2 Likes

Says infra theme is going to play for next 4-5 decades ![]()

1 Like

Rerating in the stock has already happened in my view. Current price-earning multiple is 40% higher than historical averages.

On adjusted fy24e numbers, the current market price reflects just 15 PE. Is that already high for a company like NCC?

2 Likes

Compared to 5, 10 year multiples (10-12), it’s definitely a premium of around 30%. Plus infra is a highly cyclical business so reratings don’t tend to be as dramatic as you may see in a, say, retail or technology business.

1 Like

At the same time, NCC is in a much better position than ever so far

They have consistently brought down the debt levels

They have sold off most of their non core business and are focusing primarily on core business (more than 90% of the revenue, the remaining in mines & realty)

Unlike the inefficient planning & execution of 2007/08 infrastructure projects from the then government, the current govt seems to be good in planning & execution of the same (at least so far and I hope it continues at least for next 5 - 10 years

If NCC had a PE multiple of around 14 earlier, should the above mentioned positives warrant a better valuation multiple?

(Al though, I personally feel Price to book is a better mechanism for EPC companies as they don’t have much assets)

3 Likes

The market seems to be clearly rerating NCC here. 15 year high broken today. Strong order book, low debt, great execution and 2-3 year revenue visibility. See 350 on the cards soon

3 Likes

Smart meters - NCC is doing that too

3 Likes

Fresh orders worth 1462 crores received by company in the month of Feb.

4 Likes

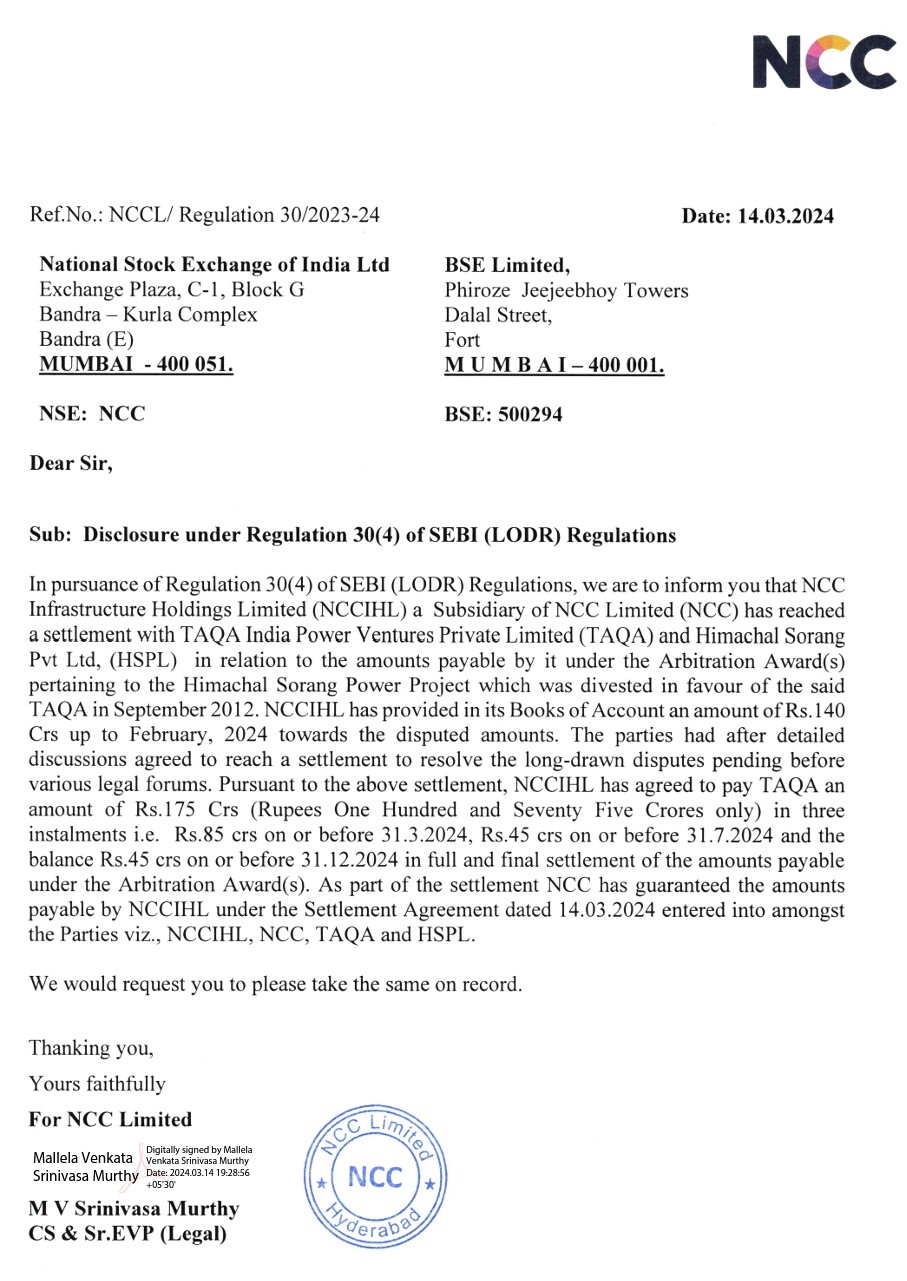

Will the difference of 35 crores be (negatively) reflected in the Q4 P&L or is it an impact on the balance sheet only?

3 Likes

NCC Ltd has donated total Rs. 60 crores through electoral bonds.

3 Likes

Why does the street value NCC the way it does? I think the other two EPC players undertake more complex projects but have far lower margins.

4 Likes

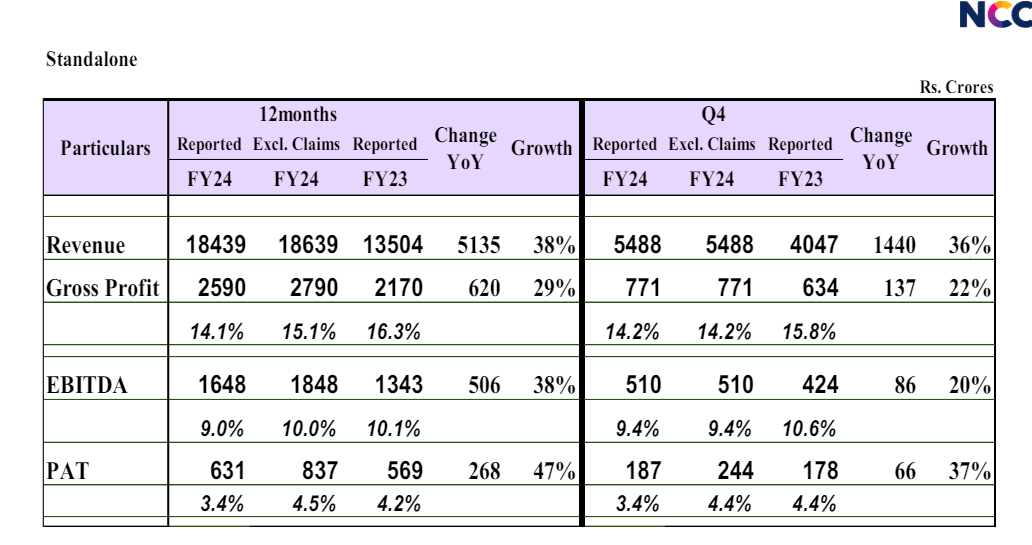

Good numbers from NCC. Excluding one-time exceptions, the net profit for the year is at 837 crores on standalone basis and around 890-920 crores consolidated.

For FY25, we can expect an EPS close to 18-20 I guess

3 Likes

A brokerage report from JM Financials says the RE arm - NCC Urban has a good land bank. Does anyone know the details of the total land bank area, location and market value of the same?

1 Like

Both KEC and Kalapatru are way overvalued while NCC in my view is perfectly valued (may be a tad higher). Again short term stock price movement don’t always reflect the value of a business.

We are in yet another infra bull run and any company associated with infra development is getting rerated by the market. So one shouldn’t really read too much into valuations.

3 Likes

Does anyone know details of the issues that NCC had with the AP govt few years ago?

Now TDP will be in power for next 5 years and Chandrababu Naidu is always pro-growth. Due to alliance compulsion, Modi will help CBN to grow the state of AP. Does this brighten up the fortunes of NCC’s business in the state of AP (old issues getting resolved and new orders coming up, especially infra growth of capital (to be) Amaravati?

1 Like

Anyone that has been tracking NCC since a long time, could you explain how post 2019 the cash conversion cycle went from `126 crore to -126 crore, and it has been negative ever since.What explains a change this drastic?

ICICI securities had given a price target of Rs. 320 in the month of May and revised it to Rs. 395 in just one month. The reason: Tailwinds due to TDP winning AP elections and the prospects of infra growth what CBN had promised in his previous term (some of the projects that NCC got during TDP regime in 2014-2019 got cancelled by YSR Party and collections etc.,)

Leaving aside the price targets, I am just curious to know if it is reasonable to have high expectations on the infra growth in Amaravati and rest of AP just because TDP is back in power that warrants a huge increase in price targets in just one month?

When the same TDP was in power from 2014 - 19, was there so much growth that actually happened on the infra side (or most of it was preparatory work like purchasing land, finalizing plans etc)?

1 Like

Does anyone know when the dividend will be paid?

Does anyone know the reason behind subdued topline growth (yoy) and de-growth (qoq)?

Q2 of last year also had an one-time net impact of 200 crores. If we consider that, then topline de-growth yoy as well.

Share prices have gone up looking at the non-adjusted numbers and see the profits have doubled.