Wanting to enter the stock what are the good levels where I can add this to my Portfolio?

I understand the RDSS and little bit of AMI. But these are related to running of the power sector. Could not connect these with NCC, who are into infrastructure building.

If you investment horizon is, like me, 5 years or more, then anytime is a good entry time.

NCC will source meters, set up the required infrastructure including installation of the meters, operate them for the mentioned number of years and handover to discoms, while getting paid by them all along (I don’t know much about how this will be funded, the monthly or annual revenue & margins for this project)

Genus will also do the above but they won’t buy meters as they produce it themselves and hence may have slightly better margins. Additionally, they will also supply such advance meters for pure EPC companies like NCC, GMR Infra etc

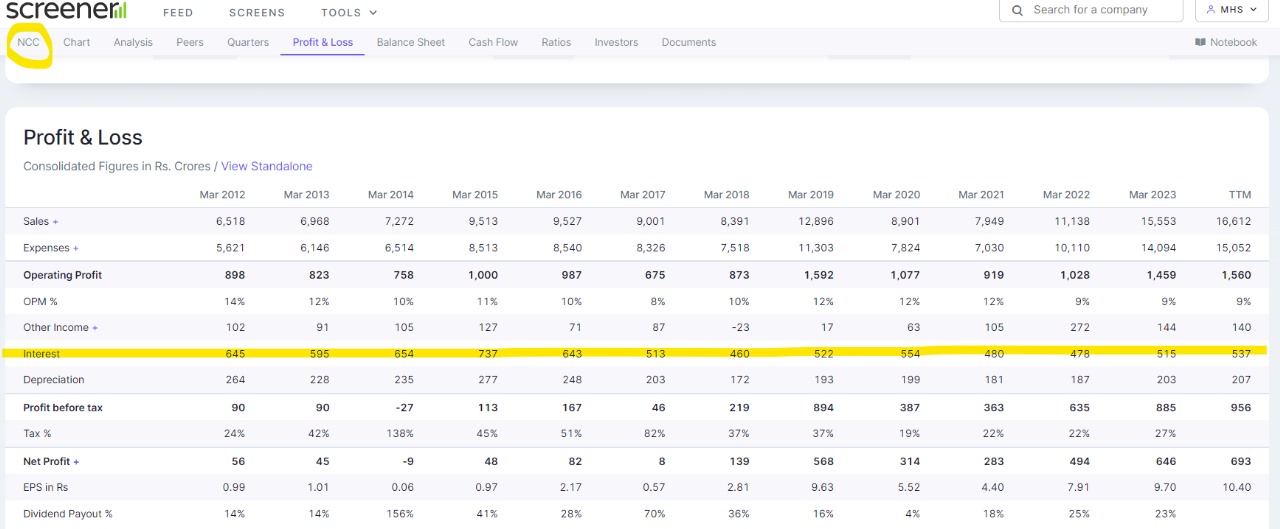

Just glanced NCC numbers : They reduced significant debt over the years, but One thing intriguing and very difficult to understand why is the interest payments almost similar after significant reduction, any idea???

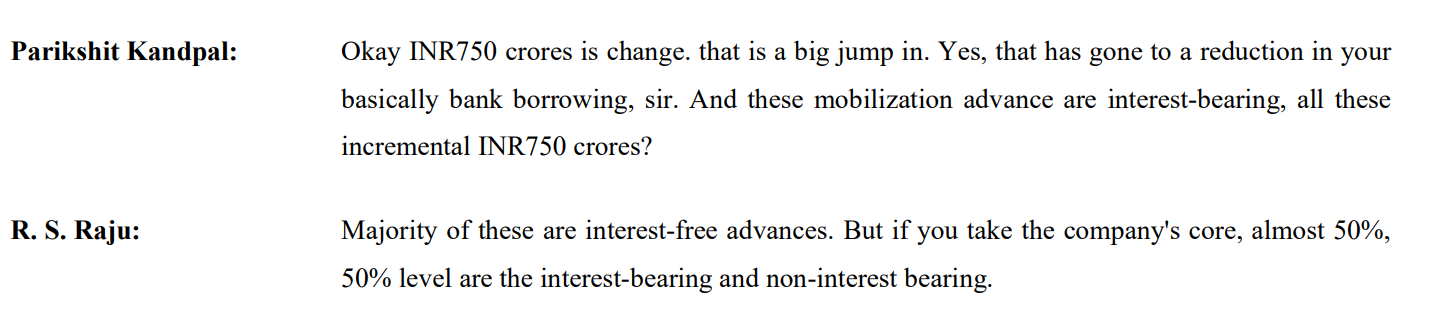

The interest cost includes interest on working capital demand loan, interest on term loan, interest on mobilization advance, commission and finance charges. The borrowings have gone down, by using mobilization advances from customer. However ,the company have to pay interest on 50% of these mobilization advances so overall the interest payment stayed at same level or gone up as per prevailing interest rate.

The mobilization advances are not put under borrowing in balance sheet, but under other liabilities.

The snapshot from May 2023 concall:

The customer advances have increased a lot in recent years, snapshot from screener:

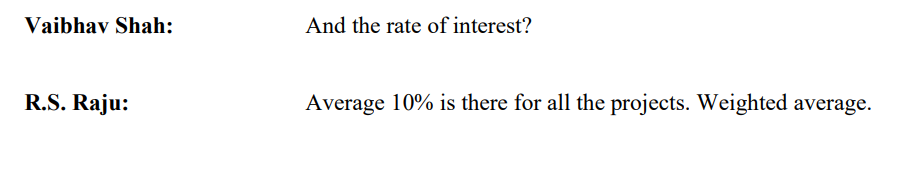

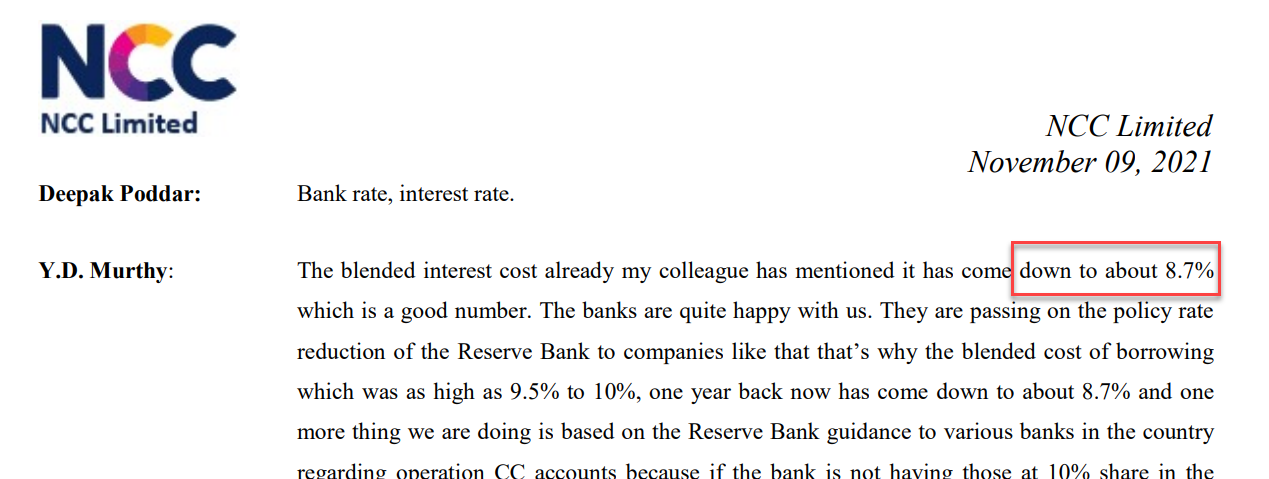

Also the interest rates have gone up from average of 8.7% in year 2021 to average of 10% in year 2023. Information available in all the concalls. the snapshot from Aug 2023 concall below:

.

The snapshot from Nov 2021:

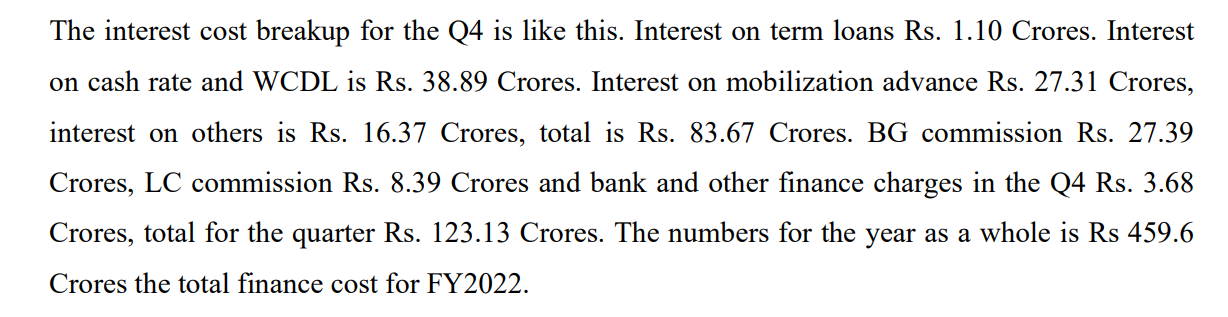

The breakdown of the interest cost below from 1 of the concall for year 2022:

4 Likes

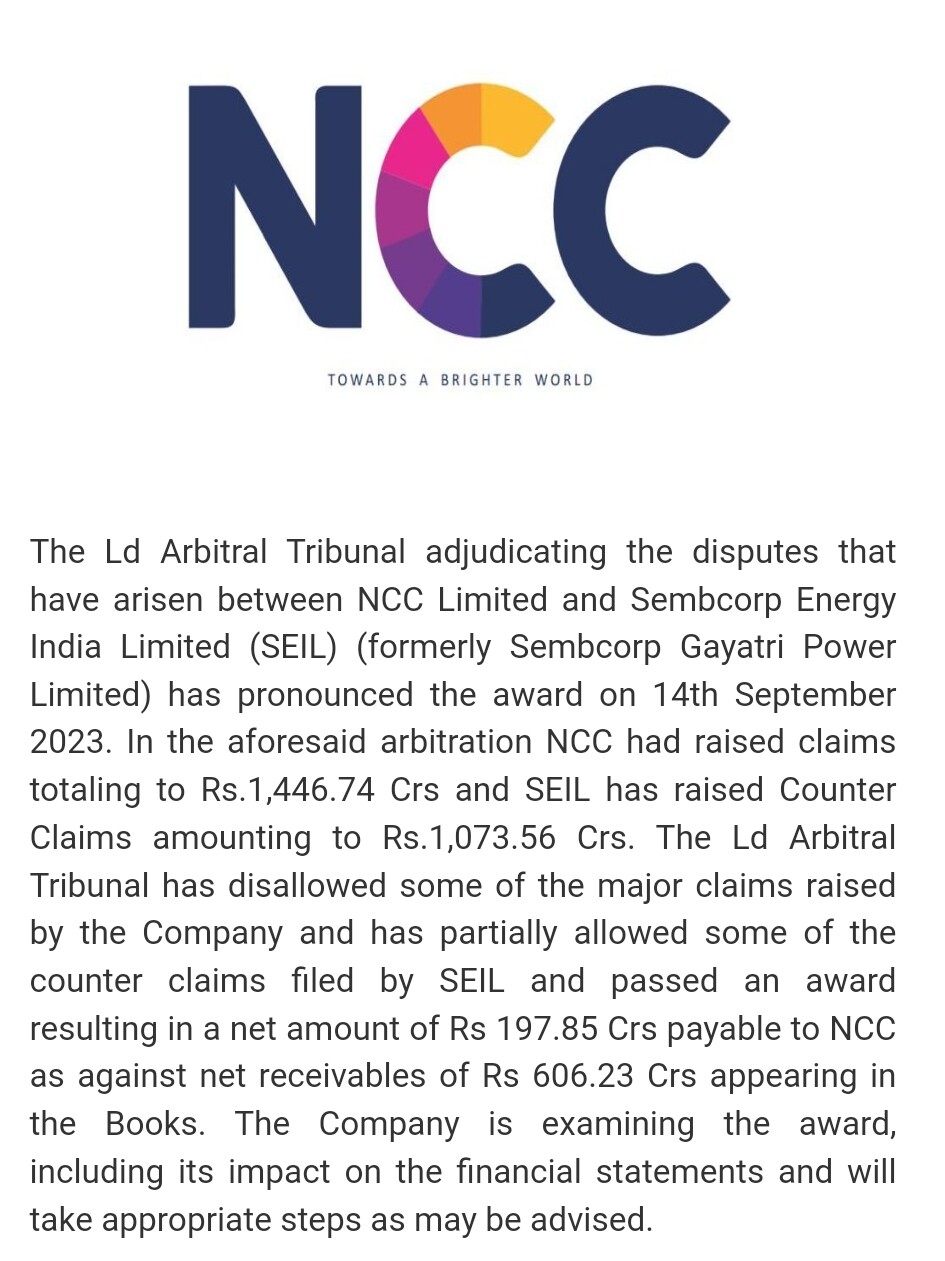

Sembcorp case - Is the arbitration amount on expected lines? I was of the view it would be around 500/600+ Crores

1 Like

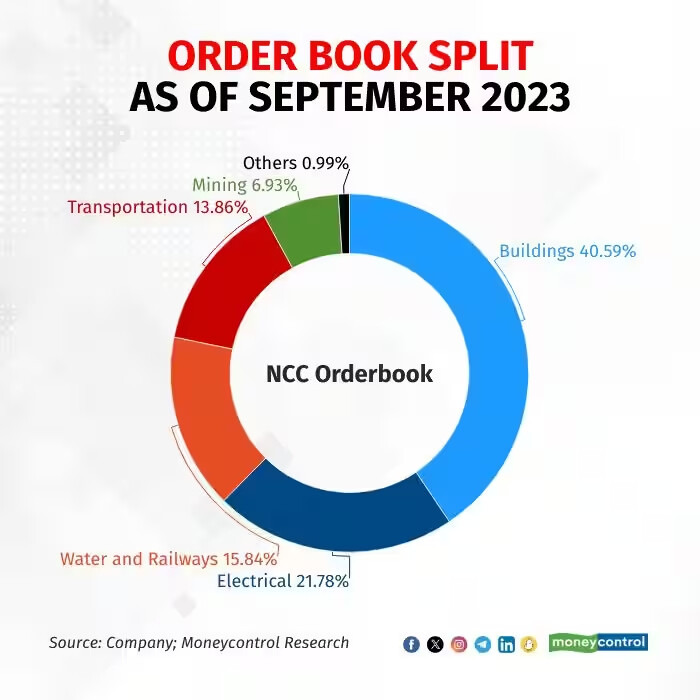

This is official now. NCC has received this order along with JKumars and NCC’s share is 3200 Crores.

As on today (Sep 22), the order book is at 68000 Crores (minus the revenue being booked in the current Q2 quarter)

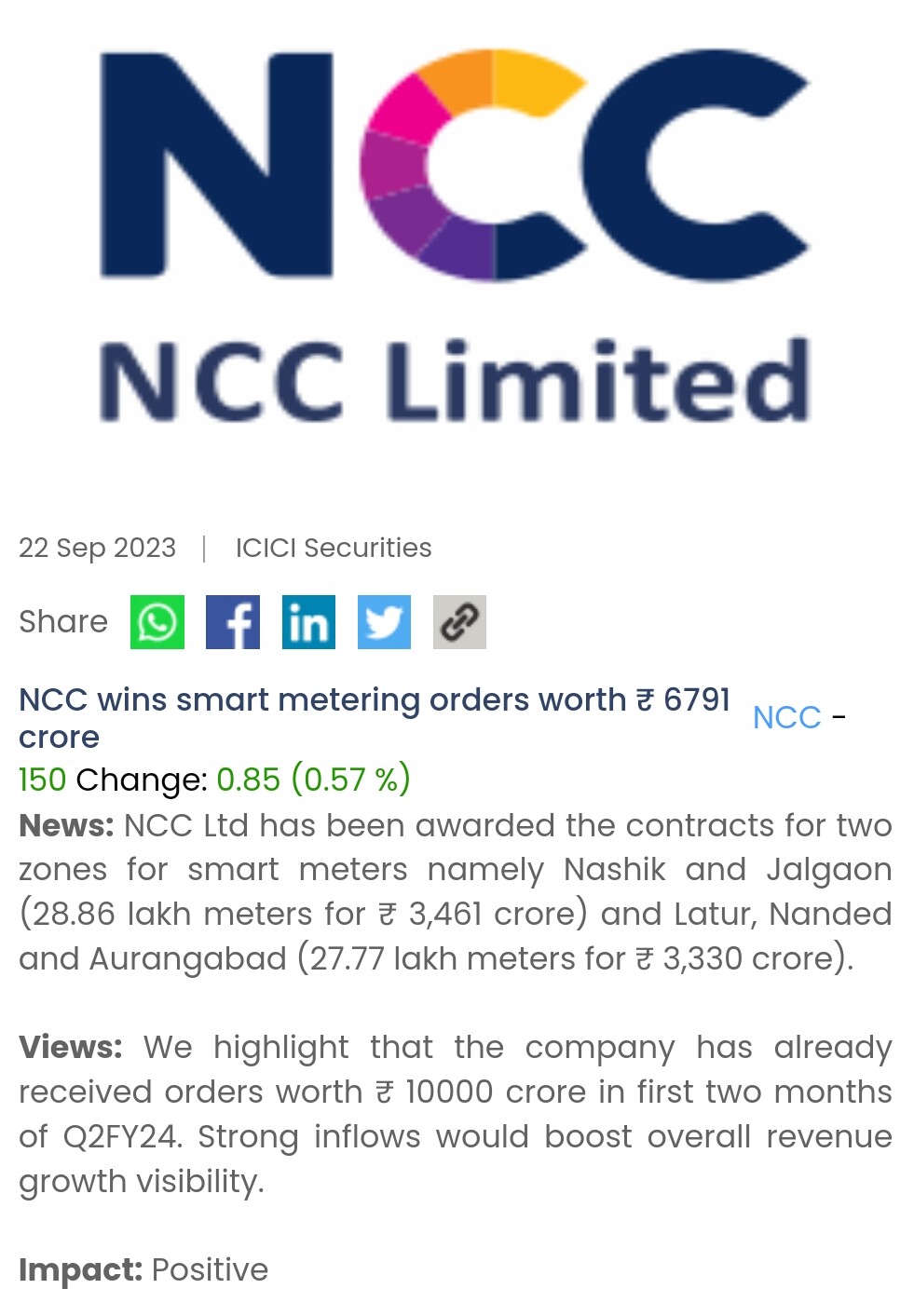

Looks like NCC has secured additional orders worth 6700 crores on advanced metering projects…it is not official news yet but it’s being reported in some websites including ICICI direct. If true, then order inflow in this fiscal YTD is at 28000 crores

Hi - Does anyone have any information on where this stands? Given the low promoter holding and they issuing warrants just prior to big win, want to reconfirm on corporate governance before investing. Thanks

1 Like

NCC has everything going good for it - Increase in

Order inflow & backlog

Revenue

Profits

Govt spending on various infra projects

It is still trading at reasonable valuation

While so many stocks have moved up very high, NCC hasn’t moved up to that extent - inspite of all the good news on business front

Can anyone share inputs on the possible reasons? Is it possible that lot of accumulation is going on?

The project completion takes time to reflect in its books, as they are long duration projects generally.

It will require adequate time for it to deserve a higher valuation multiples.

As its particular a construction company, their efficiency of operations needs to be tracked on quarter to quarter basis, so it might be a stock story where allocation by institutions will rise on QoQ basis, as I don’t feel any major institution to make a lump sum purchase currently.

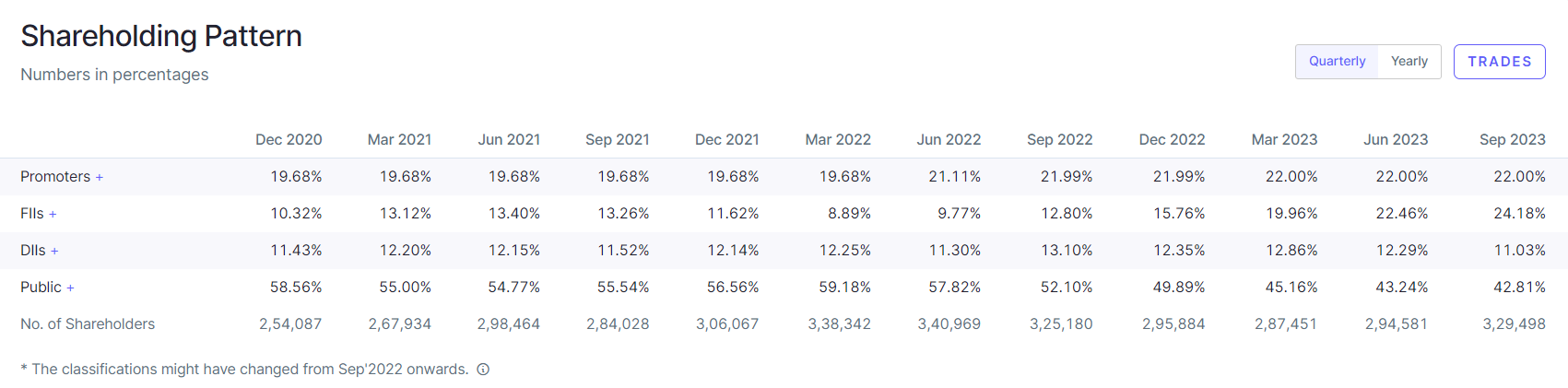

SHP from Screener:

From Mar 2022 till date, FII & DII have increased their holding from 21% to 35%. The share price has more than doubled (from 70ish to 150ish) in the mean time.

3 Likes

Ya exactly what I meant

If they had full conviction then there wouldn’t be change in institutional stake, with them buying in one single tranch

As the business is improving and proving itself, it is therefore the increase in stake

No institution will ever risk investmenting by lumpsum

Well, as long as the earnings are sustained and the valuation is not re-rated, all you need is the patience.

4 Likes

True. Still holding and adding small quantity once in a while. What baffles me is the way so many stocks have gone up with & without justification of fundamentals, while this one moves very slow. Makes me wonder if this is artificially done for the sake of accumulation

2 Likes

In so many stocks, there are Khelo India Khelo movements. Have patience in your convictions as long as your thesis is right. Patience is like a magnet for your ultimate returns.

No order inflow in October. They haven’t reported order intake for December too, at least so far