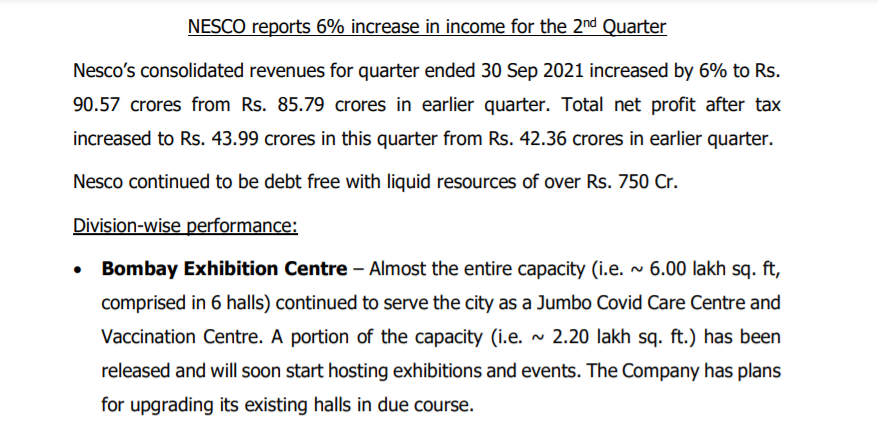

Company’s liquid resources (fixed maturity plans, mutual funds, cash and bank balances) increased by 19.48% to 819.23 cr. from 685.67 cr.

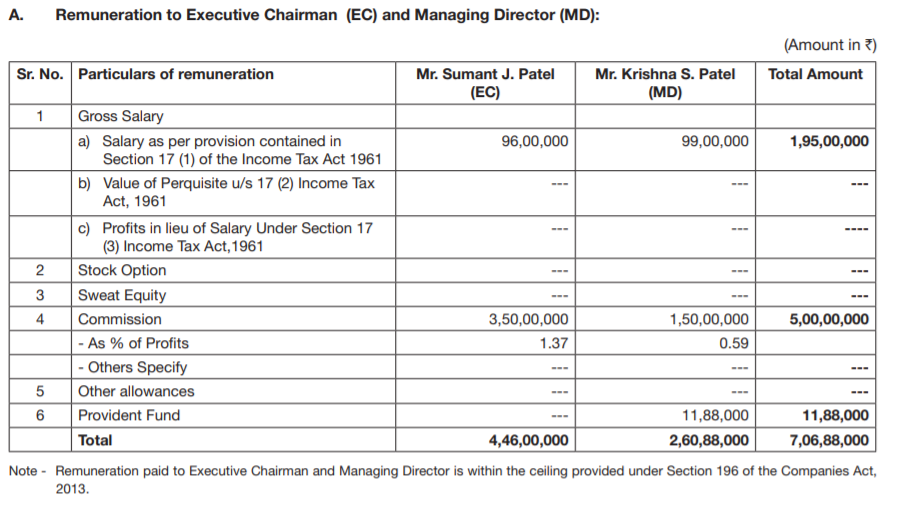

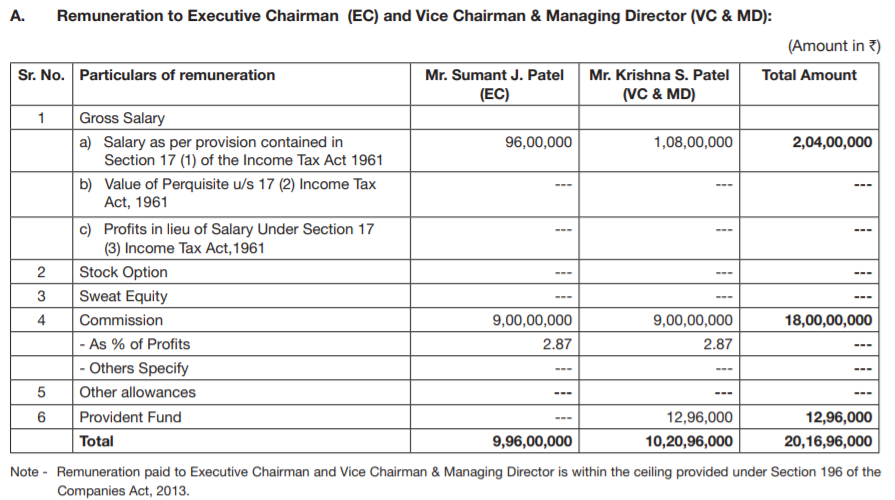

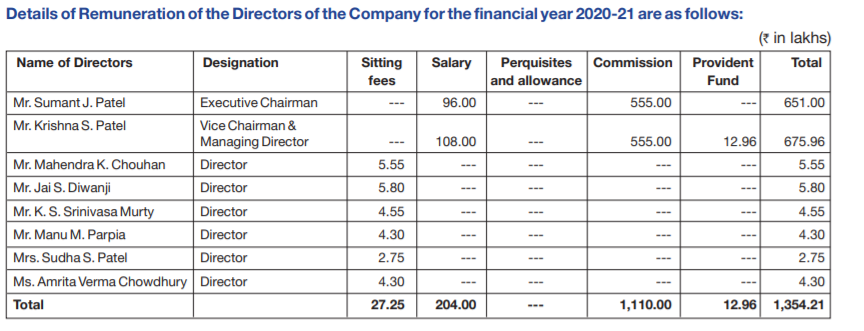

There was a decrease in the managerial remuneration for the year by 31.64% and increase in compensation of other employees by ~10%

Expansion plans

o Nesco IT Park is expecting to complete the designing & finalization of plans for the new Tower 02 which will be located in place of legacy IT building 02 and the adjoining areas. The designs are made by Singapore Based Architects – Aedas and the total development size will be about 4.6 million sq. ft. that includes office space, hotel, car parking and other amenities. Estimated cost is 1800 cr. with outflow spread over 5-years

o IT Park Division is planning to complete the F&B and Retail areas in Tower 04 which include new Restaurants, Food Court, Gym, Convenience Store, Salon and a Coffee Shop. The expected cost is approximately 50 cr.

Indabrator division, the abrasive plant manufacturing capacity of 2000 MT/annum has been ramped-up to 6000 MT/annum and expected to generate revenue of approximately 25 cr. on full capacity basis

Number of shareholders: 39’865, price (low): 380, price (high): 639

Here are the detailed business metrics since FY13.

The reduction in Managerial remuneration should be taken with a pinch of salt. Mr. & Mrs. Patel were paid 7.06 crore in 2019 which increased to 20.16 crore in 2020 (in a pandemic year) and is now reduced to 13.27 crores. So, In essence, they have almost doubled their remuneration in two years while the Investors are having lower EPS than 2019.

In fact, The reduction in remuneration has happened in 2021 because the Net profit of the company has gone down by 30% (ring a bell?). Since they can’t pay themselves 20 crores when Net profit is 170 crores only (10% limit), they had to reduce the remuneration. I would not be suprised if it goes up this year once the Net profit is up again.

While I will not call it a red signal on corporate governance, it’s definitely very close to that.

There has been increase of 22 crores YOY in other income which is mainly interest income

But increase in investments during the same period is 53 crores. Investments are maily in non convertible debentures.

Why is the interest income so high YOY Or am I missing something?

Was trying to assess moat of NESCO in context of its attractiveness vis-a-vis REITs. I found that REITs have certain advantages over n : -

Distribution of dividend : - REITs are bound by regulations to pay out 90% rental income as dividends whereas NESCO has to conserve cash to keep on funding further construction on its land. Hence the dividend payout is low & bound to remain low.

Diversification : - REITs have advantage of geographically diversified properties vs. NESCO which is concentrated in Mumbai only which increases single location event risk for it.

Capital Appreciation : - This probly follows from (2) above. More geographically spread properties means more chances of capital appreciation & subsequent rise in NAV of units. Whereas in NESCO’s case the price appreciation is only dependent on earnings’ growth - rental income + Exhibition income - which is nyways going to be subdued for sometime.

The whole point of bringing this up is that isn’t NESCO’s wide MOAT is not as wide now as it was earlier with listing of REITs & thr attractiveness as investments. So, isn’t nesco’s multiple at the risk of getting de-rated or not further re-rated going ahead. Of course, if the mgmt decides to take certain actions thngs can change.

Would love to hear long time n investors thoughts on this. Wat makes you buy/hold this stock vs. an REIT?

Disclosure :- No investment as of now. Was invested earlier.

One would always want to expand, provided if they think the success could be repeated.

I think the reason could be both a qualitative and quantitative one.

I don’t know about the management, do they have hold on Mumbai area/market only? To move to other cities and build real estate and do business, can they do it on their own or do they have to do a JV with someone else like Ashiana does? Who would want to lose control, when they can expand and grow where they are?

The profits will also be less if they don’t know about the nuances in other cities you mentioned. There have to be similar events happening and similar environment existing for Nesco to venture into those cities and become profitable. The fixed assets jumped from 213 crores to 776 crores in FY 20. They have done capex. So they don’t want to go to other cities, check the thread.

And I guess, your question may have been asked before, to the management, and they may have already replied. Check concalls or transcripts. Or they may have mentioned about this in their ARs.

The main reason is cost of land. The Mumbai land was owned by company frm many yrs back, thus cost of land is very less compared to developing same piece of land parcel today.

In any other city, they vl be on par with others as far as acquiring land & developing it is concerned. In fact, REITs vl anyways beat them in that game with thr comparitively massive scale. Question is, is that the business that they want to be in. Thn probly a solution is something sort of to hive-off land asset in a separate co. & then leverage that. Bt I blv development is not thr core competency it seems.

It looks like the Government officials do not want to let go of this prized asset. I can understand that government needed land to quarantine/ cure people during height of the pandemic but to keep 4 lakh sq. ft with you in middle of BKC area without paying a penny for just vaccinating people (I would be surprised if Covid care centre has any patients in it right now)? Can’t they do it at a regular Civil hospital?

“With deep regret, the company informs that Shri. Sumant Jethabhai Patel — Executive Director and Chief Mentor of the Company, left for heavenly abode on 17 November 2021.”

This is a big blow. I remember seeing him on CNBC/BloombergQ since many years. Always spoke with confidence. Om Shanti.

Nesco: JIO exhibition center would be solid completion . How ever greater mumbai area can have two large exhibition center. Another thought , if nesco’s exhibition segment goes down , can it be used for IT building and nesco becoming almost an REIT ?

What would be the valuation at which Nesco is screaming buy? I guess its 15x EVEBITDA should be decent since its debt free and will remain debt free and if co doesnt. need to invest further ,we might be earning 5% dividend yield with tool business for free

1 question - Why did u used EV\EBITDA as a valuation multiple here? It vl be ineteresting to know your line of thought but as far as I know, the “D” for NESCO will always understate its earnings as the cost of maintaining buildings is always way less than the cost of constructing them - which happens in phases and comes with associated risks.

2 observations -

(a) It won’t become an REIT with all its buildings converting into offices. YOu can refer my earlier comments on this thread regarding that difference. Also, because it won’t have REIT regulations levied on it, won’t its valuation will always be lesser than the actual REITS - which bound by regulations have to distribute thr earnings always.

(b) 5% dividend yield - This won’t happen bcoz its part of company’s business design and probably a partial contributor to its moat. These cash/investments are accumulated over the yrs for construction\renovation\expansion works.

sorry , I was not clear.

EV\EBITDA because with maintenance as main expense , negligible interest cost I thought it would be good scale.

yes It would not become REIT technically but for investor it may become like REIT=> income going into dividend or buyback . Of course first few years ,max income would go into building new buildings.I am talking about the time when their exhibition becomes minuscule segment and rental income becomes 3x from here.

My two cents on the recent discussion here about NESCO exhibition business going zero and turning into (about) a REIT:

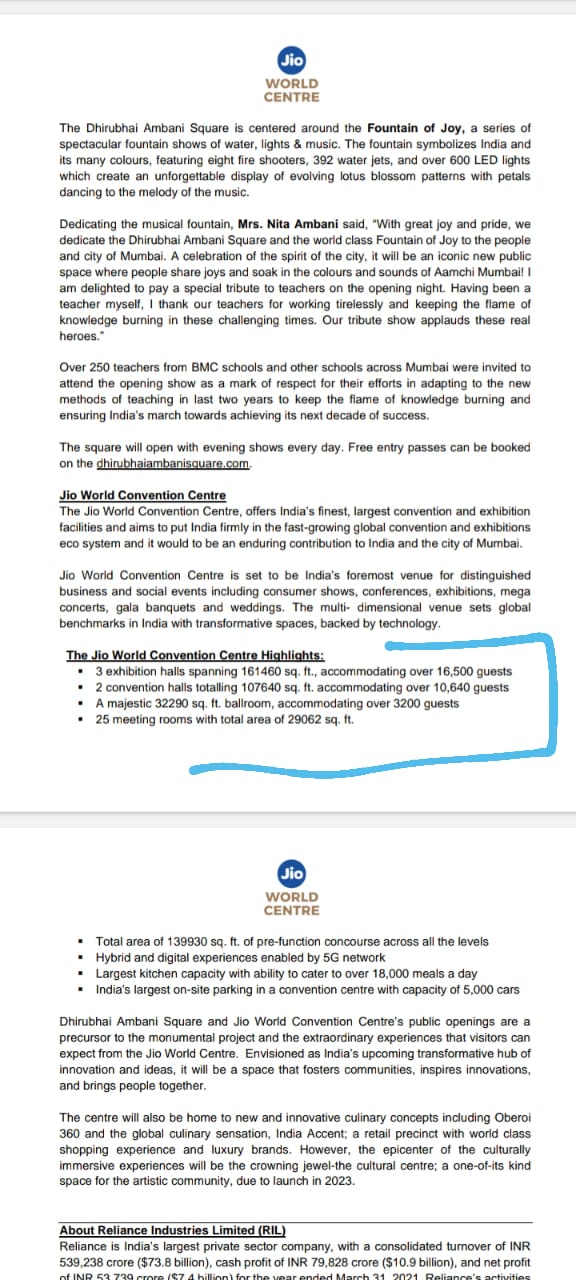

NESCO, even currently, have much much higher exhibition space than the new JIO World Centre. With the slated expansion, NESCO exhibition space would be more than 6 times of JWC.

JWC has huge (largest in India till date) Convention Centre. However, convention and exhibition are two very different genres of the larger MICE industry. They appear similar, but have very different clients. IMHO, convention is a lower margin business (20-30%), whereas exhibition commands margins as high as 70%. Anyways NESCO was never in conventions, so no effect whatsoever.

Location of NESCO is quite far away from JWC and hence cater to quite different audience. Moreover, in the greater Mumbai region, NESCO is more centralised than JWC.

In developed countries like Germany, China, Canada, US, etc. (in that order), large cities have more than 4-5 large expo centres. So India’s financial capital can easily have 3-4 centres.

For me, the main attraction of NESCO is it’s niche exhibition venue business, which is high margin and a BIG moat.

Disclosure: invested and an exhibition professional

Maybe I wasn’t clear in my point earlier - exhibition centre biz or not - For NESCO to become an REIT, lot of restructuring will have to be done with the company to be divided into one holding land asset and another operating its buildings and biz. It won’t be worth the effort.

Some of the listed REITs hold assets other than commercial office space so an exhibition centre biz might be accommodated, but the whole point is - why?

The only concern is - which I mentioned a few posts back as well also was - the onus now is on mgmt to ensure that IRRs from NESCO projects is greater than its listed REIT peers. Otherwise,why will a rational investor buy this and not the other listed REIT stocks.

MOAT - There are 2 aspects to MOAT - Its breadth and its depth. Yes, NESCO has a wide moat due to its location advantage, despite JWC coming up.However, the moat, I believe is not deep enough as its prone to single location risk. Macro events like terrorist attacks,lockdowns and now emergence of online\virtual events do pose a risk to its exhibition business.