NCC - a reasonably priced stock given the growth outlook and earning acceleration of >20% YoY going forward.

Expect PAT to more than double over the next 2-3 yrs

(Views based on management guidance, PPT and transcript)

2 Likes

Can anyone suggest how to value NCC?

-

Infra space is a cyclical sector to some extent. For NCC, business primarily depends on govt spending on infra

-

A counter to above - If BJP is in power for next two terms, there will be considerable investment in this space and thus it presents excellent business opportunities

-

NCC (EPC) has very low margins in general

-

A counter to above - New projects are coming in at slightly better margins and higher order book helps in higher absolute profits

Just based on the above, how to value NCC?

What should be a reasonable PE?

What should be a reasonable Price to Book ratio?

2 Likes

Well, NCC is in EPC, and as far as I understand you must look at the D/E for sure before even considering the valuations. You may use Price/CFO and P/E. Further one can utilize using EV/EBITDA considering asset-heavy business.

1 Like

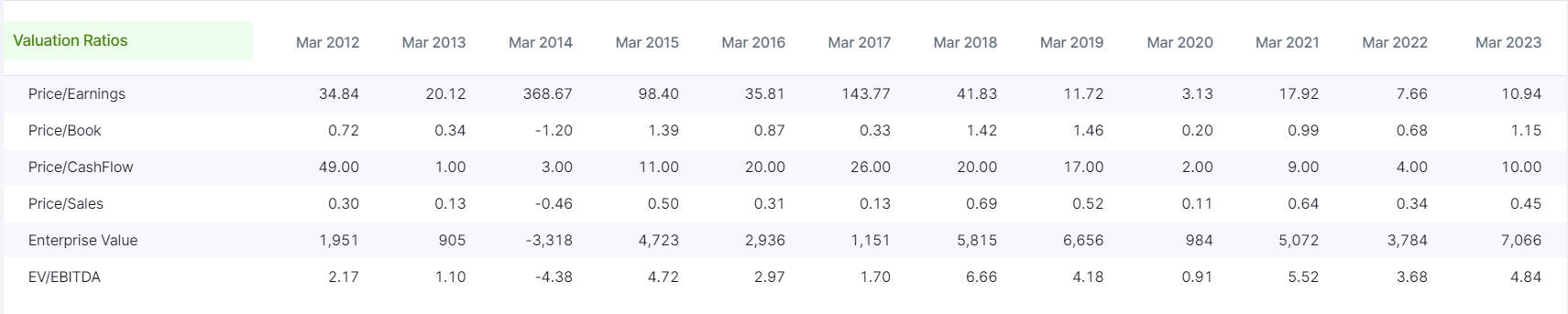

Companies in cyclical industries usually trade at their historical multiple averages. NCC’s long term P/E has been in 12-14 range. Current p/e is 20 which might be a little lower on a forward earning basis (assuming sector is still in uptrend). So to me NCC looks priced to perfection with respect to its historical valuations.

Now one might get tempted to compare multiples with peer group but one needs to account for different businesses that peer group companies might be in. A pureplay road construction company will get lower multiple than the one (e.g. IRB) that also does BOT (high margin annuity business).

If there were trigger for rerating of NCC’s multiple it might come from one or both of the following.

1- Whole sector getting rerated due to external triggers (e.g. government capex trends, improved payment schedules from state agencies such as NHAI etc)

2- Significant expansion in company’s margins due to either better efficiency in operational execution, favorable revenue mix or better receivables.

Without that I don’t see current multiples rising any further. (Of course not accounting for whims of bull markets which can often make mockery of valuations.)

2 Likes

Thanks for the good insight.

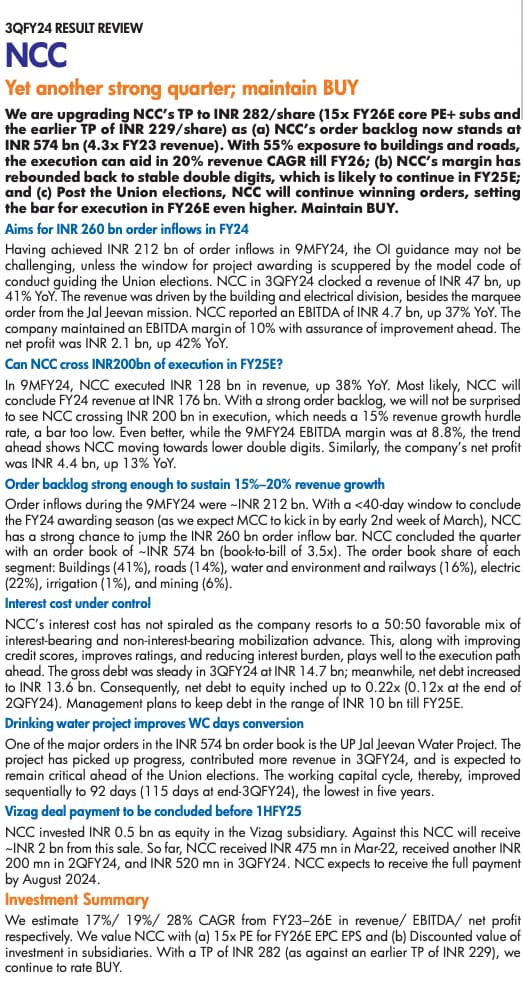

With the order book strength and the offtake in execution, I believe they can achieve anywhere between 15 to 20 rupees earnings per share in the next fiscal (roughly 20-24K standalone revenue with 5% net profit margins).

If the order book growth continues for an year (barring election related delays), a higher PE would be possible given that the cycle seems to be in the up move for a longer duration. Of course, it depends on what govt is able to achieve practically over the next 5 years

Well, stock price and P/E are two different things. A stock can give multi-bagger returns at the same P/E if earning keeps growing. So high order book and better offtake will definitely ensure earning growth and hence appreciation in stock price. But if that will lead to P/E re-reating is doubtful.

1 Like

Great earning acceleration lie ahead for the next 2-3 yrs

Basis management commentary and guidance on earnings ppt, Expect PAT to double from 650cr currently to ~1300cr in Fy25 and to cross 1650cr in Fy26 which for the CMP (Rs. 212) implies a PE multiple of 10 times on 1 year out earnings and a multiple of 8 times on 2 year out earnings.

For NCC, the PE multiple ascribed at cycle peaks crosses well over 22 times. Therefore, the stock has the potential to double in a couple of years at which point it would still trade at a very reasonable multiple of 16 times.

4 Likes

Company is continuously securing order from electrical division worth more than 5700 this financial year on DBFOOT(Design, build, Finance, own, operate, Transfer) basis. So the rerating of the company is very much on the cards.

1 Like

One of the factors for PE re-rating would be good CAGR growth for a reasonably foreseeable future. Hence, steady order inflows for another year and good commentary from govt on infra spending could trigger PE re-rating.

2 Likes

Order inflow has been very low in the 3rd quarter. No inflow in January as well. Will this continue for next 5 months, till elections are over?

2 Likes

Any views on NCC results?

I expected a standalone revenue of 5000+ Crores and net profit margins above 4.8%. But margins are lower at around 4.4%

Good news though is they are L1 for two projects worth 5200 Crores

From the Q3 FY24 con-call

Financial Performance:

-

The total order book as of the third quarter stands at 50,154 crores, with 3,660 crores attributed to smart metering projects.

-

NCC’s gel-driven projects have been awarded at 16,700 crores, with 43% executed by December end and an additional 5% expected to be completed by March end.

-

Revenue from operations for the 9 months excludes O&M figures, as longer O&M period turnover is not yet included in the current period.

Current Operational Performance: -

The company is actively involved in smart metering projects, with three in progress and a healthy order book in the water space, including supply, STP, and WTP projects.

- The gel-driven projects are underway, with 43% completed by December end, and another 5% expected to be finished by March end.

Future Outlook:

- The gel-driven projects are underway, with 43% completed by December end, and another 5% expected to be finished by March end.

-

NCC is exploring new projects in the water space due to increased budget allocations for the water department.

-

The company is also heavily involved in smart metering and is assessing IT architecture and connectivity aspects for successful project implementation.

Other Points: -

The company has received NHAI claim money in their SPV and has made progress with documentation. They have also received a portion of the investment in the Vizag Urban project and expect additional installments before March and in April 2024.

-

NCC is in advanced discussions with SBI Caps and SBI for debt financing and has mobilization advances in their contracts, ensuring funding is not a problem.

9 Likes

Good Q3 result from NCC.

Good ramp-up in execution.

On track to deliver a PAT of ~1300cr in FY25 ![]()

Based on expected FY25 PAT, stock trades v at quite cheap valuations at ~10x next year earnings !!

Stock offers good value with huge upside visible over the next 2 yrs as earnings accelerate going forward.

4 Likes

I won’t read too much into management commentary. Majority of the times management projections 2-3 year out seldom come true especially in a highly cyclical sector.

The problem for NCC (and hence lower valuations) is their operating margins. At 10% it’s much lower than peer group. PNR Infra, KNR Constructions have been delivering EBITDA margins in the range of 20-25% for last several years. Not sure where the problem is. Having a big order book is not an issue. One can bid lower to pick up new orders.

Till they can fix their revenue mix to gear it towards high margin business, rerating to me doesn’t look possible.

1 Like

Not sure what you are talking about in terms of market not rerating it. NCC PE multiple is already higher vs KNR and PNC Infratech both. Additionally its 100% up from May’21 levels whereas KNR is flat and PNC was also flat until Dec’23.

1 Like

If we exclude the claims in Q2, the 9M profits are at 650 Crores. With another 250 crores profits (estimate) in Q4, the total profit for current fiscal should be around 900 crores, which results in an EPS of Rs. 15 per share. At CMP of 225, it is 15 PE for FY 24 numbers

Not sure if that is long term cyclical peak PE or can it be further re-rated based on how orders flow in post elections.

2 Likes

The debt of NCC is continuously on a downward trajectory due to strong cashflows where as the KNR debt is stagnant.

Strong order book of more than 70000 crore

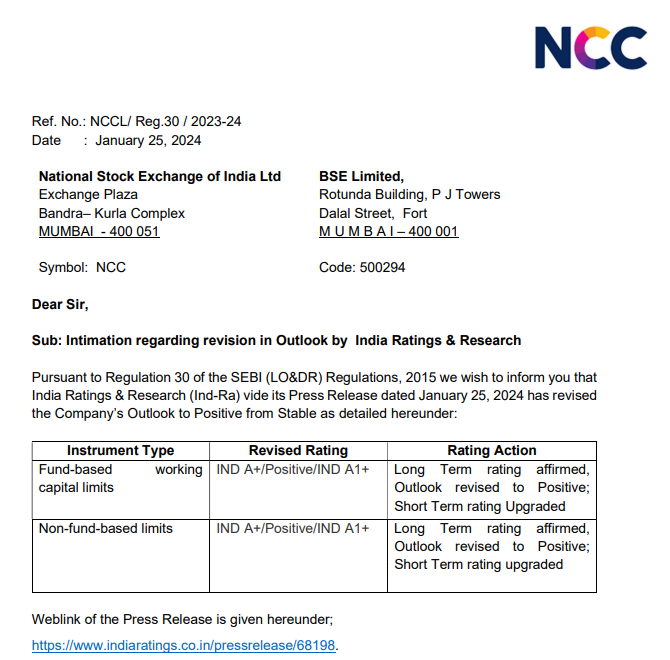

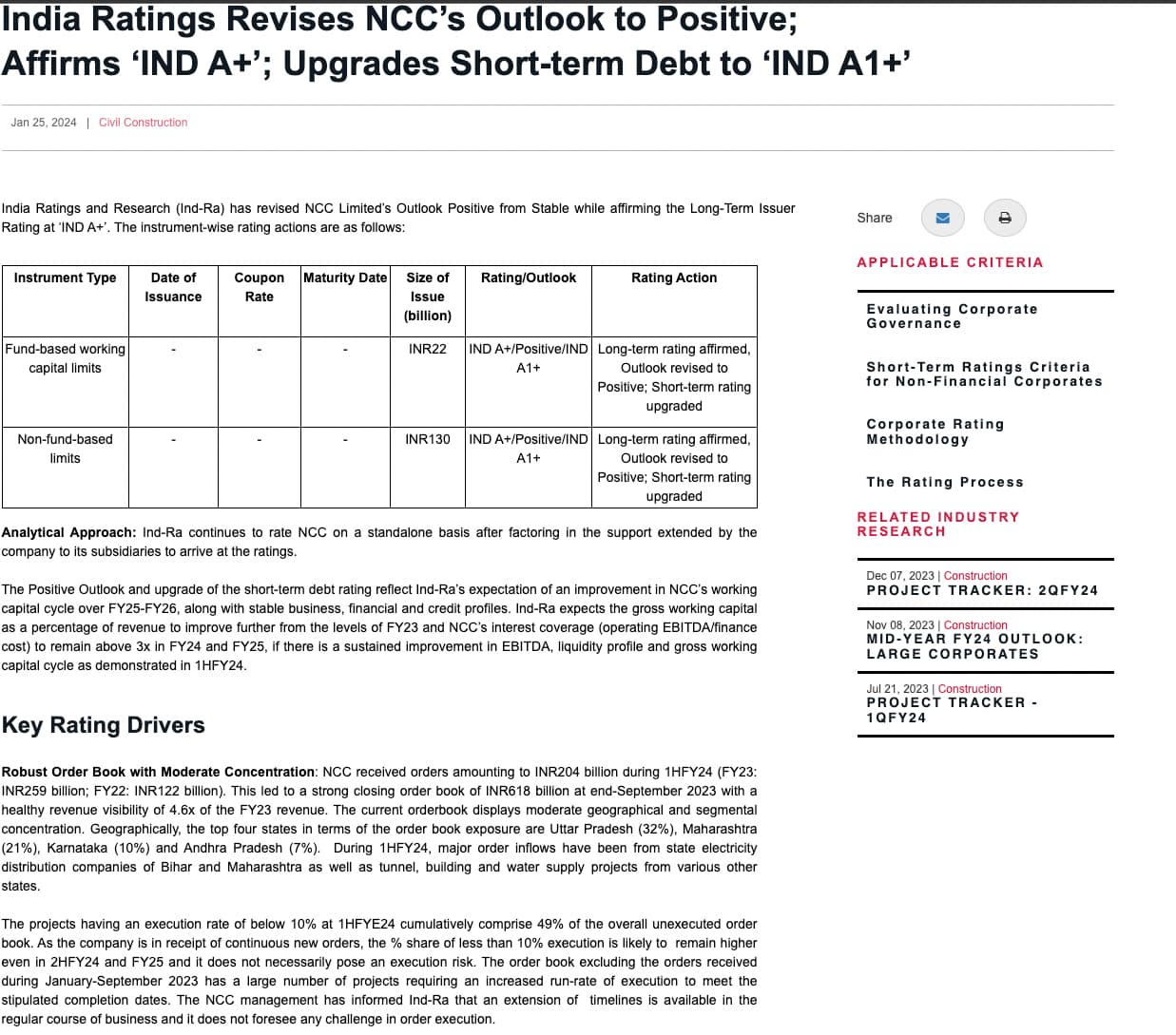

and rating upgrade by rating agency leads to the rerating of PE of the company.

1 Like