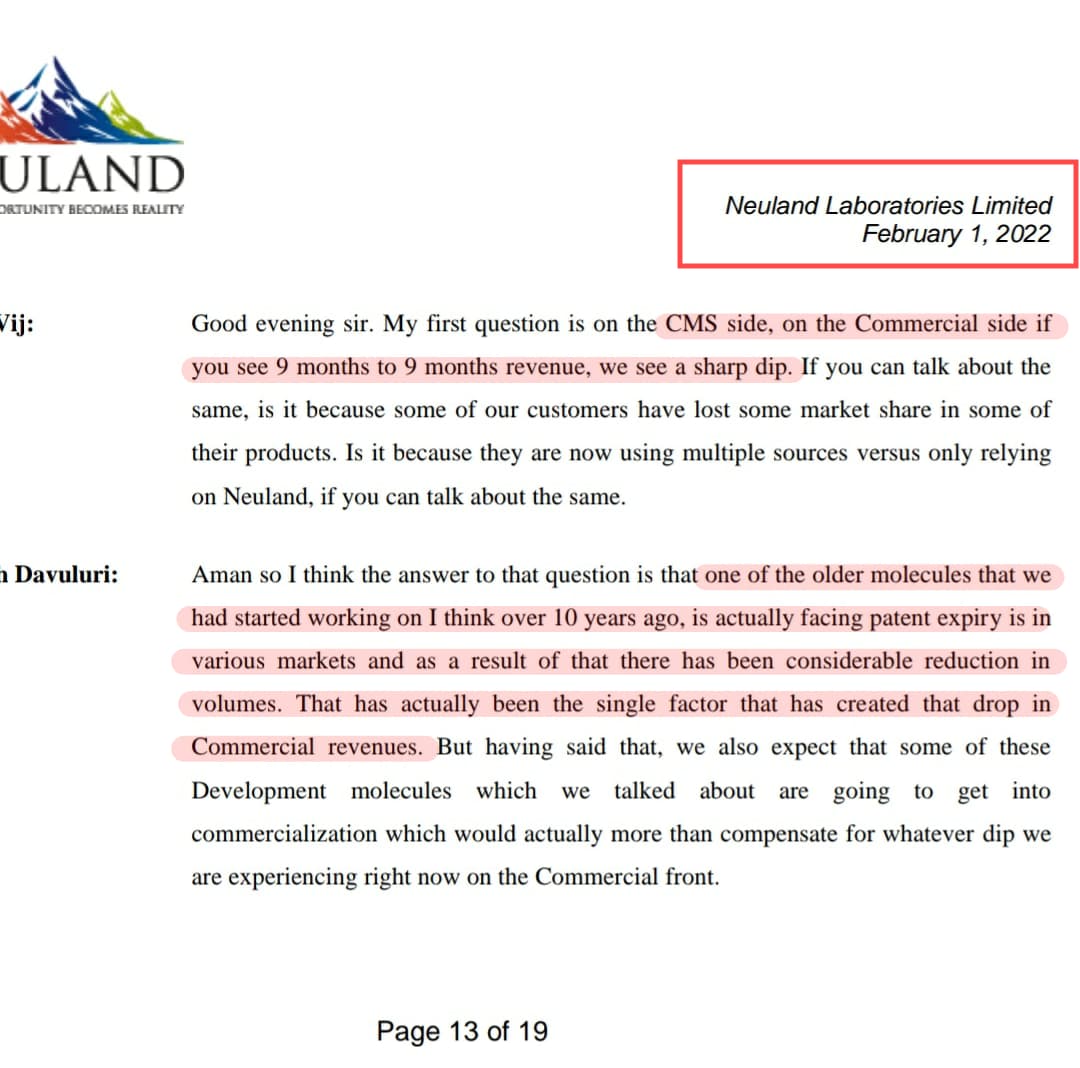

I couldn’t find such a guidance from Neuland’s management on previous earnings call. Ofcourse they had mentioned about contracts of raw materials. Higher raw material prices and it’s effect on margin was expected. But have you expected the decline in topline?

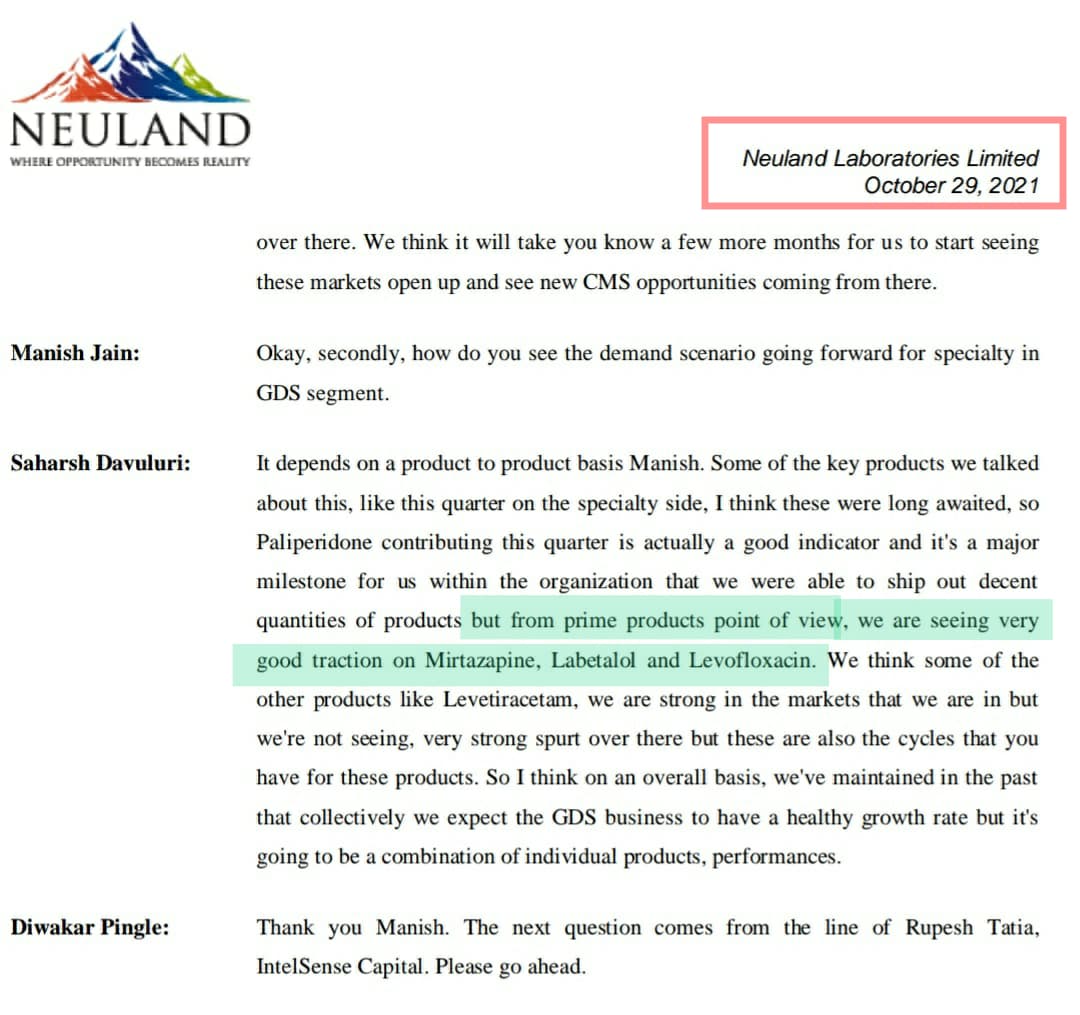

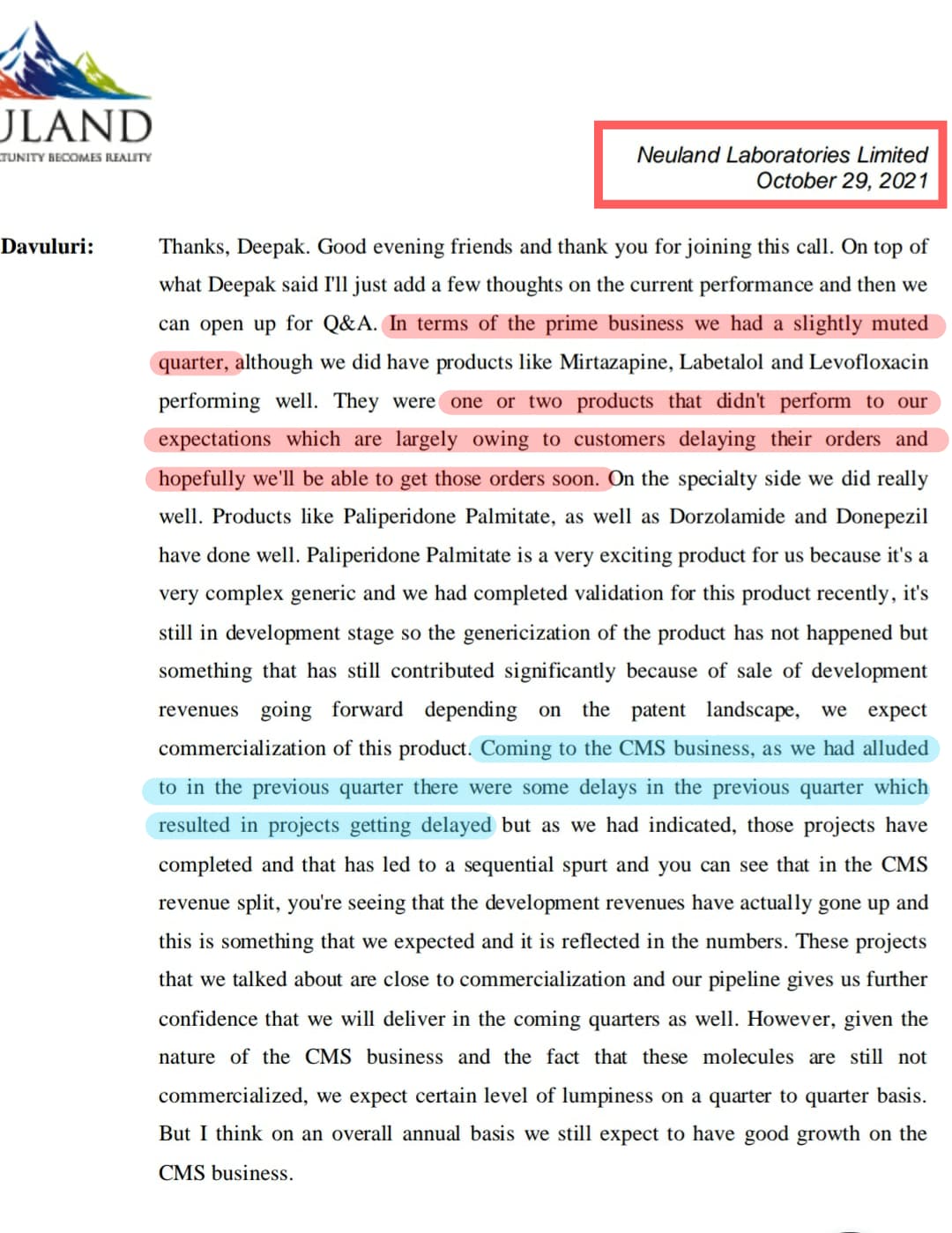

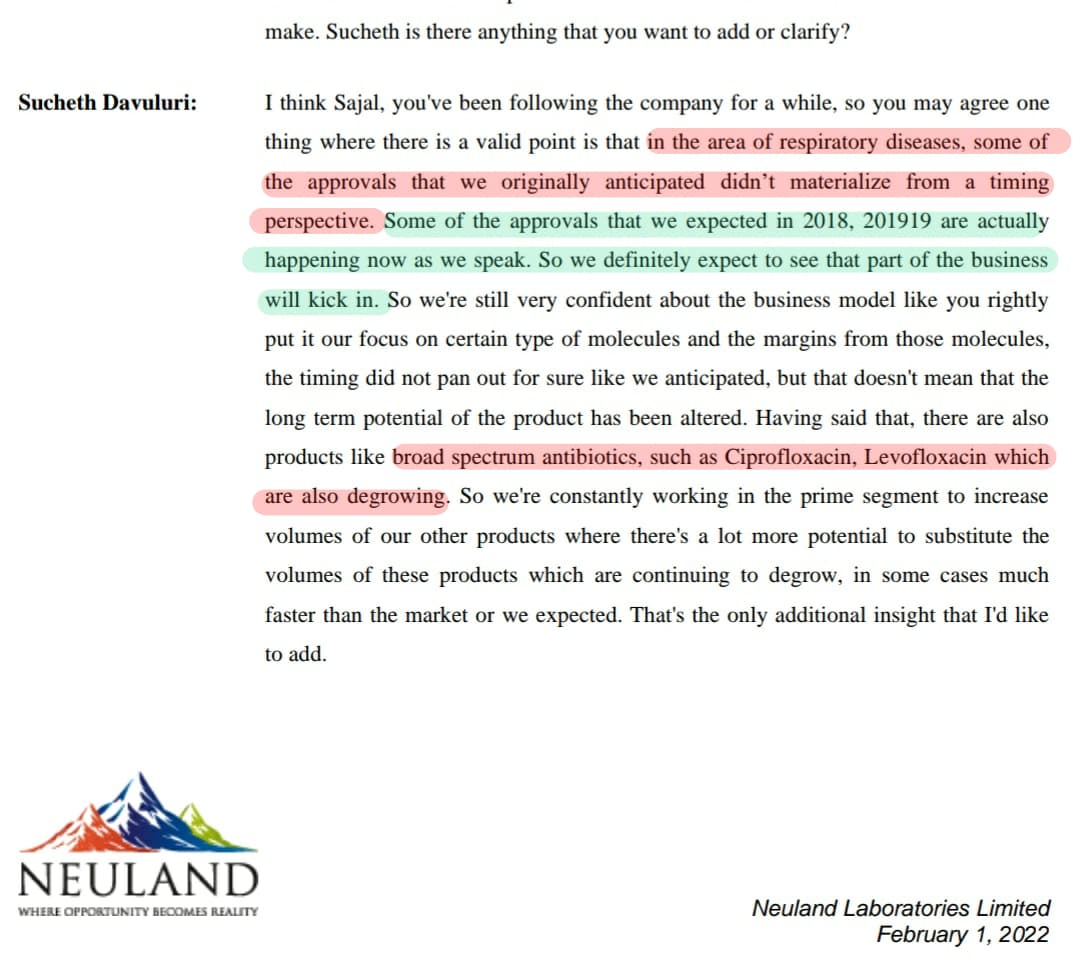

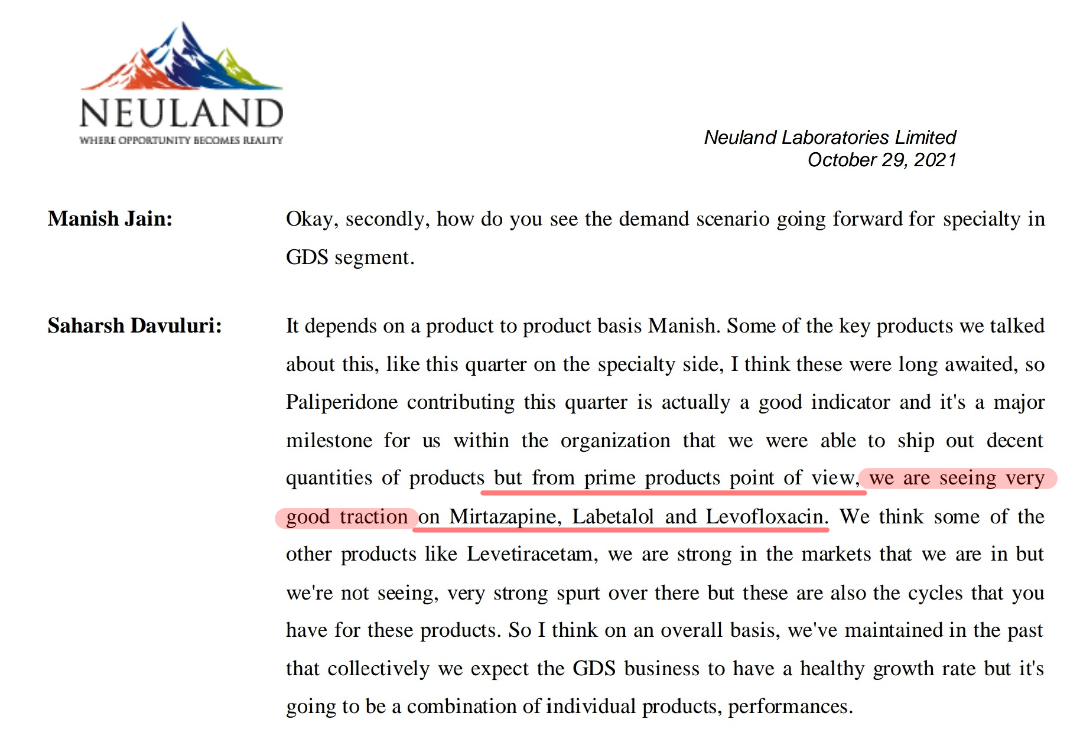

Management had mentioned on Q2 earnings call that they were seeing very good traction on Mirtazepine, Levofloxacin and Labetalol.

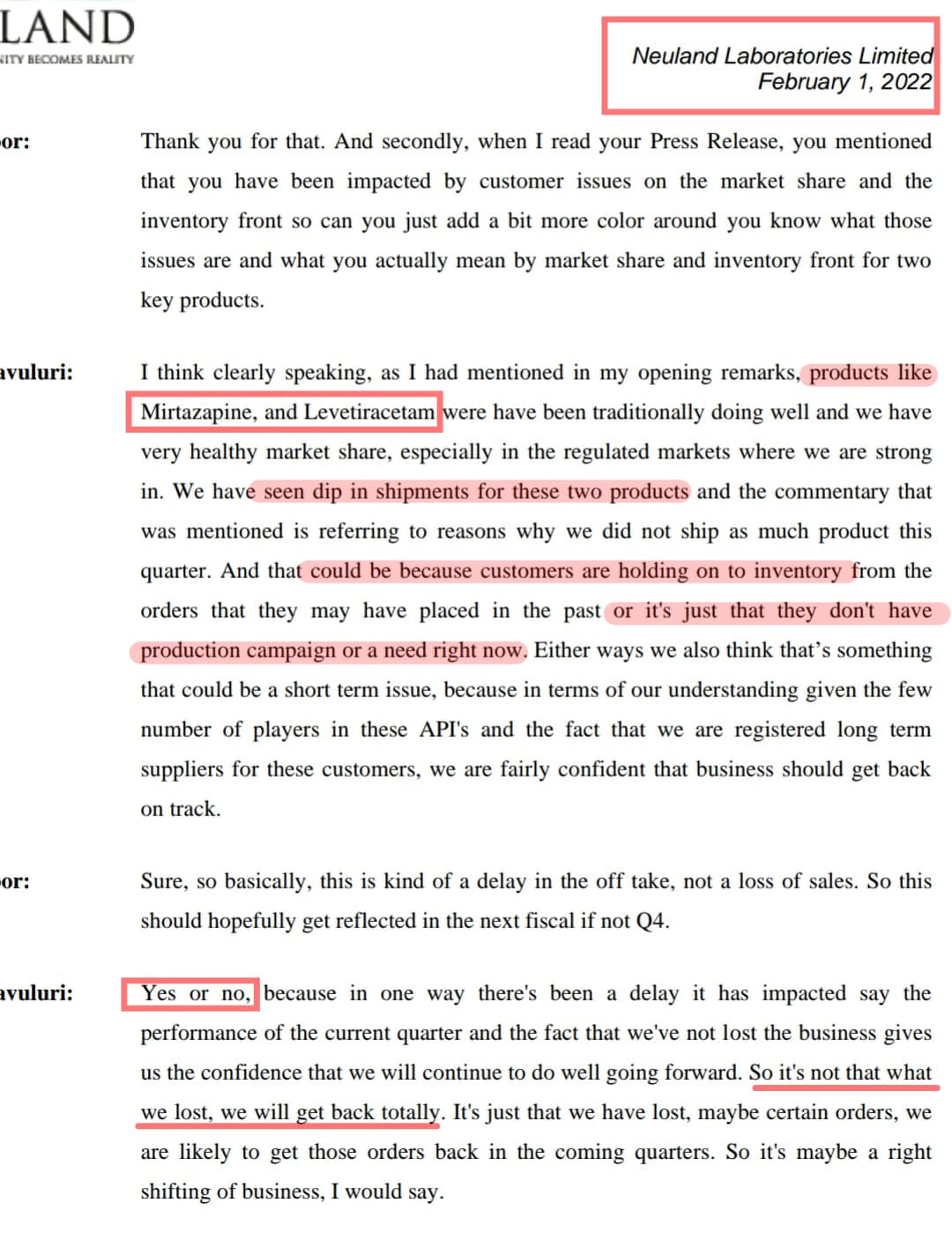

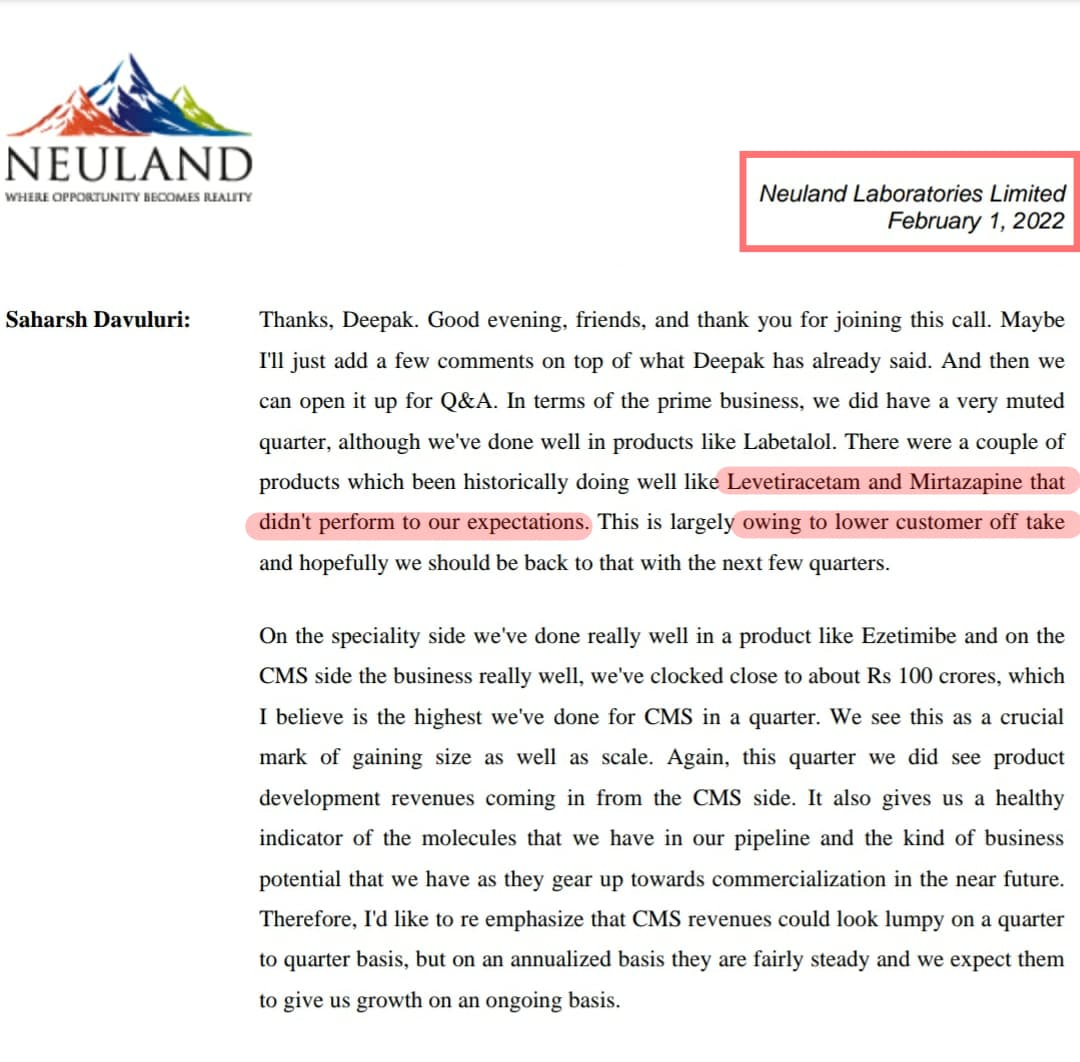

And 2 months later when the Q3 has ended, they are now saying that Mirtazepine hasn’t performed to their expectations owing to lower customer uptake.

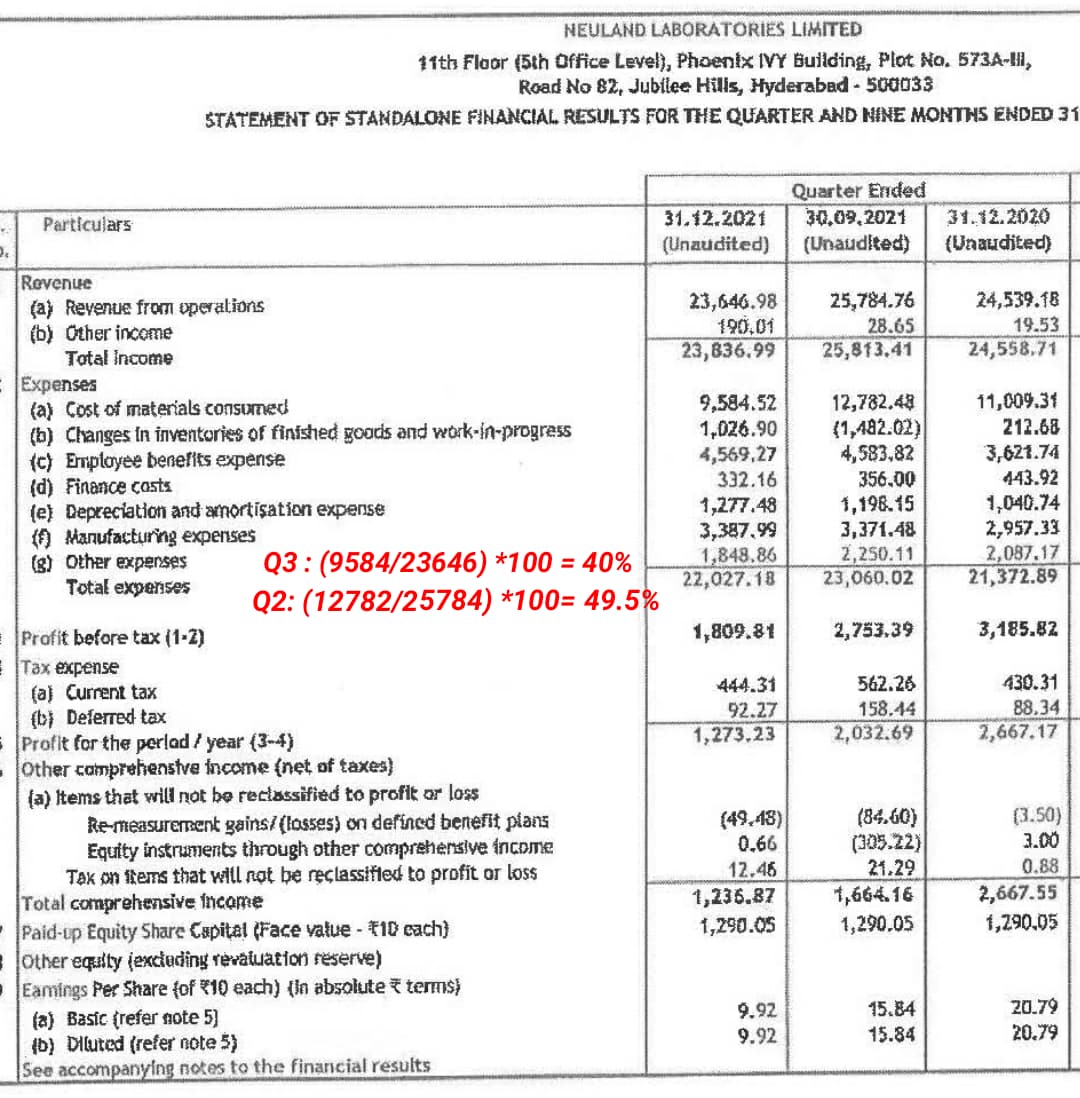

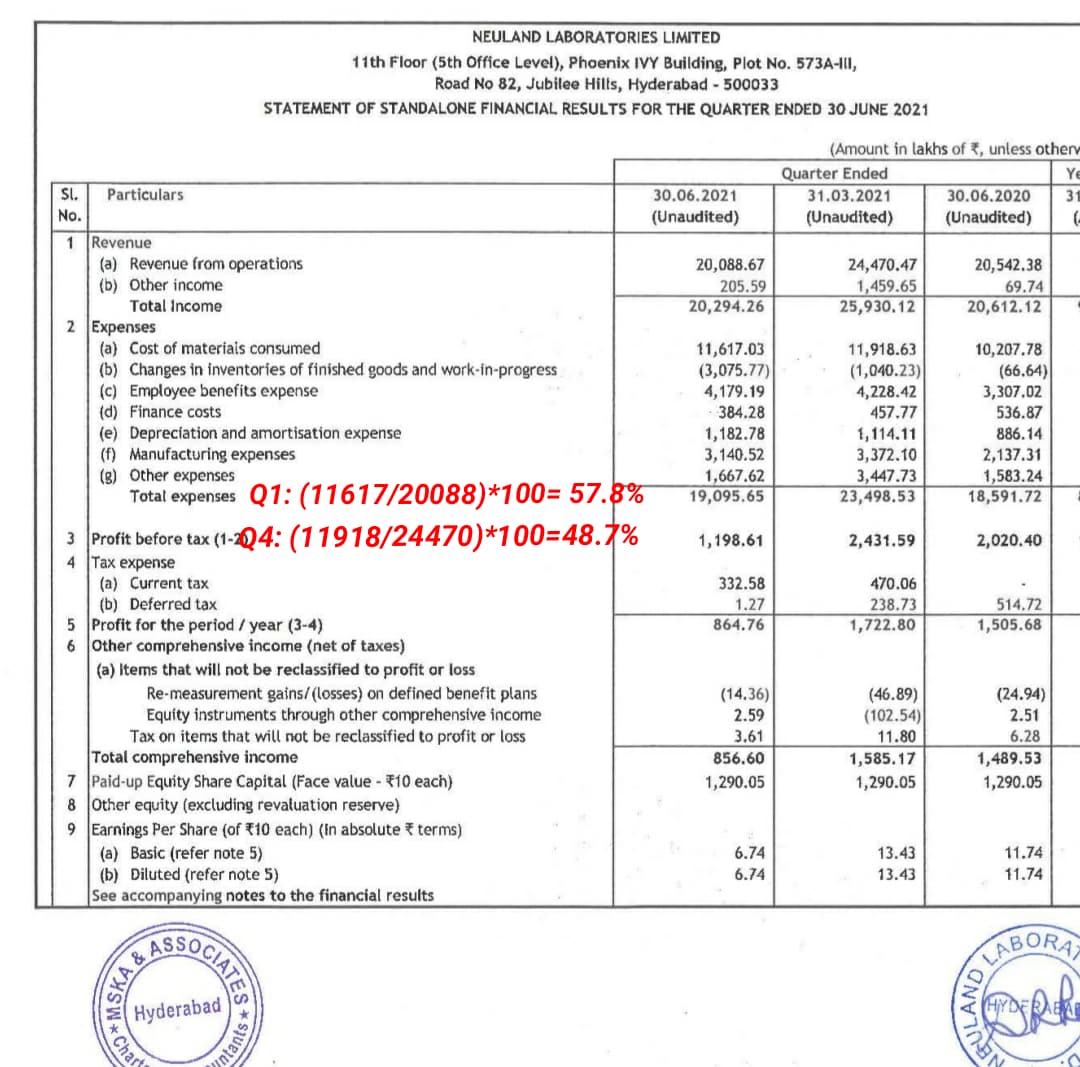

Talking about increased raw material pricing, there is one thing I didn’t understand. Material cost of Q3 is 40%, which is lower than previous quarters. Then the raw material cost is lesser than previous quarters, right?

I will add few earnings call snippets regarding management’s justification of lower revenues.

Q3 - Levetiracetam and Mirtazepine didn’t perform to our expectations. This is largely owing to lower customer off take and hopefully we should be back to that with next few quarters.

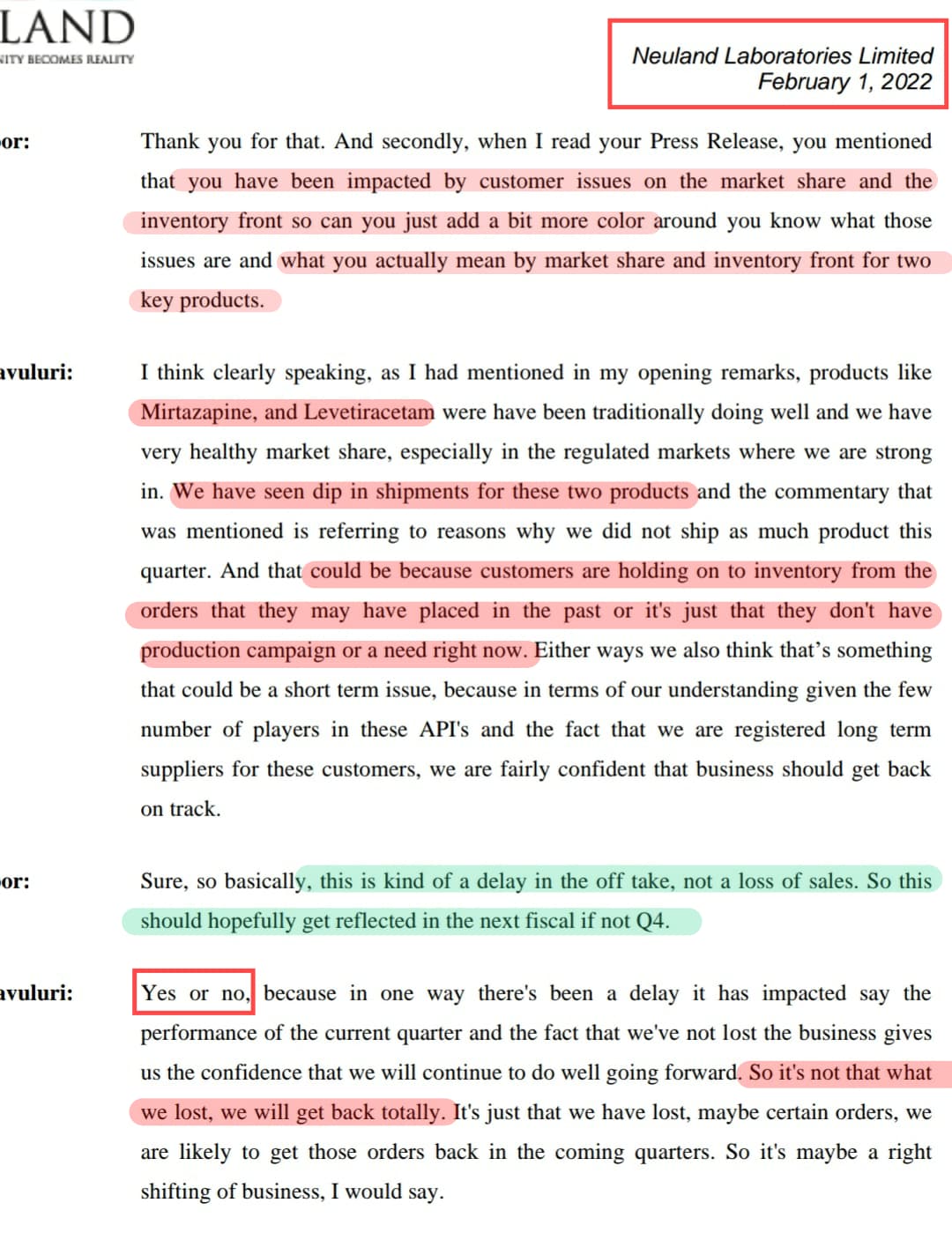

Q2 - Few products didn’t perform to our expectations which are largely owing to customers delaying their orders, hopefully we’ll be able to get those orders soon.

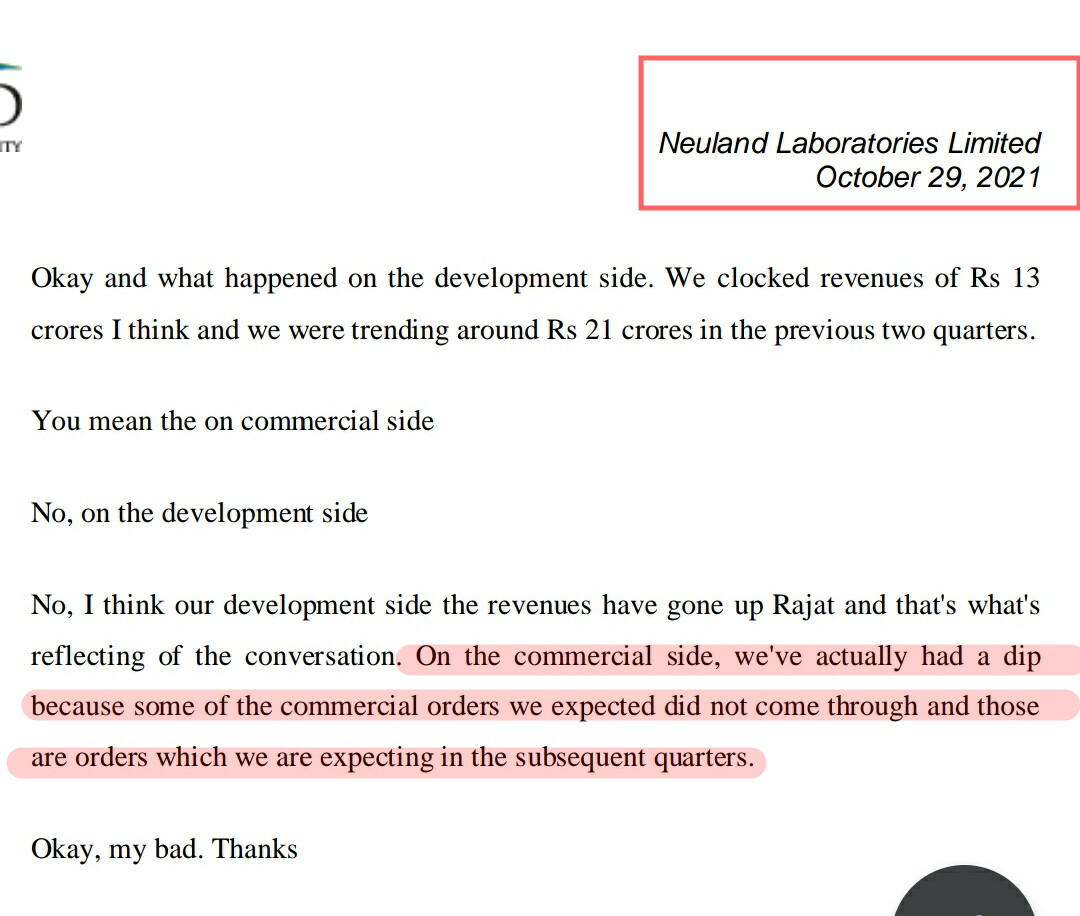

Q1 - Dip in revenues because of the delay in execution of projects. Whatever hit we had in Q1 would be delivered in subsequent quarters. Expect FY22 performance to be intact.

Q4 last year - Commercial orders were low and that’s because we didn’t have orders in that quarter, we perhaps delivered in Q3 or we will deliver them in the upcoming quarters.

It seems delay in orders are a routine thing for them. Management always had justification for lower revenues and lack in growth. They had guided about spillage of revenue into subsequent quarters, a few times. But had we seen that? I will continue moniter the company for some positive developments, better execution and better numbers.

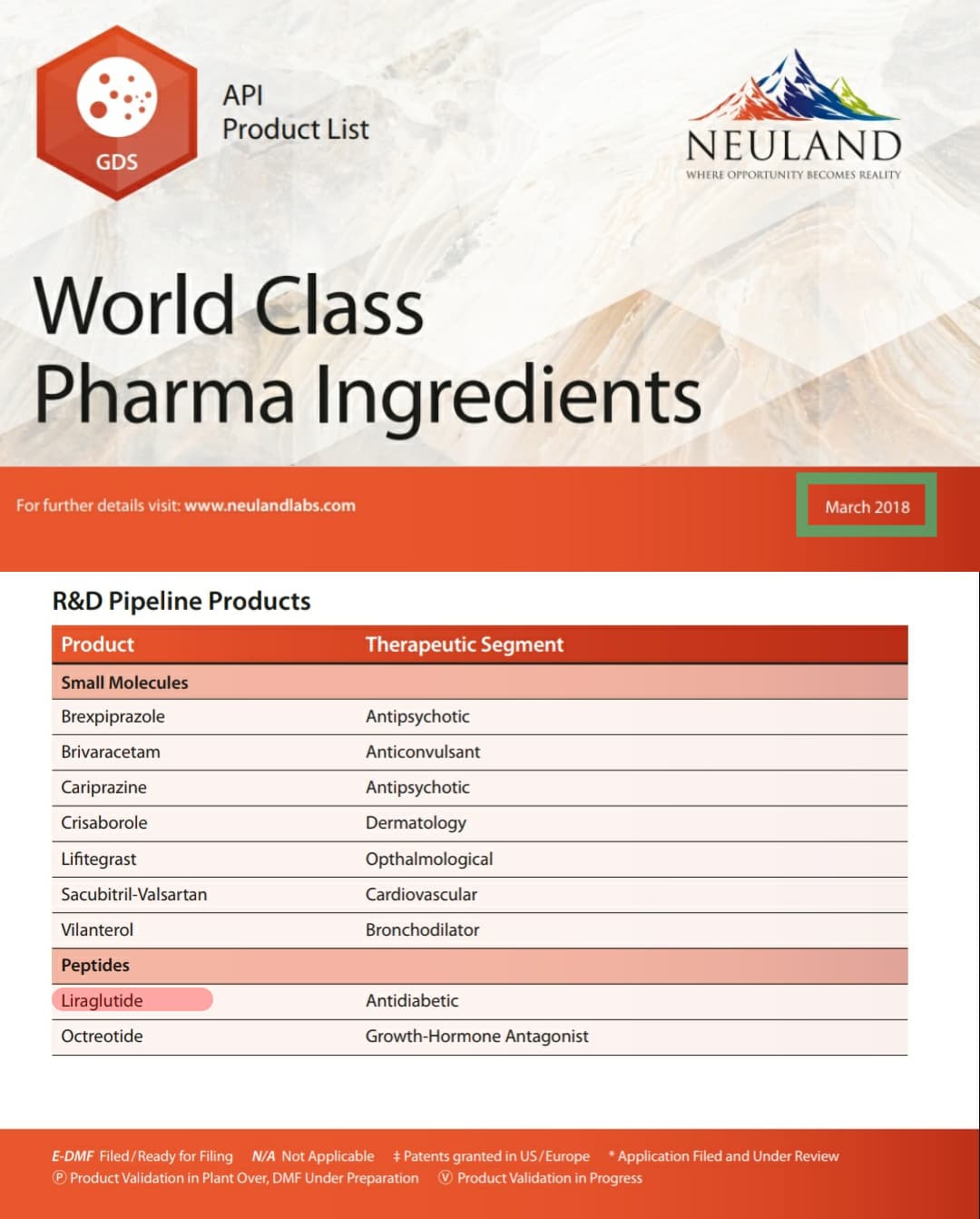

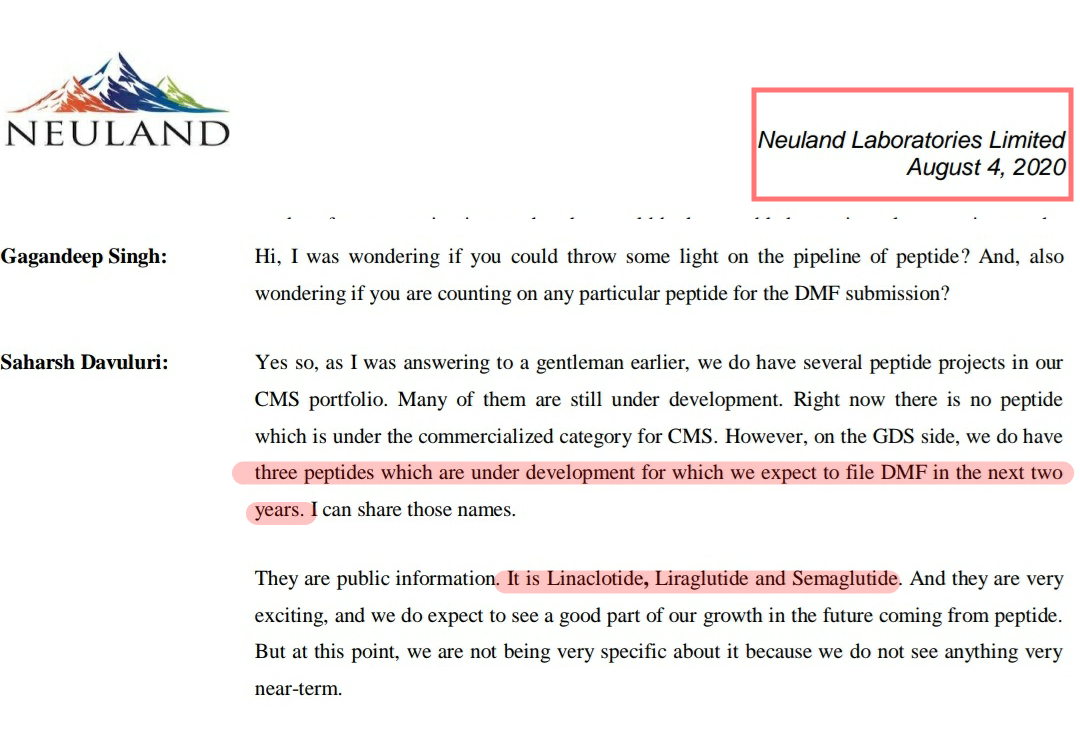

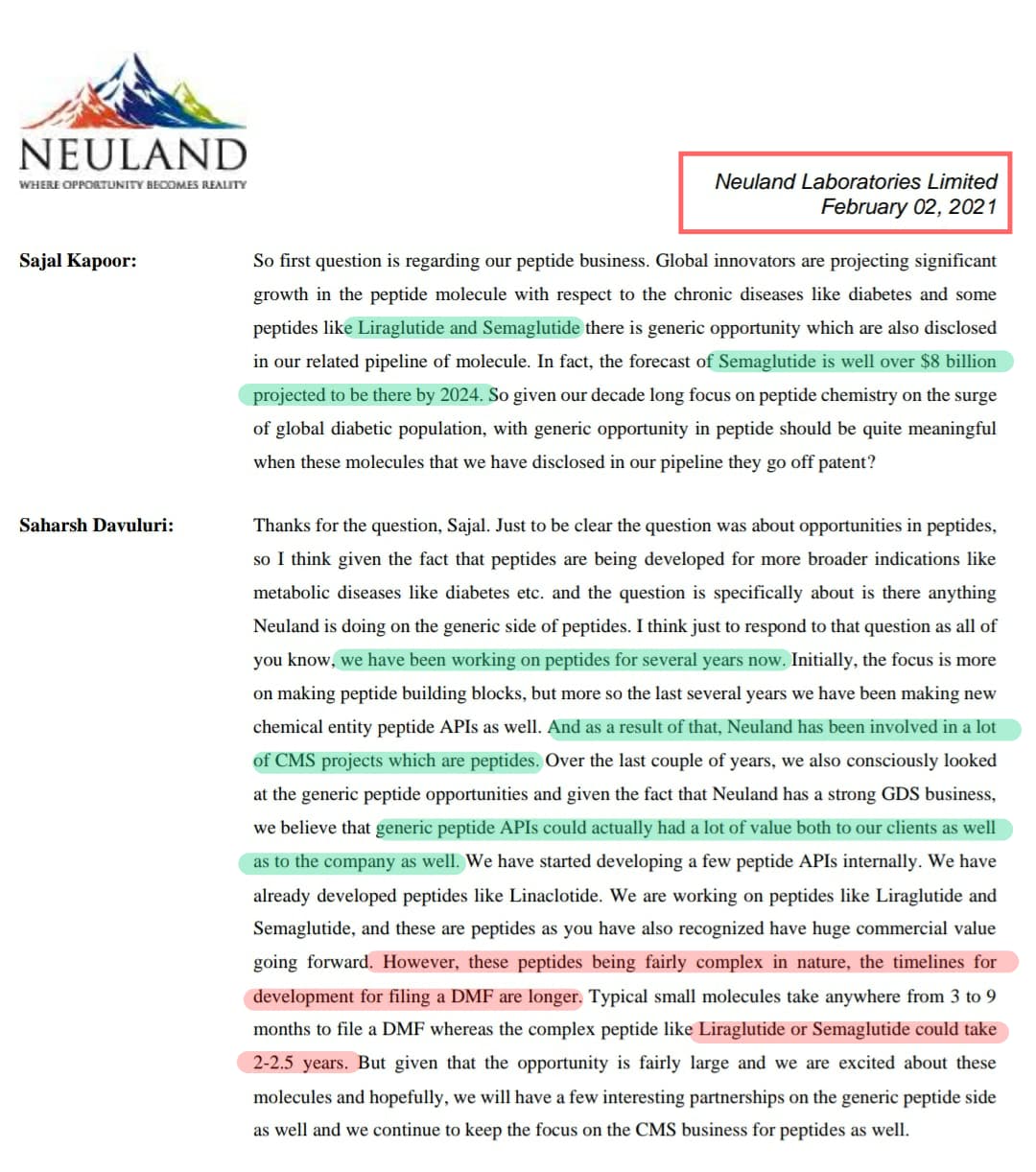

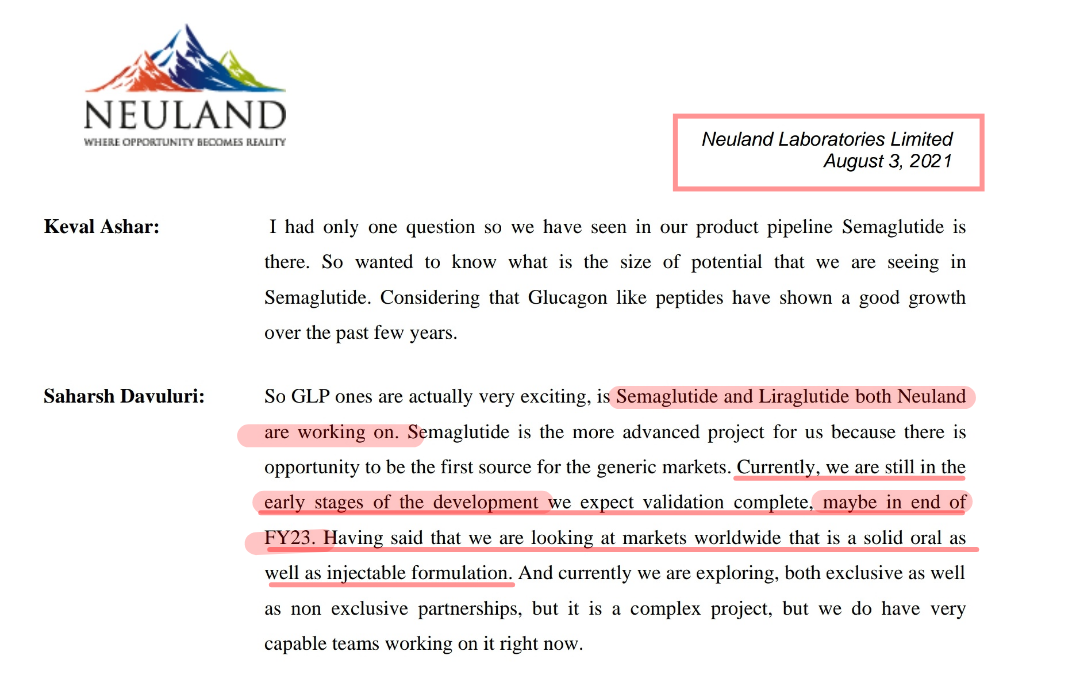

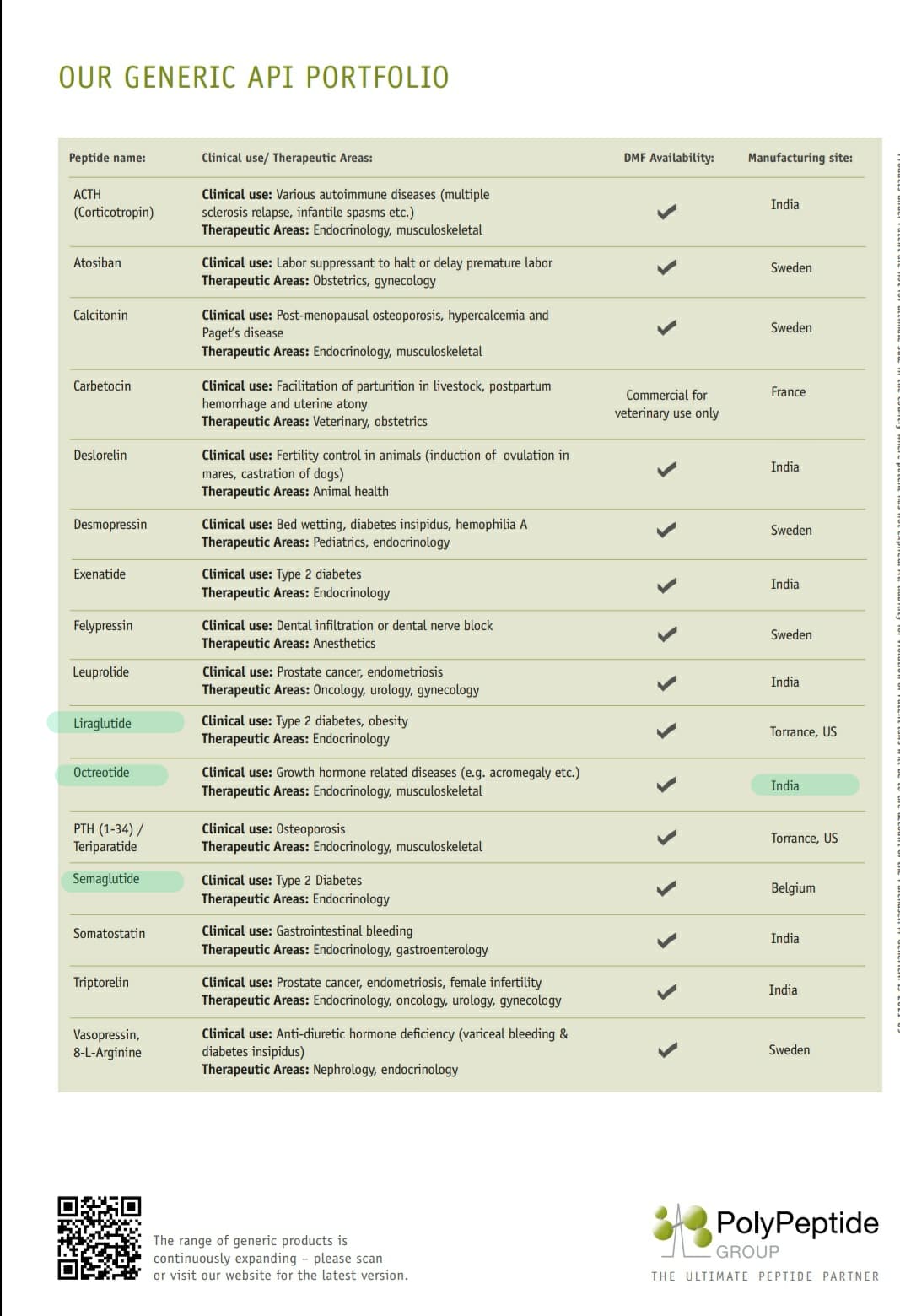

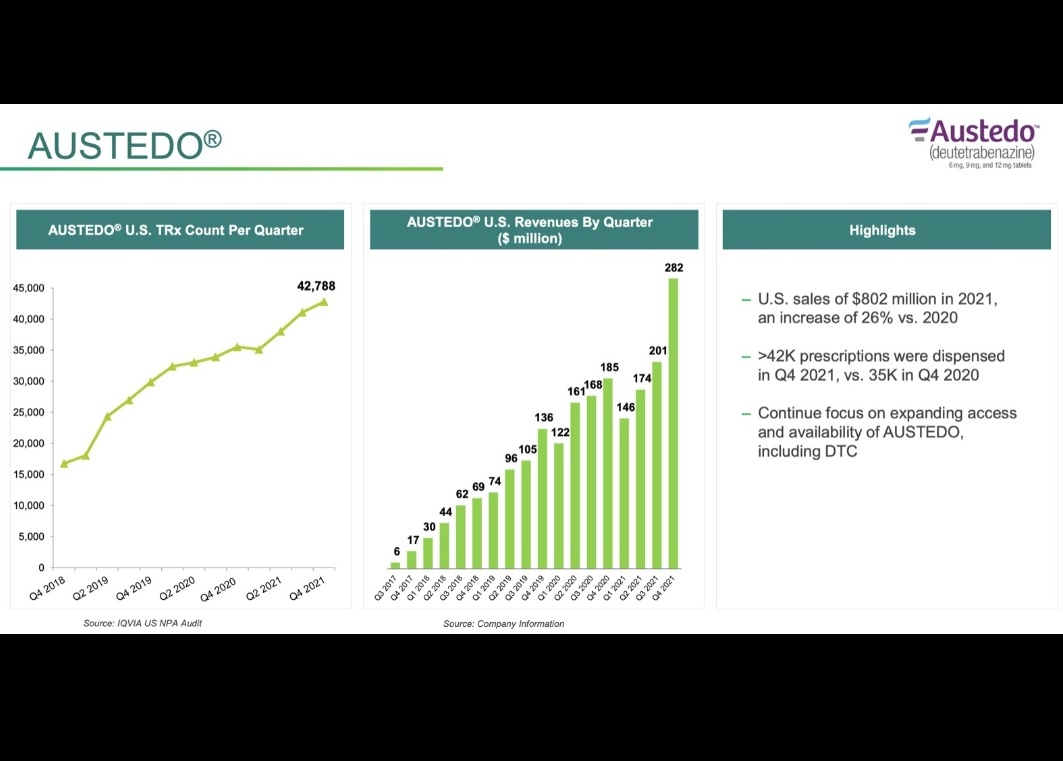

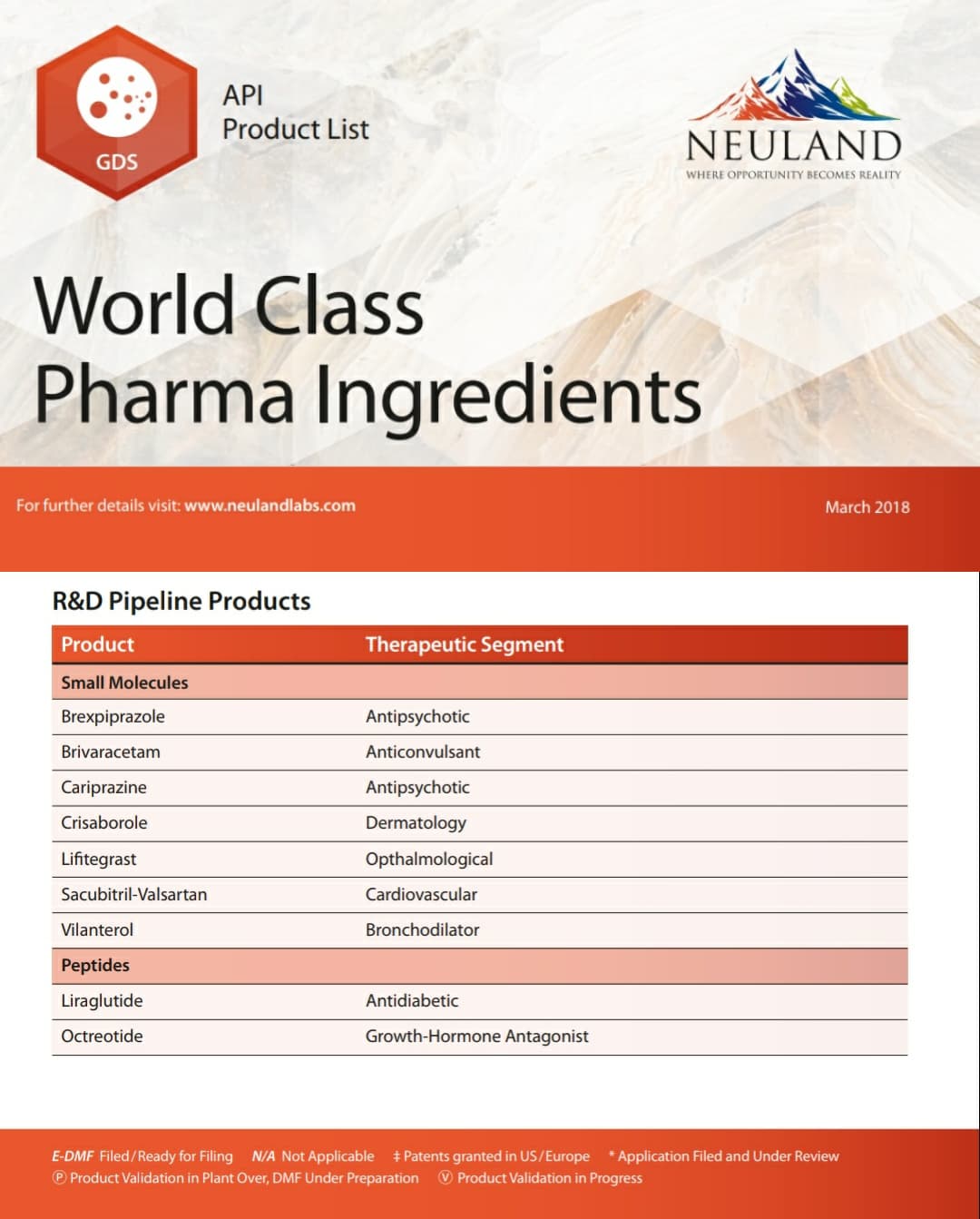

GLP-1 agonist peptides Semaglutide and Liraglutide are 2 molecules which I’m very positive on their future potential. I have been keenly watching Neuland for their ability in peptide space and to know more about their commercialisation plans of these 2 peptides.

They have been developing both these peptides from early 2019, I believe.

In the past, management had guided that it would take 2 years to file a DMF of a peptide molecule. But it has been nearly 3 years, and they are still in early development phase and expect to file DMF at the end of FY23. In annual reports and blogs, they had always highlighted about their expertise in the peptide manufacturing. But we are yet to see a peptide DMF filing from Neuland. I will wait for some execution from the management.

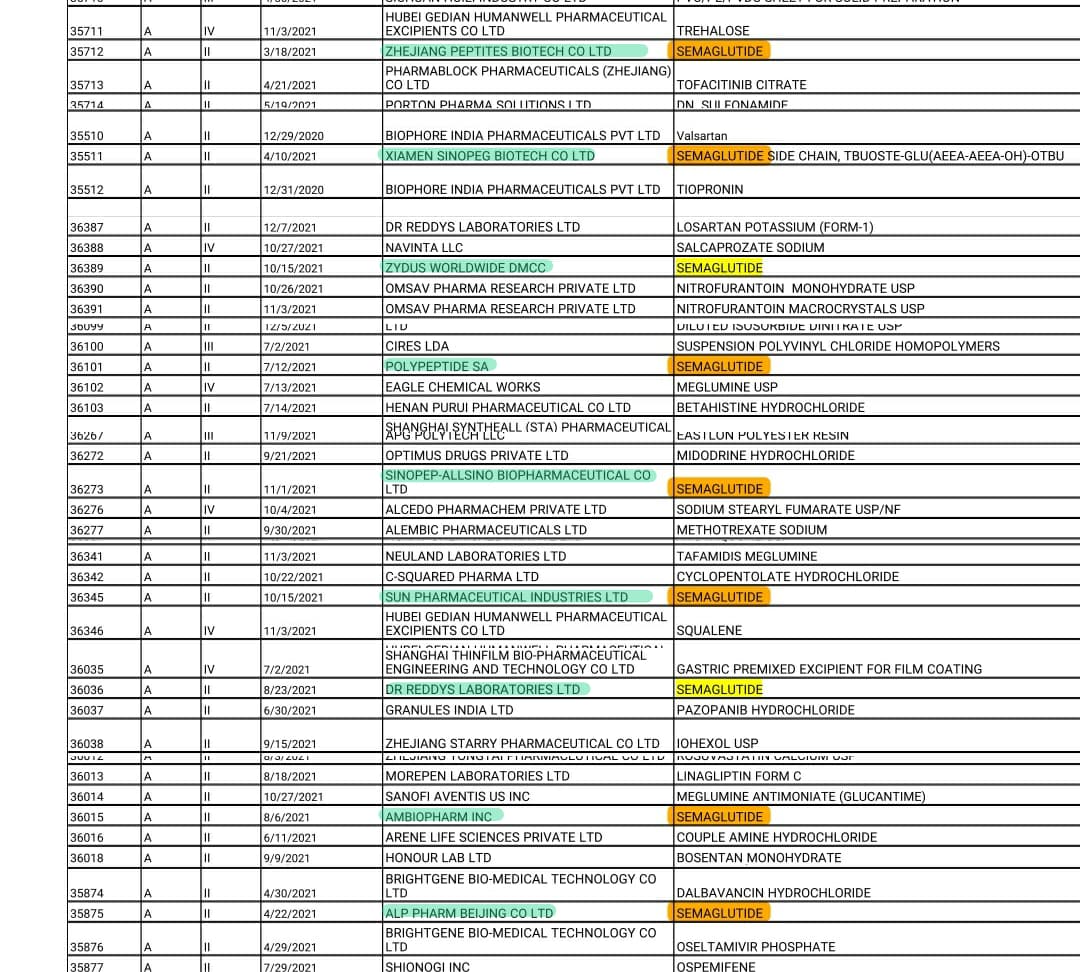

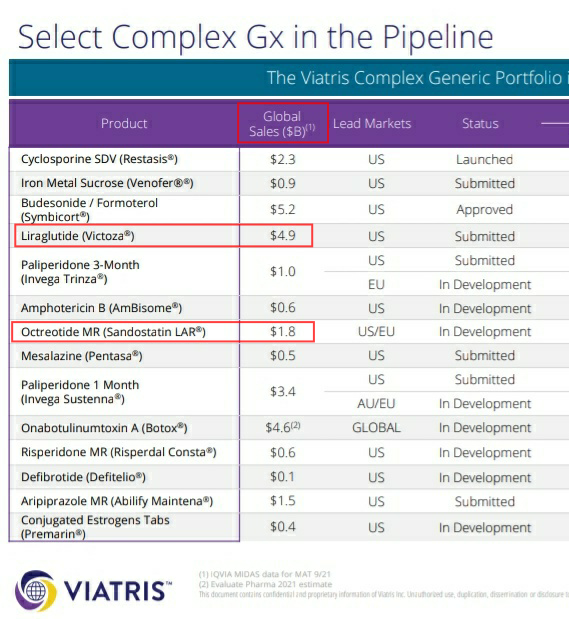

In one of the previous earnings call, they had mentioned about their aspirations of being the first to supply generic versions of Semaglutide locally and internationally. But now, Indian players like Dr.Reddy’s and Sun pharma have already got US-DMF for Semaglutide. Bigger player like Piramal pharma is also developing Semaglutide and Liraglutide. Almost 20 players are working on these 2 molecules globally and almost 9 of them have got US DMF.

Competition is little more intense in Liraglutide. Indian players like Biocon, Sun pharma, Dr.Reddys have already got US DMF for Liraglutide.

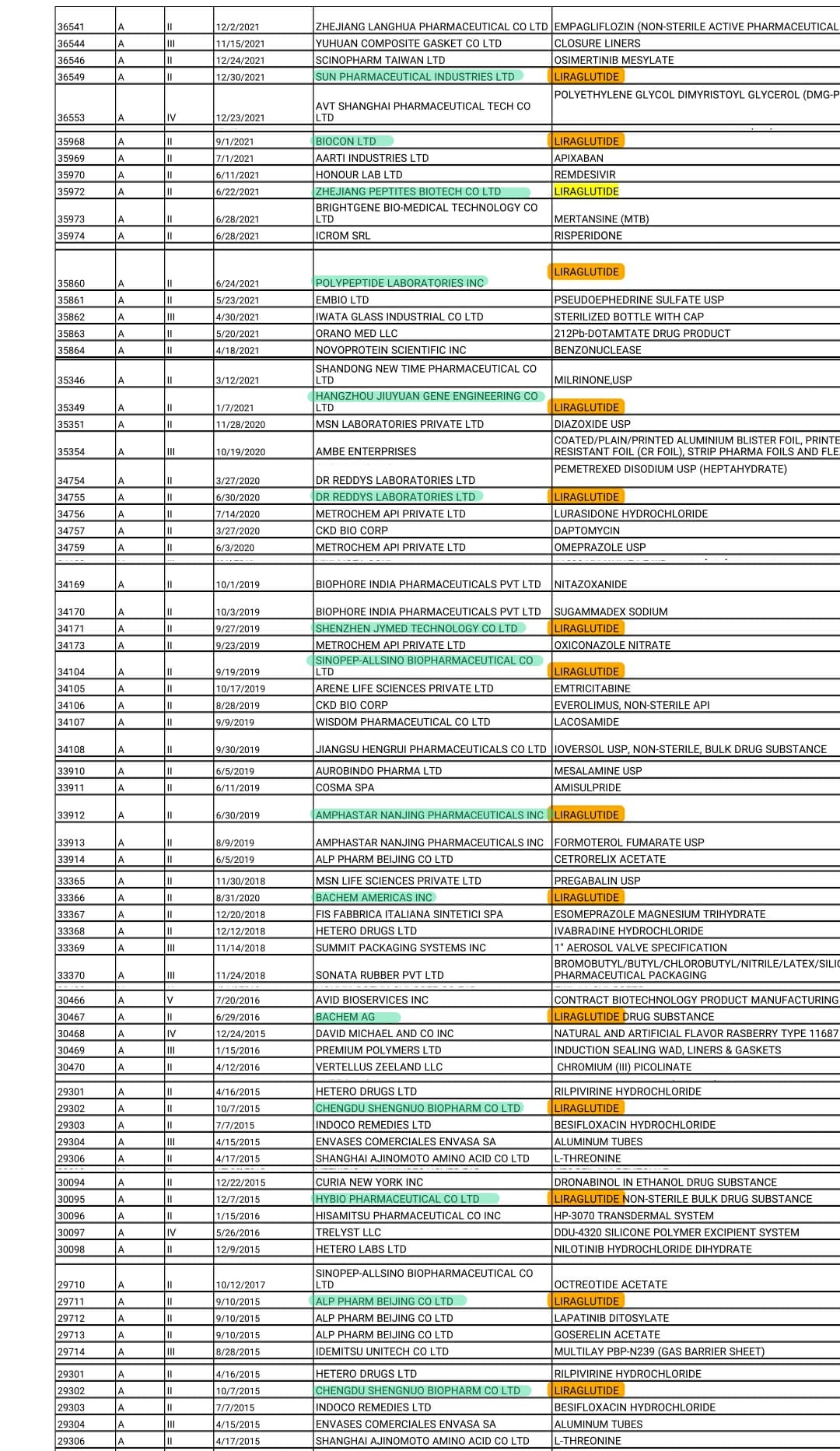

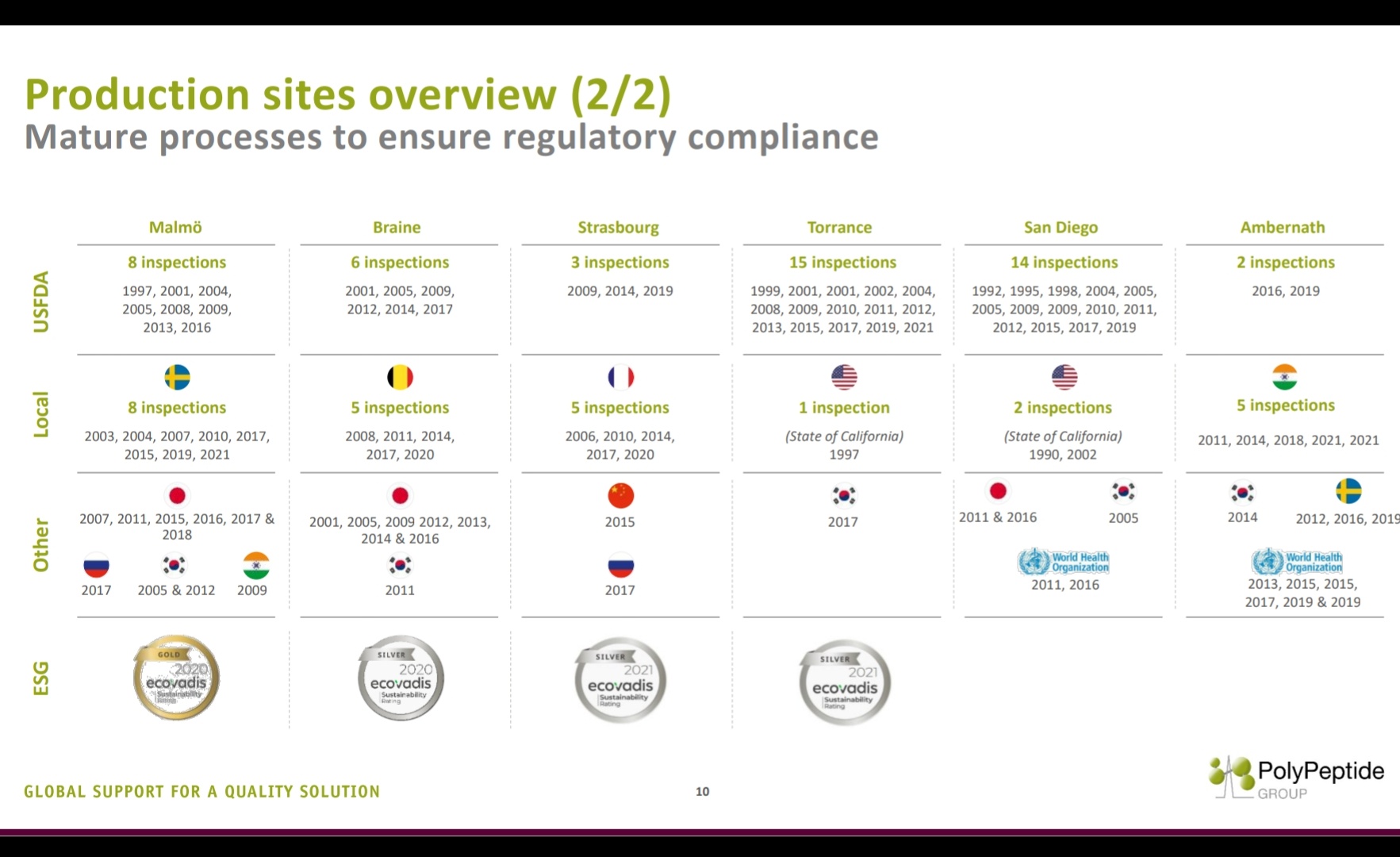

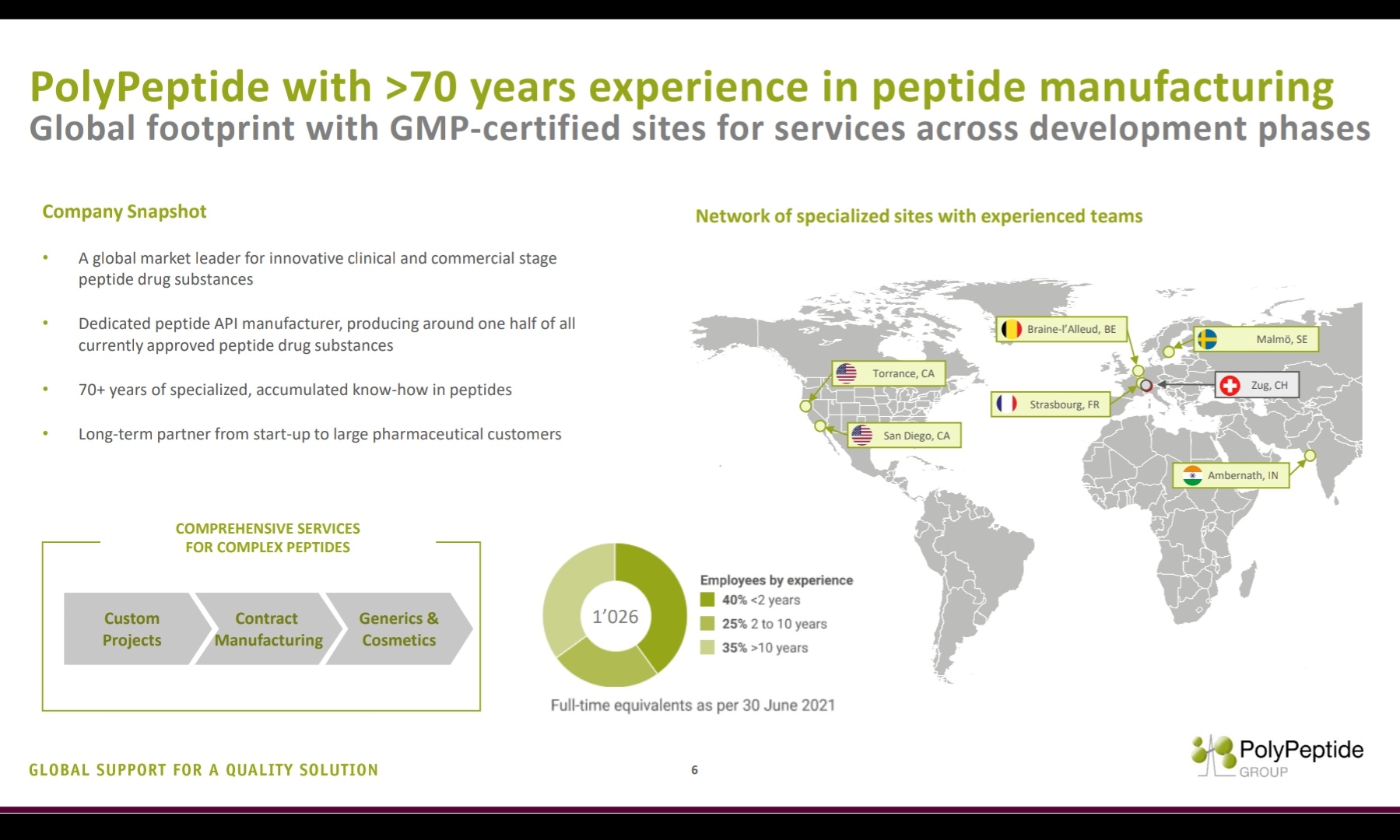

In the peptide space, one CDMO worth watching for is Swiss based ‘Polypeptide’.

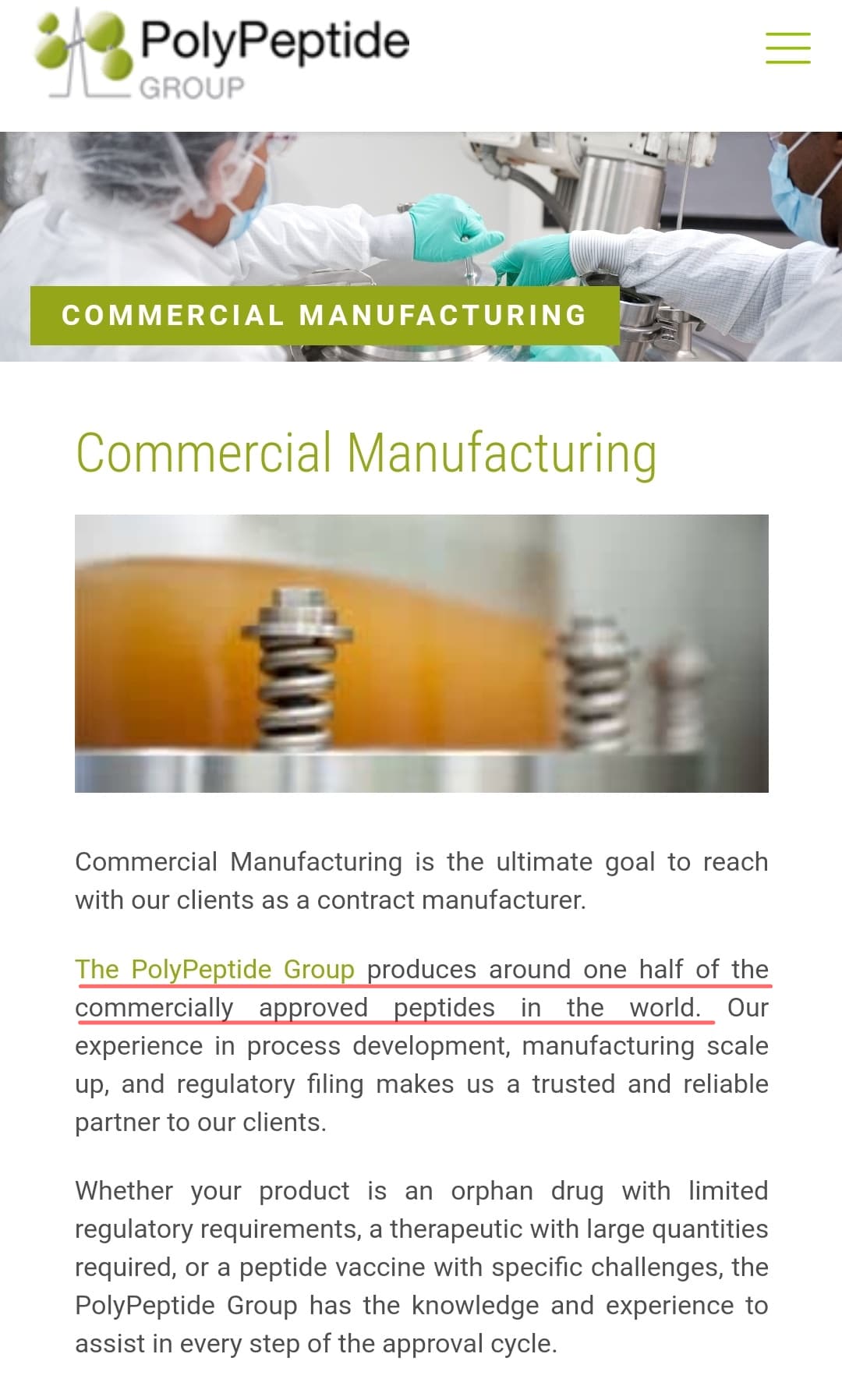

I think they are the largest peptide manufacturer in the world manufacturing nearly 50% of all currently approved peptide drugs. (Remember, Neuland is yet to file a peptide DMF)

Another concerning aspect is Polypeptide has got 6 manufacturing facilities and one of those facilities is in India, strategically placed near a port.

It will be interesting to monitor how Neuland make use of it’s expertise on peptide field and how fastly and efficiently they develop the commercial volumes of peptide molecules.

Disc: Tracking, studying. Don’t have any position. Might add if price becomes favourable for me.