Few interesting observations on NESCO

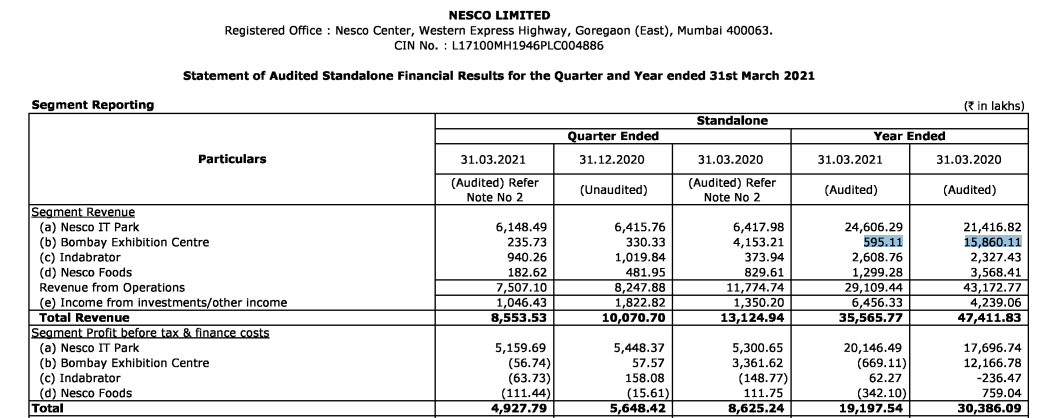

- Entire exhibition business contributing ~150 Cr revenue and ~100 Cr profit (FY20) is decimated since Covid outbreak (FY21 & FY22)

- However overall profits decreased by only ~ 50 Cr (from ~250 Cr in FY20 to ~200 Cr in FY21 & FY22)

- Increase in profitibility (~ 50 Cr) from IT Parks business (due to commencement of new building and higher leasing) compensated overall decrease in profitibility (~100 Cr).

- Assuming exhibition business will get normal in couple of years, the profitibility will see a jump of ~ 100 Cr going forward.

So overall profitibility can be 300 Cr on steady state basis, along with company holding 800 Cr cash that it plans to deploy by building 2.5 million sq ft leasable space and enhancing exhibition center from 5 lakh sq ft to 10 lakh sqft.

Growth is visible ahead but execution needs to be monitered.

Risks:

1)Time will tell if office leasing business is impaired with WFH culture being accepted by multi-nationals.

2) Single location dependency augurs risks.

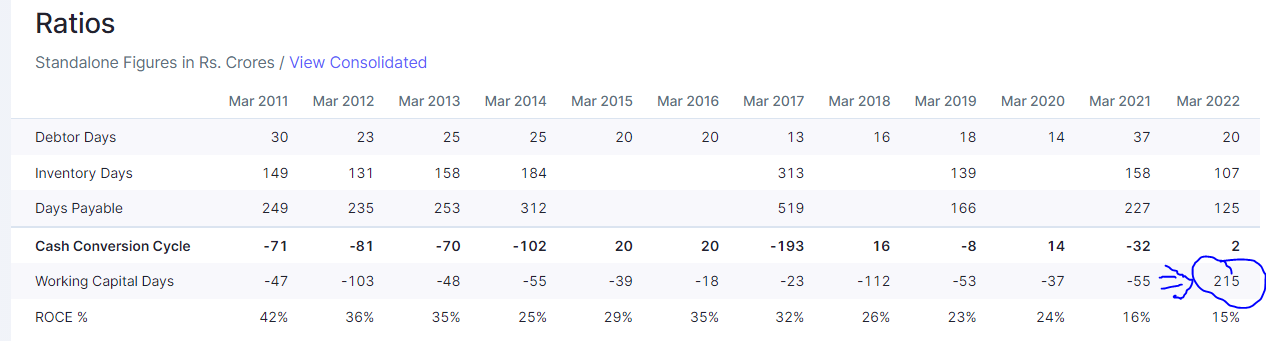

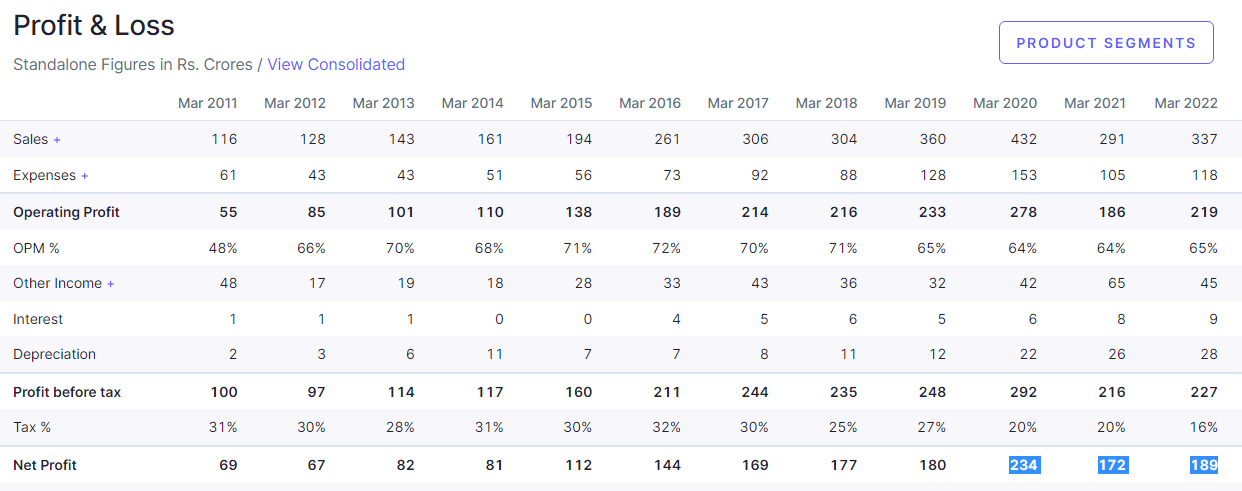

Overall Profitibility

Segmental decrease in revenues and profitibility

AR 2022 notes

- 80% of Tower 03 (same as FY21) and 92% of Tower 04 (vs 75% in FY21) are occupied

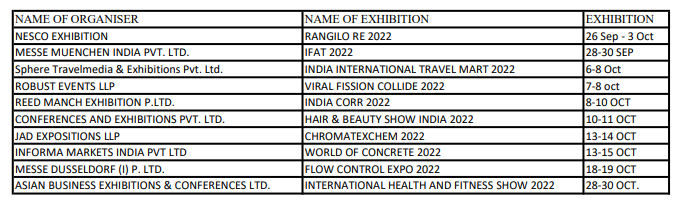

- Had 12 guest exhibitions in BEC (from Nov 2021 to March 2022) with 21 planned in FY23. Exhibitions organized were Acetech 2021, Tech textile India 2021, International Health, Sports 2021

- Bombay Exhibition business includes 73% of exhibition area within Western and Northern region - Western (38%), Northern (35%), Southern (24%), Central (2%), Eastern (1%) and it primarily focus on B2B events

- Company’s liquid resources (fixed maturity plans, mutual funds, cash and bank balances) increased by 4.46% to 855.79 cr. from 819.23 cr.

- Sumant J. Patel passed away on 17th November 2021

-

Expansion plans

o IT Park: Completed designing & finalization of plans for new Tower 02 which will be located in place of legacy IT building 02 and adjoining areas. The designs are made by Singapore Based Architects – Aedas and the total development size will be about 4.6 million sq. ft. that includes office space, hotel, car parking and other amenities. Estimated cost is 2000 cr. (increased from 1800 cr. estimated in FY21) with outflow spread over 5-years

o IT Park Division is planning to complete the F&B and Retail areas in Tower 04 which include new Restaurants, Food Court, Gym, Convenience Store, Salon and a Coffee Shop. The expected cost is approximately 50 cr.

o Completed conceptualization for landscaping of Tower 03 at cost of 4 cr. which shall be undertaken in FY23

o For FY23, Nesco Foods is planning to increase its revenue stream by foraying into outdoor catering and B2B contracts outside the Nesco Center and operating two brands in food court named as ‘Indic’ & ‘Daily Dely’ - Indabrator division: Abrasive plant manufacturing capacity is 6000 MT/annum and can generate revenue of 25 cr. on full capacity basis, two plants (Karamsad, Vishnoli)

- CSR spends: 4.97 cr.

- Auditor remuneration: 31.27 lakhs (vs 21.76 lakhs in FY21)

- Employees: 118 (excluding KMP), managerial remuneration reduced by (-34.75%), for other employees remuneration increased by 2.74%

- Number of shareholders: 36’630 (vs 39’865 in FY21), price (low): 463.5, price (high): 687.15

Here are the relevant business metrics since FY13.

| FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Total Revenues | 162.74 | 181.42 | 223.07 | 297.08 | 357.20 | 358.00 | 392.60 | 474.28 | 355.70 | 382.41 |

| IT Park | 27.86 | 47.83 | 90.67 | 124.40 | 141.91 | 145.40 | 137.00 | 214.17 | 246.06 | 264.15 |

| Exhibition centre | 90.52 | 94.89 | 85.86 | 111.83 | 132.77 | 129.70 | 156.00 | 158.60 | 5.95 | 16.18 |

| Hospitality services | 5.60 | 20.40 | 34.10 | 35.68 | 13.00 | 11.35 | ||||

| Indabrator | 25.08 | 18.39 | 17.91 | 27.93 | 33.89 | 26.40 | 32.50 | 23.27 | 26.09 | 45.71 |

| Investments | 19.28 | 20.31 | 28.62 | 32.90 | 42.98 | 36.10 | 33.00 | 42.55 | 64.60 | 45.01 |

| KMP remuneration (cr.) | 3.60 | 3.75 | 5.11 | 6.06 | 7.06 | 7.58 | 8.02 | 21.49 | 13.54 | 9.06 |

| Audit fees (lakhs) | 7.85 | 9.55 | 11.01 | 11.50 | 15.60 | 19.85 | 21.69 | 21.68 | 21.76 | 31.27 |

| Employees | 121.00 | 135.00 | 166.00 | 131.00 | 159.00 | 155.00 | 130.00 | 118.00 | ||

| KMP remuneration to sales | 2.21% | 2.07% | 2.29% | 2.04% | 1.98% | 2.12% | 2.04% | 4.53% | 3.81% | 2.37% |

Whats good to see is that KMP remuneration has come down significantly since FY20.

Disclosure: Invested (position size here, no transactions in last-30 days)

I think managerial remuneration was a concern earlier. 34.75% decrement in salary is too much of a pay cut. why it was reduced so much in a year ?

Somebody correct me if I’m wrong. But in 2020, the Managerial Remuneration was almost doubled and the additional funds were used by the Promoters to purchase Stock in the company.

The Salary as a % of Profits has remained similar throughout the recent years, but the Promoters essentially gifted themselves additional Stock in the company in 2020.

Correct me if I am wrong but the promoter of Nesco is Patel family and also related to or same Patel family who are promoters of Gmm pfaudler. And we all know the management shenanigans of Gmm…

Any idea why profitability for the IT park is down QoQ?

Any idea why prices are up 20% in last two days.

Regards

NESCO.pdf (555.8 KB)

NESCO has been one of the worst hit stocks in the pandemic. It faced a triple whammy:

- No exhibitions due to the pandemic resulting in loss of income from BEC as well as NESCO Foods which supplies food & beverages to the exhibitions

- Poor lease realisations due to the “work from home” operations of most IT and Finance companies

- Exhibition center being taken over by Municipal Corporation for Jumbo COVID Centre, which would have prevented them from investing in modernisation & upgrades during the lean period.

Add to this is the fear that the new Jio Convention Centre at BKC will eat into its business.

As per page 2, point (ii) of the Chairman’s Speech at the 63rd AGM attached for reference, BEC has the capacity to hold 150 exhibitions per annum, whereas the last year saw only 16 exhibitions, which is barely 10% of the capacity. In other words, BEC could increase its exhibition business by 10x without any new major capex.

The Annual Report 2022 page 20, mentions that in a typical year, BEC can hold 745 different events (not just exhibitions).

During COVID, many people claimed that work from home and online marketing will be a permanent change. The ‘touch & feel’ of seeing products in real or watching gadgets / equipment “live in action” in a physical exhibition is not possible to replicate with an online digital medium. Therefore, I do not believe that exhibitions are dead. My belief is that face-to-face interactions with clients, suppliers, live product displays etc. are all either back to normal or on their way to returning with a Big Bang.

Many tech companies have also raised a problem of employees’ moonlighting due to work from home (i.e. working on a 2nd job). While the right & wrong of moonlighting are being debated (and I do not wish to comment on that), the only meaningful way for the management to control this problem is to bring everyone back to office. Meaning, NESCO’s IT Park should also see good demand going forward.

As described by some of the earlier posts, Jio’s Convention Centre is not a direct competitor to BEC. So I won’t repeat this point.

Against a 10 year median value P/B of 3.4, the current P/B is only 2.7. NESCO’s sales & income both appear to be severely depressed on account of COVID factors, which now appear to be in the rear view (hopefully). The major long term valuation depressor would be that NESCO’s single location risk has now been thoroughly exposed.

However, I think that the earning power of the main assets that NESCO owns - BEC and IT Park has not diminished in any way. Many of us may have encountered the post-COVID huge spike in prices of all events - weddings, parties, etc. It is very much possible that with a sudden surge in demand for exhibitions and no major supply of new exhibition centres in Mumbai, BEC should be able to even command premium pricing.

I feel that the bad news has been baked into the price and we should be able to see mean reversion in the business prospects as well as stock price.

Disc: Biased, invested from much lower levels and holding for more than a decade

FIIs have increased stake in September 22 we may expect some positive move in near future. So far this stock has disappointed a lot.

Anyone aware of IT Building 4 occupancy percentage…is it fully rented out ?

b91b1248-e596-43e8-9106-c37f2b614b16.pdf (6.4 MB)

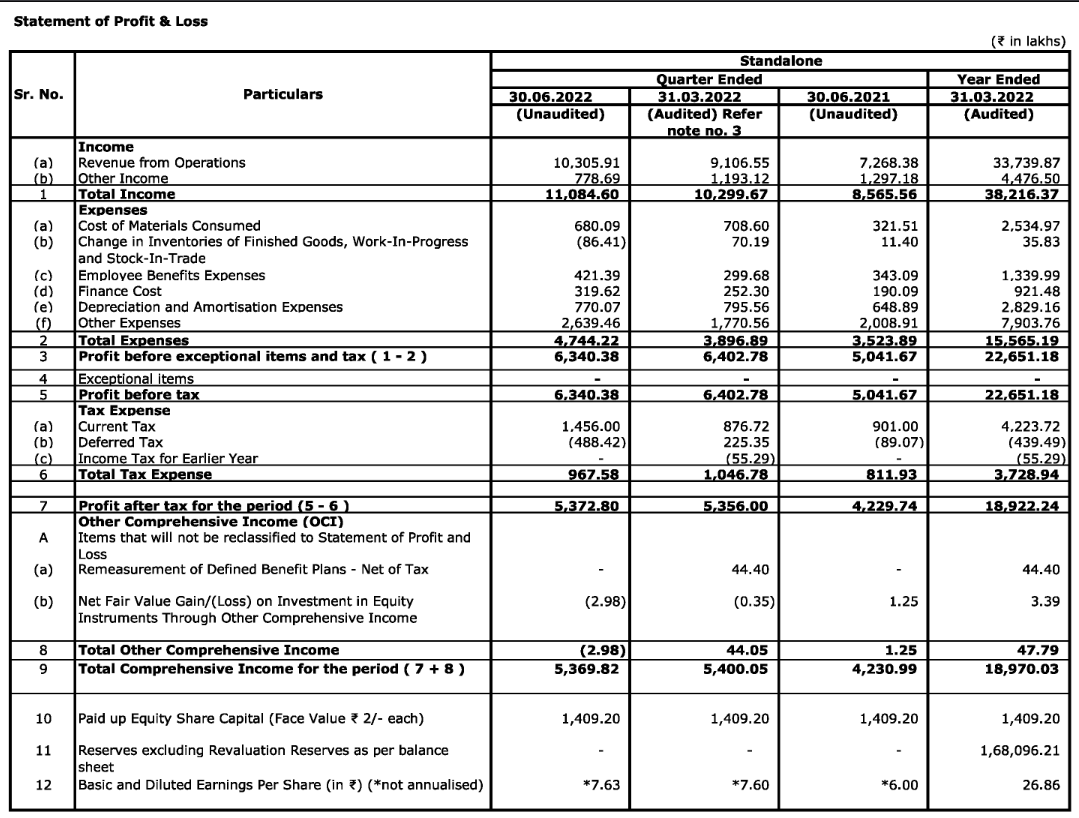

very good result…seems NESCO is back to normal business…

hi

so Jio’s center is up and running. here are its dimensions -

The above hall can be one contiguous zone if required -

while NESCO has a capacity of 60,000 meters (4x of Jio), the same is divided into 6 different halls. its biggest hall is 19,143 m, making it larger than JIO on a standalone basis, but other halls are smaller (12,000 and less) -

As such Jio seems to be a worthwhile competitor to NESCO. I am trying to figure the difference is prices for the 2 venues. Is there any way to figure the same?

@Saurabh_Sharma1 - could you tell us the difference between convention and exhibition as far as space and fundamentals go?

thanks

disc - invested.

Convention Centre (CC) business is highly linked with having 4-5 star hotels in vicinity, link with airport and quality of F&B. Also it’s a capex and opex heavy biz, as CC is very costly to run & maintain, even if it is not being used. Moreover, large conventions are dependent not just in the venue, but on the prestige of the city/country.

In sharp contrast, Exhibition Halls are more domestically linked biz. They are cheap to maintain and can be used for versatile uses. Not much opex is required, once capex has been redeemed.

In easy terms,

CC biz is more like airports/hotels

Exhibition is more like rental commercials

Above all, Reliance is here to earn name (irrespective of profitability, they have tonnes of cashflow from other biz), so they would focus on CC biz and not much B2B exhibitions.

thanks Saurabh, really helpful.